LO 14.4 Prepare the Completed Statement of Cash Flows Using the Indirect Method

Mitchell Franklin

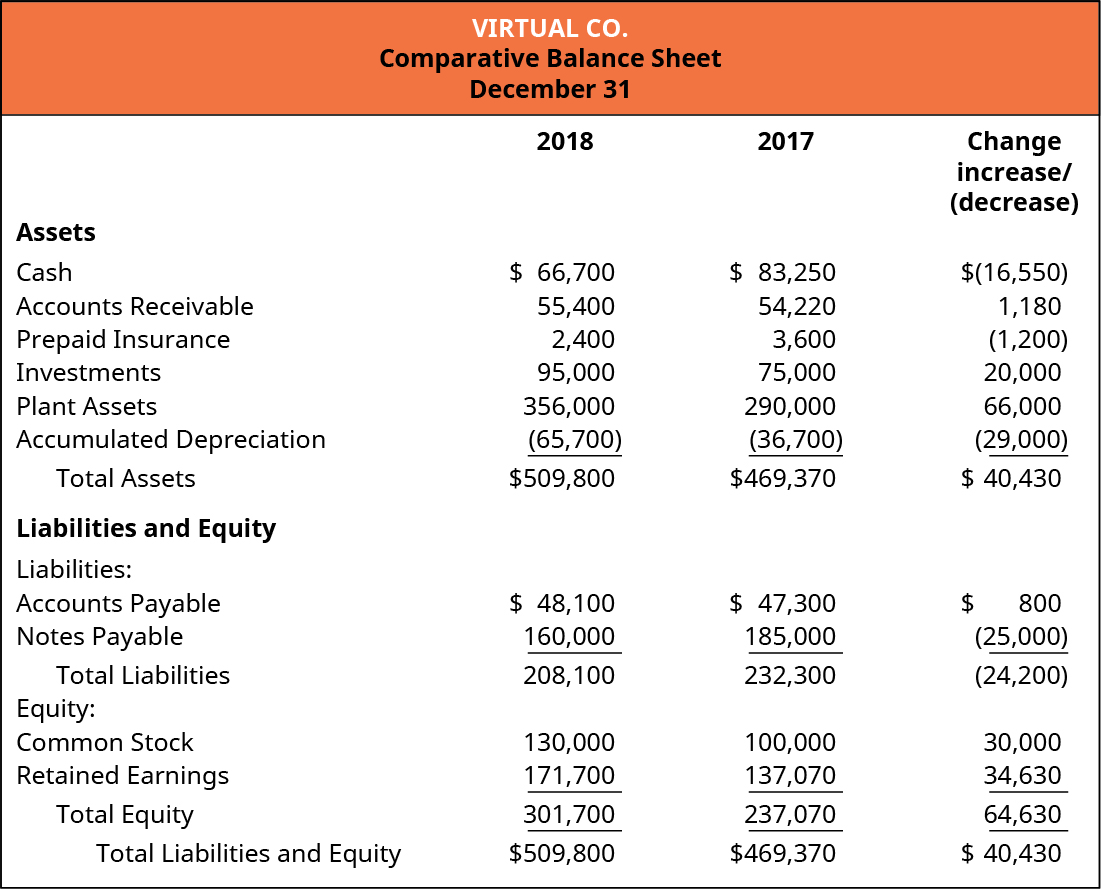

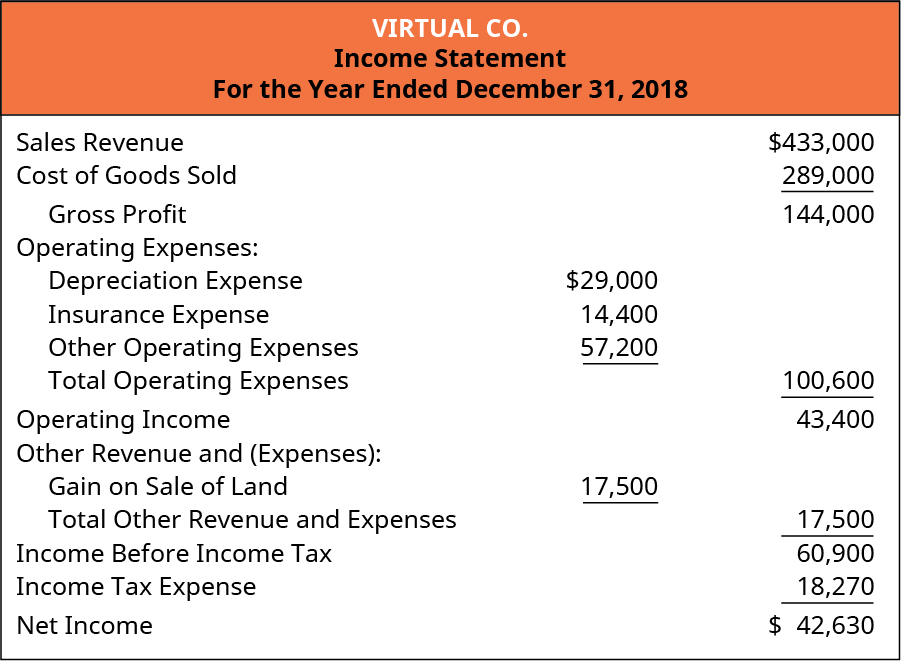

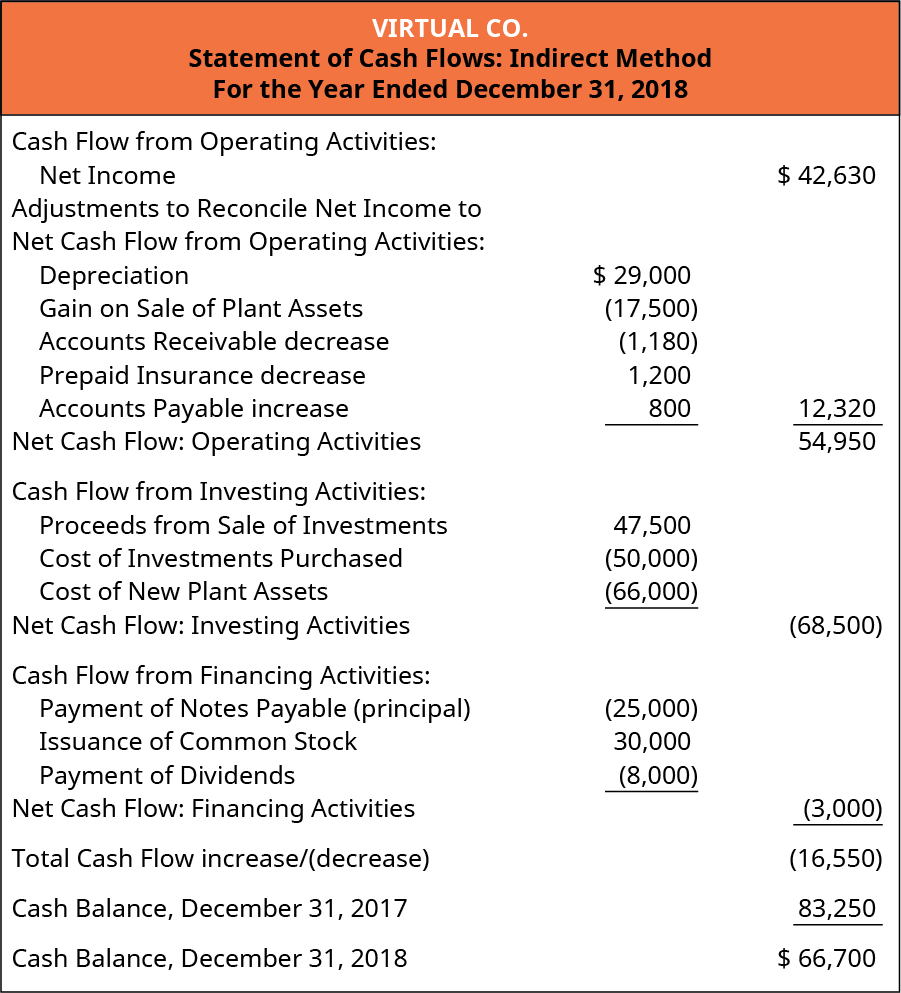

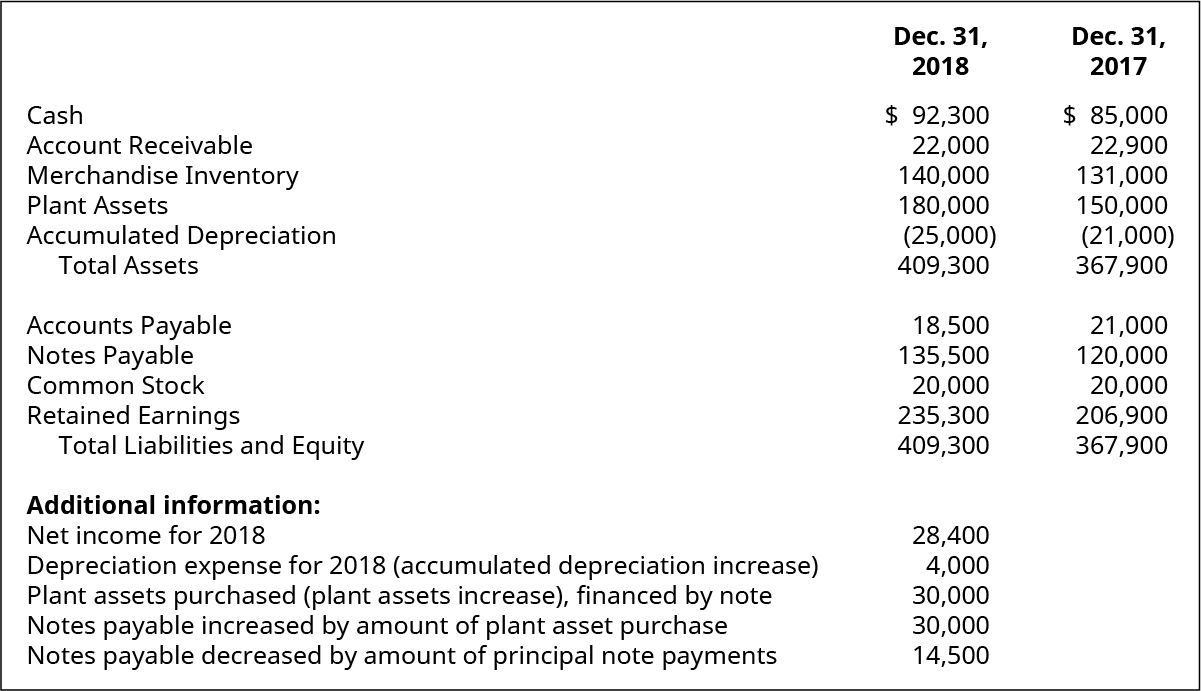

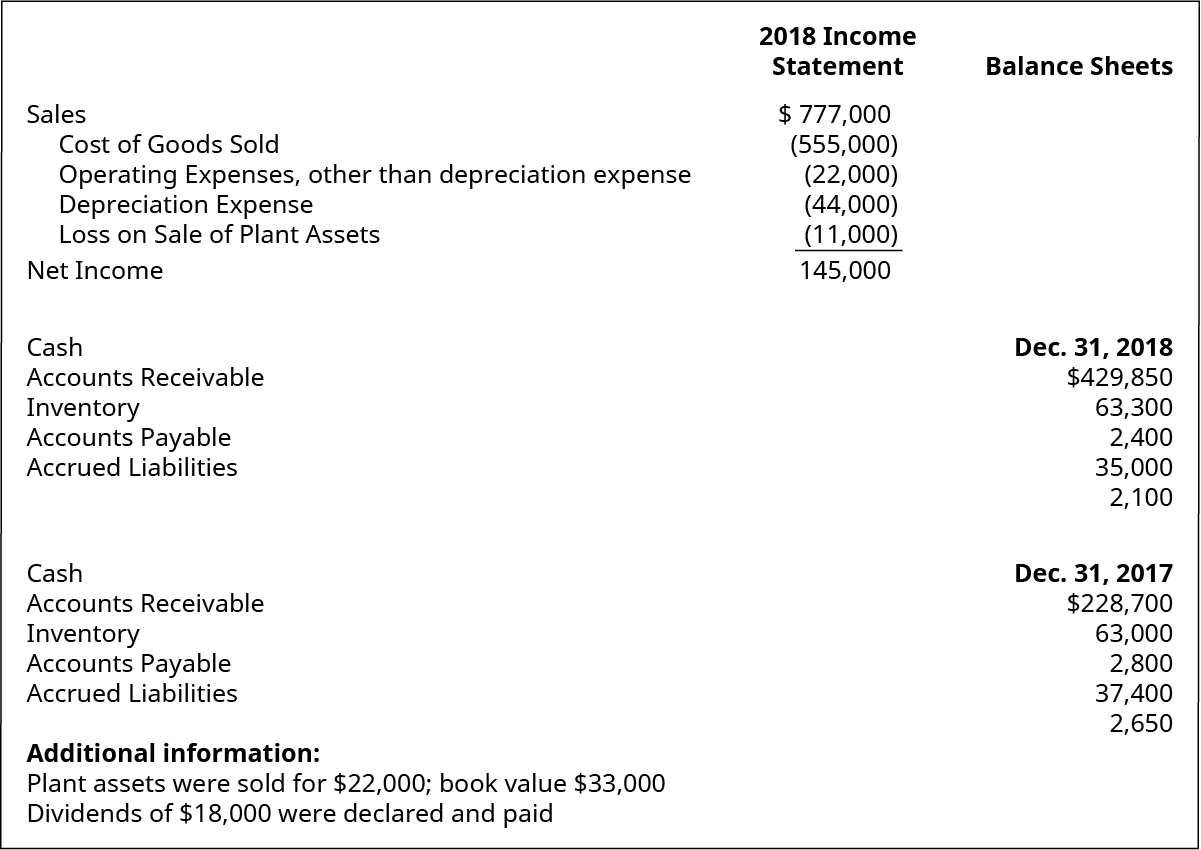

In this section, we use the example of Virtual Co. to work through the entire process of preparing the company’s statement of cash flows using the indirect method. Virtual’s comparative balance sheet and income statement are provided as a base for the preparation of the statement of cash flows.

Review Problem: Preparing the Virtual Co. Statement of Cash Flows

Additional Information

The following additional information is provided:

- Investments that originally cost $30,000 were sold for $47,500 cash.

- Investments were purchased for $50,000 cash.

- Plant assets were purchased for $66,000 cash.

- Cash dividends were declared and paid to shareholders in the amount of $8,000.

Directions:

Prepare the statement of cash flows (indirect method), for the year ended December 31, 2018.

Key Concepts and Summary

- Preparing the operating section of statement of cash flows by the indirect method starts with net income from the income statement and adjusts for items that affect cash flows differently than they affect net income.

- Multiple levels of adjustments are required to reconcile accrual-based net income to cash flows from operating activities.

- The investing section of the statement of cash flows relates to changes in long-term assets.

- The financing section of statement of cash flows relates to changes in long-term liabilities and changes in equity.

- Company activities that reflect changes in long-term assets, long-term liabilities, or equity, but have no cash impact, require special reporting treatment, as noncash investing and financing transactions.

Multiple Choice

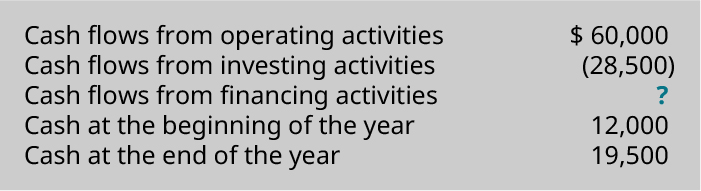

(Figure)If beginning cash equaled $10,000 and ending cash equals $19,000, which is true?

- Operating cash flow 9,000; Investing cash flow (3,500); Financing cash flow (2,500)

- Operating cash flow 4,500; Investing cash flow 9,000; Financing cash flow (4,500)

- Operating cash flow 2,000; Investing cash flow (13,000); Financing cash flow 2,000

- none of the above

Questions

(Figure)Is there any significance that can be attributed to whether net cash flows are generated from operating activities, versus investing and/or financing activities? Explain.

(Figure)Would there ever be activities that relate to operating, investing, or financing activities that would not be reported in their respective sections of the statement of cash flows? Explain. If a company had any such activities, how would they be reported in the financial statements, if at all?

Yes. Some investing and/or financing transactions do not have a cash impact initially. Examples include purchases of long-term assets that are paid for with long-term debt financing, acquisitions of long-term assets in exchange for corporate stock, and repayment of long-term debt using noncash assets. These noncash investing/financing activities would be reported in the notes to the financial statements, or as a notation on the bottom of the statement of cash flows, but not considered an integral part of the statement.

Exercise Set A

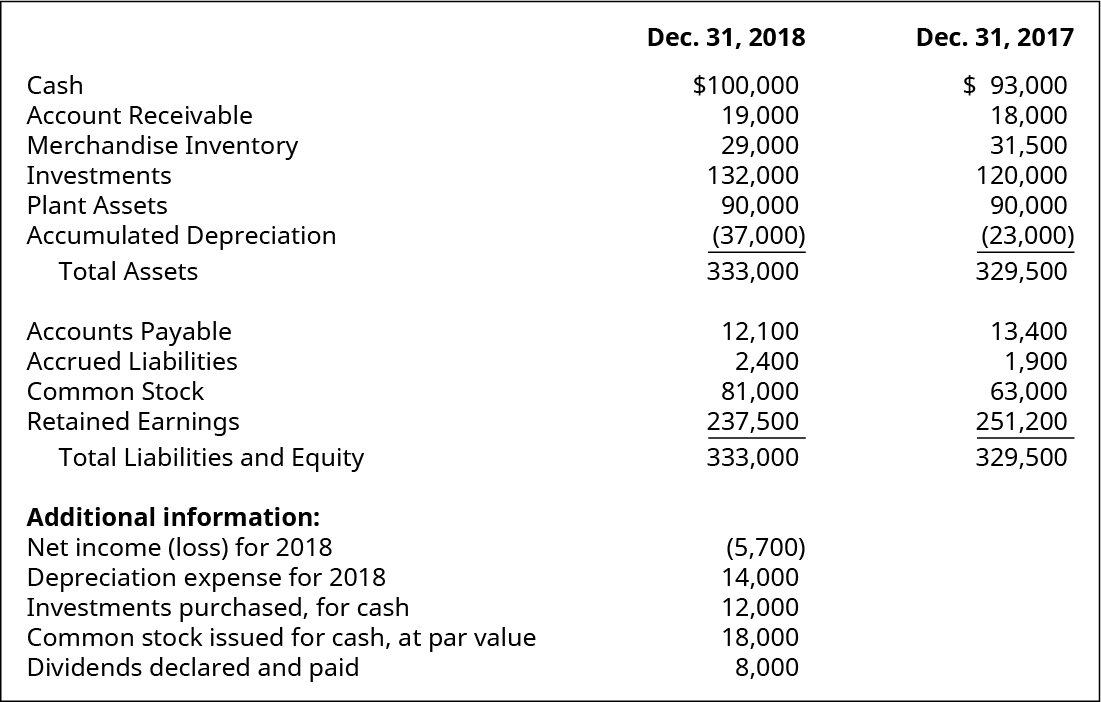

(Figure)Provide the missing piece of information for the following statement of cash flows puzzle.

(Figure)Provide the missing piece of information for the following statement of cash flows puzzle.

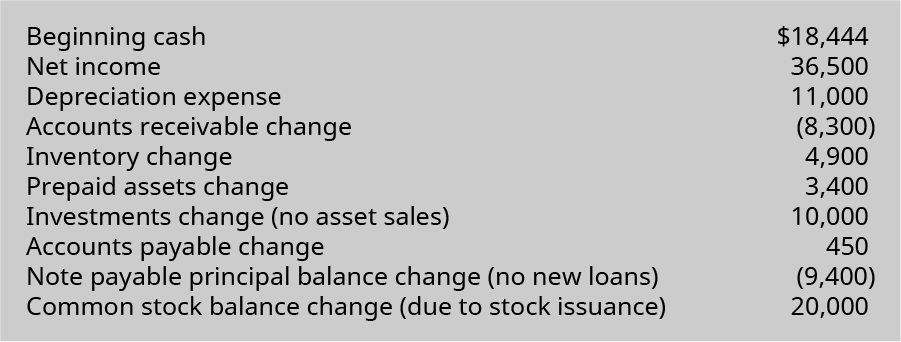

Exercise Set B

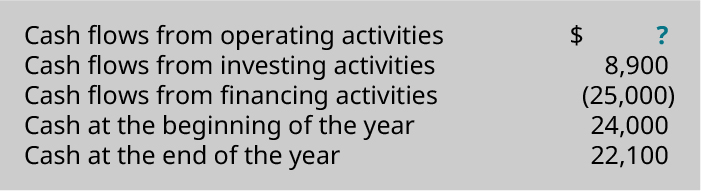

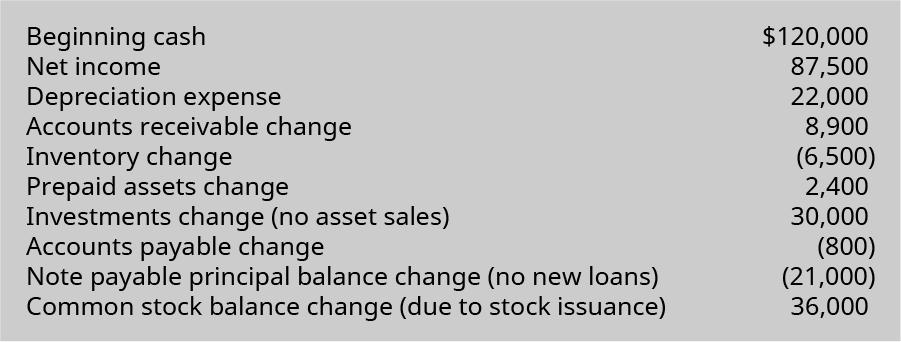

(Figure)Provide the missing piece of information for the following statement of cash flows puzzle.

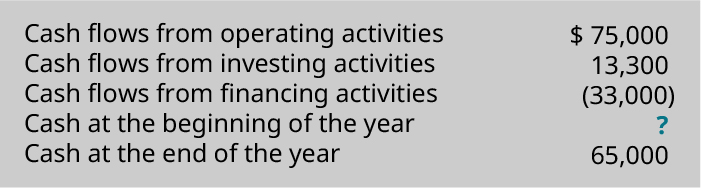

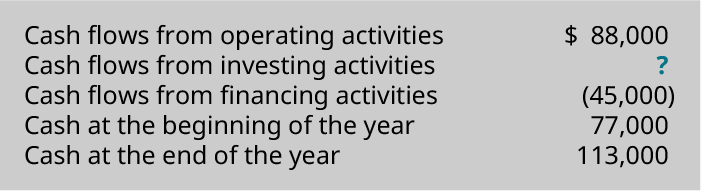

(Figure)Provide the missing piece of information for the following statement of cash flows puzzle.

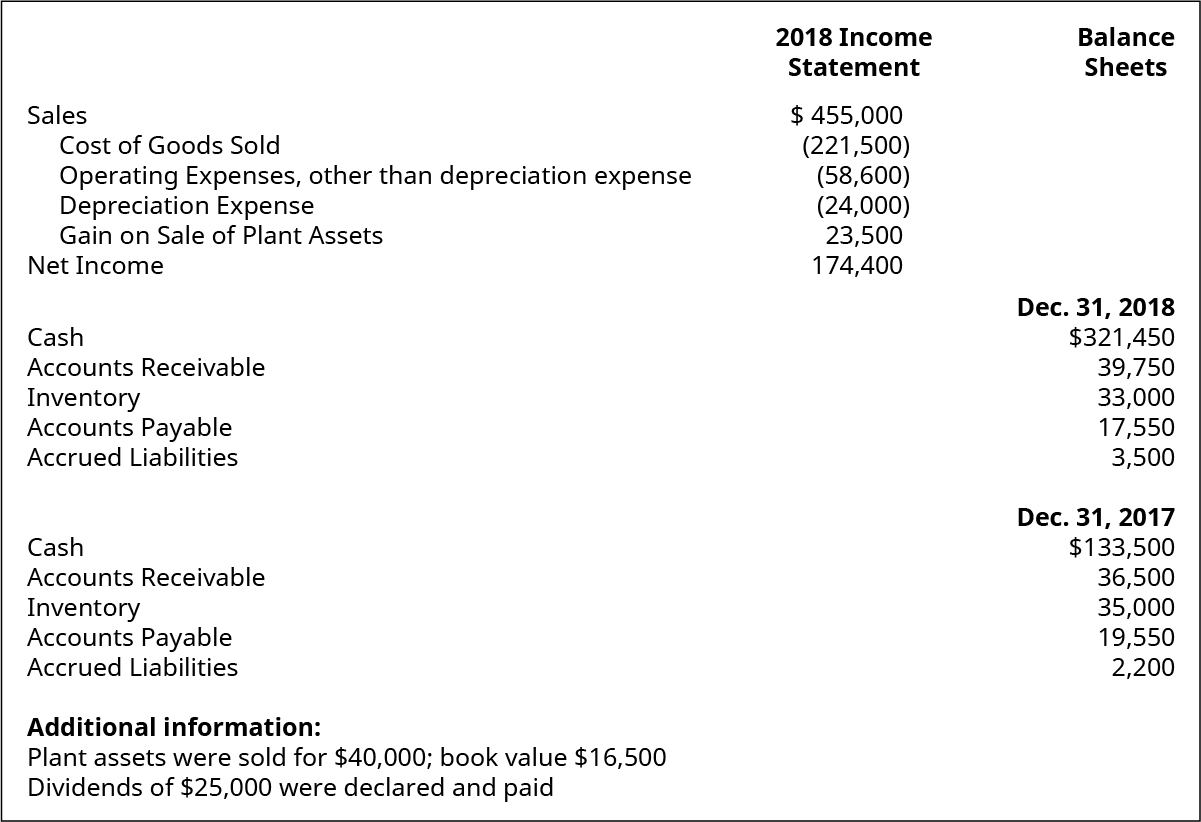

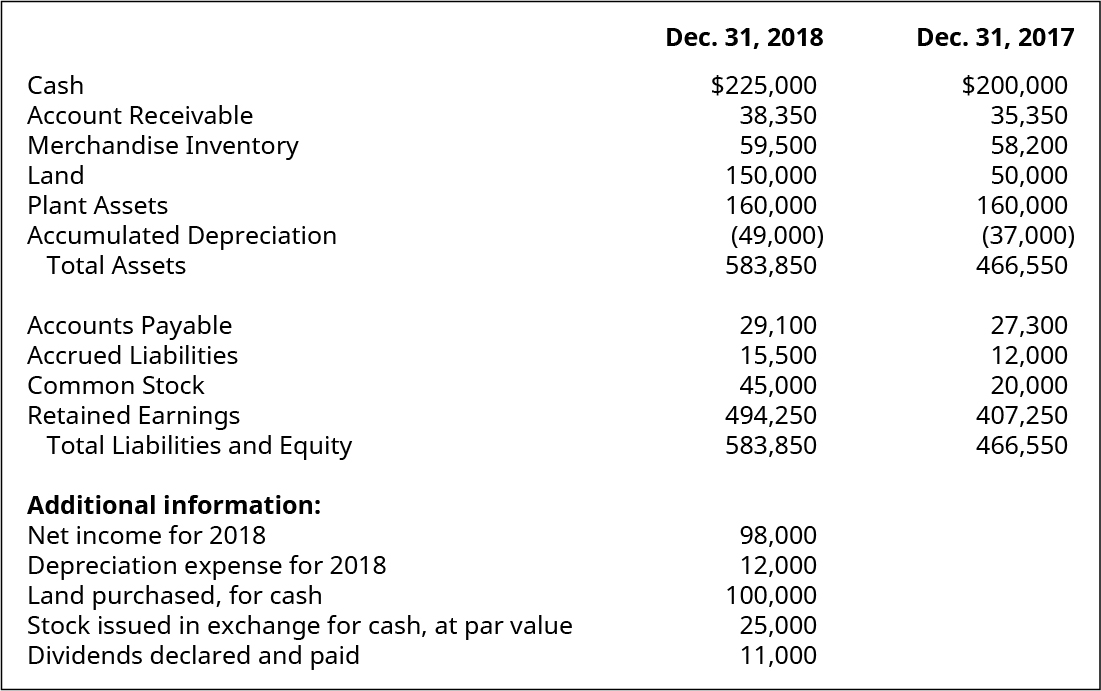

Problem Set A

(Figure)Use the following excerpts from Zowleski Company’s financial information to prepare a statement of cash flows (indirect method) for the year 2018.

(Figure)Use the following excerpts from Yardley Company’s financial information to prepare a statement of cash flows (indirect method) for the year 2018.

(Figure)Use the following excerpts from Wickham Company’s financial information to prepare a statement of cash flows (indirect method) for the year 2018.

(Figure)Use the following excerpts from Tungsten Company’s financial information to prepare a statement of cash flows (indirect method) for the year 2018.

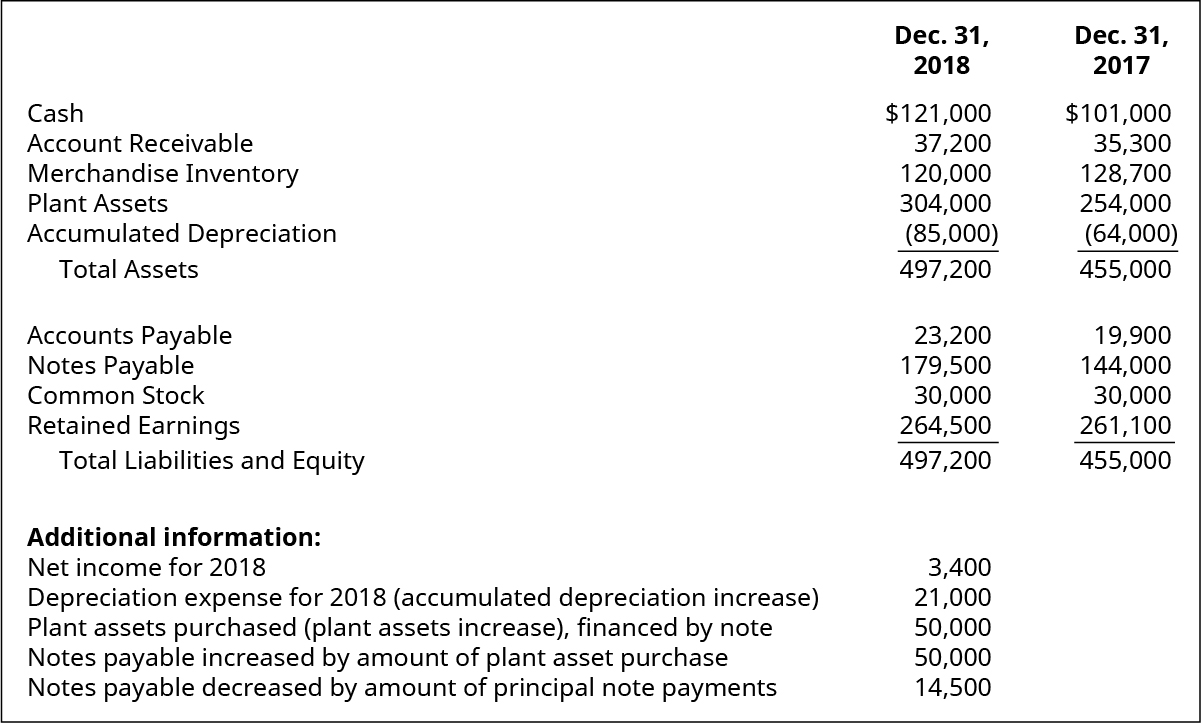

Problem Set B

(Figure)Use the following excerpts from Stern Company’s financial information to prepare a statement of cash flows (indirect method) for the year 2018.

(Figure)Use the following excerpts from Unigen Company’s financial information to prepare the operating section of the statement of cash flows (indirect method) for the year 2018.

(Figure)Use the following excerpts from Mountain Company’s financial information to prepare a statement of cash flows (indirect method) for the year 2018.

(Figure)Use the following excerpts from OpenAir Company’s financial information to prepare a statement of cash flows (indirect method) for the year 2018.

Thought Provokers

(Figure)Use the EDGAR (Electronic Data Gathering, Analysis, and Retrieval system) search tools on the US Securities and Exchange Commission website to locate the latest Form 10-K for a company you would like to analyze. Pick a company and submit a short memo that provides the following information:

- The name and ticker symbol of the company you have chosen.

- A description of two items from the company’s statement of cash flows:

- One familiar item that you expected to be reported on the statement, based on what you’ve learned about cash flows

- One unfamiliar item that you did not expect to be on the statement, based on what you’ve learned about cash flows

- The URL to the company’s Form 10-K to allow accurate verification of your answers