Use the Ledger Balances to Prepare an Adjusted Trial Balance

Mitchell Franklin; Patty Graybeal; and Dixon Cooper

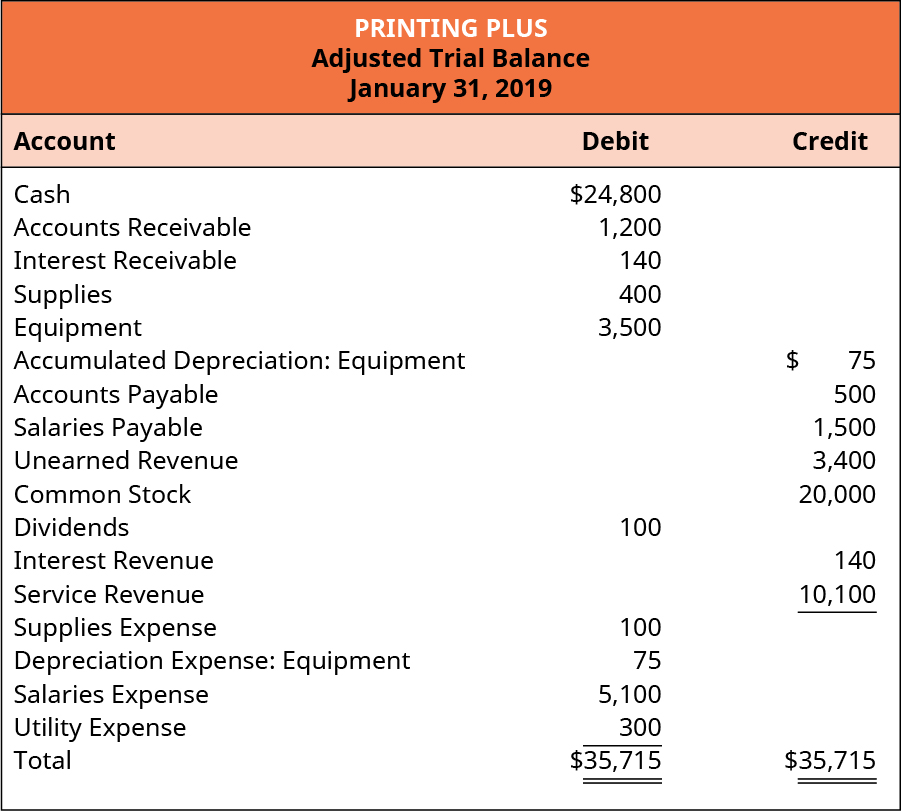

Once all of the adjusting entries have been posted to the general ledger, we are ready to start working on preparing the adjusted trial balance. Preparing an adjusted trial balance is the sixth step in the accounting cycle. An adjusted trial balance is a list of all accounts in the general ledger, including adjusting entries, which have nonzero balances. This trial balance is an important step in the accounting process because it helps identify any computational errors throughout the first five steps in the cycle.

As with the unadjusted trial balance, transferring information from T-accounts to the adjusted trial balance requires consideration of the final balance in each account. If the final balance in the ledger account (T-account) is a debit balance, you will record the total in the left column of the trial balance. If the final balance in the ledger account (T-account) is a credit balance, you will record the total in the right column.

Once all ledger accounts and their balances are recorded, the debit and credit columns on the adjusted trial balance are totaled to see if the figures in each column match. The final total in the debit column must be the same dollar amount that is determined in the final credit column.

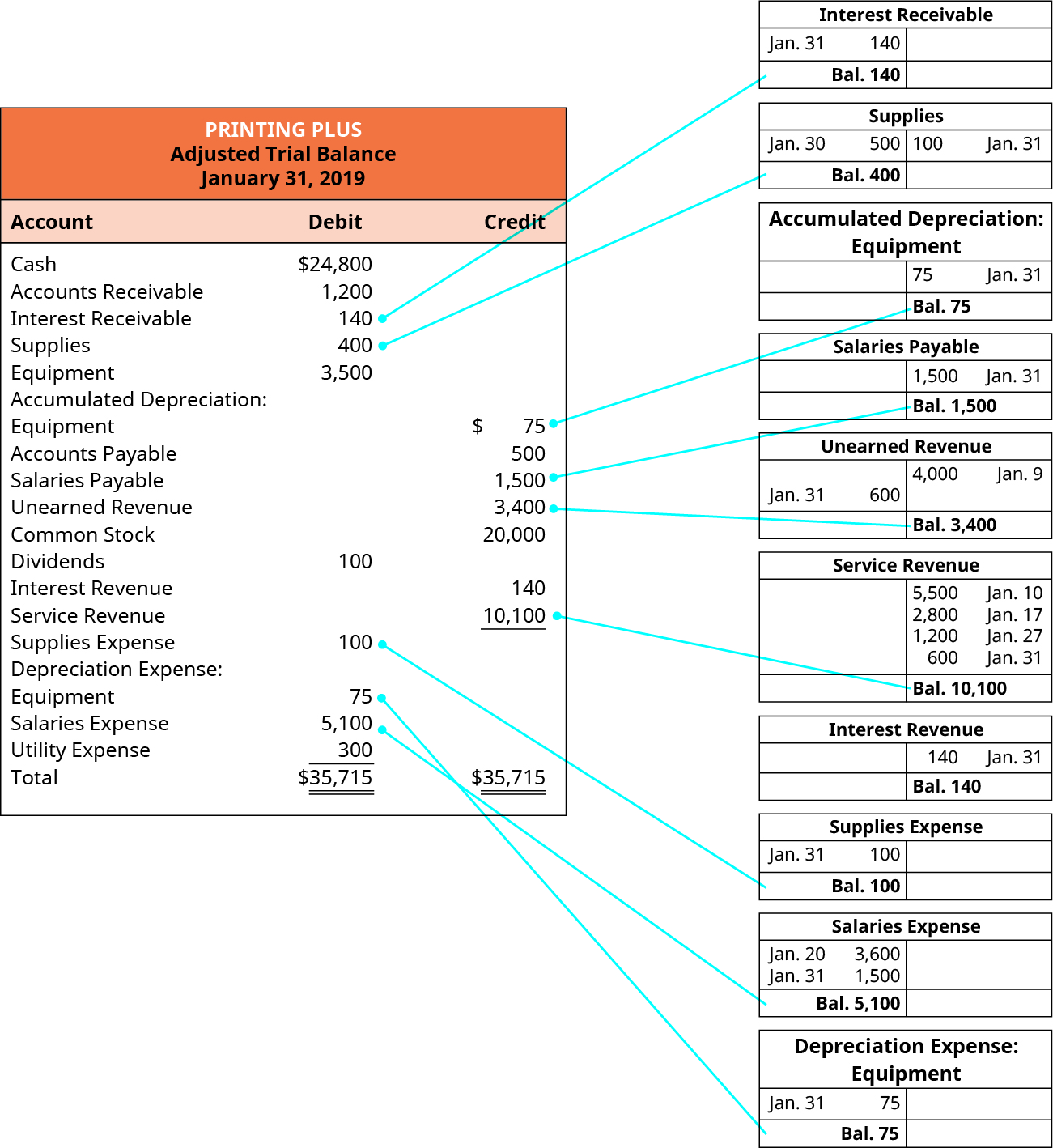

Let’s now take a look at the adjusted T-accounts and adjusted trial balance for Printing Plus to see how the information is transferred from these T-accounts to the adjusted trial balance. We only focus on those general ledger accounts that had balance adjustments.

For example, Interest Receivable is an adjusted account that has a final balance of $140 on the debit side. This balance is transferred to the Interest Receivable account in the debit column on the adjusted trial balance. Supplies ($400), Supplies Expense ($100), Salaries Expense ($5,100), and Depreciation Expense–Equipment ($75) also have debit final balances in their adjusted T-accounts, so this information will be transferred to the debit column on the adjusted trial balance. Accumulated Depreciation–Equipment ($75), Salaries Payable ($1,500), Unearned Revenue ($3,400), Service Revenue ($10,100), and Interest Revenue ($140) all have credit final balances in their T-accounts. These credit balances would transfer to the credit column on the adjusted trial balance.

Once all balances are transferred to the adjusted trial balance, we sum each of the debit and credit columns. The debit and credit columns both total $35,715, which means they are equal and in balance.

After the adjusted trial balance is complete, we next prepare the company’s financial statements.

You are a new accountant at a salon. The salon had previously used cash basis accounting to prepare its financial records but now considers switching to an accrual basis method. You have been tasked with determining if this transition is appropriate.

When you go through the records you notice that this transition will greatly impact how the salon reports revenues and expenses. The salon will now report some revenues and expenses before it receives or pays cash.

How will change positively impact its business reporting? How will it negatively impact its business reporting? If you were the accountant, would you recommend the salon transition from cash basis to accrual basis?

As you have learned, the adjusted trial balance is an important step in the accounting process. But outside of the accounting department, why is the adjusted trial balance important to the rest of the organization? An employee or customer may not immediately see the impact of the adjusted trial balance on his or her involvement with the company.

The adjusted trial balance is the key point to ensure all debits and credits are in the general ledger accounts balance before information is transferred to financial statements. Financial statements drive decision-making for a business. Budgeting for employee salaries, revenue expectations, sales prices, expense reductions, and long-term growth strategies are all impacted by what is provided on the financial statements.

So if the company skips over creating an adjusted trial balance to make sure all accounts are balanced or adjusted, it runs the risk of creating incorrect financial statements and making important decisions based on inaccurate financial information.

Key Concepts and Summary

- Adjusted trial balance: The adjusted trial balance lists all accounts in the general ledger, including adjusting entries, which have nonzero balances. This trial balance is an important step in the accounting process because it helps identify any computational errors throughout the first five steps in the cycle.

Multiple Choice

(Figure)What critical purpose does the adjusted trial balance serve?

- It proves that transactions have been posted correctly

- It is the source document from which to prepare the financial statements

- It shows the beginning balances of every account, to be used to start the new year’s records

- It proves that all journal entries have been made correctly.

(Figure)Which of the following accounts’ balance would be a different number on the Balance Sheet than it is on the adjusted trial balance?

- accumulated depreciation

- unearned service revenue

- retained earnings

- dividends

C

Questions

(Figure)What is the difference between the trial balance and the adjusted trial balance?

The adjusted trial balance is the summary of account balances after the adjustments have been posted, so it reflects the corrected balances of all accounts.

(Figure)Why is the adjusted trial balance trusted as a reliable source for building the financial statements?

Exercise Set A

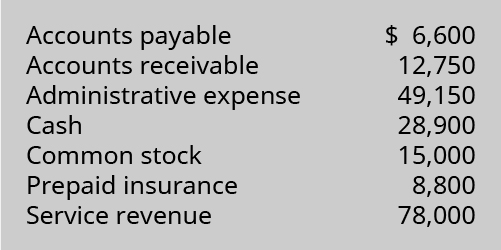

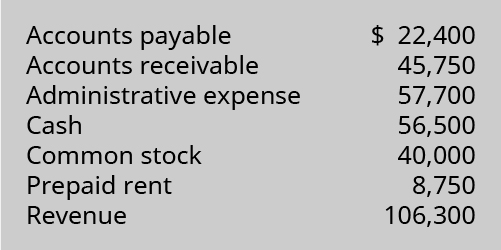

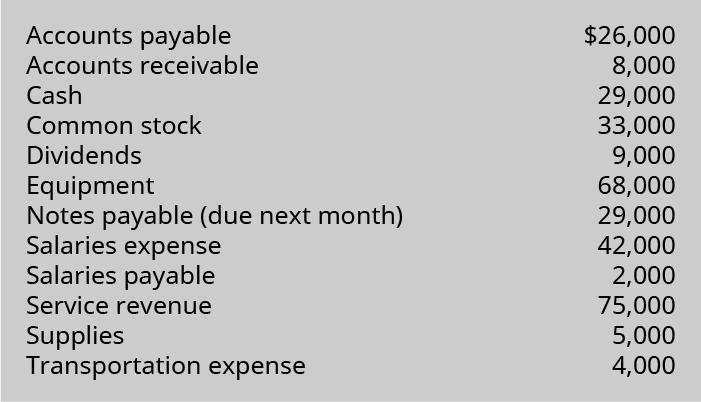

(Figure)Prepare an adjusted trial balance from the following adjusted account balances (assume accounts have normal balances).

(Figure)Prepare an adjusted trial balance from the following account information, considering the adjustment data provided (assume accounts have normal balances).

Adjustments needed:

Salaries due to administrative employees, but unpaid at period end, $2,000

Insurance still unexpired at end of the period, $12,000

Exercise Set B

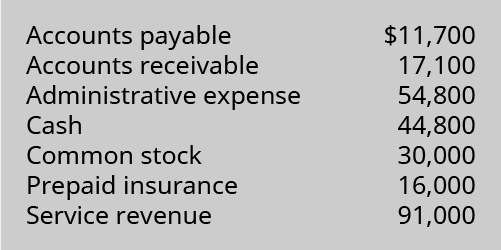

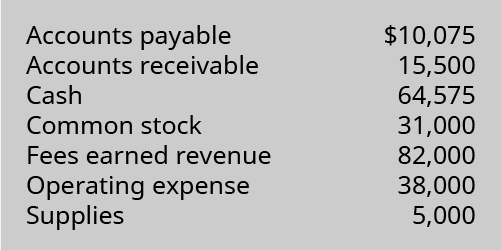

(Figure)Prepare an adjusted trial balance from the following adjusted account balances (assume accounts have normal balances).

(Figure)Prepare an adjusted trial balance from the following account information, considering the adjustment data provided (assume accounts have normal balances).

Adjustments needed:

- Physical count of supplies inventory remaining at end of period, $2,150

- Taxes payable at end of period, $3,850

Problem Set A

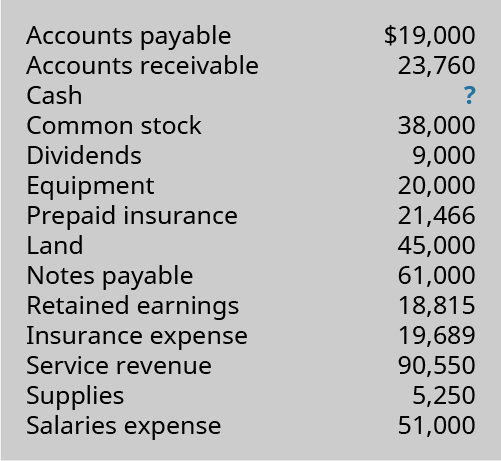

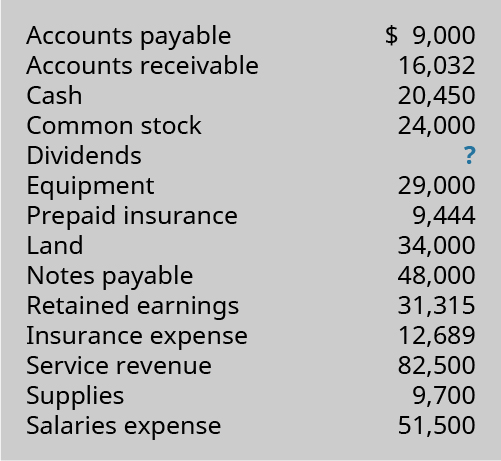

(Figure)Prepare an adjusted trial balance from the adjusted account balances; solve for the one missing account balance: Cash (assume accounts have normal balances).

(Figure)Prepare an adjusted trial balance from the following account information, considering the adjustment data provided (assume accounts have normal balances). Equipment was recently purchased, so there is neither depreciation expense nor accumulated depreciation.

Adjustments needed:

- Salaries due to employees, but unpaid at the end of the period, $2,000

- Insurance still unexpired at end of the period, $12,000

(Figure)Prepare an adjusted trial balance from the following account information, and also considering the adjustment data provided (assume accounts have normal balances). Equipment was recently purchased, so there is neither depreciation expense nor accumulated depreciation.

Adjustments needed:

- Remaining unpaid Salaries due to employees at the end of the period, $0

- Accrued Interest Payable at the end of the period, $7,700

Problem Set B

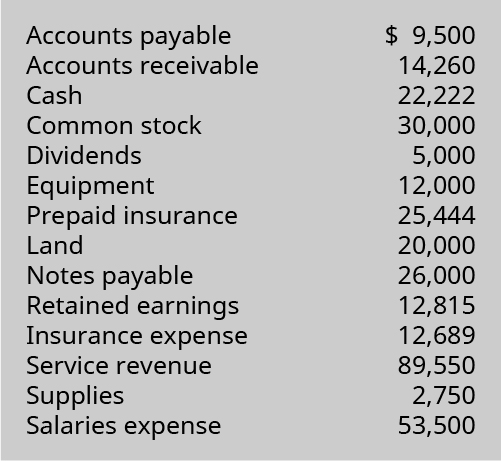

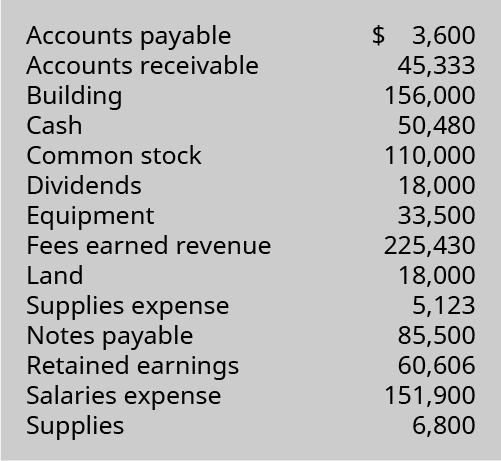

(Figure)Prepare an adjusted trial balance from the adjusted account balances; solve for the one missing account balance: Dividends (assume accounts have normal balances). Equipment was recently purchased, so there is neither depreciation expense nor accumulated depreciation.

(Figure)Prepare an adjusted trial balance from the following account information, considering the adjustment data provided (assume accounts have normal balances). Building and Equipment were recently purchased, so there is neither depreciation expense nor accumulated depreciation.

Adjustments needed:

- Physical count of supplies inventory remaining at end of period, $3,300

- Customer fees collected in advance (payments were recorded as Fees Earned), $18,500

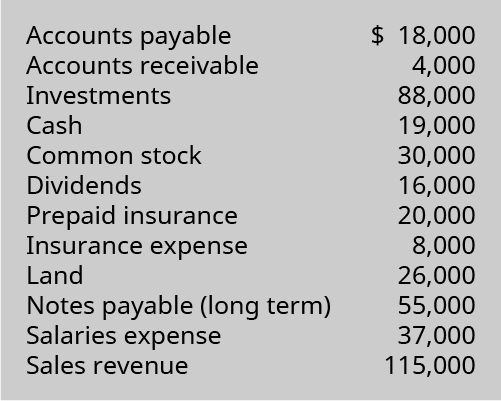

(Figure)Prepare an adjusted trial balance from the following account information, and also considering the adjustment data provided (assume accounts have normal balances).

Adjustments needed:

- Accrued interest revenue on investments at period end, $2,200

- Insurance still unexpired at end of the period, $12,000

Thought Provokers

(Figure)Assume you are employed as the chief financial officer of a corporation and are responsible for preparation of the financial statements, including the adjusting process and preparation of the adjusted trial balance. The company is facing a slow year, and after your adjusting entries, the financial statements are accurately reflecting that fact. However, as you are discussing the matter with your boss, the chief executive officer (CEO), he suggests that you have the power to make further adjustments to the statements, and that you should use that power to “adjust” the profits and equity into a stronger position, so that investor confidence in the company’s prospects will be restored.

Write a short memo to the CEO, stating your intentions about what you can and/or will do to make the financial statements more appealing. Be specific about any planned adjustments that could be made, assuming that normal period-end adjustments have already been reflected accurately in the financial statements that you prepared.

Glossary

- adjusted trial balance

- list of all accounts in the general ledger, including adjusting entries, which have nonzero balances