33 Prepare Journal Entries for a Process Costing System

Patty Graybeal

Calculating the costs associated with the various processes within a process costing system is only a part of the accounting process. Journal entries are used to record and report the financial information relating to the transactions. The example that follows illustrates how the journal entries reflect the process costing system by recording the flow of goods and costs through the process costing environment.

Purchased Materials for Multiple Departments

Each department within Rock City Percussion has a separate work in process inventory account. Raw materials totaling $33,500 were ordered prior to being requisitioned by each department: $25,000 for the shaping department and $8,500 for the packaging department. The July 1 journal entry to record the purchases on account is:

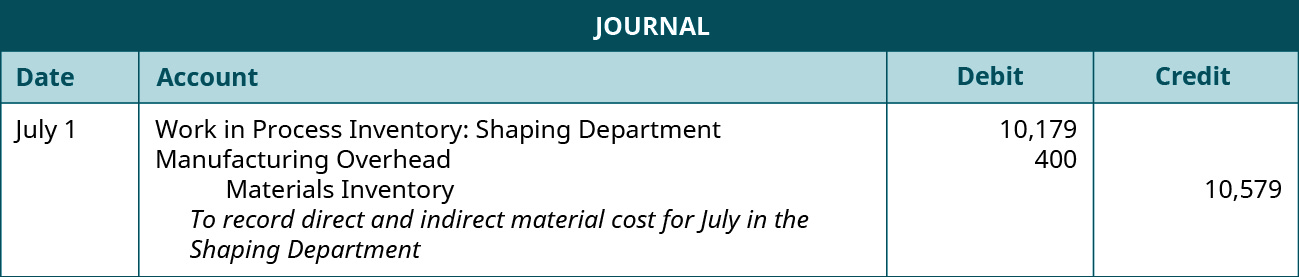

Direct Materials Requisitioned by the Shaping and Packaging Departments and Indirect Material Used

During July, the shaping department requisitioned $10,179 in direct material. Similar to job order costing, indirect material costs are accumulated in the manufacturing overhead account. The overhead costs are applied to each department based on a predetermined overhead rate. In the example, assume that there was an indirect material cost for water of $400 in July that will be recorded as manufacturing overhead. The journal entry to record the requisition and usage of direct materials and overhead is:

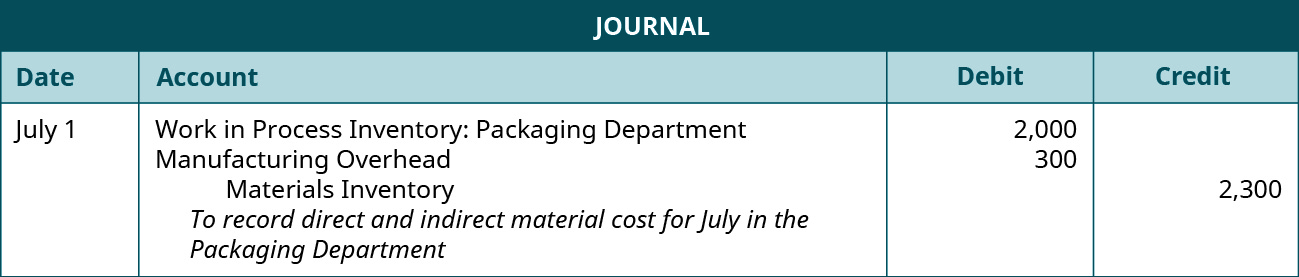

During July, the packaging department requisitioned $2,000 in direct material and overhead costs for indirect material totaled $300 for the month of July. The journal entry to record the requisition and usage of materials is:

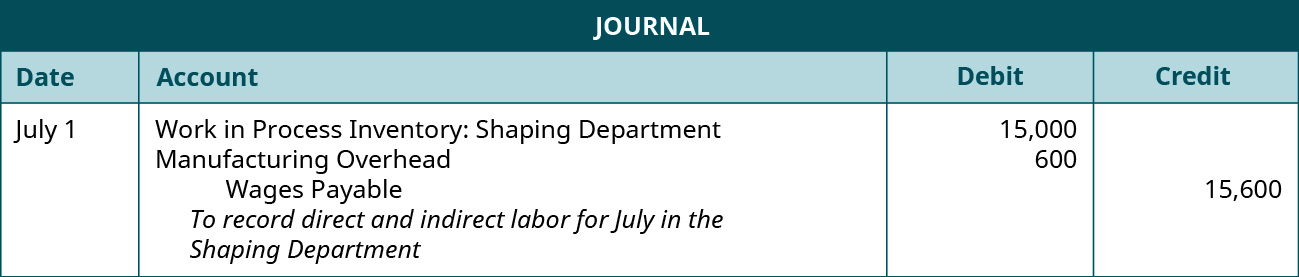

Direct Labor Paid by All Production Departments

During July, the shaping department incurred $15,000 in direct labor costs and $600 in indirect labor. The journal entry to record the labor costs is:

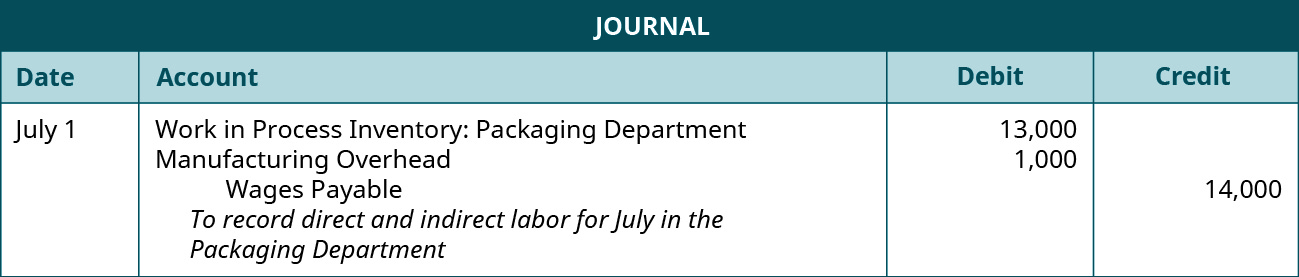

During July, the packaging department incurred $13,000 of direct labor costs and indirect labor of $1,000. The journal entry to record the labor costs is:

Applied Manufacturing Overhead to All Production Departments

Manufacturing overhead includes indirect material, indirect labor, and other types of manufacturing overhead. It is difficult, if not impossible, to trace manufacturing overhead to a specific product, and yet, the total cost per unit needs to include overhead in order to make management decisions.

Overhead costs are accumulated in a manufacturing overhead account and applied to each department on the basis of a predetermined overhead rate. Properly allocating overhead to each department depends on finding an activity that provides a fair basis for the allocation. It needs to be an activity common to each department and influential in driving the cost of manufacturing overhead. In traditional costing systems, the most common activities used are machine hours, direct labor in dollars, or direct labor in hours. If the number of machine hours can be related to the manufacturing overhead, the overhead can be applied to each department based on the machine hours. The formula for overhead allocation is:

Rock City Percussion determined that machine hours is the appropriate base to use when allocating overhead. The estimated annual overhead cost is $340,000 per year. It was also estimated that the total machine hours will be 34,000 hours, so the allocation rate is computed as:

The shaping department used 700 machine hours, and with an overhead application rate of $10 per direct labor hour, the journal entry to record the overhead allocation is:

The finishing department used 910 machine hours, and with an overhead application rate of $10 per direct labor hour, the journal entry to record the overhead allocation is:

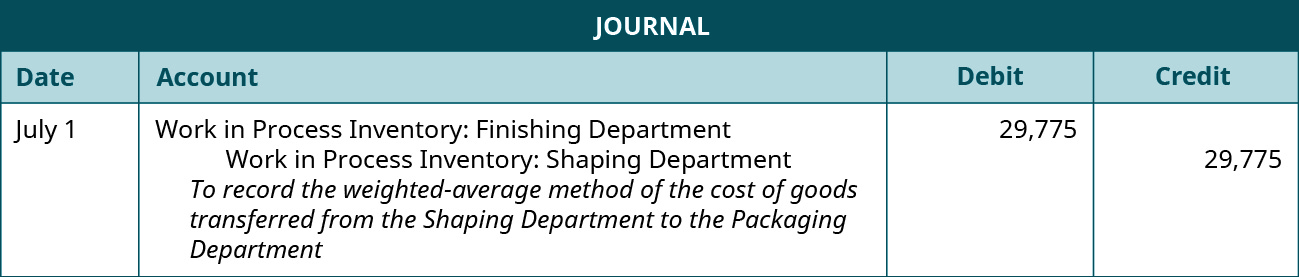

Transferred Costs of Finished Goods from the Shaping Department to the Packaging Department

When the units are transferred from the shaping department to the packaging department, they are transferred at $3.97 per unit, as calculated previously. The amount transferred from the shaping department is the same amount listed on the production cost report in (Figure). The journal entry is:

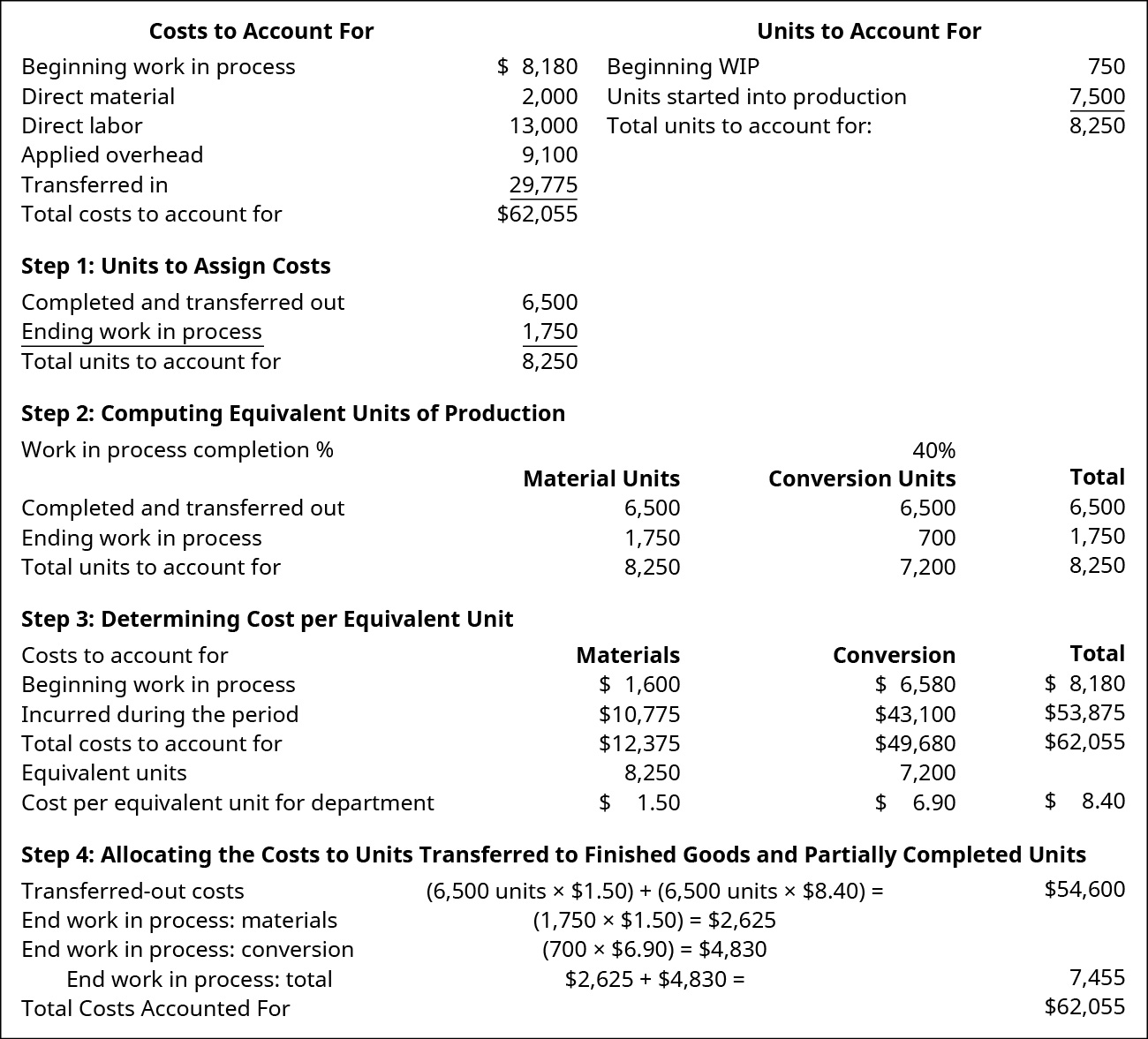

Transferred Goods from the Packaging Department to Finished Goods

The computation of inventory for the packaging department is shown in (Figure).

The value of the inventory transferred to finished goods in the production cost report is the same as in the journal entry:

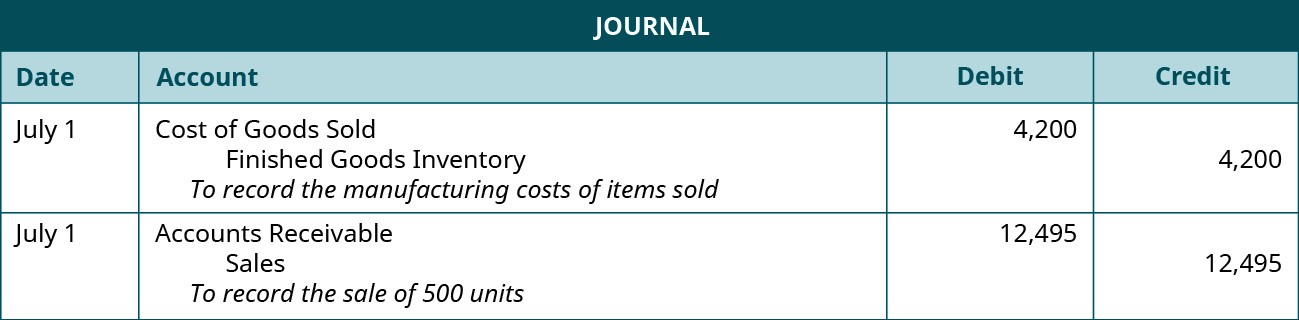

Recording the Cost of Goods Sold Out of the Finished Goods Inventory

Each unit is a package of two drumsticks that cost $8.40 to make and sells for $24.99. There are two transactions when recording a sale. One entry is to transfer the inventory from finished goods inventory to cost of goods sold and is at the cost of the product. The second transaction is to record the sale at the sales price. The compound entry to record both transactions for the sale of 500 units on account is:

The importance of properly recording the production process is illustrated in this report on work in process inventory from InventoryOps.com.

Key Concepts and Summary

- Traditional journal entries show the purchase of material and the incurring of overhead costs.

- Each department records the transfer of material from the storeroom into production, its direct labor costs, the application of overhead, and the transfer of goods to the next department or finished goods.

- The value of the inventory transferred to the next department or to finished goods equals the amount listed as transferred on the production cost report.

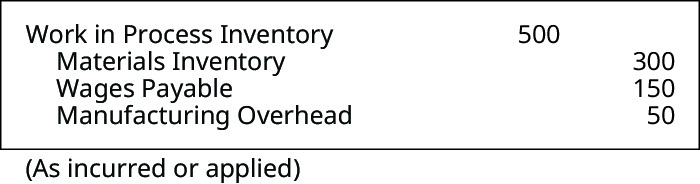

(Figure)The journal entry to record the $500 of work in process ending inventory that consists of $300 of direct materials, $50 of manufacturing overhead, and $150 od direct labor is which of the following?

(Figure)Assigning indirect costs to departments is completed by ________.

- applying the predetermined overhead rate

- debiting the manufacturing costs incurred

- applying the costs to manufacturing overhead

- applying the costs to work in process inventory

C

(Figure)In a process costing system, which account shows the overhead assigned to the department?

- cost of goods sold

- finished goods inventory

- raw material inventory

- work in process inventory

(Figure)In a process cost system, factory depreciation expense incurred is debited to ________.

- finished goods inventory

- work in process inventory

- manufacturing overhead

- cost of goods sold

C

(Figure)Match each term with its description.

| A. conversion costs | i. total of direct material costs and direct labor costs |

| B. cost of goods sold | ii. manufacturing costs of the items sold |

| C. cost of production report | iii. number of units produced if each unit was produced sequentially |

| D. cost per equivalent unit | iv. total of direct labor costs, indirect labor costs, indirect material costs, and manufacturing overhead |

| E. equivalent units of production | v. where costs in a process cost system are reported before being applied to the product |

| F. manufacturing department | vi. detailed listing of the total costs of the product including the value of work in process |

| G. prime costs | vii. cost of materials or conversion for a specific department during production |

| H. transferred out costs | viii. product of the total cost per unit and the number of units completed and transferred during the time period |

A. iv; B. ii; C. vi; D. vii; E. iii; F. v; G. i; H. viii.

(Figure)How is manufacturing overhead handled in a process cost system?

(Figure)How are predetermined overhead rates used in process costing?

Prior to the new year, a company computes the estimates of the annual overhead per department divided by the estimated driver for that department. A driver is the measure that increases the cost of overhead and is commonly direct labor hours, direct labor cost, or machine hours. The result is the predetermined overhead rate. Costs are accumulated in an account called manufacturing overhead. At the end of each period, the overhead is removed from the overhead account and applied to the department.

(Figure)Overhead is assigned to the manufacturing department at the rate of $10 per machine hour. There were 3,500 machine hours during October in the shaping department and 2,500 in the packaging department. Prepare the journal entry to apply overhead to the manufacturing departments.

(Figure)Prepare the journal entry to record the factory wages of $28,000 incurred for a single production department assuming payment will be made in the next pay period.

(Figure)Prepare the journal entry to record the transfer of 3,000 units from the packaging department to finished goods if the material cost per unit is $4 and the conversion cost per unit is $5.50.

(Figure)Prepare the journal entry to record the sale of 2,000 units that cost $8 per unit and sold for $15 per unit.

(Figure)Overhead is assigned to the manufacturing department at the rate of $5 per machine hour. There were 3,000 machine hours used in the molding department. Prepare the journal entry to apply overhead to the manufacturing department.

(Figure)Prepare the journal entry to record the factory wages of $25,000 incurred in the processing department and $15,000 incurred in the production department assuming payment will be made in the next pay period.

(Figure)Prepare the journal entry to record the transfer of 3,500 units from the separation department to the mash department if the material cost per unit is $2 and the conversion cost per unit is $5.

(Figure)Prepare the journal entry to record the sale of 700 units that cost $5 per unit and sold for $15 per unit.

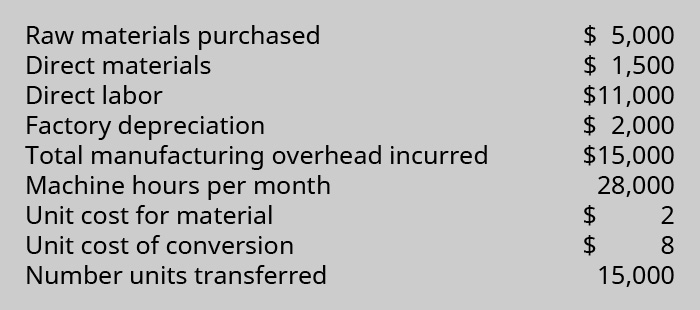

(Figure)Selected information from Skylar Studios shows the following:

Prepare journal entries to record the following:

- raw material purchased

- direct labor incurred

- depreciation expense (hint: this is part of manufacturing overhead)

- raw materials used

- overhead applied on the basis of $0.50 per machine hour

- the transfer from department 1 to department 2

(Figure)Loanstar had 100 units in beginning inventory before starting 950 units and completing 800 units. The beginning work in process inventory consisted of $2,000 in materials and $5,000 in conversion costs before $8,500 of materials and $11,200 of conversion costs were added during the month. The ending WIP inventory was 100% complete with regard to materials and 40% complete with regard to conversion costs. Prepare the journal entry to record the transfer of inventory from the manufacturing department to the finished goods department.

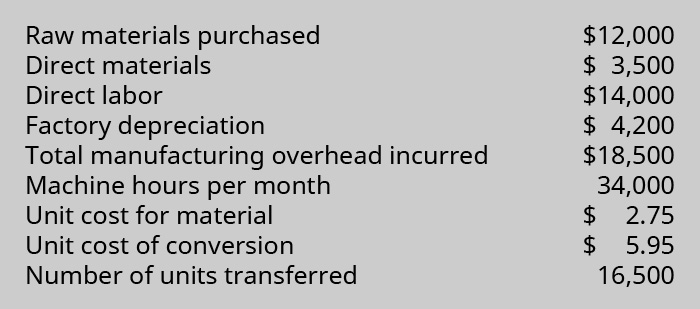

(Figure)Selected information from Hernandez Corporation shows the following:

Prepare journal entries to record the following:

- raw material purchased

- direct labor incurred

- depreciation expense (hint: this is part of manufacturing overhead)

- raw materials used

- overhead applied on the basis of $0.50 per machine hour

- the transfer from department 1 to department 2

(Figure)Rexar had 1,000 units in beginning inventory before starting 9,500 units and completing 8,000 units. The beginning work in process inventory consisted of $5,000 in materials and $8,500 in conversion costs before $16,000 of materials and $18,500 of conversion costs were added during the month. The ending WIP inventory was 100% complete with regard to materials and 40% complete with regard to conversion costs. Prepare the journal entry to record the transfer of inventory from the manufacturing department to the finished goods department.

(Figure)What is different between the journal entries for process costing and that of job order costing?