26 Prepare Journal Entries for a Job Order Cost System

Patty Graybeal

Although you have seen the job order costing system using both T-accounts and job cost sheets, it is necessary to understand how these transactions are recorded in the company’s general ledger.

Journal Entries to Move Direct Materials, Direct Labor, and Overhead into Work in Process

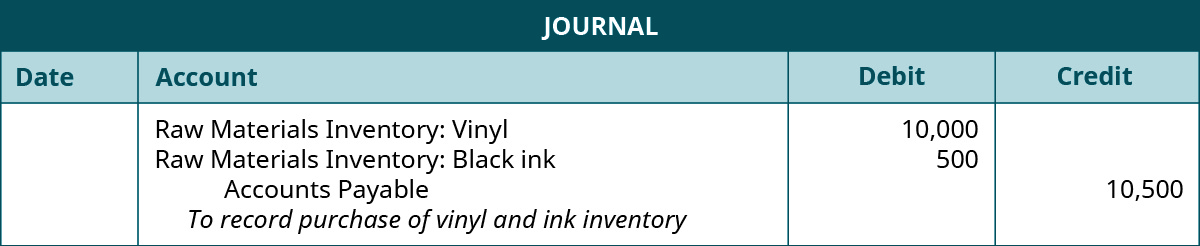

Dinosaur Vinyl keeps track of its inventory and orders additional inventory to have on hand when the production department requests it. This inventory is not associated with any particular job, and the purchases stay in raw materials inventory until assigned to a specific job. For example, Dinosaur Vinyl purchased an additional $10,000 of vinyl and $500 of black ink to complete Macs & Cheese’s billboard. If the purchase is made on account, the entry is as shown:

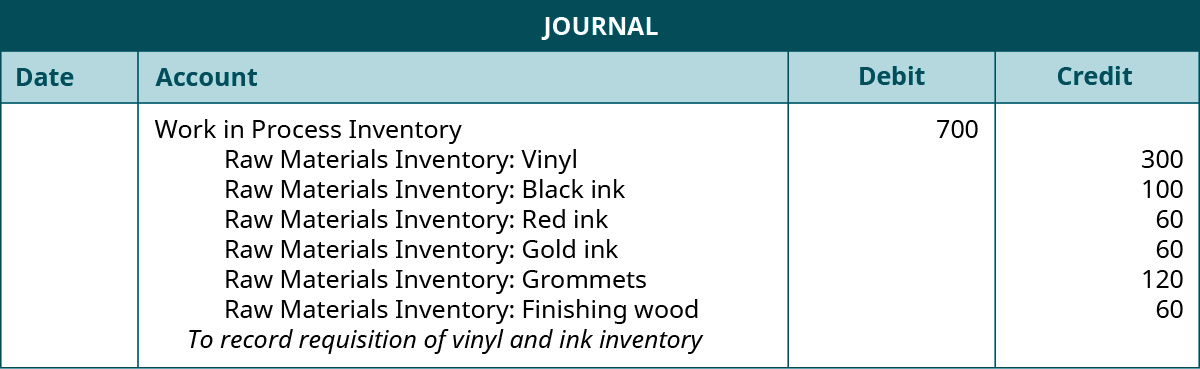

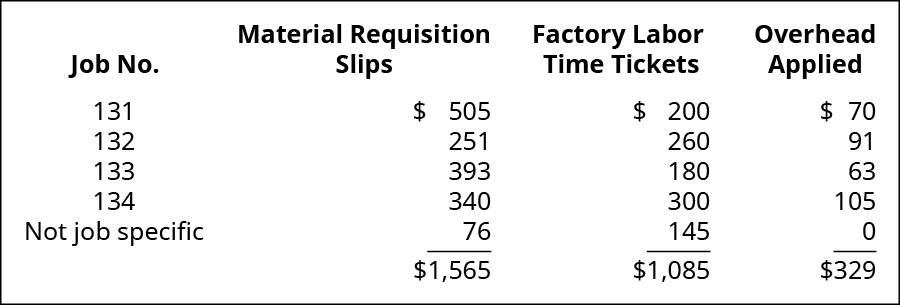

As shown in (Figure), for the production process for job MAC001, the job supervisor submitted a materials requisition form for $300 in vinyl, $100 in black ink, $60 in red ink, and $60 in gold ink. For the finishing process for Job MAC001, $120 in grommets and $60 in finishing wood were requisitioned. The entry to reflect these actions is:

The production department employees work on the sign and send it over to the finishing/assembly department when they have completed their portion of the job.

The direct cost of factory labor includes the direct wages paid to the employees and all other payroll costs associated with that labor. Typically, this includes wages and the payroll taxes and fringe benefits directly tied to those wages. The accounting system needs to keep track of the labor and the other related expenses assigned to a particular job. These records are typically kept in a time ticket submitted by employees daily.

On April 10, the labor time sheet totaling $30 is recorded for Job MAC001 through this entry:

The assembly personnel in the finishing/assembly department complete Job MAC001 in two hours. The labor is recorded as shown:

Indirect materials also have a materials requisition form, but the costs are recorded differently. They are first transferred into manufacturing overhead and then allocated to work in process. The entry to record the indirect material is to debit manufacturing overhead and credit raw materials inventory.

Indirect labor records are also maintained through time tickets, although such work is not directly traceable to a specific job. The difference between direct labor and indirect labor is that the indirect labor records the debit to manufacturing overhead while the credit is to factory wages payable.

Dinosaur Vinyl’s time tickets indicate that $4,000 in indirect labor costs were incurred during the period. The entry is:

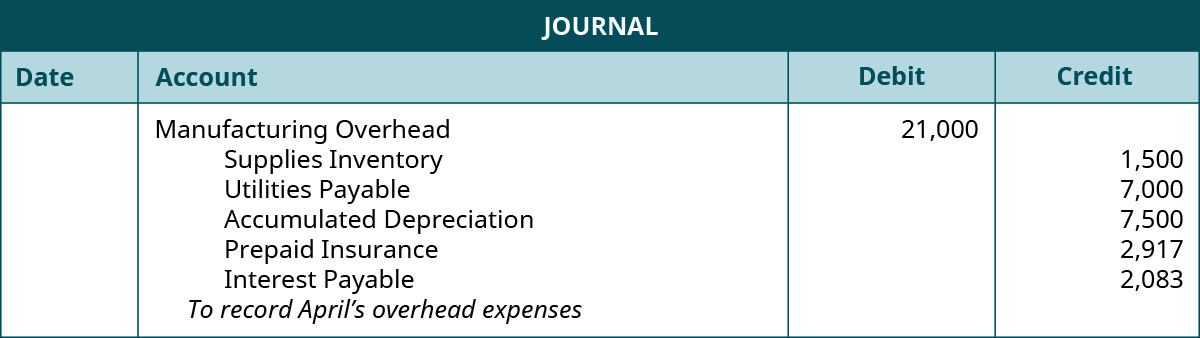

Dinosaur Vinyl also records the actual overhead incurred. As shown in (Figure), manufacturing overhead costs of $21,000 were incurred. The entry to record these expenses increases the amount of overhead in the manufacturing overhead account. The entry is:

The amount of overhead applied to Job MAC001 is $165. The process of determining the manufacturing overhead calculation rate was explained and demonstrated in Accounting for Manufacturing Overhead. The journal entry to record the manufacturing overhead for Job MAC001 is:

Journal Entry to Move Work in Process Costs into Finished Goods

When each job and job order cost sheet have been completed, an entry is made to transfer the total cost from the work in process inventory to the finished goods inventory. The total cost of the product for Job MAC001 is $931 and the entry is:

Journal Entries to Move Finished Goods into Cost of Goods Sold

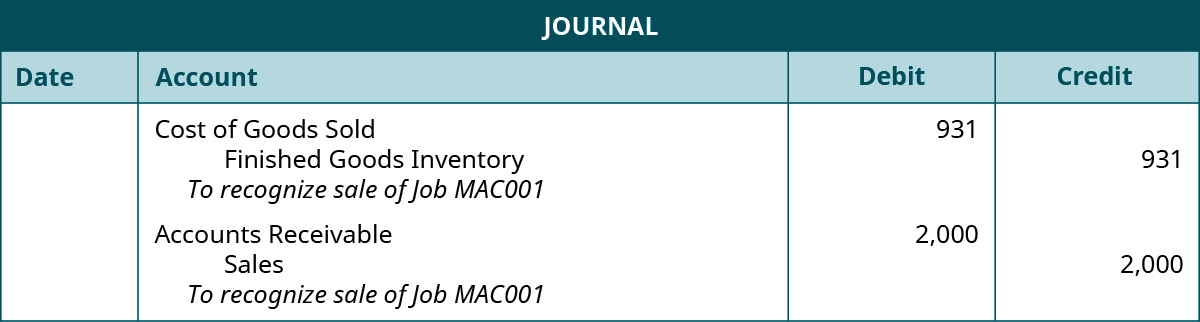

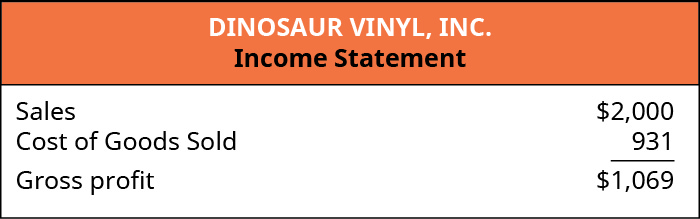

When the sale has occurred, the goods are transferred to the buyer. The product is transferred from the finished goods inventory to cost of goods sold. A corresponding entry is also made to record the sale. The sign for Job MAC001 had a sales price of $2,000 and a cost of $931. These are the entries to record the transfer of goods and sale to the buyer:

The resulting accounting is shown on the company’s income statement:

At the end of each year, manufacturing overhead is analyzed, and an adjusting entry is made to dispose of the under- or overapplied overhead. How would you advise a company that has had overapplied overhead for each of the last five years?

Key Concepts and Summary

- Job cost sheets record the material, labor, and overhead costs for each job, whereas journal entries actually transfer the costs into the work in process inventory, the finished goods inventory, and cost of goods sold.

(Figure)In a job order cost system, raw materials purchased are debited to which account?

- raw materials inventory

- work in process inventory

- finished goods inventory

- cost of goods sold

(Figure)In a job order cost system, overhead applied is debited to which account?

- work in process inventory

- finished goods inventory

- manufacturing overhead

- cost of goods sold

A

(Figure)In a job order cost system, factory wage expense is debited to which account?

- raw materials inventory

- work in process inventory

- finished goods inventory

- cost of goods sold

(Figure)In a job order cost system, utility expense incurred is debited to which account?

- work in process inventory

- finished goods inventory

- manufacturing overhead

- cost of goods sold

C

(Figure)In a job order cost system, indirect labor incurred is debited to which account?

- work in process inventory

- finished goods inventory

- manufacturing overhead

- cost of goods sold

(Figure)Match the concept on the left to its correct description.

| A. job order costing | i. computes the overhead applied to each job |

| B. materials requisition sheet | ii. source document indicating the number of hours an employee worked on specific jobs |

| C. overapplied overhead | iii. source document indicating the raw materials assigned to a specific production job |

| D. predetermined overhead rate | iv. the cost accounting system used by pet food manufacturers |

| E. process costing | v. the cost accounting system used by law firms |

| F. time ticket | vi. the result when the actual overhead is less than the amount assigned to each specific job |

| G. underapplied overhead | vii. the result when the actual overhead is more than the amount assigned to each specific job |

(Figure)A company has the following transactions during the week.

- Purchase of $1,000 raw materials inventory

- Assignment of $500 of raw materials inventory to Job 5

- Payroll for 20 hours with $1,000 assigned to Job 5

- Factory utility bills of $750

- Overhead applied at the rate of $10 per hour

What is the cost assigned to Job 5 at the end of the week?

(Figure)During the month, Job AB2 used specialized machinery for 450 hours and incurred $500 in utilities on account, $300 in factory depreciation expense, and $100 in property tax on the factory. Prepare journal entries for the following:

- Record the expenses incurred.

- Record the allocation of overhead at the predetermined rate of $1.50 per machine hour.

(Figure)Job 113 was completed at a cost of $5,000, and Job 85 was completed at a cost of $3,000 and sold on account for $4,500. Prepare journal entries for the following:

- Completion of Job 113.

- Completion and sale of Job 85.

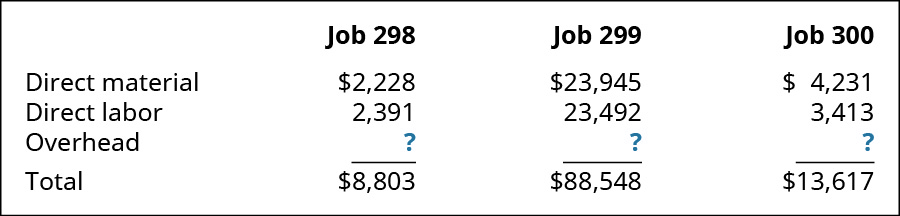

(Figure)A company’s individual job sheets show these costs:

Overhead is applied at 1.25 times the direct labor cost. Use the data on the cost sheets to perform these tasks:

- Apply overhead to each of the jobs.

- Prepare an entry to record the assignment of direct materials to work in process.

- Prepare an entry to record the assignment of direct labor to work in process.

- Prepare an entry to record the assignment of manufacturing overhead to work in process.

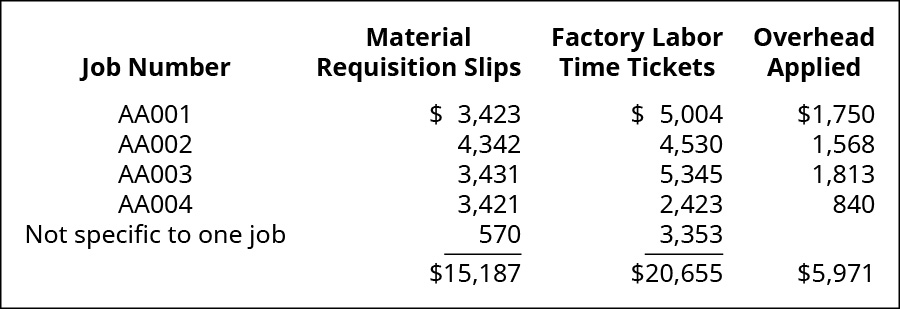

(Figure)A summary of material requisition slips and time tickets, along with the overhead allocation, show these costs:

- Prepare an entry to record the assignment of direct material to work in process.

- Prepare an entry to record the assignment of direct labor to work in process.

- Prepare an entry to record the assignment of manufacturing overhead to work in process.

(Figure)A company has the following transactions during the week.

- Purchase of $3,000 raw materials inventory

- Assignment of $700 of raw materials inventory to Job 7

- Payroll for 10 hours and $3,000 is assigned to Job 7

- Factory depreciation of $1,750

- Overhead applied at the rate of $200 per hour

What is the cost assigned to Job 7 at the end of the week?

(Figure)During the month, Job Arch2 used specialized machinery for 350 hours and incurred $700 in utilities on account, $400 in factory depreciation expense, and $200 in property tax on the factory. Prepare journal entries for the following:

- Record the expenses incurred.

- Record the allocation of overhead at the predetermined rate of $1.50 per machine hour.

(Figure)Job 113 was completed at a cost of $7,500, and Job 85 was completed at a cost of $2,300 and sold on account for $4,500. Prepare journal entries for the following:

- Completion of Job 113.

- Completion and sale of Job 85.

(Figure)A company’s individual job sheets show these costs:

Overhead is applied at 1.75 times the direct labor cost. Use the data on the cost sheets to perform these tasks:

- Apply overhead to each of the jobs.

- Prepare an entry to record the assignment of direct material to work in process.

- Prepare an entry to record the assignment of direct labor to work in process.

- Prepare an entry to record the assignment of manufacturing overhead to work in process.

(Figure)A summary of materials requisition slips and time tickets, along with the overhead allocation, show these costs:

- Prepare an entry to record the assignment of direct material to work in process.

- Prepare an entry to record the assignment of direct labor to work in process.

- Prepare an entry to record the assignment of manufacturing overhead to work in process.

(Figure)The following data summarize the operations during the year. Prepare a journal entry for each transaction.

- Purchase of raw materials on account: $3,000

- Raw materials used by Job 1: $500

- Raw materials used as indirect materials: $100

- Direct labor for Job 1: $300

- Indirect labor incurred: $50

- Factory utilities incurred on account: $700

- Adjusting entry for factory depreciation: $250

- Manufacturing overhead applied as percent of direct labor: 200%

- Job 1 is transferred to finished goods

- Job 1 is sold: $3,000

- Manufacturing overhead is overapplied: $100

(Figure)The following events occurred during March for Ajax Company. Prepare a journal entry for each transaction.

- Materials were purchased on account for $35,429.

- Materials were requisitioned to begin work on Job C15 in the amount of $25,259.

- Direct labor expense for Job C15 was $24,129.

- Actual overhead was incurred on account of $32,852.

- Factory overhead was charged to Job C15 at the rate of 200% of direct labor.

- Job C15 was transferred to finished goods at $97,646.

- Job C15 was sold on account for $401,000.

(Figure)The following data summarize the operations during the year. Prepare a journal entry for each transaction.

- Purchase of raw materials on account: $1,500

- Raw materials used by Job 1: $400

- Raw materials used as indirect materials: $50

- Direct labor for Job 1: $200

- Indirect labor incurred for Job 1: $30

- Factory utilities incurred on account: $500

- Adjusting entry for factory depreciation: $200

- Manufacturing overhead applied as percent of direct labor: 100%

- Job 1 is transferred to finished goods

- Job 1 is sold: $1,000

- Manufacturing overhead is underapplied: $100

(Figure)The following events occurred during March for Ajax Company. Prepare a journal entry for each transaction.

- Materials were purchased on account for $5,429.

- Materials were requisitioned to begin work on Job C15 in the amount of $2,500.

- Direct labor expense for Job C15 was $4,250.

- Actual overhead was incurred on account for $5,385.

- Factory overhead was charged to Job C15 at the rate of 200% direct labor.

- Job C15 was transferred to finished goods at $15,250.

- Job C15 was sold on account for $28,000.

(Figure)How do the job cost sheets act as a subsidiary ledger for the work in process inventory if journal entries are not made to the job cost sheets?