42 Prepare Operating Budgets

Patty Graybeal

Operating budgets are a primary component of the master budget and involve examining the expectations for the primary operations of the business. Assumptions such as sales in units, sales price, manufacturing costs per unit, and direct material needed per unit involve a significant amount of time and input from various parts of the organization. It is important to obtain all of the information, however, because the more accurate the information, the more accurate the resulting budget, and the more likely management is to effectively monitor and achieve its budget goals.

Individual Operating Budgets

In order for an organization to align the budget with the strategic plan, it must budget for the day-to-day operations of the business. This means the company must understand when and how many sales will occur, as well as what expenses are required to generate those sales. In short, each component—sales, production, and other expenses—must be properly budgeted to generate the operating budget components and the resulting pro-forma budgeted income statement.

The budgeting process begins with the estimate of sales. When management has a solid estimate of sales for each quarter, month, week, or other relevant time period, they can determine how many units must be produced. From there, they determine the expenditures, such as direct materials necessary to produce the units. It is critical for the sales estimate to be accurate so that management knows how many units to produce. If the estimate is understated, the company will not have enough inventory to satisfy customers, and they will not have ordered enough material or scheduled enough direct labor to manufacture more units. Customers may then shop somewhere else to meet their needs. Likewise, if sales are overestimated, management will have purchased more material than necessary and have a larger labor force than needed. This overestimate will cause management to have spent more cash than was necessary.

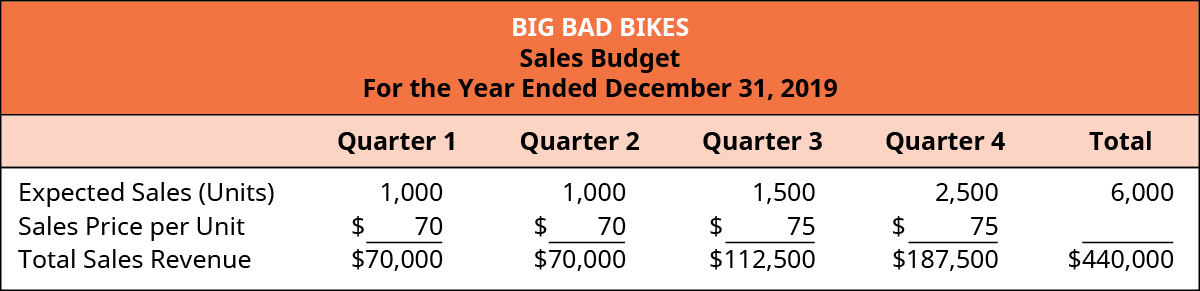

Sales Budget

The sales budget details the expected sales in units and the sales price for the budget period. The information from the sales budget is carried to several places in the master budget. It is used to determine how many units must be produced as well as when and how much cash will be collected from those sales.

For example, Big Bad Bikes used information from competitor sales, its marketing department, and industry trends to estimate the number of units that will be sold in each quarter of the coming year. The number of units is multiplied by the sales price to determine the sales by quarter as shown in (Figure).

The sales budget leads into the production budget to determine how many units must be produced each week, month, quarter, or year. It also leads into the cash receipts budget, which will be discussed in Prepare Financial Budgets.

Production Budget

Estimating sales leads to identifying the desired quantity of inventory to meet the demand. Management wants to have enough inventory to meet production, but they do not want too much in the ending inventory to avoid paying for unnecessary storage. Management often uses a formula to estimate how much should remain in ending inventory. Management wants to be flexible with its budgeting, wants to create budgets that can grow or shrink as needed, and needs to have inventory on hand. So the amount of ending inventory often is a percentage of the next week’s, month’s, or quarter’s sales.

In creating the production budget, a major issue is how much inventory should be on hand. Having inventory on hand helps the company avoid losing a customer because the product isn’t available. However, there are storage costs associated with holding inventory as well as having a lag time between paying to manufacture a product and receiving cash from selling that product. Management must balance the two issues and determine the amount of inventory that should be available.

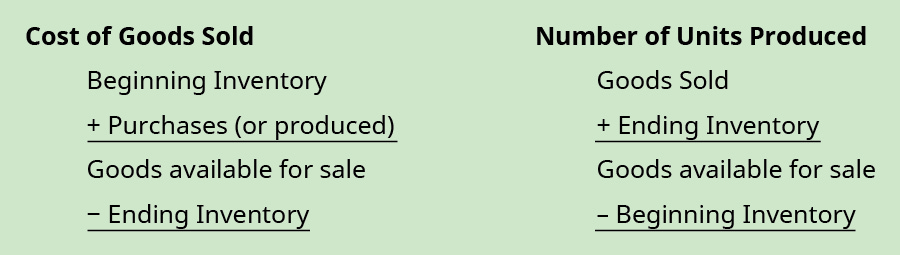

When determining the number of units needed to be produced, start with the estimated sales plus the desired ending inventory to derive the maximum number of units that must be available during the period. Since the number of units in beginning inventory are already produced, subtracting the beginning inventory from the goods available results in the number of units that need to be produced.

After management has estimated how many units will sell and how many units need to be in ending inventory, it develops the production budget to compute the number of units that need to be produced during each quarter. The formula is the reverse of the formula for the cost of goods sold.

The number of units expected to be sold plus the desired ending inventory equals the number of units that are available. When the beginning inventory is subtracted from the number of units available, management knows how many units must be produced during that quarter to meet sales.

In a merchandising firm, retailers do not produce their inventory but purchase it. Therefore, stores such as Walmart do not have raw materials and instead substitute the number of units to be purchased in place of the number of units to be produced; the result is the merchandise inventory to be purchased.

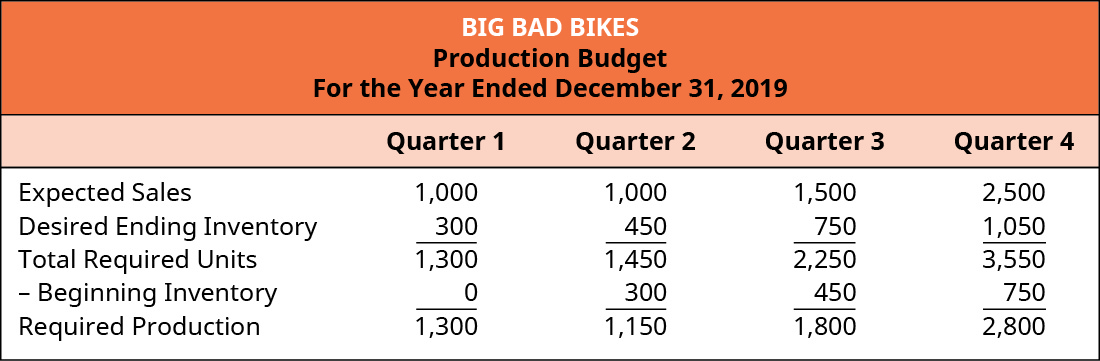

To illustrate the steps in developing a production budget, recall that Big Bad Bikes is introducing a new product that the marketing department thinks will have strong sales. For new products, Big Bad Bikes requires a target ending inventory of 30% of the next quarter’s sales. Unfortunately, they were unable to manufacture any units before the end of the current year, so the first quarter’s beginning inventory is 0 units. As shown in (Figure), sales in quarter 2 are estimated at 1,000 units; since 30% is required to be in ending inventory, the ending inventory for quarter 1 needs to be 300 units. With expected sales of 1,000 units for quarter 2 and a required ending inventory of 30%, or 300 units, Big Bad Bikes needs to have 1,300 units available during the quarter. Since 1,300 units needed to be available and there are zero units in beginning inventory, Big Bad Bikes needs to manufacture 1,300 units, as shown in (Figure)

The ending inventory from one quarter is the beginning inventory for the next quarter and the calculations are all the same. In order to determine the ending inventory in quarter 4, Big Bad Bikes must estimate the sales for the first quarter of the next year. Big Bad Bikes’s marketing department believes sales will increase in each of the next several quarters, and they estimate sales as 3,500 for the first quarter of the next year and 4,500 for the second quarter of the next year. Thirty percent of 3,500 is 1,050, so the number of units required in the ending inventory for quarter 4 is 1,050.

The number of units needed in production for the first quarter of the next year provides information needed for other budgets such as the direct materials budget, so Big Bad Bikes must also determine the number of units needed in production for that first quarter. The estimated sales of 3,500 and the desired ending inventory of 1,350 (30% of the next quarter’s estimated sales of 4,500) determines that 4,850 units are required during the quarter. The beginning inventory is estimated to be 1,050, which means the number of units that need to be produced during the first quarter of year 2 is 3,800.

The number of units needed to be produced each quarter was computed from the estimated sales and is used to determine the quantity of direct or raw material to purchase, to schedule enough direct labor to manufacture the units, and to approximate the overhead required for production. It is also necessary to estimate the sales for the first quarter of the next year. The ending inventory for the current year is based on the sales estimates for the first quarter of the following year. From this amount, the production budget and direct materials budget are calculated and flow to the operating and cash budget.

Direct Materials Budget

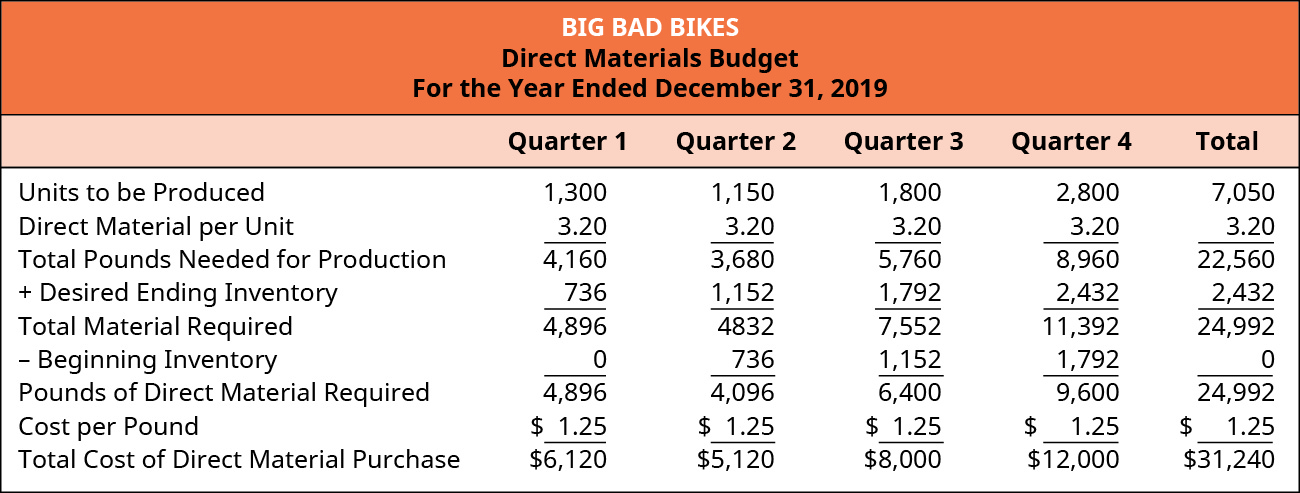

From the production budget, management knows how many units need to be produced in each budget period. Management is already aware of how much material it needs to produce each unit and can combine the direct material per unit with the production budget to compute the direct materials budget. This information is used to ensure the correct quantity of materials is ordered and the correct amount is budgeted for those materials.

Similar to the production budget, management wants to have an ending inventory available to ensure there are enough materials on hand. The direct materials budget illustrates how much material needs to be ordered and how much that material costs. The calculation is similar to that used in the production budget, with the addition of the cost per unit.

If Big Bad Bikes uses 3.2 pounds of material for each trainer it manufactures and each pound of material costs $1.25, we can create a direct materials budget. Management’s goal is to have 20% of the next quarter’s material needs on hand as the desired ending materials inventory. Therefore, the determination of each quarter’s material needs is partially dependent on the following quarter’s production requirements. The desired ending inventory of material is readily determined for quarters 1 through 3 as those needs are based on the production requirements for quarters 2 through 4. To compute the desired ending materials inventory for quarter 4, we need the production requirements for quarter 1 of year 2. Recall that the number of units to be produced during the first quarter of year 2 is 3,800. Thus, quarter 4 materials ending inventory requirement is 20% of 3,800. That information is used to compute the direct materials budget shown in (Figure).

Management knows how much the materials will cost and integrates this information into the schedule of expected cash disbursements, which will be shown in Prepare Financial Budgets. This information will also be used in the budgeted income statement and on the budgeted balance sheet. With 6,000 units estimated for sale, 3.2 pounds of material per unit, and $1.25 per pound, the direct materials used represent $24,000 of the cost of goods sold. The remaining $7,240 is included in ending inventory as units completed and raw material.

Direct Labor Budget

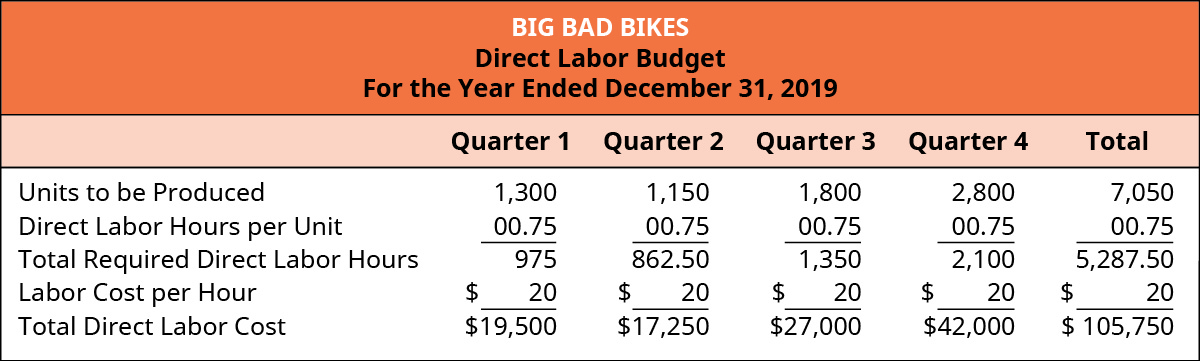

Management uses the same information in the production budget to develop the direct labor budget. This information is used to ensure that the proper amount of staff is available for production and that there is money available to pay for the labor, including potential overtime. Typically, the number of hours is computed and then multiplied by an hourly rate, so the total direct labor cost is known.

If Big Bad Bikes knows that they need 45 minutes or 0.75 hours of direct labor for each unit produced, and the labor rate for this type of manufacturing is $20 per hour, the computation for direct labor simply begins with the number of units in the production budget. As shown in (Figure), the number of units produced each quarter multiplied by the number of hours per unit equals the required direct labor hours needed to be scheduled in order to meet production needs. The total number of hours is next multiplied by the direct labor rate per hour, and the labor cost can be budgeted and used in the cash disbursement budget and operating budget illustrated in Prepare Financial Budgets.

The direct labor of $105,750 will be apportioned to the budgeted income statement and budgeted balance sheet. With 0.75 hours of direct labor per unit and $20 per direct labor hour, each unit will cost $15 in direct labor. Of the 7,050 units produced, 6,000 units will be sold, so $90,000 represents the labor portion of the cost of goods sold and will be shown on the income statement, while the remaining $15,750 will be the labor portion of ending inventory and will be shown on the balance sheet.

Manufacturing Overhead Budget

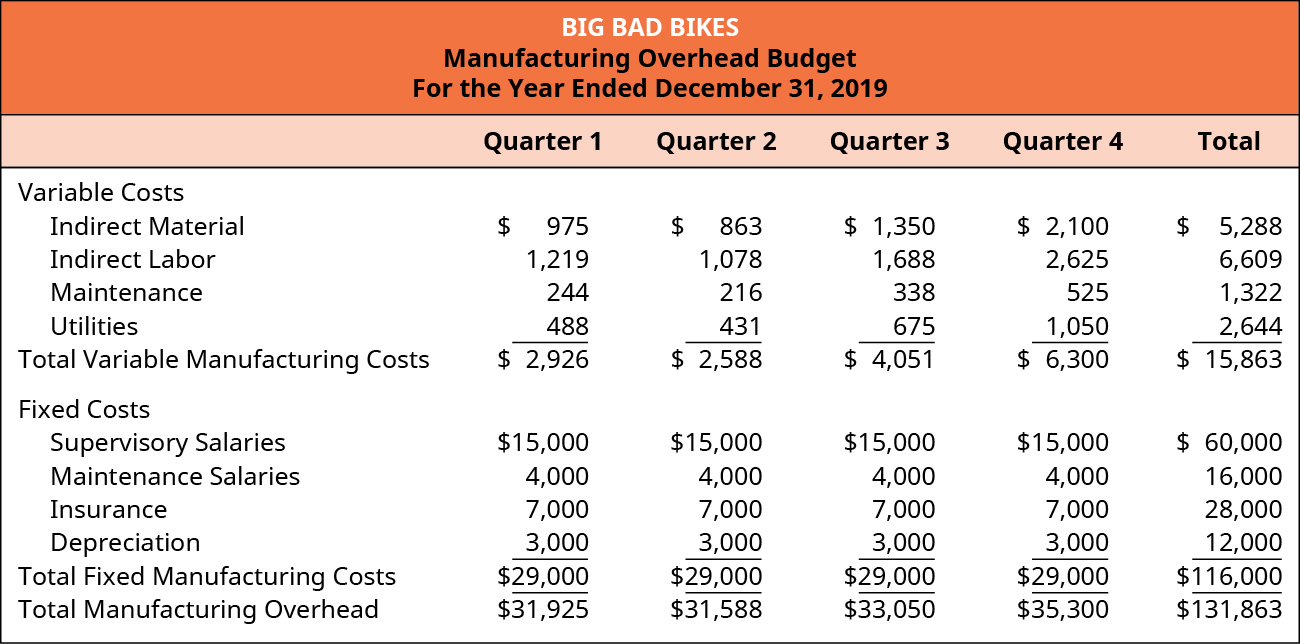

The manufacturing overhead budget includes the remainder of the production costs not covered by the direct materials and direct labor budgets. In the manufacturing overhead budgeting process, producers will typically allocate overhead costs depending upon their cost behavior production characteristics, which are generally classified as either variable or fixed. Based on this allocation process, the variable component will be treated as occurring proportionately in relation to budgeted activity, while the fixed component will be treated as remaining constant. This process is similar to the overhead allocation process you learned in studying product, process, or activity-based costing.

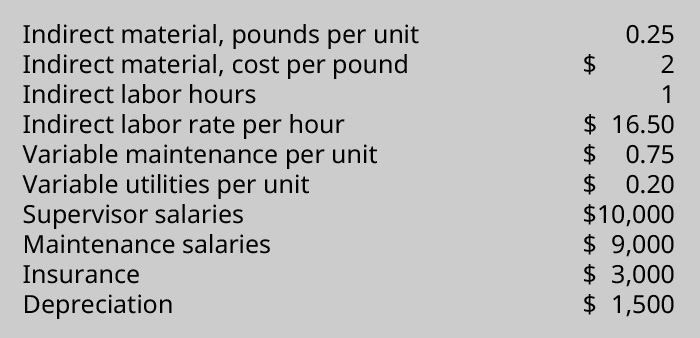

For Big Bad Bikes to create their manufacturing overhead budget, they first determine that the appropriate driver for assigning overhead costs to products is direct labor hours. The overhead allocation rates for the variable overhead costs are: indirect material of $1.00 per hour, indirect labor of $1.25 per hour, maintenance of $0.25 per hour, and utilities of $0.50 per hour. The fixed overhead costs per quarter are: supervisor salaries of $15,000, fixed maintenance salaries of $4,000, insurance of $7,000, and depreciation expenses of $3,000.

Given the direct labor hours for each quarter from the direct labor budget, the variable costs are the number of hours multiplied by the variable overhead application rate. The fixed costs are the same for each quarter, as shown in the manufacturing overhead budget in (Figure).

The total manufacturing overhead cost was $131,863 for 7,050 units, or $18.70 per unit (rounded). Since 6,000 units are sold, $112,200 (6,000 units × $18.70 /unit) will be expensed as cost of goods sold, while the remaining $19,663 will be part of finished goods ending inventory.

Sales and Administrative Expenses Budget

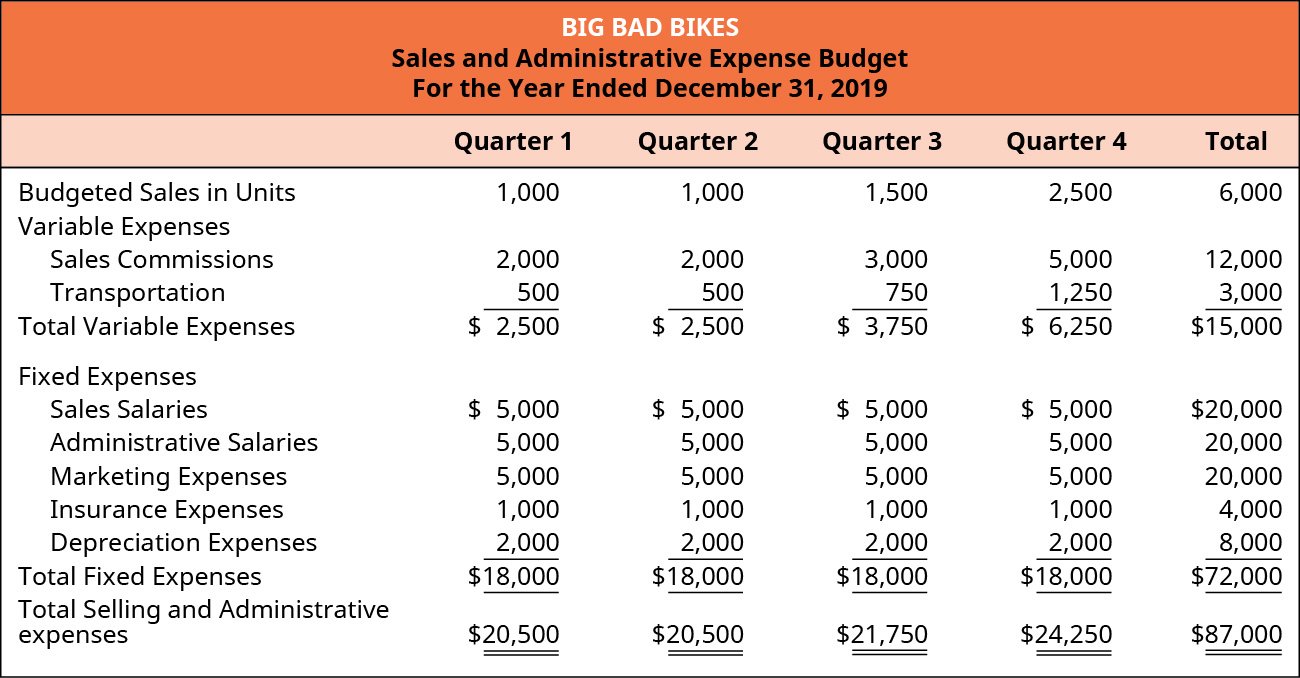

The direct materials budget, the direct labor budget, and the manufacturing overhead budget plan for all costs related to production, while the selling and administrative expense budget contains a listing of variable and fixed expenses estimated to be incurred in all areas other than production costs. While this one budget contains all nonmanufacturing expenses, in practice, it actually comprises several small budgets created by managers in sales and administrative positions. All managers must follow the budget, but setting an appropriate budget for selling and administrative functions is complicated and is not always thoroughly understood by managers without a background in managerial accounting.

If Big Bad Bikes pays a sales commission of $2 per unit sold and a transportation cost of $0.50 per unit, they can use these costs to put together their sales and administrative budget. All other costs are fixed costs per quarter: sales salaries of $5,000; administrative salaries of $5,000; marketing expenses of $5,000; insurance of $1,000; and depreciation of $2,000. The sales and administrative budget is shown in (Figure), along with the budgeted sales used in the computation of variable sales and administrative expenses.

Only manufacturing costs are treated as a product cost and included in ending inventory, so all of the expenses in the sales and administrative budget are period expenses and included in the budgeted income statement.

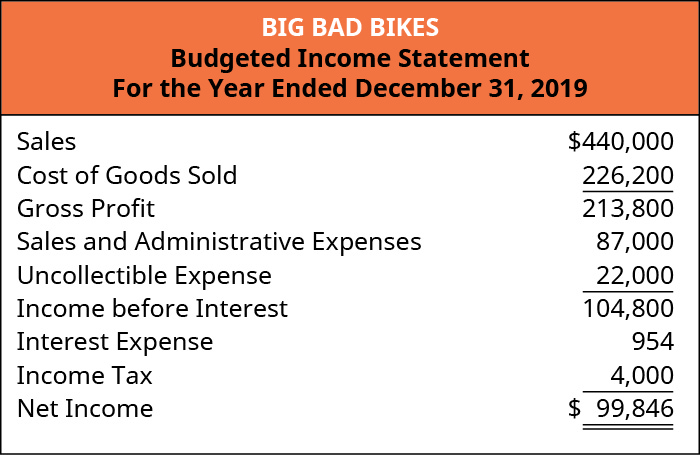

Budgeted Income Statement

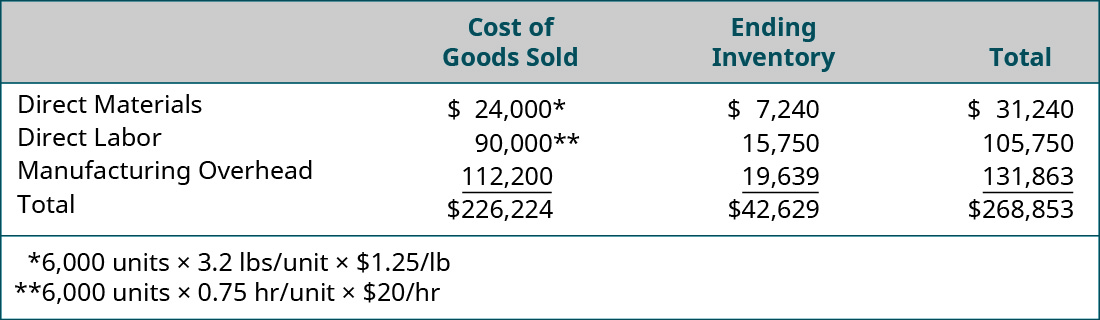

A budgeted income statement is formatted similarly to a traditional income statement except that it contains budgeted data. Once all of the operating budgets have been created, these costs are used to prepare a budgeted income statement and budgeted balance sheet. The manufacturing costs are allocated to the cost of goods sold and the ending inventory.

Big Bad Bikes uses the information on direct materials ((Figure)), direct labor ((Figure)), and manufacturing overhead ((Figure)) to allocate the manufacturing costs between the cost of goods sold and the ending work in process inventory, as shown in ((Figure)).

Once they perform this allocation, the budgeted income statement can be prepared. Big Bad Bikes estimates an interest of $954. It also estimates that $22,000 of its income will not be collected and will be reported as uncollectible expense. The budgeted income statement is shown in (Figure).

Which error has the potential to cause more problems with the budgeted balance sheet: overstating sales or understating the cash collected?

Key Concepts and Summary

- The sales budget is the first budget developed, and the estimated sales in turn guide the production budget.

- The production budget shows the quantity of goods produced for each time period and leads to computing when and how much direct material needs to be ordered, when and how much labor needs to be scheduled, and when and how much manufacturing overhead needs to be planned.

- The sales and administrative budget plans for the nonmanufacturing expenses.

- All operating budgets combine to develop the budgeted income statement.

(Figure)Which of the operating budgets is prepared first?

- production budget

- sales budget

- cash received budget

- cash payments budget

(Figure)The direct materials budget is prepared using which budget’s information?

- cash payments budget

- cash receipts budget

- production budget

- raw materials budget

C

(Figure)Which of the following is not an operating budget?

- sales budget

- production budget

- direct labor budget

- cash budget

(Figure)Which of the following statements is not correct?

- The sales budget is computed by multiplying estimated sales by the sales price.

- The production budget begins with the sales estimated for each period.

- The direct materials budget begins with the sales estimated for each period.

- The sales budget is typically the first budget prepared.

C

(Figure)The units required in production each period are computed by which of the following methods?

- adding budgeted sales to the desired ending inventory and subtracting beginning inventory

- adding beginning inventory, budgeted sales, and desired ending inventory

- adding beginning inventory to budgeted sales and subtracting desired ending inventory

- adding budgeted sales to the beginning inventory and subtracting the desired ending inventory.

(Figure)What information is necessary for the operating budgets?

Operating budgets plan the primary operations of the business and need accurate information in order to provide accurate planning. Assumptions such as sales in units, sales price, desired ending inventory in units, manufacturing costs per unit, which include direct material needed per unit, desired direct materials ending inventory, amount of direct labor hours and rate, and the overhead required for production and managing the company.

(Figure)What operating budget exists for manufacturing but not for a retail company?

(Figure)Blue Book printing is budgeting sales of 25,000 units and already has 5,000 in beginning inventory. How many units must be produced to also meet the 7,000 units required in ending inventory?

(Figure)How many units are in beginning inventory if 32,000 units are budgeted for sales, 35,000 units are produced, and the desired ending inventory is 9,000 units?

(Figure)Navigator sells GPS trackers for $50 each. It expects sales of 5,000 units in quarter 1 and a 5% increase each subsequent quarter for the next 8 quarters. Prepare a sales budget by quarter for the first year.

(Figure)One Device makes universal remote controls and expects to sell 500 units in January, 800 in February, 450 in March, 550 in April, and 600 in May. The required ending inventory is 20% of the next month’s sales. Prepare a production budget for the first four months of the year.

(Figure)Sunrise Poles manufactures hiking poles and is planning on producing 4,000 units in March and 3,700 in April. Each pole requires a half pound of material, which costs $1.20 per pound. The company’s policy is to have enough material on hand to equal 10% of the next month’s production needs and to maintain a finished goods inventory equal to 25% of the next month’s production needs. What is the budgeted cost of purchases for March?

(Figure)Given the following information from Rowdy Enterprises’ direct materials budget, how much direct materials needs to be purchased?

(Figure)Each unit requires direct labor of 2.2 hours. The labor rate is $11.50 per hour and next year’s direct labor budget totals $834,900. How many units are included in the production budget for next year?

(Figure)How many units are estimated to be sold if Skyline, Inc., has a planned production of 900,000 units, a desired beginning inventory of 160,000 units, and a desired ending inventory of 100,000 units?

(Figure)Lovely Wedding printing is budgeting sales of 32,000 units and already has 4,000 in beginning inventory. How many units must be produced to also meet the 6,000 units required in ending inventory?

(Figure)How many units are in beginning inventory if 32,000 units are budgeted for sales, 35,000 units are produced, and the desired ending inventory is 9,000 units?

(Figure)Barnstormer sells airplane accessories for $20 each. It expects sales of 120,000 units in quarter 1 and a 7% increase each subsequent quarter for the next 8 quarters. Prepare a sales budget by quarter for the first year.

(Figure)Rehydrator makes a nutrition additive and expects to sell 3,000 units in January, 2,000 in February, 2,500 in March, 2,700 in April, and 2,900 in May. The required ending inventory is 20% of the next month’s sales, and the beginning inventory on January 1 was 600 units. Prepare a production budget for the first four months of the year.

(Figure)Cloud Shoes manufactures recovery sandals and is planning on producing 12,000 units in March and 11,500 in April. Each sandal requires 1.2 yards if material, which costs $3.00 per yard. The company’s policy is to have enough material on hand to equal 15% of next month’s production needs and to maintain a finished goods inventory equal to 20% of the next month’s production needs. What is the budgeted cost of purchases for March?

(Figure)Given the following information from Power Enterprises’ direct materials budget, how much direct materials needs to be purchased?

(Figure)Each unit requires direct labor of 4.1 hours. The labor rate is $13.75 per hour and next year’s production is estimated at 75,000 units. What is the amount to be included in next year’s direct labor budget?

(Figure)How many units are estimated to be sold if Kino, Inc., has planned production of 750,000 units, a desired beginning inventory of 30,000 units, and a desired ending inventory of 45,000 units?

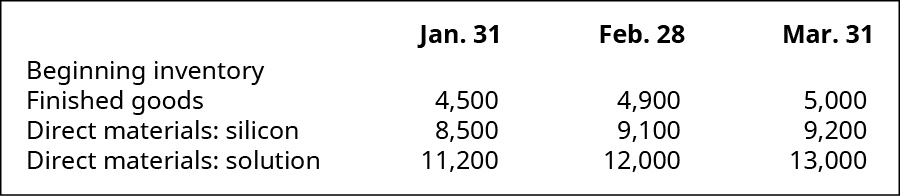

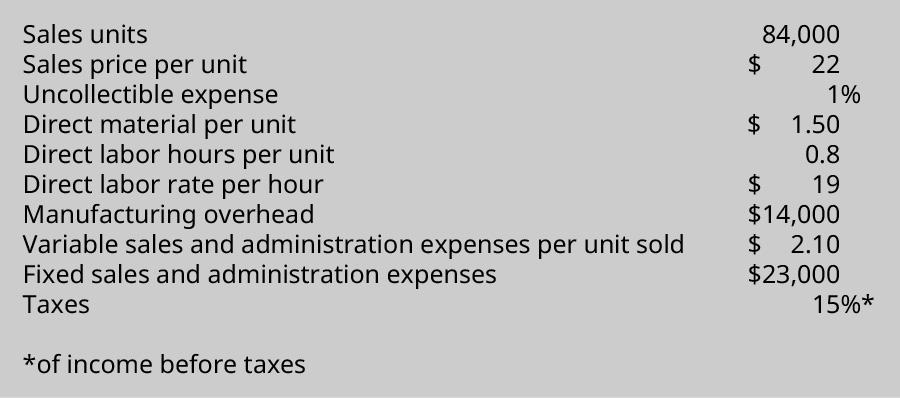

(Figure)Lens Junction sells lenses for $45 each and is estimating sales of 15,000 units in January and 18,000 in February. Each lens consists of 2 pounds of silicon costing $2.50 per pound, 3 oz of solution costing $3 per ounce, and 30 minutes of direct labor at a labor rate of $18 per hour. Desired inventory levels are:

Prepare a sales budget, production budget, direct materials budget for silicon and solution, and a direct labor budget.

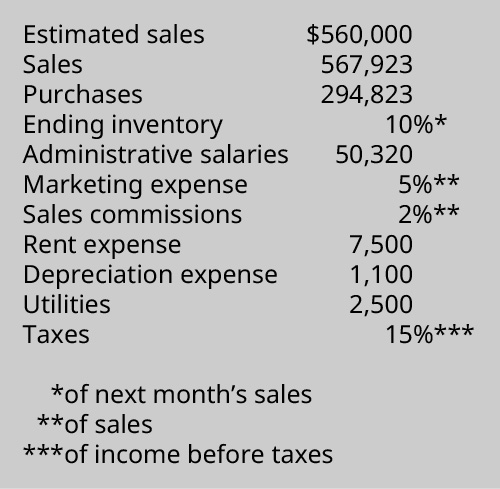

(Figure)The data shown were obtained from the financial records of Italian Exports, Inc., for March:

Sales are expected to increase each month by 10%. Prepare a budgeted income statement.

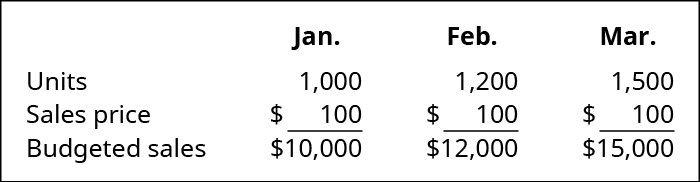

(Figure)Echo Amplifiers prepared the following sales budget for the first quarter of 2018:

It also has this additional information related to its expenses:

Prepare a sales and administrative expense budget for each month in the quarter ending March 31, 2018.

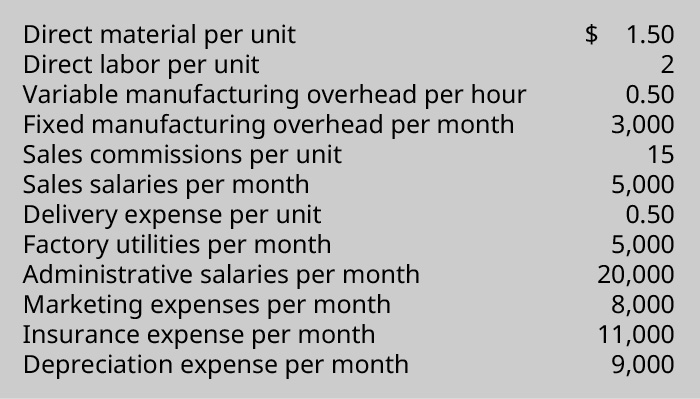

(Figure)Prepare a budgeted income statement using the information shown.

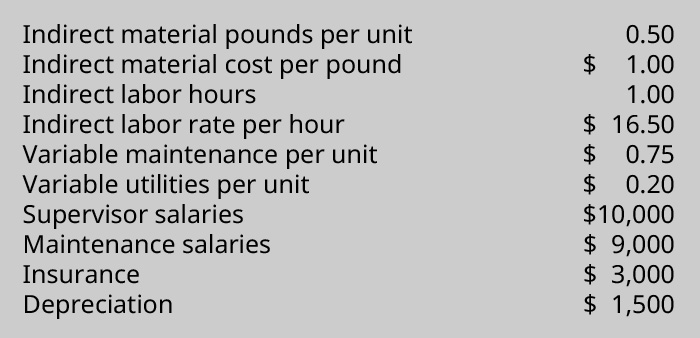

(Figure)Spree Party Lights overhead expenses are:

Prepare a manufacturing overhead budget if the number of units to produce for January, February, and March are 2,500, 3,000, and 2,700, respectively.

(Figure)Lens & Shades sells sunglasses for $37 each and is estimating sales of 21,000 units in January and 19,000 in February. Each lens consists of 2.00 mm of plastic costing $2.50 per mm, 1.7 oz of dye costing $2.80 per ounce, and 0.50 hours direct labor at a labor rate of $18 per unit. Desired inventory levels are:

Prepare a sales budget, production budget, direct materials budget for silicon and solution, and a direct labor budget.

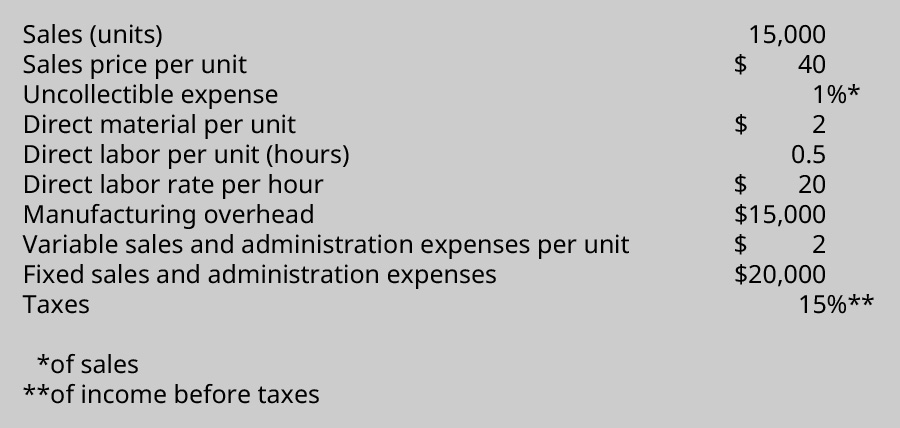

(Figure)The following data were obtained from the financial records of Sonicbrush, Inc., for March:

Sales are expected to increase each month by 15%. Prepare a budgeted income statement.

(Figure)TIB makes custom guitars and prepared the following sales budget for the second quarter

It also has this additional information related to its expenses:

Prepare a sales and administrative expense budget for each month in the quarter ended June 30, 2018.

(Figure)Prepare a budgeted income statement using the information shown.

(Figure)Sunshine Gardens overhead expenses are:

Given production of 10,200; 11,300; 12,900; and 13,200 for each quarter of the next year, prepare a manufacturing overhead budget for each quarter.

(Figure)How would a human resources department use information in the operating budgets?

(Figure)How would maintenance departments use information in the budget?

(Figure)How might service industries predict revenue?

Glossary

- budgeted income statement

- statement similar to a traditional income statement except it contains budgeted data

- direct labor budget

- budget based on the production budget used to ensure the proper amount of staff is available for production and that there is money available to pay for the labor

- direct materials budget

- budget combining the production budget with the direct material per unit to ensure the proper quantity of direct materials is available when needed for production

- manufacturing overhead budget

- budget including the remainder of the production costs not covered by the direct materials and direct labor budgets

- production budget

- budget showing the number of units that need to be produced for each period based on sales estimates and required inventory levels

- sales budget

- budget showing the expected sales in units and the sales price for the budget period

- selling and administrative expense budget

- budget showing the variable and fixed expenses estimated to be incurred in all areas other than production