Time Value of Money — Tables of Factors

Mitchell Franklin

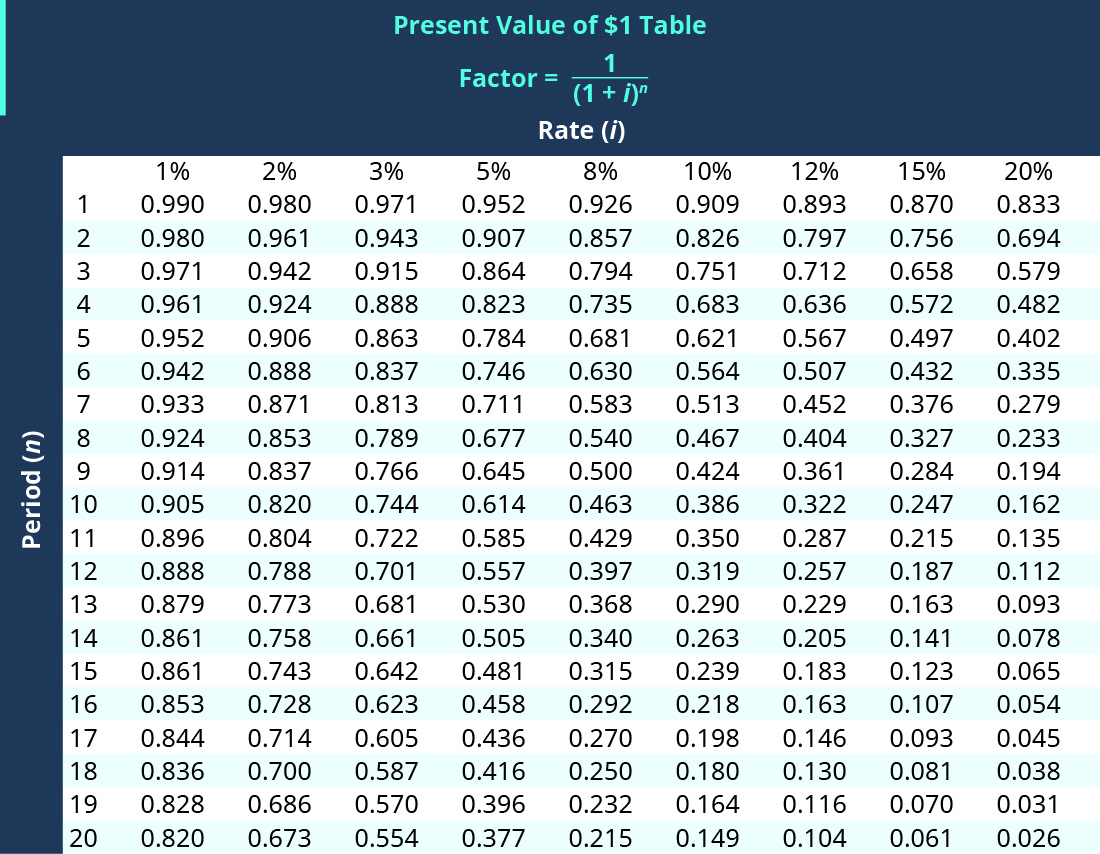

Present Value of $1 Table

Present Value of $1 Table.

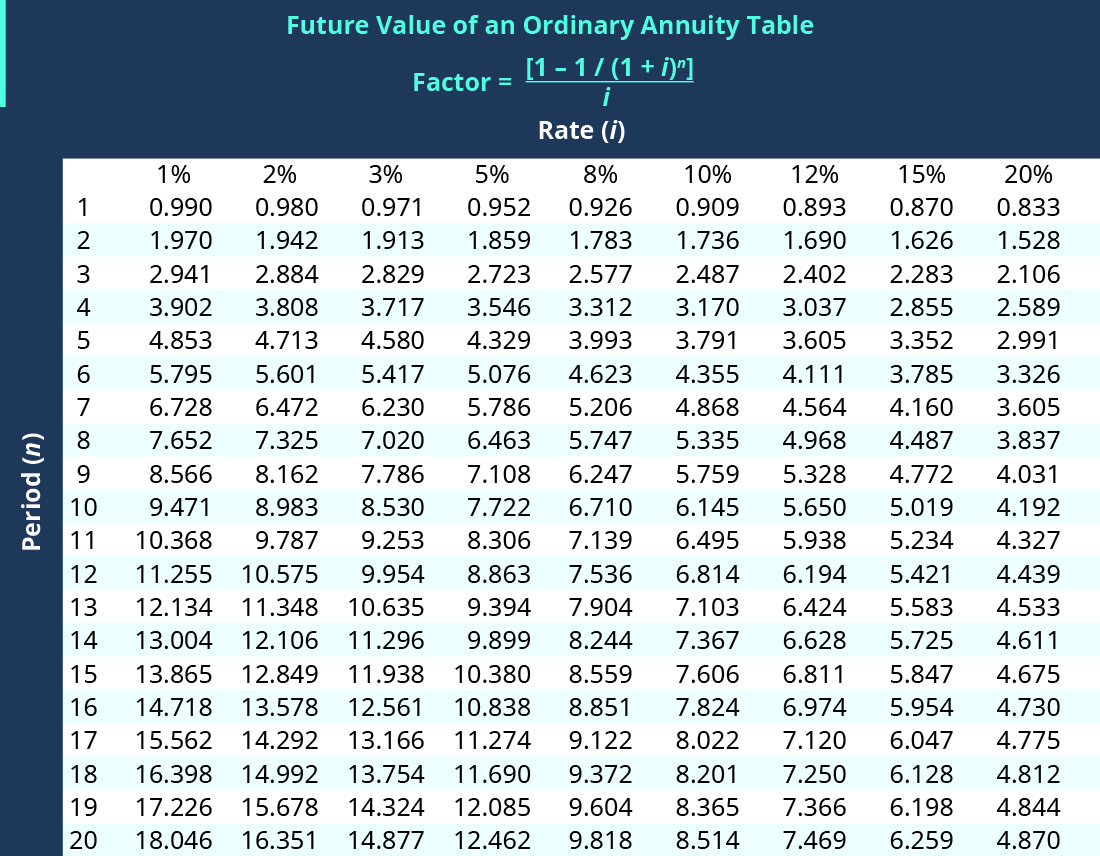

Present Value of an Ordinary Annuity Table

Present Value of an Ordinary Annuity Table.

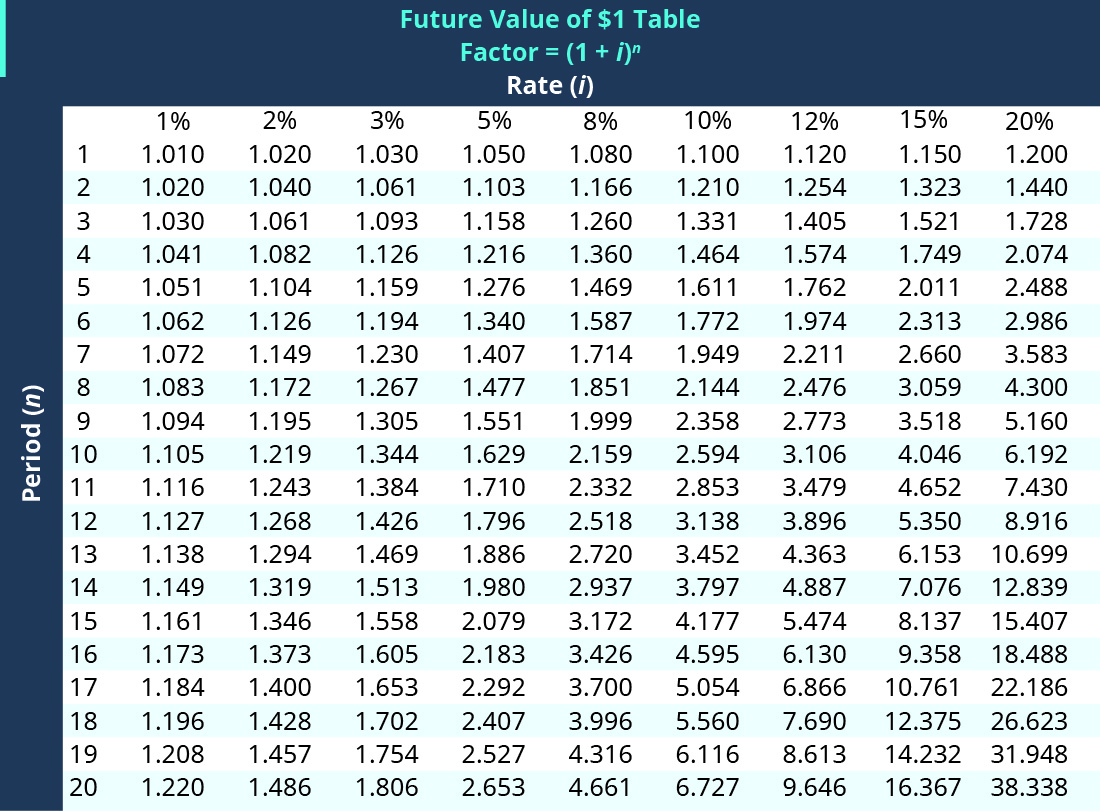

Future Value of $1 Table

Future Value of $1 Table.

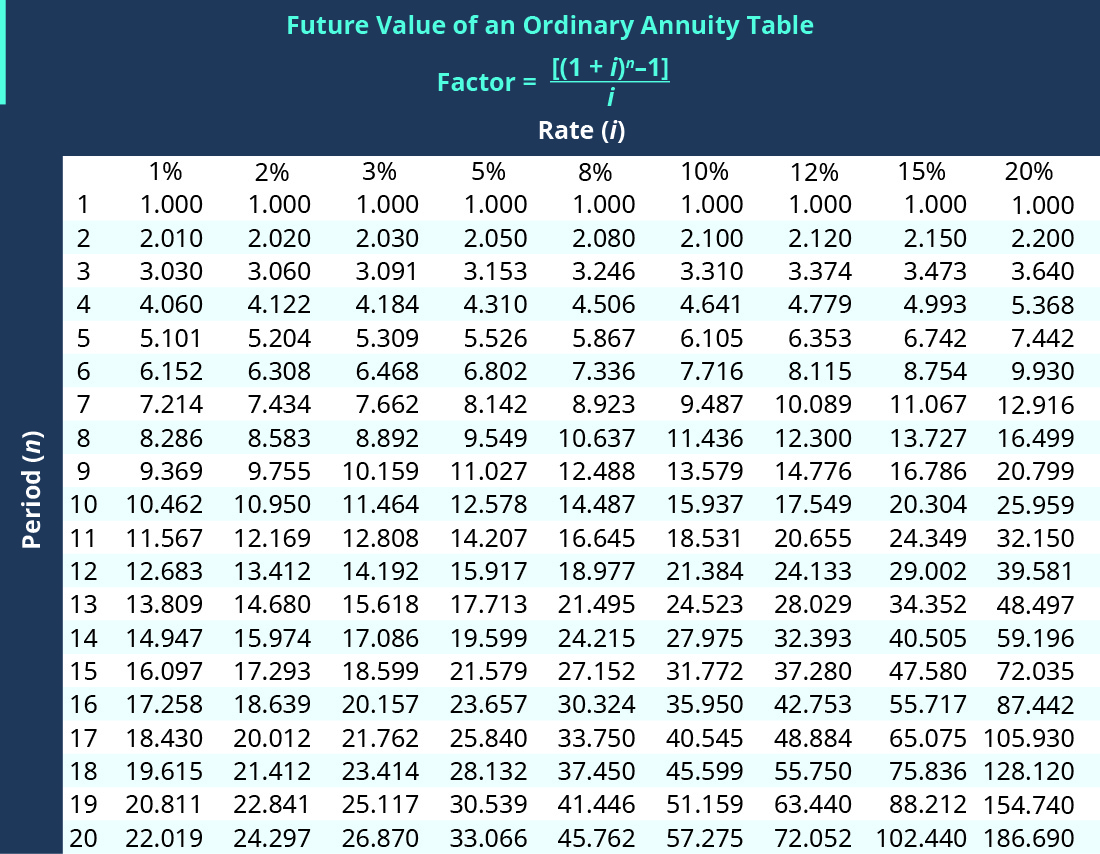

Future Value of an Ordinary Annuity Table

Future Value of an Ordinary Annuity Table.