LO 11.3 Define and Apply Accounting Treatment for Contingent Liabilities

Mitchell Franklin

What happens if your business anticipates incurring a loss or debt? Do you need to report this if you are uncertain it will occur? What if you know the loss or debt will occur but it has not happened yet? Do you have to report this event now, or in the future? These are questions businesses must ask themselves when exploring contingencies and their effect on liabilities.

A contingency occurs when a current situation has an outcome that is unknown or uncertain and will not be resolved until a future point in time. The outcome could be positive or negative. A contingent liability can produce a future debt or negative obligation for the company. Some examples of contingent liabilities include pending litigation (legal action), warranties, customer insurance claims, and bankruptcy.

While a contingency may be positive or negative, we only focus on outcomes that may produce a liability for the company (negative outcome), since these might lead to adjustments in the financial statements in certain cases. Positive contingencies do not require or allow the same types of adjustments to the company’s financial statements as do negative contingencies, since accounting standards do not permit positive contingencies to be recorded.

Pending litigation involves legal claims against the business that may be resolved at a future point in time. The outcome of the lawsuit has yet to be determined but could have negative future impact on the business.

Warranties arise from products or services sold to customers that cover certain defects (see (Figure)). It is unclear if a customer will need to use a warranty, and when, but this is a possibility for each product or service sold that includes a warranty. The same idea applies to insurance claims (car, life, and fire, for example), and bankruptcy. There is an uncertainty that a claim will transpire, or bankruptcy will occur. If the contingencies do occur, it may still be uncertain when they will come to fruition, or the financial implications.

The answer to whether or not uncertainties must be reported comes from Financial Accounting Standards Board (FASB) pronouncements.

Two Financial Accounting Standards Board (FASB) Requirements for Recognition of a Contingent Liability

There are two requirements for contingent liability recognition:

- There is a likelihood of occurrence.

- Measurement of the occurrence is classified as either estimable or inestimable.

Application of Likelihood of Occurrence Requirement

Let’s explore the likelihood of occurrence requirement in more detail.

According to the FASB, if there is a probable liability determination before the preparation of financial statements has occurred, there is a likelihood of occurrence, and the liability must be disclosed and recognized. This financial recognition and disclosure are recognized in the current financial statements. The income statement and balance sheet are typically impacted by contingent liabilities.

For example, Sierra Sports has a one-year warranty on part repairs and replacements for a soccer goal they sell. The warranty is good for one year. Sierra Sports notices that some of its soccer goals have rusted screws that require replacement, but they have already sold goals with this problem to customers. There is a probability that someone who purchased the soccer goal may bring it in to have the screws replaced. Not only does the contingent liability meet the probability requirement, it also meets the measurement requirement.

Application of Measurement Requirement

The measurement requirement refers to the company’s ability to reasonably estimate the amount of loss. Even though a reasonable estimate is the company’s best guess, it should not be a frivolous number. For a financial figure to be reasonably estimated, it could be based on past experience or industry standards (see (Figure)). It could also be determined by the potential future, known financial outcome.

Let’s continue to use Sierra Sports’ soccer goal warranty as our example. If the warranties are honored, the company should know how much each screw costs, labor cost required, time commitment, and any overhead costs incurred. This amount could be a reasonable estimate for the parts repair cost per soccer goal. Since not all warranties may be honored (warranty expired), the company needs to make a reasonable determination for the amount of honored warranties to get a more accurate figure.

Another way to establish the warranty liability could be an estimation of honored warranties as a percentage of sales. In this instance, Sierra could estimate warranty claims at 10% of its soccer goal sales.

When determining if the contingent liability should be recognized, there are four potential treatments to consider.

Let’s expand our discussion and add a brief example of the calculation and application of warranty expenses. To begin, in many ways a warranty expense works similarly to the bad debt expense concept covered in Accounting for Receivables in that the anticipated expense is determined by examining past period expense experiences and then basing the current expense on current sales data. Also, as with bad debts, the warranty repairs typically are made in an accounting period sometimes months or even years after the initial sale of the product, which means that we need to estimate future costs to comply with the revenue recognition and matching principles of generally accepted accounting principles (GAAP).

Some industries have such a large number of transactions and a vast data bank of past warranty claims that they have an easier time estimating potential warranty claims, while other companies have a harder time estimating future claims. In our case, we make assumptions about Sierra Sports and build our discussion on the estimated experiences.

For our purposes, assume that Sierra Sports has a line of soccer goals that sell for $800, and the company anticipates selling 500 goals this year (2019). Past experience for the goals that the company has sold is that 5% of them will need to be repaired under their three-year warranty program, and the cost of the average repair is $200. To simplify our example, we concentrate strictly on the journal entries for the warranty expense recognition and the application of the warranty repair pool. If the company sells 500 goals in 2019 and 5% need to be repaired, then 25 goals will be repaired at an average cost of $200. The average cost of $200 × 25 goals gives an anticipated future repair cost of $5,000 for 2019. Assume for the sake of our example that in 2020 Sierra Sports made repairs that cost $2,800. Following are the necessary journal entries to record the expense in 2019 and the repairs in 2020. The resources used in the warranty repair work could have included several options, such as parts and labor, but to keep it simple we allocated all of the expenses to repair parts inventory. Since the company’s inventory of supply parts (an asset) went down by $2,800, the reduction is reflected with a credit entry to repair parts inventory. First, following is the necessary journal entry to record the expense in 2019.

Next, here is the journal entry to record the repairs in 2020.

Before we finish, we need to address one more issue. Our example only covered the warranty expenses anticipated from the 2019 sales. Since the company has a three-year warranty, and it estimated repair costs of $5,000 for the goals sold in 2019, there is still a balance of $2,200 left from the original $5,000. However, its actual experiences could be more, the same, or less than $2,200. If it is determined that too much is being set aside in the allowance, then future annual warranty expenses can be adjusted downward. If it is determined that not enough is being accumulated, then the warranty expense allowance can be increased.

Since this warranty expense allocation will probably be carried on for many years, adjustments in the estimated warranty expenses can be made to reflect actual experiences. Also, sales for 2020, 2021, 2022, and all subsequent years will need to reflect the same types of journal entries for their sales. In essence, as long as Sierra Sports sells the goals or other equipment and provides a warranty, it will need to account for the warranty expenses in a manner similar to the one we demonstrated.

Consider the following scenario: A hoverboard is a self-balancing scooter that uses body position and weight transfer to control the device. Hoverboards use a lithium-ion battery pack, which was found to overheat causing an increased risk for the product to catch fire or explode. Several people were badly injured from these fires and explosions. As a result, a recall was issued in mid-2016 on most hoverboard models. Customers were asked to return the product to the original point of sale (the retailer). Retailers were required to accept returns and provide repair when available. In some cases, retailers were held accountable by consumers, and not the manufacturer of the hoverboards. You are the retailer in this situation and must decide if the hoverboard scenario creates any contingent liabilities. If so, what are the contingent liabilities? Do the conditions meet FASB requirements for contingent liability reporting? Which of the four possible treatments are best suited for the potential liabilities identified? Are there any journal entries or note disclosures necessary?

Four Potential Treatments for Contingent Liabilities

If the contingency is probable and estimable, it is likely to occur and can be reasonably estimated. In this case, the liability and associated expense must be journalized and included in the current period’s financial statements (balance sheet and income statement) along with note disclosures explaining the reason for recognition. The note disclosures are a GAAP requirement pertaining to the full disclosure principle, as detailed in Analyzing and Recording Transactions.

If the contingent liability is probable and inestimable, it is likely to occur but cannot be reasonably estimated. In this case, a note disclosure is required in financial statements, but a journal entry and financial recognition should not occur until a reasonable estimate is possible.

If the contingency is reasonably possible, it could occur but is not probable. The amount may or may not be estimable. Since this condition does not meet the requirement of likelihood, it should not be journalized or financially represented within the financial statements. Rather, it is disclosed in the notes only with any available details, financial or otherwise.

If the contingent liability is considered remote, it is unlikely to occur and may or may not be estimable. This does not meet the likelihood requirement, and the possibility of actualization is minimal. In this situation, no journal entry or note disclosure in financial statements is necessary.

| Financial Statement Treatments | ||

|---|---|---|

| Journalize | Note Disclosure | |

| Probable and estimable | Yes | Yes |

| Probable and inestimable | No | Yes |

| Reasonably possible | No | Yes |

| Remote | No | No |

Google, a subsidiary of Alphabet Inc., has expanded from a search engine to a global brand with a variety of product and service offerings. Like many other companies, contingent liabilities are carried on Google’s balance sheet, report expenses related to these contingencies on its income statement, and note disclosures are provided to explain its contingent liability treatments. Check out Google’s contingent liability considerations in this press release for Alphabet Inc.’s First Quarter 2017 Results to see a financial statement package, including note disclosures.

Let’s review some contingent liability treatment examples as they relate to our fictitious company, Sierra Sports.

Probable and Estimable

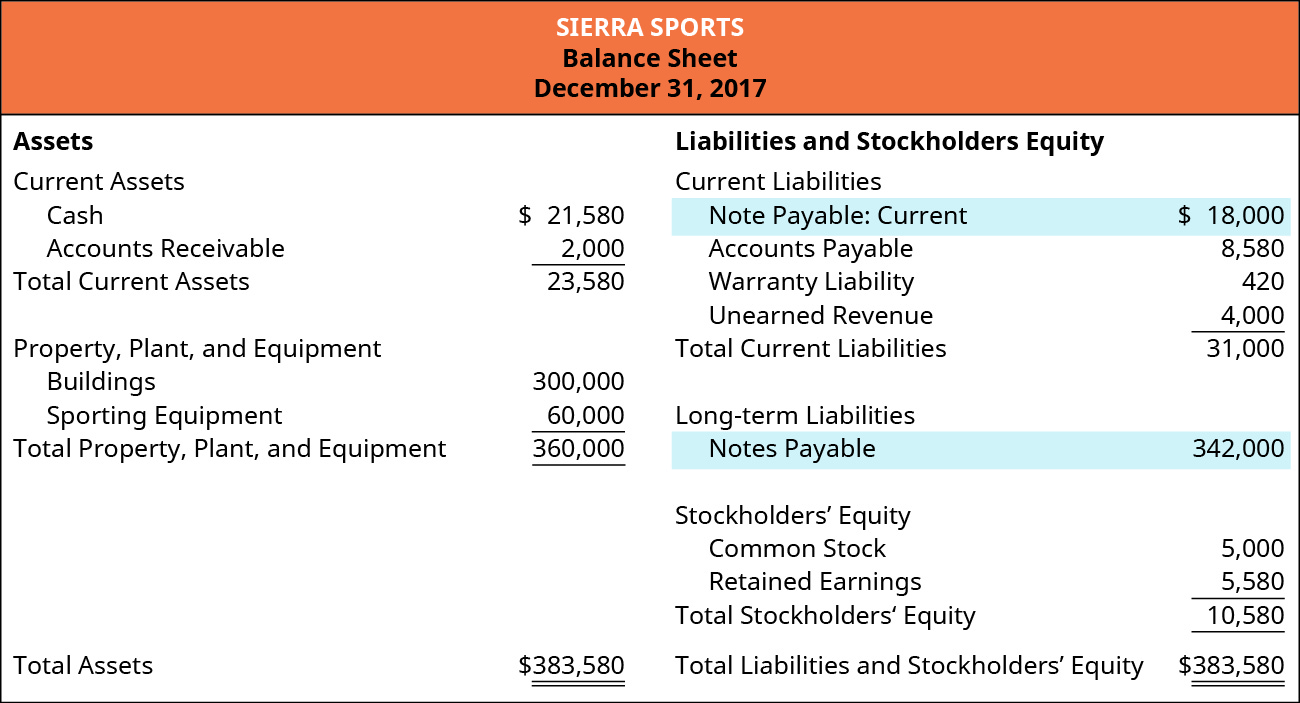

If Sierra Sports determines the cost of the soccer goal screws are $30, the labor requirement is one hour at a rate of $40 per hour, and there is no extra overhead applied, then the total estimated warranty repair cost would be $70 per goal: $30 + (1 hour × $40 per hour). Sierra Sports sold ten goals before it discovered the rusty screw issue. The company believes that only six of those goals will have their warranties honored, based on past experience. This means Sierra will incur a warranty liability of $420 ($70 × 6 goals). The $420 is considered probable and estimable and is recorded in Warranty Liability and Warranty Expense accounts during the period of discovery (current period).

An example of determining a warranty liability based on a percentage of sales follows. The sales price per soccer goal is $1,200, and Sierra Sports believes 10% of sales will result in honored warranties. The company would record this warranty liability of $120 ($1,200 × 10%) to Warranty Liability and Warranty Expense accounts.

When the warranty is honored, this would reduce the Warranty Liability account and decrease the asset used for repair (Parts: Screws account) or Cash, if applicable. The recognition would happen as soon as the warranty is honored. This first entry shown is to recognize honored warranties for all six goals.

This second entry recognizes an honored warranty for a soccer goal based on 10% of sales from the period.

As you’ve learned, not only are warranty expense and warranty liability journalized, but they are also recognized on the income statement and balance sheet. The following examples show recognition of Warranty Expense on the income statement (Figure) and Warranty Liability on the balance sheet (Figure) for Sierra Sports.

Probable and Not Estimable

Assume that Sierra Sports is sued by one of the customers who purchased the faulty soccer goals. A settlement of responsibility in the case has been reached, but the actual damages have not been determined and cannot be reasonably estimated. This is considered probable but inestimable, because the lawsuit is very likely to occur (given a settlement is agreed upon) but the actual damages are unknown. No journal entry or financial adjustment in the financial statements will occur. Instead, Sierra Sports will include a note describing any details available about the lawsuit. When damages have been determined, or have been reasonably estimated, then journalizing would be appropriate.

Sierra Sports could say the following in its financial statement disclosures: “There is pending litigation against our company with the likelihood of settlement probable. Detailed terms and damages have not yet reached agreement, and a reasonable assessment of financial impact is currently unknown.”

Reasonably Possible

Sierra Sports may have more litigation in the future surrounding the soccer goals. These lawsuits have not yet been filed or are in the very early stages of the litigation process. Since there is a past precedent for lawsuits of this nature but no establishment of guilt or formal arrangement of damages or timeline, the likelihood of occurrence is reasonably possible. The outcome is not probable but is not remote either. Since the outcome is possible, the contingent liability is disclosed in Sierra Sports’ financial statement notes.

Sierra Sports could say the following in their financial statement disclosures: “We anticipate more claimants filing legal action against our company with the likelihood of settlement reasonably possible. Assignment of guilt, detailed terms, and potential damages have not been established. A reasonable assessment of financial impact is currently unknown.”

Remote

Sierra Sports worries that as a result of pending litigation and losses associated with the faulty soccer goals, the company might have to file for bankruptcy. After consulting with a financial advisor, the company is pretty certain it can continue operating in the long term without restructuring. The chances are remote that a bankruptcy would occur. Sierra Sports would not recognize this remote occurrence on the financial statements or provide a note disclosure.

US GAAP and International Financial Reporting Standards (IFRS) define “current liabilities” similarly and use the same reporting criteria for most all types of current liabilities. However, two primary differences exist between US GAAP and IFRS: the reporting of (1) debt due on demand and (2) contingencies.

Liquidity and solvency are measures of a company’s ability to pay debts as they come due. Liquidity measures evaluate a company’s ability to pay current debts as they come due, while solvency measures evaluate the ability to pay debts long term. One common liquidity measure is the current ratio, and a higher ratio is preferred over a lower one. This ratio—current assets divided by current liabilities—is lowered by an increase in current liabilities (the denominator increases while we assume that the numerator remains the same). When lenders arrange loans with their corporate customers, limits are typically set on how low certain liquidity ratios (such as the current ratio) can go before the bank can demand that the loan be repaid immediately.

In theory, debt that has not been paid and that has become “on demand” would be considered a current liability. However, in determining how to report a loan that has become “on-demand,” US GAAP and IFRS differ:

- Under US GAAP, debts on which payment has been demanded because of violations of the contractual agreement between the lender and creditor are only included in current liabilities if, by the financial statement presentation date, there have been no arrangements made to pay off or restructure the debt. This allows companies time between the end of the fiscal year and the actual publication of the financial statements (typically two months) to make arrangements for repayment of the loan. Most often these loans are refinanced.

- Under IFRS, any payment or refinancing arrangements must be made by the fiscal year-end of the debtor. This difference means that companies reporting under IFRS must be proactive in assessing whether their debt agreements will be violated and make appropriate arrangements for refinancing or differing payment options prior to final year-end numbers being reported.

A second set of differences exist regarding reporting contingencies. Where US GAAP uses the term “contingencies,” IFRS uses “provisions.” In both cases, gain contingencies are not recorded until they are essentially realized. Both systems want to avoid prematurely recording or overstating gains based on the principles of conservatism. Loss contingencies are recorded (accrued) if certain conditions are met:

- Under US GAAP, loss contingencies are accrued if they are probable and can be estimated. Probable means “likely” to occur and is often assessed as an 80% likelihood by practitioners.

- Under IFRS, probable is defined as “more likely than not” and is typically assessed at 50% by practitioners.

The determination of whether a contingency is probable is based on the judgment of auditors and management in both situations. This means a contingent situation such as a lawsuit might be accrued under IFRS but not accrued under US GAAP. Finally, how a loss contingency is measured varies between the two options as well. For example, if a company is told it will be probable that it will lose an active lawsuit, and the legal team gives a range of the dollar value of that loss, under IFRS, the discounted midpoint of that range would be accrued, and the range disclosed. Under US GAAP, the low end of the range would be accrued, and the range disclosed.

Key Concepts and Summary

- Contingent liabilities arise from a current situation with an uncertain outcome that may occur in the future. Contingent liabilities may include litigation, warranties, insurance claims, and bankruptcy.

- Two FASB recognition requirements must be met before declaring a contingent liability. There must be a probable likelihood of occurrence, and the loss amount is reasonably estimated.

- The four contingent liability treatments are probable and estimable, probable and inestimable, reasonably possible, and remote.

- Recognition in financial statements, as well as a note disclosure, occurs when the outcome is probable and estimable. Probable and not estimable and reasonably possible outcomes require note disclosures only. There is not recognition or note disclosure for a remote outcome.

Multiple Choice

(Figure)Which of the following best describes a contingent liability that is likely to occur but cannot be reasonably estimated?

- reasonably possible

- probable and estimable

- probable and inestimable

- remote

(Figure)Blake Department Store sells television sets with one-year warranties that cover repair and replacement of television parts. In the month of June, Blake sells forty television sets with a per unit cost of $500. If Blake estimates warranty fulfillment at 10% of sales, what would be the warranty liability reported in June?

- $1,000

- $2,000

- $500

- $20,000

B

(Figure)What accounts are used to record a contingent warranty liability that is probable and estimable but has yet to be fulfilled?

- warranty liability and cash

- warranty expense and cash

- warranty liability and warranty expense, cash

- warranty expense and warranty liability

(Figure)Which of the following best describes a contingent liability that is unlikely to occur?

- remote

- probable and estimable

- reasonably possible

- probable and inestimable

A

Questions

(Figure)What is a contingent liability?

(Figure)What are the two FASB required conditions for a contingent liability to be recognized?

The likelihood of occurrence and the measurement requirement are the FASB required conditions. A contingent liability must be recognized and disclosed if there is a probable liability determination before the preparation of financial statements has occurred, and the company can reasonably estimate the amount of loss.

(Figure)If a bankruptcy is deemed likely to occur and is reasonably estimated, what would be the recognition and disclosure requirements for the company?

(Figure)Name the four contingent liability treatments.

They are probable and estimable, probable and inestimable, reasonably possible, and remote.

(Figure)A company’s sales for January are $250,000. If the company projects warranty obligations to be 5% of sales, what is the warranty liability amount for January?

Exercise Set A

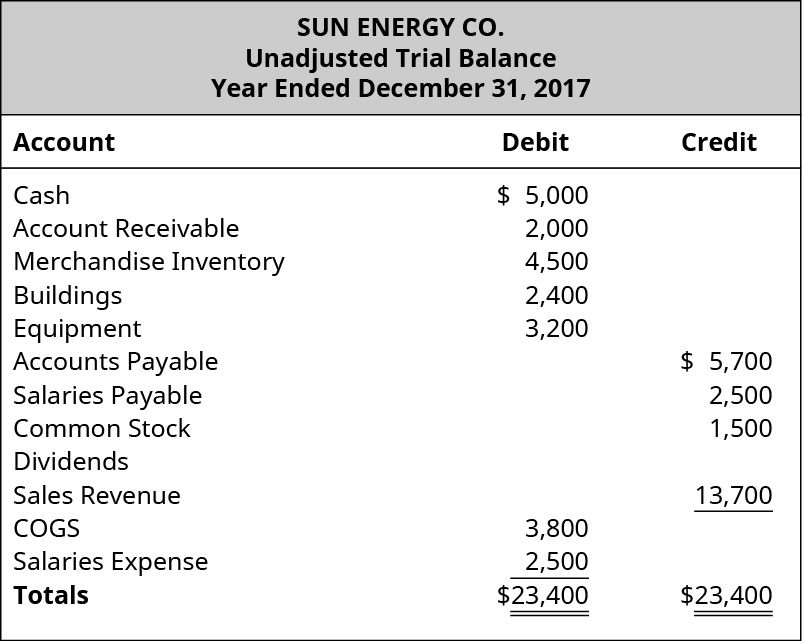

(Figure)Following is the unadjusted trial balance for Sun Energy Co. on December 31, 2017.

You are also given the following supplemental information: A pending lawsuit, claiming $2,700 in damages, is considered likely to favor the plaintiff and can be reasonably estimated. Sun Energy Co. believes a customer may win a lawsuit for $3,500 in damages, but the outcome is only reasonably possible to occur. Sun Energy calculated warranty expense estimates of $210.

- Using the unadjusted trial balance and supplemental information for Sun Energy Co., construct an income statement for the year ended December 31, 2017. Pay particular attention to expenses resulting from contingencies.

- Construct a balance sheet, for December 31, 2017, from the given unadjusted trial balance, supplemental information, and income statement for Sun Energy Co., paying particular attention to contingent liabilities.

- Prepare any necessary contingent liability note disclosures for Sun Energy Co. Only give one to three sentences for each contingency note disclosure.

Exercise Set B

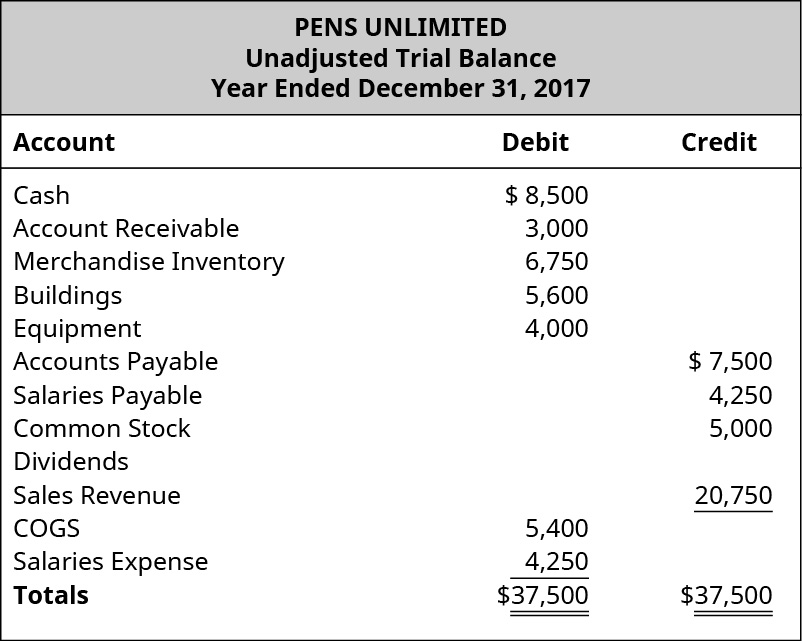

(Figure)Following is the unadjusted trial balance for Pens Unlimited on December 31, 2017.

You are also given the following supplemental information: A pending lawsuit, claiming $4,200 in damages, is considered likely to favor the plaintiff and can be reasonably estimated. Pens Unlimited believes a customer may win a lawsuit for $5,000 in damages, but the outcome is only reasonably possible to occur. Pens Unlimited records warranty estimates on the basis of 2% of annual sales revenue.

- Using the unadjusted trial balance and supplemental information for Pens Unlimited, construct an income statement for the year ended December 31, 2017. Pay particular attention to expenses resulting from contingencies.

- Construct a balance sheet, for December 31, 2017, from the given unadjusted trial balance, supplemental information, and income statement for Pens Unlimited. Pay particular attention to contingent liabilities.

- Prepare any necessary contingent liability note disclosures for Pens Unlimited. Only give one to three sentences for each contingency note disclosure.

Problem Set A

(Figure)Machine Corp. has several pending lawsuits against its company. Review each situation and (1) determine the treatment for each situation as probable and estimable, probable and inestimable, reasonably possible, or remote; (2) determine what, if any, recognition or note disclosure is required; and (3) prepare any journal entries required to recognize a contingent liability.

- A pending lawsuit, claiming $100,000 in damages, is considered likely to favor the plaintiff and can be reasonably estimated.

- Machine Corp. believes there might be other potential lawsuits about this faulty machinery, but this is unlikely to occur.

- A claimant sues Machine Corp. for damages, from a dishonored service contract agreement; the plaintiff will likely win the case but damages cannot be reasonably estimated.

- Machine Corp. believes a customer will win a lawsuit it filed, but the outcome is not likely and is not remote. It is possible the customer will win.

(Figure)Emperor Pool Services provides pool cleaning and maintenance services to residential clients. It offers a one-year warranty on all services. Review each of the transactions, and prepare any necessary journal entries for each situation.

- March 31: Emperor provides cleaning services for fifteen pools during the month of March at a sales price per pool of $550 cash. Emperor records warranty estimates when sales are recognized and bases warranty estimates on 2% of sales.

- April 5: A customer files a warranty claim that Emperor honors in the amount of $100 cash.

- April 13: Another customer, J. Jones, files a warranty claim that Emperor does not honor due to customer negligence.

- June 8: J. Jones files a lawsuit requesting damages related to the dishonored warranty in the amount of $1,500. Emperor determines that the lawsuit is likely to end in the plaintiff’s favor and the $1,500 is a reasonable estimate for damages.

Problem Set B

(Figure)Roundhouse Tools has several potential warranty claims as a result of damaged tool kits. Review each situation and (1) determine the treatment for each situation as probable and estimable, probable and inestimable, reasonably possible, or remote; (2) determine what, if any, recognition or note disclosure is required; and (3) prepare any journal entries required to recognize a contingent liability.

- Roundhouse Tools has several claims for replacement of another tool kit not listed as one of their damaged tool kits. The honored warranty for these tool kits is not likely but is not remote. It is possible.

- A pending warranty claim has been received with the projected cost to be $450. Roundhouse Tools believes honoring that warranty claim is likely to occur and that figure is reasonably estimated.

- Roundhouse Tools believes other potential warranties may have to be honored outside of the warranty period, but this is unlikely to occur.

- Warranty replacements will cost the company a percentage of sales for the period. This amount allotted for warranty replacements cannot be reasonably estimated but is likely to occur.

(Figure)Shoe Hut sells custom, handmade shoes. It offers a one-year warranty on all shoes for repair or replacement. Review each of the transactions and prepare any necessary journal entries for each situation.

- May 31: Shoe Hut sells 100 pairs of shoes during the month of May at a sales price per pair of shoes of $240 cash. Shoe Hut records warranty estimates when sales are recognized and bases warranty estimates on 4% of sales.

- June 2: A customer files a warranty claim that Shoe Hut honors in the amount of $30 for repair to laces. Laces Inventory corresponds to shoelace inventory used for repairs.

- June 4: Another customer files a warranty claim that Shoe Hut honors. Shoe Hut replaces the damaged shoes at a cost of $200, affecting their Shoe Replacement Inventory account.

- August 10: Shoe Hut explores the possibility of bankruptcy, given the current economic conditions (recession). It determines the bankruptcy is unlikely to occur (remote).

Thought Provokers

(Figure)Toyota is a car manufacturer that has issued several recalls over the years. One major recall centered on faulty air bags from Takata. A prior recall focused on unintentional pedal acceleration. Research information about the car manufacturer, and one of the two recall situations described. Answer the following questions:

- What are some of the main points discussed in the supplements you researched?

- What negative impact did this recall have on Toyota?

- As a result of the recall, what contingent liabilities were (or could be) created?

- How did Toyota handle the reporting of these contingent liabilities?

- How did Toyota determine the estimated liability amounts?

- Do you agree with Toyota’s treatment assignment for reported liabilities (probable and estimable, probable and inestimable, for example)?

- What note disclosures accompanied the recognized contingent liabilities?

- What long-term effect, if any, did the recall have on Toyota’s financials and reputation?

Glossary

- contingency

- current situation, where the outcome is unknown or uncertain and will not be resolved until a future point in time

- contingent liability

- uncertain outcome to a current condition that could produce a future debt or negative obligation for the company

- likelihood of occurrence

- contingent liability must be recognized and disclosed if there is a probable liability determination before the preparation of financial statements has occurred

- measurement requirement

- company’s ability to reasonably estimate the amount of loss

- probable and estimable

- contingent liability is likely to occur and can be reasonably estimated

- probable and inestimable

- contingent liability is likely to occur but cannot be reasonably estimated

- reasonably possible

- contingent liability could occur but is not probable

- remote

- contingent liability is unlikely to occur