Define the Purpose and Use of a Petty Cash Fund, and Prepare Petty Cash Journal Entries

Mitchell Franklin; Patty Graybeal; and Dixon Cooper

As we have discussed, one of the hardest assets to control within any organization is cash. One way to control cash is for an organization to require that all payments be made by check. However, there are situations in which it is not practical to use a check. For example, imagine that the Galaxy’s Best Yogurt runs out of milk one evening. It is not possible to operate without milk, and the normal shipment does not come from the supplier for another 48 hours. To maintain operations, it becomes necessary to go to the grocery store across the street and purchase three gallons of milk. It is not efficient for time and cost to write a check for this small purchase, so companies set up a petty cash fund, which is a predetermined amount of cash held on hand to be used to make payments for small day-to-day purchases. A petty cash fund is a type of imprest account, which means that it contains a fixed amount of cash that is replaced as it is spent in order to maintain a set balance.

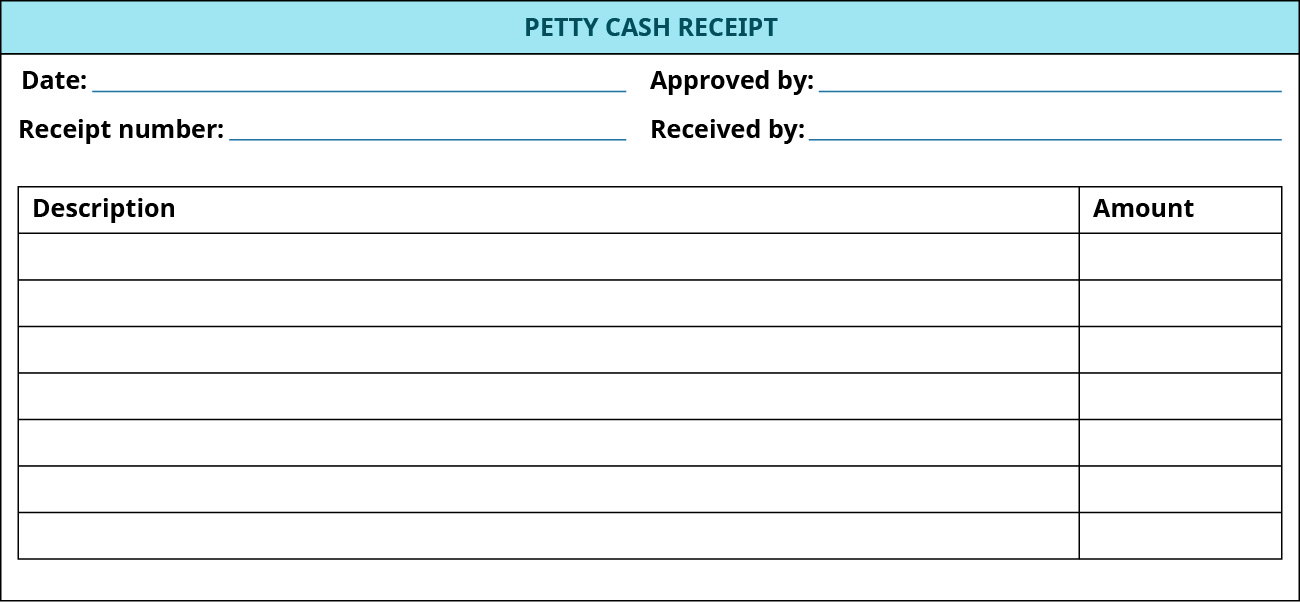

To maintain internal controls, managers can use a petty cash receipt ((Figure)), which tracks the use of the cash and requires a signature from the manager.

As cash is spent from a petty cash fund, it is replaced with a receipt of the purchase. At all times, the balance in the petty cash box should be equal to the cash in the box plus the receipts showing purchases.

For example, the Galaxy’s Best Yogurt maintains a petty cash box with a stated balance of $75 at all times. Upon review of the box, the balance is counted in the following way.

Because there may not always be a manager with check signing privileges available to sign a check for unexpected expenses, a petty cash account allows employees to make small and necessary purchases to support the function of a business when it is not practical to go through the formal expense process. In all cases, the amount of the purchase using petty cash would be considered to not be material in nature. Recall that materiality means that the dollar amount in question would have a significant impact in financial results or influence investor decisions.

Demonstration of Typical Petty Cash Journal Entries

Petty cash accounts are managed through a series of journal entries. Entries are needed to (1) establish the fund, (2) increase or decrease the balance of the fund (replenish the fund as cash is used), and (3) adjust for overages and shortages of cash. Consider the following example.

The Galaxy’s Best Yogurt establishes a petty cash fund on July 1 by cashing a check for $75 from its checking account and placing cash in the petty cash box. At this point, the petty cash box has $75 to be used for small expenses with the authorization of the responsible manager. The journal entry to establish the petty cash fund would be as follows.

As this petty cash fund is established, the account titled “Petty Cash” is created; this is an asset on the balance sheet of many small businesses. In this case, the cash account, which includes checking accounts, is decreased, while the funds are moved to the petty cash account. One asset is increasing, while another asset is decreasing by the same account. Since the petty cash account is an imprest account, this balance will never change and will remain on the balance sheet at $75, unless management elects to change the petty cash balance.

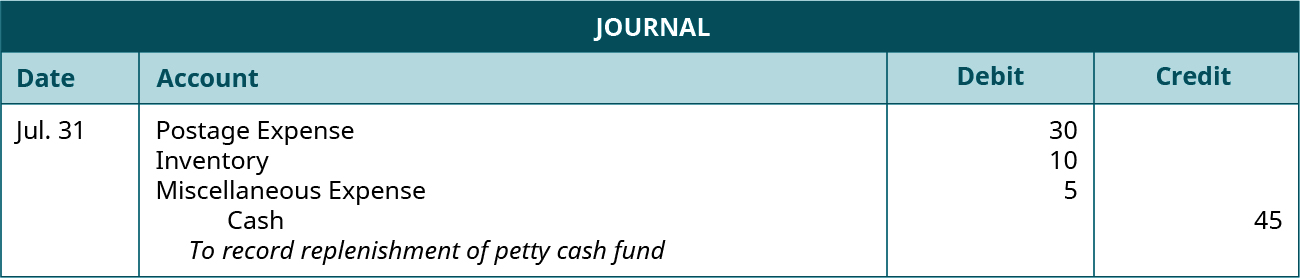

Throughout the month, several payments are made from the petty cash account of the Galaxy’s Best Yogurt. Assume the following activities.

At the end of July, in the petty cash box there should be a receipt for the postage stamp purchase, a receipt for the milk, a receipt for the window cleaner, and the remaining cash. The employee in charge of the petty cash box should sign each receipt when the purchase is made. The total amount of purchases from the receipts ($45), plus the remaining cash in the box should total $75. As the receipts are reviewed, the box must be replenished for what was spent during the month. The journal entry to replenish the petty cash account will be as follows.

Typically, petty cash accounts are reimbursed at a fixed time period. Many small businesses will do this monthly, which ensures that the expenses are recognized within the proper accounting period. In the event that all of the cash in the account is used before the end of the established time period, it can be replenished in the same way at any time more cash is needed. If the petty cash account often needs to be replenished before the end of the accounting period, management may decide to increase the cash balance in the account. If, for example, management of the Galaxy’s Best Yogurt decides to increase the petty cash balance to $100 from the current balance of $75, the journal entry to do this on August 1 would be as follows.

If the management at a later date decides to decrease the balance in the petty cash account, the previous entry would be reversed, with cash being debited and petty cash being credited.

Occasionally, errors may occur that affect the balance of the petty cash account. This may be the result of an employee not getting a receipt or getting back incorrect change from the store where the purchase was made. In this case, an expense is created that creates a cash overage or shortage.

Consider Galaxy’s expenses for July. During the month, $45 was spent on expenses. If the balance in the petty cash account is supposed to be $75, then the petty cash box should contain $45 in signed receipts and $30 in cash. Assume that when the box is counted, there are $45 in receipts and $25 in cash. In this case, the petty cash balance is $70, when it should be $75. This creates a $5 shortage that needs to be replaced from the checking account. The entry to record a cash shortage is as follows.

When there is a shortage of cash, we record the shortage as a “debit” and this has the same effect as an expense. If we have an overage of cash, we record the overage as a credit, and this has the same impact as if we are recording revenue. If there were cash overage, the petty cash account would be debited and the cash over and short account would be credited. In this case, the expense balance decreases, and the year-end balance is the net balance from all overages and shortages during the year.

If a petty cash account is consistently short, this may be a warning sign that there is not a proper control of the account, and management may want to consider additional controls to better monitor petty cash.

A petty cash system in some businesses may be replaced by use of a prepaid credit card (or debit card) on site. What would be the pros and cons of actually maintaining cash on premises for the petty cash system, versus a rechargeable debit card that employees may use for petty cash purposes? Which option would you select for your petty cash account if you were the owner of a small business?

See this article on tips for companies to establish and manage petty cash systems to learn more.

Key Concepts and Summary

- The purpose of a petty cash fund is to make payments for small amounts that are immaterial, such as postage, minor repairs, or day-to-day supplies.

- A petty cash account is an imprest account, so it is only debited when the fund is initially established or increased in amount. Transactions to replenish the account involve a debit to the expenses and a credit to the cash account (e.g., bank account).

(Figure)What is the best way for owners of small businesses to maintain proper internal controls?

- The owner must have enough knowledge of all aspects of the company and have controls in place to track all assets.

- Small businesses do not need to worry about internal controls.

- Small businesses should make one of their employees in charge of all aspects of the company, giving the owner the ability to run the company and generate sales.

- Only managers need to be concerned about internal controls.

A

(Figure)Which of the following is not considered to be part of the internal control structure of a company?

- Ensure that assets are kept secure.

- Monitor operations of the organization to ensure maximum efficiency.

- Publish accurate financial statements on a regular basis.

- Ensure assets are properly used.

(Figure)There are several elements to internal controls. Which of the following would not address the issue of having cash transactions reported in the accounting records?

- One employee would have access to the cash register.

- The cash drawer should be closed out, and cash and the sales register should be reconciled on a prenumbered form.

- Ask customers to report to a manager if they do not receive a sales receipt or invoice.

- The person behind the cash register should also be responsible for making price adjustments.

D

(Figure)A company is trying to set up proper internal controls for their accounts payable/inventory purchasing system. Currently the purchase order is generated by the same person who receives the inventory. Together the purchase order and the receiving ticket are sent to accounts payable for payment. What changes would you make to improve the internal control structure?

- No changes would be made since the person paying the bills is different from the person ordering the inventory.

- The person in accounts payable should generate the purchase order.

- The person in accounts payable should generate the receiving ticket once the invoice from the supplier is received.

- The responsibilities of generating the purchase order and receiving the inventory should be separated among two different people.

(Figure)There are three employees in the accounting department: payroll clerk, accounts payable clerk, and accounts receivable clerk. Which one of these employees should not make the daily deposit?

- payroll clerk

- account payable clerk

- accounts receivable clerk

- none of them

C

(Figure)Which one of the following documents is not needed to process a payment to a vendor?

- vendor invoice

- packing slip

- check request

- purchase order

(Figure)What is the advantage of using technology in the internal control system?

- Passwords can be used to allow access by employees.

- Any cash received does not need to be reconciled because the computer tracks all transactions.

- Transactions are easily changed.

- Employees cannot steal because all cash transactions are recorded by the computer/cash register.

A

(Figure)Which of the following assets require the strongest of internal controls?

- inventory

- credit cards

- computer equipment

- cash

(Figure)Discuss the importance of a company having proper insurance and bonding its employees.

(Figure)On June 1 French company has decided to initiate a petty cash fund in the amount of $800. Prepare journal entries for the following transactions:

- On June 5, the petty cash fund needed replenishment, and the following are the receipts: Auto Expense $37, Supplies $124, Postage Expense $270, Repairs and Maintenance Expense $168, Miscellaneous Expense $149. The cash on hand at this time was $48.

- On June 14, the petty cash fund needed replenishment, and the following are the receipts: Auto Expense $18, Supplies $175, Postage Expense $50, Repairs and Maintenance Expense $269, Miscellaneous Expense $59. The cash on hand at this time was $220.

- On June 23, the petty cash fund needed replenishment, and the following are the receipts: Auto Expense $251, Supplies $88, Postage Expense $63, Repairs and Maintenance Expense $182, Miscellaneous Expense $203. The cash on hand at this time was $20.

- On June 29, the company determined that the petty cash fund needed to be increased to $1,000.

- On June 30, the petty cash fund needed replenishment, as it was month end. The following are the receipts: Auto Expense $18, Supplies $175, Postage Expense $50, Repairs and Maintenance Expense $269, Miscellaneous Expense $59. The cash on hand at this time was $437.

(Figure)On July 2 Kellie Company has decided to initiate a petty cash fund in the amount of $1,200. Prepare journal entries for the following transactions:

- On July 5, the petty cash fund needed replenishment, and the following are the receipts: Auto Expense $125, Supplies $368, Postage Expense $325, Repairs and Maintenance Expense $99, Miscellaneous Expense $259. The cash on hand at this time was $38.

- On June 14, the petty cash fund needed replenishment, and the following are the receipts: Auto Expense $425, Supplies $95, Postage Expense $240, Repairs and Maintenance Expense $299, Miscellaneous Expense $77. The cash on hand at this time was $110.

- On June 23, the petty cash fund needed replenishment and the following are the receipts: Auto Expense $251, Supplies $188, Postage Expense $263, Repairs and Maintenance Expense $182, Miscellaneous Expense $203. The cash on hand at this time was $93.

- On June 29, the company determined that the petty cash fund needed to be decreased to $1,000.

- On June 30, the petty cash fund needed replenishment, as it was month end. The following are the receipts: Auto Expense $14, Supplies $75, Postage Expense $150, Repairs and Maintenance Expense $121, Miscellaneous Expense $39. The cash on hand at this time was $603.

(Figure)Hajun Company started its business on May 1, 2019. The following transactions occurred during the month of May. Prepare the journal entries in the journal on Page 1.

- The owners invested $5,000 from their personal account to the business account.

- Paid rent $400 with check #101.

- Initiated a petty cash fund $200 check #102.

- Received $400 cash for services rendered

- Purchased office supplies for $90 with check #103.

- Purchased computer equipment $1,000 , paid $350 with check #104 and will pay the remainder in 30 days.

- Received $500 cash for services rendered.

- Paid wages $250, check #105.

- Petty cash reimbursement office supplies $25, Maintenance Expense $125, Miscellaneous Expense $35. Cash on hand $18. Check #106.

- Increased Petty Cash by $50, check #107.

(Figure)Lavender Company started its business on April 1, 2019. The following are the transactions that happened during the month of April. Prepare the journal entries in the journal on Page 1.

- The owners invested $7,500 from their personal account to the business account.

- Paid rent $600 with check #101.

- Initiated a petty cash fund $250 check #102.

- Received $350 cash for services rendered.

- Purchased office supplies for $125 with check #103.

- Purchased computer equipment $1,500, paid $500 with check #104, and will pay the remainder in 30 days.

- Received $750 cash for services rendered.

- Paid wages $375, check #105.

- Petty cash reimbursement Office Supplies $50, Maintenance Expense $80, Miscellaneous Expense $60. Cash on hand $8. Check #106.

- Increased Petty Cash by $70, check #107.

(Figure)A manufacturing plant was finding a huge increase in the scrapping of raw materials. Its internal controls were reviewed, and the plant appeared to be strong; segregation of duties was in place. As the accountant was reconciling some inventory accounts, she found more than a normal amount of scrap tickets. The tickets were for scrapping the same inventory part, signed by the same person, and the scrap was sold to only one company. The inventory item was still being ordered, and only one supplier was used to purchase the parts. After further investigation by the accountant, the company buying the inventory and the company selling the inventory to the company had different names but shared the same address. Comment on what went wrong. What happened to the internal controls the company had in place?

(Figure)The vice president of finance asks the accounts payable (AP) clerk to write a check in the name of the president for $10,000. He and the president will sign the check (two signatures needed on a check of this size). He further instructs the AP clerk not to disclose this check to her immediate supervisor. What should the AP clerk do? Should she prepare the check? Should she inform her immediate supervisor? Discuss with internal controls in mind.

(Figure)Even though technology has improved the internal control structure of a company, a supervisor cannot depend totally on technology. Discuss other internal controls a supervisor needs to implement to ensure a strong structure.

Glossary

- petty cash fund

- amount of cash held on hand to be used to make payments for small day-to-day purchases

- imprest account

- account that is only debited when the account is established or the total ending balance is increased