LO 2.1 Describe the Income Statement, Statement of Retained Earnings, Balance Sheet, and Statement of Cash Flows, and How They Interrelate

Mitchell Franklin; Patty Graybeal; and Dixon Cooper

The study of accounting requires an understanding of precise and sometimes complicated terminology, purposes, principles, concepts, and organizational and legal structures. Typically, your introductory accounting courses will familiarize you with the overall accounting environment, and for those of you who want greater detail, there is an assortment of more advanced accounting courses available.

This chapter concentrates on the four major types of financial statements and their interactions, the major types of business structures, and some of the major terms and concepts used in this course. Coverage here is somewhat basic since these topics are accorded much greater detail in future chapters.

Types of Business Structure

As you learned in Role of Accounting in Society, virtually every activity that occurs in a business has an associated cost or value. Part of an accountant’s role is to quantify these activities, or transactions.

Also, in business—and accounting in particular—it is necessary to distinguish the business entity from the individual owner(s). The personal transactions of the owners, employees, and other parties connected to the business should not be recorded in the organization’s records; this accounting principle is called the business entity concept. Accountants should record only business transactions in business records.

This separation is also reflected in the legal structure of the business. There are several common types of legal business structures. While the accounting concepts for the various types of businesses are essentially the same regardless of the legal structure, the terminology will change slightly depending on the organization’s legal structure, and it is important to understand the differences.

There are three broad categories for the legal structure of an organization: sole proprietorship, partnership, and corporation. A sole proprietorship is a legal business structure consisting of a single individual. Benefits of this type of structure include ease of formation, favorable tax treatment, and a high level of control over the business. The risks involved with sole proprietorships include unlimited personal liability and a limited life for the business. Unless the business is sold, the business ends when the owner retires or passes away. In addition, sole proprietorships have a fairly limited ability to raise capital (funding), and often sole proprietors have limited expertise—they are excellent at what they do but may have limited expertise in other important areas of business, such as accounting or marketing.

A partnership is a legal business structure consisting of an association of two or more people who contribute money, property, or services to operate as co-owners of a business. Benefits of this type of structure include favorable tax treatment, ease of formation of the business, and better access to capital and expertise. The downsides to a partnership include unlimited personal liability (although there are other legal structures—a limited liability partnership, for example—to help mitigate the risk); limited life of the partnership, similar to sole proprietorships; and increased complexity to form the venture (decision-making authority, profit-sharing arrangement, and other important issues need to be formally articulated in a written partnership agreement).

A corporation is a legal business structure involving one or more individuals (owners) who are legally distinct (separate) from the business. A primary benefit of a corporate legal structure is the owners of the organization have limited liability. That is, a corporation is “stand alone,” conducting business as an entity separate from its owners. Under the corporate structure, owners delegate to others (called agents) the responsibility to make day-to-day decisions regarding the operations of the business. Other benefits of the corporate legal structure include relatively easy access to large amounts of capital by obtaining loans or selling ownership (stock), and since the stock is easily sold or transferred to others, the business operates beyond the life of the shareholders. A major disadvantage of a corporate legal structure is double taxation—the business pays income tax and the owners are taxed when distributions (also called dividends) are received.

| Types of Business Structures | |||

|---|---|---|---|

| Sole Proprietorship | Partnership | Corporation | |

| Number of Owners | Single individual | Two or more individuals | One or more owners |

| Ease of Formation | Easier to form | Harder to form | Difficult to form |

| Ability to Raise Capital | Difficult to raise capital | Harder to raise capital | Easier to raise capital |

| Liability Risk | Unlimited liability | Unlimited liability | Limited liability |

| Taxation Consideration | Single taxation | Single taxation | Double taxation |

The Four Financial Statements

Are you a fan of books, movies, or sports? If so, chances are you have heard or said the phrase “spoiler alert.” It is used to forewarn readers, viewers, or fans that the ending of a movie or book or outcome of a game is about to be revealed. Some people prefer knowing the end and skipping all of the details in the middle, while others prefer to fully immerse themselves and then discover the outcome. People often do not know or understand what accountants produce or provide. That is, they are not familiar with the “ending” of the accounting process, but that is the best place to begin the study of accounting.

Accountants create what are known as financial statements. Financial statements are reports that communicate the financial performance and financial position of the organization.

In essence, the overall purpose of financial statements is to evaluate the performance of a company, governmental entity, or not-for-profit entity. This chapter illustrates this through a company, which is considered to be in business to generate a profit. Each financial statement we examine has a unique function, and together they provide information to determine whether a company generated a profit or loss for a given period (such as a month, quarter, or year); the assets, which are resources of the company, and accompanying liabilities, which are obligations of the company, that are used to generate the profit or loss; owner interest in profits or losses; and the cash position of the company at the end of the period.

The four financial statements that perform these functions and the order in which we prepare them are:

- Income Statement

- Statement of Retained Earnings

- Balance Sheet

- Statement of Cash Flows

The order of preparation is important as it relates to the concept of how financial statements are interrelated. Before explaining each in detail, let’s explore the purpose of each financial statement and its main components.

CONTINUING APPLICATION AT WORK

Gearhead Outfitters, founded by Ted Herget in 1997 in Jonesboro, Arkansas, is a retail chain that sells outdoor gear for men, women, and children. The company’s inventory includes clothing, footwear for hiking and running, camping gear, backpacks, and accessories, by brands such as The North Face, Birkenstock, Wolverine, Yeti, Altra, Mizuno, and Patagonia. Herget fell in love with the outdoor lifestyle while working as a ski instructor in Colorado and wanted to bring that feeling back home to Arkansas. And so, Gearhead was born in a small downtown location in Jonesboro. The company has had great success over the years, expanding to numerous locations in Herget’s home state, as well as Louisiana, Oklahoma, and Missouri.

While Herget knew his industry when starting Gearhead, like many entrepreneurs he faced regulatory and financial issues that were new to him. Several of these issues were related to accounting and the wealth of decision-making information that accounting systems provide.

For example, measuring revenue and expenses, providing information about cash flow to potential lenders, analyzing whether profit and positive cash flow is sustainable to allow for expansion, and managing inventory levels. Accounting, or the preparation of financial statements (balance sheet, income statement, and statement of cash flows), provides the mechanism for business owners such as Herget to make fundamentally sound business decisions.

Purpose of Financial Statements

Before exploring the specific financial statements, it is important to know why these are important documents. To understand this, you must first understand who the users of financial statements are. Users of the information found in financial statements are called stakeholders. A stakeholder is someone affected by decisions made by a company; this can include groups or individuals affected by the actions or policies of an organization, including include investors, creditors, employees, managers, regulators, customers, and suppliers. The stakeholder’s interest sometimes is not directly related to the entity’s financial performance. Examples of stakeholders include lenders, investors/owners, vendors, employees and management, governmental agencies, and the communities in which the businesses operate. Stakeholders are interested in the performance of an organization for various reasons, but the common goal of using the financial statements is to understand the information each contains that is useful for making financial decisions. For example, a banker may be interested in the financial statements to decide whether or not to lend the organization money.

Likewise, small business owners may make decisions based on their familiarity with the business—they know if the business is doing well or not based on their “gut feeling.” By preparing the financial statements, accountants can help owners by providing clarity of the organization’s financial performance. It is important to understand that, in the long term, every activity of the business has a financial impact, and financial statements are a way that accountants report the activities of the business. Stakeholders must make many decisions, and the financial statements provide information that is helpful in the decision-making process.

As described in Role of Accounting in Society, the complete set of financial statements acts as an X-ray of a company’s financial health. By evaluating all of the financial statements together, someone with financial knowledge can determine the overall health of a company. The accountant can use this information to advise outside (and inside) stakeholders on decisions, and management can use this information as one tool to make strategic short- and long-term decisions.

ETHICAL CONSIDERATIONS

Utilitarianism is a well-known and influential moral theory commonly used as a framework to evaluate business decisions. Utilitarianism suggests that an ethical action is one whose consequence achieves the greatest good for the greatest number of people. So, if we want to make an ethical decision, we should ask ourselves who is helped and who is harmed by it. Focusing on consequences in this way generally does not require us to take into account the means of achieving that particular end, however. Put simply, the utilitarian view is an ethical theory that the best action of a company is the one that maximizes utility of all stakeholders to the decision. This view assumes that all individuals with an interest in the business are considered within the decision.

Financial statements are used to understand the financial performance of companies and to make long- and short-term decisions. A utilitarian approach considers all stakeholders, and both the long- and short-term effects of a business decision. This allows corporate decision makers to choose business actions with the potential to produce the best outcomes for the majority of all stakeholders, not just shareholders, and therefore maximize stakeholder happiness.

Accounting decisions can change the approach a stakeholder has in relation to a business. If a company focuses on modifying operations and financial reporting to maximize short-term shareholder value, this could indicate the prioritization of certain stakeholder interests above others. When a company pursues only short-term profit for shareholders, it neglects the well-being of other stakeholders. Professional accountants should be aware of the interdependent relationship between all stakeholders and consider whether the results of their decisions are good for the majority of stakeholder interests.

YOUR TURN

Think of a business owner in your family or community. Schedule some time to talk with the business owner, and find out how he or she uses financial information to make decisions.

Solution

Business owners will use financial information for many decisions, such as comparing sales from one period to another, determining trends in costs and other expenses, and identifying areas in which to reduce or reallocate expenses. This information will be used to determine, for example, staffing and inventory levels, streamlining of operations, and advertising or other investment decisions.

The Income Statement

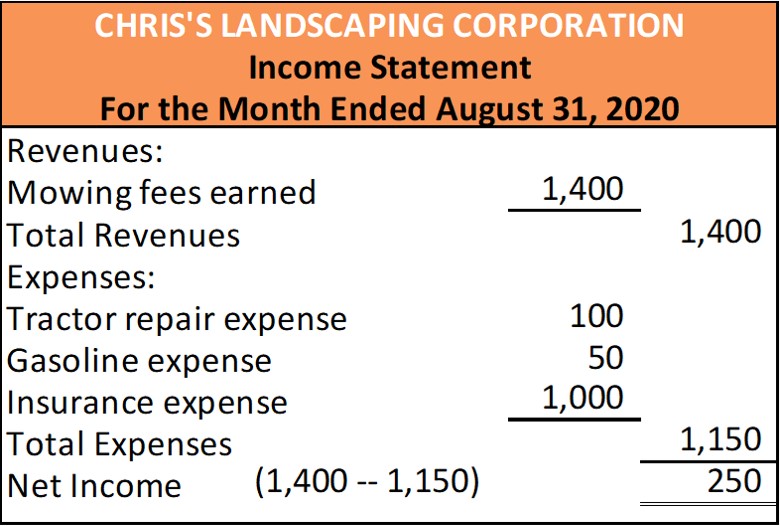

The first financial statement prepared is the income statement, a statement that shows the organization’s financial performance for a given period of time. Let’s illustrate the purpose of an income statement using a real-life example. Assume your friend, Chris, started a summer landscaping business on August 1, 2020 and decided to organize the business as a corporation. It is categorized as a service entity. To keep this example simple, assume that she is using her family’s tractor, and we are using the cash basis method of accounting to demonstrate Chris’s initial operations for her business. The other available basis method that is commonly used in accounting is the accrual basis method. She is responsible for paying for fuel and any maintenance costs. She named the business Chris’s Landscaping Corporation. On August 31, Chris checked the account balance and noticed there is only $250 in the checking account. This balance is lower than expected because she thought she had been paid by some customers. Chris decides to do some research to determine why the balance in the checking account is lower than expected. Her research shows that she earned a total of $1,400 from her customers but had to pay $100 to fix the brakes on her tractor, $50 for fuel, and also made a $1,000 payment to the insurance company for business insurance. The reason for the lower-than-expected balance was due to the fact that she spent ($1,150 for brakes, fuel, and insurance) only slightly less than she earned ($1,400)—a net increase of $250. While she would like the checking balance to grow each month, she realizes most of the August expenses were infrequent (brakes and insurance) and the insurance, in particular, was an unusually large expense. She is convinced the checking account balance will likely grow more in September because she will earn money from some new customers; she also anticipates having fewer expenses.

The Income Statement can also be visualized by the formula: Revenue – Expenses = Net Income or (Net Loss).

Let’s change this example slightly and assume the $1,000 payment to the insurance company will be paid in September, rather than in August. In this case, the ending balance in Chris’s checking account would be $1,250, a result of earning $1,400 and only spending $100 for the brakes on her car and $50 for fuel. This stream of cash flows is an example of cash basis accounting because it reflects when payments are received and made, not necessarily the time period that they affect. At the end of this section and in The Adjustment Process you will address accrual accounting, which does reflect the time period that they affect.

In accounting, this example illustrates an income statement, a financial statement that is used to measure the financial performance of an organization for a particular period of time. We use the simple landscaping account example to discuss the elements of the income statement, which are revenues and expenses. Together, these determine whether the organization has net income (where revenues are greater than expenses) or net loss (where expenses are greater than revenues). Revenues and expenses are further defined here.

Revenue

Revenue1 is the value of goods and services the organization sold or provided to customers for a given period of time. In our current example, Chris’s landscaping business, the “revenue” earned for the month of August would be $1,400. It is the value Chris received in exchange for the services provided to her clients. Likewise, when a business provides goods or services to customers for cash at the time of the service or in the future, the business classifies the amount(s) as revenue. Just as the $1,400 earned from a business made Chris’s checking account balance increase, revenues increase the value of a business. In accounting, revenues are often also called sales revenue or fees earned. Revenues (and the other terms) are used to indicate the dollar value of goods and services provided to customers for a given period of time.

YOUR TURN

Think about the coffee shop in your area. Identify items the coffee shop sells that would be classified as revenues. Remember, revenues for the coffee shop are related to its primary purpose: selling coffee and related items. Or, better yet, make a trip to the local coffee shop and get a first-hand experience.

Solution

Many coffee shops earn revenue through multiple revenue streams, including coffee and other specialty drinks, food items, gift cards, and merchandise.

Expenses

An expense2 is a cost associated with providing goods or services to customers. In our opening example, the expenses that Chris incurred totaled $1,150 (consisting of $100 for brakes, $50 for fuel, and $1,000 for insurance). You might think of expenses as the opposite of revenue in that expenses reduce Chris’s checking account balance. Likewise, expenses decrease the value of the business and represent the dollar value of costs incurred to provide goods and services to customers for a given period of time.

YOUR TURN

While thinking about or visiting the coffee shop in your area, look around (or visualize) and identify items or activities that are the expenses of the coffee shop. Remember, expenses for the coffee shop are related to resources consumed while generating revenue from selling coffee and related items. Do not forget about any expenses that might not be so obvious—as a general rule, every activity in a business has an associated cost.

Solution

Costs of the coffee shop that might be readily observed would include rent; wages for the employees; and the cost of the coffee, pastries, and other items/merchandise that may be sold. In addition, costs such as utilities, equipment, and cleaning or other supplies might also be readily observable. More obscure costs of the coffee shop would include insurance, regulatory costs such as health department licensing, point-of-sale/credit card costs, advertising, donations, and payroll costs such as workers’ compensation, unemployment, and so on.

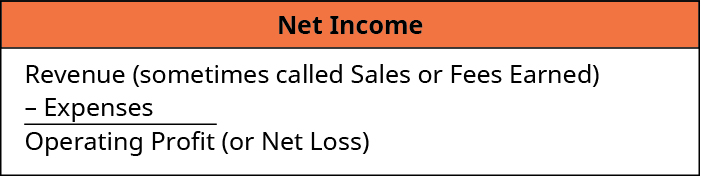

Net Income (Net Loss)

Net income (net loss) is determined by comparing revenues and expenses. Net income is a result of revenues (inflows) being greater than expenses (outflows). A net loss occurs when expenses (outflows) are greater than revenues (inflows). In accounting it is common to present net income in the following format:

Recall that revenue is the value of goods and services a business provides to its customers and increase the value of the business. Expenses, on the other hand, are the costs of providing the goods and services and decrease the value of the business. When revenues exceed expenses, companies have net income. This means the business has been successful at earning revenues, containing expenses, or a combination of both. If, on the other hand, expenses exceed revenues, companies experience a net loss. This means the business was unsuccessful in earning adequate revenues, sufficiently containing expenses, or a combination of both. While businesses work hard to avoid net loss situations, it is not uncommon for a company to sustain a net loss from time-to-time. It is difficult, however, for businesses to remain viable while experiencing net losses over the long term.

Shown as a formula, the net income (loss) function is:

Equity — Statement of Retained Earnings

Equity is a term that is often confusing but is a concept with which you are probably already familiar. In short, equity is the value of an item that remains after considering what is owed for that item. The following example may help illustrate the concept of equity.

When thinking about the concept of equity, it is often helpful to think about an example many families are familiar with: purchasing a home. Suppose a family purchases a home worth $200,000. After making a down payment of $25,000, they secure a bank loan to pay the remaining $175,000. What is the value of the family’s equity in the home? If you answered $25,000, you are correct. At the time of the purchase, the family owns a home worth $200,000 (an asset), but they owe $175,000 (a liability), so the equity or net worth in the home is $25,000.

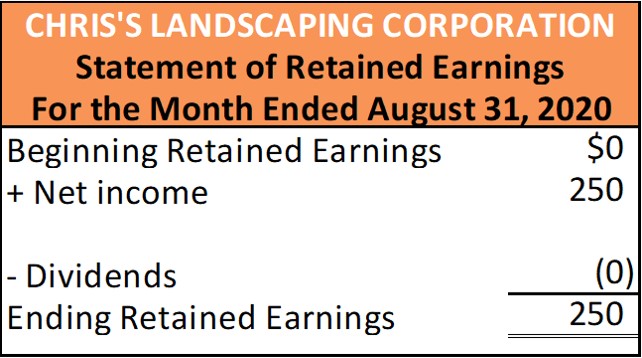

The statement of retained earnings, which is the second financial statement created by accountants, is a statement that shows how the equity (or value) of the organization has changed over time. Similar to the income statement, the statement of retained earnings is for a specific period of time, typically one year. Recall that another way to think about equity is net worth, or value. So, the statement of retained earnings is a financial statement that shows how the net worth, or value, of the business has changed for a given period of time.

The elements of equity shown on the statement of retained earnings include three of the four ways that total equity is increased or decreased. Contributed capital (assets received from) owners is kept separate. But revenues, expenses, and distributions of assets to owners (dividends) are all included in the statement of retained earnings. Instead of showing revenues and expenses in detail (which would be a repeat of the Income Statement) the summary of revenues and expenses, Net Income or Net Loss, is copied from the Income Statement to the Statement of Retained Earnings. Net income will increase retained earnings, while a net loss will decrease retained earnings. Distributions to owners (dividends) also cause retained earnings to decrease.

In our example, to make it less complicated, we started with the first month of operations for Chris’s Landscaping Corporation. In the first month of operations, Retained Earnings begins the month of August 2020, at $0, since there have been no transactions. During the month, the business earned revenue of $1,400 and incurred expenses of $1,150, for net income of $250. Since the business did not make any distributions of assets to owners, the ending balance in the Retained Earnings account on August 31, 2020, would be $250.

Contributed Capital (Receive Assets from Owners)

Generally, there are two ways by which organizations become more valuable: profitable operations (when revenues exceed expenses) and receiving assets from owners. Organizations often have long-term goals or projects that are very expensive (for example, building a new manufacturing facility or purchasing another company).

While having profitable operations is a viable way to “fund” these goals and projects, organizations often want to undertake these projects in a quicker time frame. Selling ownership is one way to quickly obtain the funding necessary for these goals. Receiving assets from owners (investments from owners) represent an exchange of cash or other assets for which the investor is given an ownership interest in the organization. This is a mutually beneficial arrangement: the organization gets the funding it needs on a timely basis, and the investor gets an ownership interest in the organization.

When organizations generate funding by selling ownership, the ownership interest usually takes the form of common stock, which is the corporation’s primary class of stock issued, with each share representing a partial claim to ownership or a share of the company’s business. When the organization issues common stock for the first time, it is called an initial public offering (IPO). In Corporation Accounting, you learn more about the specifics of this type of accounting. Once a company issues (or sells) common stock after an IPO, we describe the company as a publicly traded company, which simply means the company’s stock can be purchased by the general public on a public exchange like the New York Stock Exchange (NYSE). That is, investors can become owners of the particular company. Companies that issue publicly traded common shares in the United States are regulated by the Securities and Exchange Commission (SEC), a federal regulatory agency that, among other responsibilities, is charged with oversight of financial investments such as common stock.

CONCEPTS IN PRACTICE

On September 1, 2017, Roku, Inc. filed a Form S-1 with the Securities and Exchange Commission (SEC).5 In this form, Roku disclosed its intention to become a publicly traded company, meaning its stock will trade (sell) on public stock exchanges, allowing individual and institutional investors an opportunity to own a portion (shares) of the company. The Form S-1 included detailed financial and nonfinancial information about the company. The information from Roku also included the purpose of the offering as well as the intended uses of the funds. Here is a portion of the disclosure: “The principal purposes of this offering are to increase our capitalization and financial flexibility and create a public market for our Class A common stock. We intend to use the net proceeds we receive from this offering primarily for general corporate purposes, including working capital . . . research and development, business development, sales and marketing activities and capital expenditures.”6

On September 28, 2017, Roku “went public” and exceeded expectations. Prior to the IPO, Roku estimated it would sell between $12 and $14 per share, raising over $117 million for the company. The closing price per share on September 28 was $23.50, nearly doubling initial expectations for the share value.7

Distributions to Owners (Dividends)

There are basically two ways in which organizations become less valuable in terms of owners’ equity: from unprofitable operations (when expenses or losses exceed revenues or gains) and by distributions to owners. Owners (investors) of an organization want to see their investment appreciate (gain) in value. Over time, owners of common stock can see the value of the stock increase in value—the share price increases—due to the success of the organization. Organizations may also make distributions to owners, which are periodic rewards issued to the owners in the form of cash or other assets. Distributions to owners represent giving up some of the value (equity) of the organization.

For investors who hold common stock in the organization, these periodic payments or distributions to owners are called dividends. For sole proprietorships, distributions to owners are withdrawals or drawings. From the organization’s perspective, dividends represent a portion of the net worth (equity) of the organization that is returned to owners as a reward for their investment. While issuing dividends does, in fact, reduce the organization’s assets, some argue that paying dividends increases the organization’s long-term value by making the stock more desirable. (Note that this topic falls under the category of “dividend policy” and there is a significant stream of research addressing this.)

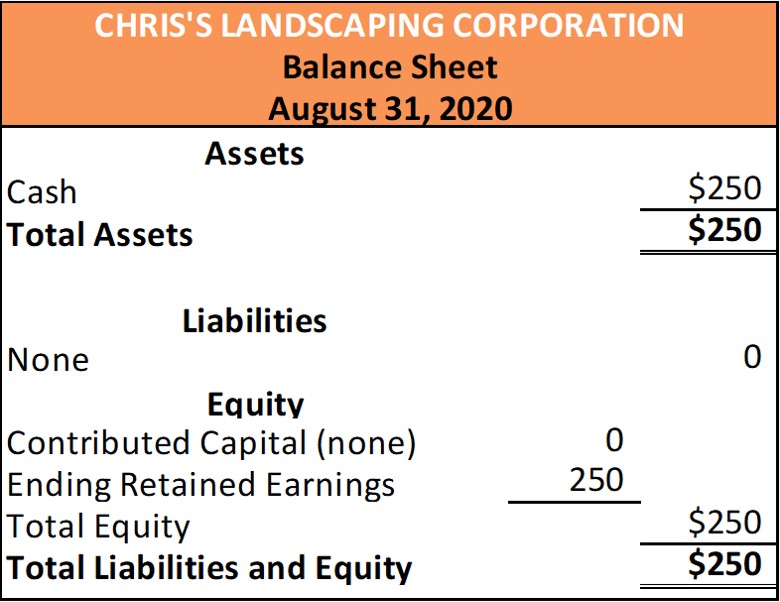

Balance Sheet

Once the statement of retained earnings is completed, accountants typically complete the balance sheet, a statement that lists what the organization owns (assets), what it owes (liabilities), and what it is worth (equity) on a specific date. Notice the change in timing of the report. The income statement and statement of retained earnings report the financial performance and equity change for a period of time. The balance sheet, however, lists the financial position at the close of business on a specific date. (Refer to (Figure) for the balance sheet as of August 31, 2020, for Chris’s Landscaping.)

Assets

If you recall our previous example involving Chris and her newly established landscaping business, you are probably already familiar with the term asset8—these are resources used to generate revenue. In Chris’s business, to keep the example relatively simple, the business ended the month with one asset, cash, assuming that the insurance was for one month’s coverage.

However, as organizations become more complex, they often have dozens or more types of assets. An asset can be categorized as a short-term asset or current asset (which is typically used up, sold, or converted to cash in one year or less) or as a long-term asset or noncurrent asset (which is not expected to be converted into cash or used up within one year). Long-term assets are often used in the production of products and services.

Examples of short-term assets that businesses own include cash, accounts receivable, and inventory, while examples of long-term assets include land, machinery, office furniture, buildings, and vehicles. Several of the chapters that you will study are dedicated to an in-depth coverage of the special characteristics of selected assets. Examples include Merchandising Transactions, which are typically short term, and Long-Term Assets, which are typically long term.

An asset can also be categorized as a tangible asset or an intangible asset. Tangible assets have a physical nature, such as trucks or many inventory items, while intangible assets have value but often lack a physical existence or corpus, such as insurance policies or trademarks.

Liabilities

You are also probably already familiar with the term liability9—these are amounts owed to others (called creditors). A liability can also be categorized as a short-term liability (or current liability) or a long-term liability (or noncurrent liability), similar to the treatment accorded assets. Short-term liabilities are typically expected to be paid within one year or less, while long-term liabilities are typically expected to be due for payment more than one year past the current balance sheet date.

Common short-term liabilities or amounts owed by businesses include amounts owed for items purchased on credit (also called accounts payable), taxes, wages, and other business costs that will be paid in the future. Long-term liabilities can include such liabilities as long-term notes payable, mortgages payable, or bonds payable.

Equity

In the Statement of Retained Earnings discussion, you learned that equity (or net assets) refers to book value or net worth. In our example, Chris’s Landscaping, we determined that Chris had $250 worth of equity in her company at the end of the first month (see (Figure)).

At any point in time it is important for stakeholders to know the financial position of a business. Stated differently, it is important for employees, managers, and other interested parties to understand what a business owns, owes, and is worth at any given point. This provides stakeholders with valuable financial information to make decisions related to the business.

Statement of Cash Flows

The fourth and final financial statement prepared is the statement of cash flows, which is a statement that lists the cash inflows and cash outflows for the business for a period of time. The changes in cash within this statement are often referred to as sources and uses of cash. A source of cash lets one see where cash is coming from. For example, is cash being generated from sales to customers, or is the cash a result of an advance in a large loan. Use of cash looks at what cash is being used for. Is cash being used to make an interest payment on a loan, or is cash being used to purchase a large piece of machinery that will expand business capacity? An entire chapter will be dedicated to the statement of cash flows and its preparation, later in this textbook.

Footnotes

- 1 In a subsequent section of this chapter, you will learn that the accounting profession is governed by the Financial Accounting Standards Board (or FASB), a professional body that issues guidelines/pronouncements for the accounting profession. A set of theoretical pronouncements issued by FASB is called Statement of Financial Accounting Concepts (SFAC). In SFAC No. 6, FASB defines revenues as “inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations” (SFAC No. 6, p. 23).

- 2 Expenses are formally defined by the FASB as “outflows or other using up of assets or incurrences of liabilities (or a combination of both) from delivering or producing goods, rendering services, or carrying out other activities that constitute the entity’s ongoing major or central operations” (SFAC No. 6, p. 23).

- 3 FASB notes that gains represent an increase in organizational value from activities that are “incidental or peripheral” (SFAC No. 6, p. 24) to the primary purpose of the business.

- 4 FASB notes losses represent a decrease in organizational value from activities that are “incidental or peripheral” (SFAC No. 6, p. 24) to the primary purpose of the business.

- 5 Roku, Inc. “Form S-1 Filing with the Securities and Exchange Commission.” September 1, 2017. https://www.sec.gov/Archives/edgar/data/1428439/000119312517275689/d403225ds1.htm

- 6 Roku, Inc. “Form S-1 Filing with the Securities and Exchange Commission.” September 1, 2017. https://www.sec.gov/Archives/edgar/data/1428439/000119312517275689/d403225ds1.htm

- 7 Roku, Inc. Data. https://finance.yahoo.com/quote/ROKU/history?p=ROKU

- 8 The FASB defines assets as “probable future economic benefits obtained or controlled by a particular entity as a result of past transactions or events” (SFAC No. 6, p. 12).

- 9 The FASB defines liabilities as “probable future sacrifices of economic benefits arising from present obligations of a particular entity to transfer assets or provide services to other entities in the future as a result of past transactions or events” (SFAC No. 6, p. 13).

legal business structure consisting of a single individual

legal business structure consisting of an association of two or more people who contribute money, property, or services to operate as co-owners of a business

legal business structure involving one or more individuals (owners) who are legally distinct (separate) from the business

someone affected by decisions made by a company; may include an investor, creditor, employee, manager, regulator, customer, supplier, and layperson

financial statement that measures the organization’s financial performance for a given period of time

inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivering or producing goods, rendering services, or other activities that constitute the entity’s ongoing major or central operations

cost associated with providing goods or services

when revenues and gains are greater than expenses and losses

when expenses and losses are greater than revenues and gains

residual interest in the (leftover) assets of an entity that remains after deducting its liabilities

a financial statement that shows how the equity of the organization has changed over a period of time

exchange of cash or other assets for an ownership interest in the organization

the business receives cash or other assets in exchange for an ownership interest in the organization. Also called "contributed capital".

corporation’s primary class of stock issued, with each share representing a partial claim to ownership or a share of the company’s business

when a company issues shares of its stock to the public for the first time

company whose stock is traded (bought and sold) on an organized stock exchange

federal regulatory agency that regulates corporations with shares listed and traded on security exchanges through required periodic filings

periodic “reward” distributed to owner of cash or other assets (called a "dividend" if business is organized as a corporation)