LO 14.2 Differentiate between Operating, Investing, and Financing Activities

Mitchell Franklin

The statement of cash flows presents sources and uses of cash in three distinct categories: cash flows from operating activities, cash flows from investing activities, and cash flows from financing activities. Financial statement users are able to assess a company’s strategy and ability to generate a profit and stay in business by assessing how much a company relies on operating, investing, and financing activities to produce its cash flows.

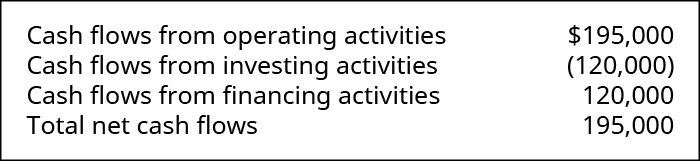

Assume you are the chief financial officer of T-Shirt Pros, a small business that makes custom-printed T-shirts. While reviewing the financial statements that were prepared by company accountants, you discover an error. During this period, the company had purchased a warehouse building, in exchange for a $200,000 note payable. The company’s policy is to report noncash investing and financing activities in a separate statement, after the presentation of the statement of cash flows. This noncash investing and financing transaction was inadvertently included in both the financing section as a source of cash, and the investing section as a use of cash.

T-Shirt Pros’ statement of cash flows, as it was prepared by the company accountants, reported the following for the period, and had no other capital expenditures.

Because of the misplacement of the transaction, the calculation of free cash flow by outside analysts could be affected significantly. Free cash flow is calculated as cash flow from operating activities, reduced by capital expenditures, the value for which is normally obtained from the investing section of the statement of cash flows. As their manager, would you treat the accountants’ error as a harmless misclassification, or as a major blunder on their part? Explain.

Cash Flows from Operating Activities

Cash flows from operating activities arise from the activities a business uses to produce net income. For example, operating cash flows include cash sources from sales and cash used to purchase inventory and to pay for operating expenses such as salaries and utilities. Operating cash flows also include cash flows from interest and dividend revenue interest expense, and income tax.

Cash Flows from Investing Activities

Cash flows from investing activities are cash business transactions related to a business’ investments in long-term assets. They can usually be identified from changes in the Fixed Assets section of the long-term assets section of the balance sheet. Some examples of investing cash flows are payments for the purchase of land, buildings, equipment, and other investment assets and cash receipts from the sale of land, buildings, equipment, and other investment assets.

Cash Flows from Financing Activities

Cash flows from financing activities are cash transactions related to the business raising money from debt or stock, or repaying that debt. They can be identified from changes in long-term liabilities and equity. Examples of financing cash flows include cash proceeds from issuance of debt instruments such as notes or bonds payable, cash proceeds from issuance of capital stock, cash payments for dividend distributions, principal repayment or redemption of notes or bonds payable, or purchase of treasury stock. Cash flows related to changes in equity can be identified on the Statement of Stockholder’s Equity, and cash flows related to long-term liabilities can be identified by changes in long-term liabilities on the balance sheet.

Investors do not always take a negative cash flow as a negative. For example, assume in 2018 Amazon showed a loss of $124 billion and a net cash outflow of $262 billion from investing activities. Yet during the same year, Amazon was able to raise a net $254 billion through financing. Why would investors and lenders be willing to place money with Amazon? For one thing, despite having a net loss, Amazon produced $31 billion cash from operating activities. Much of this was through delaying payment on inventories. Amazon’s accounts payable increased by $78 billion, while its inventory increased by $20 billion.

Another reason lenders and investors were willing to fund Amazon is that investing payments are often signs of a company growing. Assume that in 2018 Amazon paid almost $50 billion to purchase fixed assets and to acquire other businesses; this is a signal of a company that is growing. Lenders and investors interpreted Amazon’s cash flows as evidence that Amazon would be able to produce positive net income in the future. In fact, Amazon had net income of $19 billion in 2017. Furthermore, Amazon is still showing growth through its statement of cash flows; it spent about $26 billion in fixed equipment and acquisitions.

Key Concepts and Summary

- Transactions must be segregated into the three types of activities presented on the statement of cash flows: operating, investing, and financing.

- Operating cash flows arise from the normal operations of producing income, such as cash receipts from revenue and cash disbursements to pay for expenses.

- Investing cash flows arise from a company investing in or disposing of long-term assets.

- Financing cash flows arise from a company raising funds through debt or equity and repaying debt.

Multiple Choice

(Figure)Which of these transactions would not be part of the cash flows from the operating activities section of the statement of cash flows?

- credit purchase of inventory

- sales of product, for cash

- cash paid for purchase of equipment

- salary payments to employees

(Figure)Which is the proper order of the sections of the statement of cash flows?

- financing, investing, operating

- operating, investing, financing

- investing, operating, financing

- operating, financing, investing

B

(Figure)Which of these transactions would be part of the financing section?

- inventory purchased for cash

- sales of product, for cash

- cash paid for purchase of equipment

- dividend payments to shareholders, paid in cash

(Figure)Which of these transactions would be part of the operating section?

- land purchased, with note payable

- sales of product, for cash

- cash paid for purchase of equipment

- dividend payments to shareholders, paid in cash

B

(Figure)Which of these transactions would be part of the investing section?

- land purchased, with note payable

- sales of product, for cash

- cash paid for purchase of equipment

- dividend payments to shareholders, paid in cash

Questions

(Figure)What categories of activities are reported on the statement of cash flows? Does it matter in what order these sections are presented?

Operating, Investing, Financing (always in this order).

(Figure)Describe three examples of operating activities, and identify whether each of them represents cash collected or cash spent.

(Figure)Describe three examples of investing activities, and identify whether each of them represents cash collected or cash spent.

Any transaction that is related to acquiring or disposing of long-term assets like land, buildings, equipment, stocks, bonds, or other investments. Can be cash spent for purchase of long-term assets, or cash collected from sale of long-term assets.

(Figure)Describe three examples of financing activities, and identify whether each of them represents cash collected or cash spent.

Exercise Set A

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- paid advertising expense

- paid dividends to shareholders

- purchased business equipment

- sold merchandise to customers

- purchased plant assets

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- borrowed from the bank for business loan

- declared dividends, to be paid next year

- purchased treasury stock

- purchased a two-year insurance policy

- purchased plant assets

Exercise Set B

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- collected accounts receivable from customers

- issued common stock for cash

- declared and paid dividends

- paid accounts payable balance

- sold a long-term asset for the same amount as purchased

(Figure)In which section of the statement of cash flows would each of the following transactions be included? For each, identify the appropriate section of the statement of cash flows as operating (O), investing (I), financing (F), or none (N). (Note: some transactions might involve two sections.)

- purchased stock in Xerox Corporation

- purchased office supplies

- issued common stock

- sold plant assets for cash

- sold equipment for cash

Problem Set A

(Figure)Provide journal entries to record each of the following transactions. For each, also identify *the appropriate section of the statement of cash flows, and **whether the transaction represents a source of cash (S), a use of cash (U), or neither (N).

- paid $12,000 of accounts payable

- collected $6,000 from a customer

- issued common stock at par for $24,000 cash

- paid $6,000 cash dividend to shareholders

- sold products to customers for $15,000

- paid current month’s utility bill, $1,500

Problem Set B

(Figure)Provide journal entries to record each of the following transactions. For each, also identify: *the appropriate section of the statement of cash flows, and **whether the transaction represents a source of cash (S), a use of cash (U), or neither (N).

- reacquired $30,000 treasury stock

- purchased inventory for $20,000

- issued common stock of $40,000 at par

- purchased land for $25,000

- collected $22,000 from customers for accounts receivable

- paid $33,000 principal payment toward note payable to bank

Thought Provokers

(Figure)Use the EDGAR (Electronic Data Gathering, Analysis, and Retrieval system) search tools on the US Securities and Exchange Commission website to locate the latest Form 10-K for a company you would like to analyze. Submit a short memo that provides the following information:

- the name and ticker symbol of the company you have chosen

- the following information from the company’s statement of cash flows:

- amount of cash flows from operating activities

- amount of cash flows from investing activities

- amount of cash flows from financing activities

- the URL to the company’s Form 10-K to allow accurate verification of your answers

Glossary

- financing activity

- cash business transaction reported on the statement of cash flows that obtains or retires financing

- investing activity

- cash business transaction reported on the statement of cash flows from the acquisition or disposal of a long-term asset

- operating activity

- cash business transaction reported on the statement of cash flows that relates to ongoing day-to-day operations