71 Explain the Importance of Performance Measurement

Patty Graybeal

As you learned in Responsibility Accounting and Decentralization, as a company grows, it will often decentralize to better control operations and therefore improve decision-making. Remember, a decentralized organization is one in which the decision-making is spread among various managers throughout the organization and does not solely rest with the chief executive officer (CEO). However, with this dispersion of decision-making comes an even greater need to monitor the results of the decisions made by the many managers at the various levels of the organization to ensure that the overall goals of the organization are still being met.

To evaluate whether decisions made by management are both effective and ethical, performance is measured through responsibility accounting. This is a double-layer ethical analysis that requires some thought to establish and implement, as the evaluation system must also operate in an ethical fashion, just as the decision-making process itself does. In most organizations, the overall results of choices made by management, not just the resulting profit, need to be examined to determine whether or not the decisions are ethical.

When an organization’s customers and other stakeholders are happy, and the corporate assets are in good condition, these are indicators that the customers, stakeholders, and assets are being treated ethically. Evaluation of customer and stakeholder satisfaction should come directly from the customer, such as through surveys or other direct questionnaires. Proper treatment of organizational assets can be determined by viewing the physical condition of such assets, or the loss rates and productivity of equipment. Customer satisfaction and positive results in the utilization of corporate assets typically indicate ethical decision-making and behavior, while negative results typically indicate the opposite. An organization with a satisfied group of stakeholders and customers, as well as assets that operate efficiently, is often more profitable in the long term.

Managerial accountants therefore must design a framework of responsibility accounting in which the evaluation system is based on criteria for which a manager is responsible. The framework should be structured to encourage managers to make decisions that will meet the goals of the company as well as their own professional goals. In your study of managerial accounting, you have learned about company goals such as increasing market share, increasing revenues, decreasing costs, and decreasing defects. Managers and employees have their own goals. These goals can be work related such as promotions or awards, or they can be more personal such as receiving raises, receiving bonuses, the privilege of telecommuting, or shares of company stock. This aligning of goals between a corporation’s strategy and a manager’s personal goals is known as goal congruence. Managers should make the best decisions for the benefit of the corporation, and the best way to motivate a manager to make those decisions is to link a reward system to performance results. To accomplish this, a business establishes performance evaluation measures that align the decisions made by management with the goals of the corporation and the professional goals of the manager.

Fundamentals of Performance Measurement

Performance measurement is used to motivate managers to make decisions that benefit the corporation and themselves. Therefore, the key to good performance measurement techniques is to set goals that are realistic and that incorporate decisions over which the manager has control. Then, the company can evaluate the manager based on controllable factors, which are the components of the organization for which the manager is responsible and that the manager can control, such as revenues, costs and procurement of long-term assets, and other possible factors. Recall that in Responsibility Accounting and Decentralization, you learned about responsibility centers, which are a means by which an organization can be divided based on factors that the manager can control. This makes it easier to align the goals of the manager with those of the organization and to design effective performance measures. The four types of responsibility centers are revenue centers, cost centers, profit centers, and investment centers.

In a revenue center, the manager has control over the revenues that are generated for the corporation but not over the costs of the organization. For example, the reservations department of an airline is a revenue center because the reservationists can control revenues by selling customers upgrades such as meals or first-class seating, by selling trip insurance, or by trying to keep customers from going to another airline. However, reservationists cannot control the costs of the flights the airline is offering and reserving because the reservation department cannot control the cost of the planes, airport space rental, or jet fuel. Therefore, the manager of the reservation department should have performance evaluations measures closely related to revenue generation.

In a cost center, the manager has control over costs but not over revenues. An example of a cost center would be the accounting department of a grocery store chain. The manager can control the types of people hired, the wages that are paid, and the hours that are worked within that department, and each of these costs contributes to the total cost of the department. However, the manager of the accounting department has no control over the generation of revenues.

In a profit center, the manager has control over both revenues and costs. An example would be a single location of Best Buy. The manager at that store has control over both revenues and costs; therefore, one component of evaluation for that manager will be store profits.

An investment center is a component of a business for which the manager has control over revenues, costs, and capital assets. This means the manager not only can make decisions regarding generating revenues and controlling costs but also has authority to make decisions regarding assets, such as buying new machines, expanding facilities, or selling old assets. With each of these types of centers, designing the appropriate performance measures begins with evaluating management based on which business areas they oversee.

Using the previous revenue center example, the manager of the reservation department should be evaluated on how well his team generates revenues. The proper incentives will motivate the team to perform better at their jobs. Evaluating a manager on the outcome of decisions over which he or she has no control, or uncontrollable factors, will be demotivating and does not promote goal congruence between the organization and the manager. The reservations manager has no control over fuel costs, plane maintenance costs, or pilot salaries. Thus, it would not be logical to evaluate the manager on flight costs.

A good performance measurement system is one that utilizes appropriate performance measures, which are performance metrics used to evaluate a specific attribute of a manager’s role, to evaluate management in a way that will link the goals of the corporation with those of the manager. A metric is simply a means to measure something. For example, high school grade point average is a metric used by colleges when considering admission of prospective students, as it is considered a measure of prior academic success. In the business environment, individuals who design the performance measurement system must have extensive knowledge of the corporate strategic plan and the overall goals set by the organization, and a clear understanding of the job descriptions, responsibilities of each manager, and trends in rewards and compensation.

As a dentist and owner of your own practice, you are considering ways to both reward and motivate your staff. The obvious choice is to simply give each employee a raise. However, you have heard that many businesses are compensating their employees for meeting various goals that are beneficial to the business. What types of goals might the dental practice have? What are several ideas for ways to motivate the staff, which consists of a receptionist, dental assistants, and dental hygienists? What are possible rewards for meeting goals?

Advantages Derived from Performance Measurement

Every business has a strategic plan, or a broad vision of how it will be in the future. This plan leads to goals that must be achieved to fulfill that vision. As shown in (Figure), a business will use the strategic plan to determine the goals needed to achieve the strategic vision. Once goals are determined, the business will decide on the appropriate actions necessary to meet the goals. Then, the business will implement, review, and adjust the goals as needed. Properly designed performance measures will help move the company toward meeting the goals of its strategic plan. Advantages of a good performance management system include increased employee retention and loyalty, better communication between the various levels of management, increased productivity, and increased efficiencies. In addition, a well-designed performance plan should lead to improved job satisfaction for the manager and increased personal wealth if the rewards are monetarily based. In summary, a company needs to first identify and create a strategy and then set the necessary goals, which will lead to actions, and finally to an applicable evaluation process.

All companies need ways to measure the performance of employees. These measures should be designed in a way that the rewards for performance will motivate the employees to make decisions that are good for the business. Reflecting on the Why It Matters scenario, if this were your company, what are five goals you would have for your business? What are some measures you could use to see if you are meeting those goals? What types of incentives could you offer to motivate your employees to help meet these goals? Use (Figure) for your answers.

| Motivating Employees toward Business Goals | ||

|---|---|---|

| Five Business Goals | Measures to Meet Goals | Incentives to Motivate Employees toward Goals |

Solution

Answers will vary. Sample answer:

| Motivating Employees toward Business Goals | ||

|---|---|---|

| Five Business Goals | Measures to Meet Goals | Incentives to Motivate Employees toward Goals |

| Grow customer base | Number of new customers | Give a gift card to employees for each new customer they get |

| Increase company name recognition | Number of “likes” on Facebook, number of reviews on Google | Host a party or take employees to dinner after certain number of likes or positive reviews occur |

| Grow revenue each quarter | Percent change in revenue from prior quarter | Have a bonus pool that is shared after a targeted percentage increase in revenue is reached |

| Lower cost of supplies used per job | Compare supplies used to a standard for each type of job | Provide a paid day off for suggestions that successfully reduce cost of supplies per job by 5% |

| Decrease time at each job/increase efficiency | Measure time on job using a call-in system of entering and leaving the job | Pay a flat additional amount for each time the employee performs a job within the allotted time and that customer satisfaction is a 5/5 |

Potential Limitations of Traditional Performance Measurement

What types of measures are used to evaluate management performance? Historically, performance measurement systems have been based on accounting or other quantitative numbers. One reason for this is that most accounting-based measures are easy to use due to their availability, since many accounting measures can be found in or generated from a company’s financial statements. Although this type of information is readily available, it does not mean the use of accounting numbers as performance measures is the best or only way to measure performance. One issue is that some accounting numbers can be affected by the actions of managers, and this may result in distorted performance results.

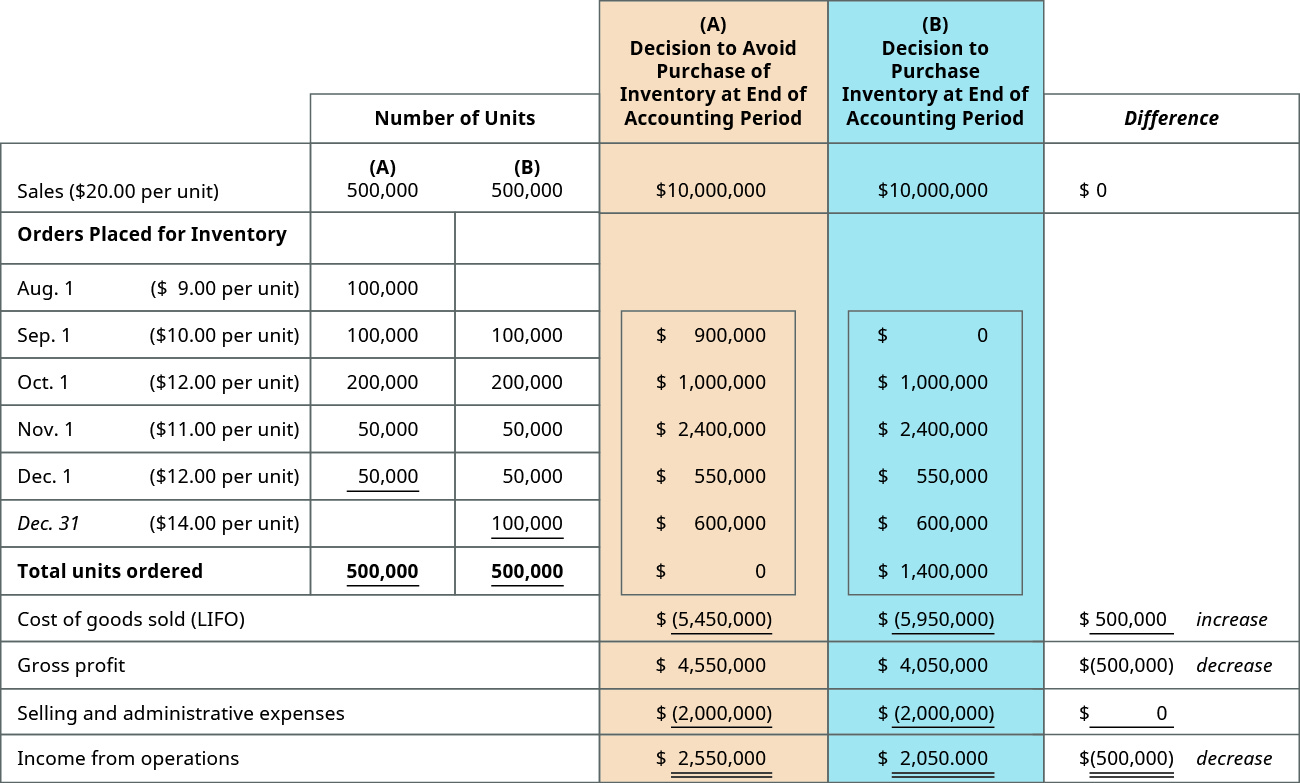

For example, as shown in (Figure), if a retail company uses a last-in, first-out (LIFO) inventory system and the manager of the retail store is evaluated based on either cost containment or profit, the manager can postpone a decision to purchase inventory at the end of the year until the beginning of the next fiscal year if prices of the inventory have risen. This decision will postpone the effect of that purchase and, in turn, the higher costs associated with that inventory, until the next accounting cycle. As you can see, in either scenario, the company ordered 500,000 units of inventory but the timing of those orders, given the changing prices of the inventory, has a significant effect on income from operations. This scenario is an example of the possibility of an unintended conflict of interests between procurement and production decisions by an individual manager or department and the overall best interests of the company. A well-designed performance measurement system should eliminate these potential conflicts, as much as possible.

Accounting numbers are often affected by economic conditions, but these economic effects are beyond the control of the manager. For example, if the parts used in a manufacturing process are ordered from another country, the manager cannot control the exchange rate that occurs between the two currencies, yet this can impact the cost of the components to the manager and thus affect the cost of the product the company is producing.

Some management decisions affect multiple periods, or the decision being made will have the greatest impact in a future period. For example, capital budgeting decisions affect not only the current but future periods as well. This may compel a manager to have a short-term focus, because increasing his immediate remuneration, or compensation, is often his goal. Many long-term decisions, such as capital budgeting decisions, maintenance on equipment, or advertising campaigns, may most significantly affect future accounting numbers and, in turn, the compensation of the manager in future periods. If a manager cannot see himself reaping the rewards of that decision in future years, the decision becomes less attractive. If a performance measurement system is not designed properly, it can lead to managers having a short-term focus or making decisions that have the greatest impact on their individual goals (such as reaching a bonus goal), even if these decisions are not in the best long-term interest of the corporation. Last, a manager focused solely on accounting numbers may miss opportunities for future benefits because making the decision will have a negative impact on accounting measures in the current period. For example, spending money to build a potential customer database may decrease income in the current year. If the manager’s performance is measured based on the profitability of his division, he may avoid spending the money to create the customer database. However, that database may result in a significant increase in profitability in future years if the potential customers become actual customers.

Is there a way to prevent these issues associated with using accounting measures as performance measures? The use of nonaccounting measures in conjunction with accounting-based measures can help mitigate the problems of using accounting-based measures alone. Therefore, most performance measurement systems today use a combination of accounting-based measures and non-accounting-based measures, short-term or long-term indicators, or quantitative and qualitative components. Let’s first look at the use of accounting-based measures, and then we’ll consider a methodology that also incorporates non-accounting-based measures.

Noah Barnes just graduated from college and took a position as production supervisor for Morgensen Machines, who manufactures sewing machine and vacuum cleaner parts. On his first day at work, one of Morgensen’s sales managers asked Noah if it would be OK to rearrange his manufacturing job schedule so that a special order from a new customer could be pushed to the front of the line. This new customer requires fast turnarounds; unfortunately, this also means running the production equipment for all three shifts at maximum output for at least one week, possibly more. This would completely prohibit the schedule that management told Noah to implement. Noah does not want to make the sales manager angry at him, but he also does not want to lose his job in the first month out of college. He knows that the manager is focused on landing this new customer, who could reward the company with a needed increase in overall sales and plant output. The problems, as Noah sees them, are that (1) current jobs will be delayed; (2) there will be greater demand on the machines during all three shifts, increasing the possibility that they will fail; (3) there will not be time for needed maintenance; and (4) eventually all of these factors will snowball into significant delays for the new customer, as well as extensive delays for the previously scheduled orders.

How should Noah handle this problem? What managerial principles would you advise him to use from his college studies to help him develop better policies for future events like this?

Key Concepts and Summary

- Well-designed performance measurement systems help businesses achieve goal congruence between the company and the employees.

- Managers should be evaluated only on factors over which they have control.

- Performance measures can be based on financial measures and/or nonfinancial measures.

- Performance measurement systems should help the company meet its strategic goals while helping the employee meet his or her professional goals.

(Figure)Components of the organization that are demotivating for purposes of performance management are known as ________.

- business goals

- strategic plans

- uncontrollable factors

- incentives

C

(Figure)When managerial accountants design an evaluation system that is based on criteria for which a manager is responsible, and it is structured to encourage managers to make decisions that will meet the goals of the company as well as their own personal job goals, the framework used is ________.

- a controllable factors framework

- an uncontrollable factors framework

- a strategic plan framework

- a responsibility accounting framework

(Figure)Goal congruence in well-designed performance measurement systems best explains a congruence between ________.

- employees and the company

- strategic plans and the future

- decisions and outcomes

- feedback and measurement

A

(Figure)Responsibility accounting holds managers responsible for ________.

- all costs charged to their subunit

- all costs charged to their subunit plus a share of company-wide fixed costs

- only the costs that they can control

- only the costs that they have personally approved

(Figure)Performance measures are only useful if ________.

- there are both controllable and uncontrollable factors to evaluate managers

- manager reward systems are designed by the chief financial officer prior to implementation

- all of the measures used are accounting numbers

- there is a baseline against which to compare the measured results

A

(Figure)Why might a manager focused solely on accounting numbers miss opportunities for future benefits?

Answers will vary. Responses may focus on the short-term view versus long-term views and include examples such as: managers focusing on only profitability might avoid spending the money for long-term assets to fuel the future; managers may miss other opportunities like funding the expense for creation of a customer database, if profitability is the focus in the short term; managers may avoid research and development costs that would be used to create the next generation of their product to achieve profitability in the short term.

(Figure)Is there a way to prevent managers from focusing on accounting measures as performance measures?

(Figure)Should an organization focus on controllable or uncontrollable factors to effectively implement a successful performance measurement system? Explain your answer.

Controllable. Responses will vary based on students’ prior experiences.

(Figure)What are the components of a strategic plan? Find one of these components for the company you work for and share (if you are not currently employed, use the college you attend).

(Figure)What are the four types of centers and their corresponding responsibilities?

Revenue center—the manager has control over the revenues that are generated for the corporation but not over the costs of the organization. Cost center—the manager has control over costs but not over revenues. Profit center—the manager has control over both revenues and costs. Investment center— the manager has control over revenues, costs, and capital assets.

(Figure)For the following situations, identify whether the description is probably a centralized or decentralized organization.

- Seaside Furniture, a small builder of side tables managed solely by its sole proprietor

- Harbor Marketing, which wants Advertising Team Leaders to be able to respond quickly to needs of potential clients so Team Leaders have the authority to make decisions about advertising and pricing

- Couture’s Creations, with a single owner who manages the production, accounting, engineering, sales, and other administrative functions

- British Navy

- McDonalds franchise #3101 in Canton, Ohio

- United States Army

(Figure)For the following descriptions state whether the cost is controllable or uncontrollable by responsibility center managers.

- property tax of an existing manufacturing facility

- research and development of a product

- advertising of a product

- insurance cost of the existing manufacturing facility

- design of a product

(Figure)Identify the type of responsibility center (revenue center, cost center, profit center, or investment center) for each of the following situations.

- the accounting department for Tubelite Inc.

- the Best Buy in Traverse City, Michigan

- the reservation department of Allegiant airlines

- the sales department of Four Winns

- the Kohl’s store in Mount Pleasant, Michigan

- The Hershey Company

- Procter and Gamble

- the shoe department in the Kohl’s store in Mount Pleasant, Michigan

(Figure)For the following situations identify whether the description is a centralized or decentralized organization.

- the United States Navy

- Farah’s Domino’s franchise store

- Domino’s Pizza

- Middie’s Furniture, which is divided into separate operating units, such as living room, kitchen, flooring

- the local community college, which has a single payroll department, a single administrative headquarters, and a single human resources department since it “flattened” its organization structure

- Conner Corporation, which promotes managers from within the organization whenever possible and which has formal training programs for lower-level managers

(Figure)For the following descriptions, state whether the cost is controllable or uncontrollable by responsibility center managers.

- advertising for a merchandiser

- corporate income taxes

- office supplies for a merchandiser

- donations to the Salvation Army

- insurance for delivery vehicles

(Figure)Identify the type of responsibility center (revenue center, cost center, profit center, or investment center) for each of the following situations.

- the legal department for Avon Manufacturing

- the Macy’s store in Mansfield, Ohio

- the food and beverage division of the Best Western

- the marketing department of the Hershey Company

- the Walmart #5030 on Central Avenue in Toledo, Ohio

- Apple’s Braeburn Capital Inc., where most of Apple’s billions of dollars are invested

- Zappo’s department store

- the men’s clothing department in the Walmart #5030 in Toledo, Ohio

(Figure)Match each of the following with its appropriate term.

| A. Controllable factors | i. This is the part of an organization in which management is evaluated based on the ability to contain costs; the manager primarily has control only over costs. |

| B. Cost center | ii. This means to align the goals of the business with the personal goals of the manager. |

| C. Metric | iii. These components of the organization are components for which the manager is responsible and can control. |

| D. Goal congruence | iv. This is the means to measure something such as a goal or target. |

| E. Investment center | v. This is a system that evaluates management in a way that will link the goals of the corporation with those of the manager. |

| F. Performance measurement system | vi. For this center, management is responsible for revenues, costs, and assets and is evaluated based on these three components. |

(Figure)Florentino Allers is the production manager of Electronics Manufacturer. Due to limited capacity, the company can only produce one of two possible products:

- An industrial motherboard with a 75% probability of making a profit of $1 million and a 25% probability of making a profit of $150,000

- A regular motherboard with a 100% chance of making a profit of $710,000

Florentino will get a 20% bonus from his department. Florentino has the responsibility to choose between the two products and is more of a risk-taker, more so than most of the top management at Electronics Manufacturer.

- Which option is Florentino more likely to choose and why?

- Which option would the company be more likely to choose and why?

- What changes should the company make to Florentino’s compensation to avoid unnecessary risks?

(Figure)Match each of the following with its appropriate term:

| A. Performance measures | i. The decisions and outcomes over which a manager does not have control |

| B. Profit center | ii. That part of an organization in which management is evaluated based on the ability to generate revenues; the manager primarily has control only over revenues |

| C. Responsibility accounting | iii. The part of an organization in which management is evaluated based on the ability to generate profits because the manager has control over both revenues and costs |

| D. Revenue center | iv. A broad vision of how a company will be in the future |

| E. Strategic plan | v. A system that collects and reports data for which a manager has responsibility |

| F. Uncontrollable factors | vi. The metrics used to evaluate a specific attribute of a manager’s role |

(Figure)Oleg Markov is the production manager of NASA Solvents. Due to limited capacity, the company can only produce one of two possible products:

- an industrial concentrated solvent with a 15% probability of making a profit of $1 million and an 85% probability of making a profit of $200,000

- a household diluted solvent with a 100% chance of making a profit of $310,000

Oleg will get a 20% bonus from his department. Oleg has the responsibility to choose between the two products and is more risk averse than most of the top management at NASA Solvents.

- Which option is Oleg more likely to choose and why?

- Which option would the company be more likely to choose and why?

- What changes should the company make to Oleg’s compensation to encourage managers to take appropriate risks

(Figure)What combination of quantitative factors and qualitative factors would you like your potential employer to use as a performance management system? Explain your answer.

Glossary

- controllable factor

- component of the organization for which the manager is responsible and that the manager can control

- cost center

- part of an organization in which management is evaluated based on the ability to contain costs; the manager primarily has control only over costs

- goal congruence

- integration of multiple goals, either within an organization or across multiple components or entities; congruence is achieved by aligning goals to achieve an anticipated mission

- investment center

- organizational segment in which a manager is accountable for profits (revenues minus expenses) and the invested capital used by the segment

- metric

- means to measure something such as a goal or target

- performance measurement system

- evaluates management in a way that will link the goals of the corporation with those of the manager

- performance measure

- metric used to evaluate a specific attribute of a manager’s role

- profit center

- organizational segment in which a manager is responsible for and evaluted on both revenues and costs

- responsibility accounting

- method of encouraging goal congruence by setting and communicating the financial performance measures by which managers will be evaluated

- revenue center

- part of an organization in which management is evaluated based on the ability to generate revenues; the manager’s primary control is only revenues

- strategic plan

- broad vision of how a company will be in the future

- uncontrollable factor

- decision or outcome over which a manager does not have control