Chapter 5 LO 3 — Explain and Compute Equivalent Units and Total Cost of Production in an Initial Processing Stage

As described previously, process costing can have more than one work in process account. Determining the value of the work in process inventory accounts is challenging because each product is at varying stages of completion and the computation needs to be done for each department. Trying to determine the value of those partial stages of completion requires application of the equivalent unit computation. The equivalent unit computation determines the number of units if each is manufactured in its entirety before manufacturing the next unit. For example, forty units that are 25% complete would be ten (40 × 25%) units that are totally complete.

Direct material is added in stages, such as the beginning, middle, or end of the process, while conversion costs are expensed evenly over the process. Often there is a different percentage of completion for materials than there is for labor. For example, if material is added at the beginning of the process, the forty units that are100% complete with respect to material and 25% complete with respect to conversion costs would be the same as forty units of material and ten units (40 × 25%) completed with conversion costs.

For example, during the month of July, Rock City Percussion purchased raw material inventory of $25,000 for the shaping department. Although each department tracks the direct material it uses in its own department, all material is held in the material storeroom. The inventory will be requisitioned for each department as needed.

During the month, Rock City Percussion’s shaping department requested $10,179 in direct material and started into production 8,700 hickory drumsticks of size 5A. There was no beginning inventory in the shaping department, and 7,500 drumsticks were completed in that department and transferred to the packaging department. Wood is the only direct material in the shaping department, and it is added at the beginning of the process, so the work in process (WIP) is considered to be 100% complete with respect to direct materials. At the end of the month, the drumsticks still in the shaping department were estimated to be 35% complete with respect to conversion costs. All materials are added at the beginning of the shaping process. While beginning the size 5A drumsticks, the shaping department incurred these costs in July:

These costs are then used to calculate the equivalent units and total production costs in a four-step process. The Four Steps Needed to Determine the Cost of Units Completed in a Department and the Cost of Units Left in Ending WIP:

- 1. Determine the Units to Which Costs Will Be Assigned (reconcile physical units)

- 2. Compute the Equivalent Units of Production (calculate equivalent units)

- 3. Determine the Cost per Equivalent Unit (calculate cost per equivalent unit)

- 3.a. Summarize total costs to account for

- 3.b. Calculate cost per equivalent unit

- 4. Allocate the Costs to the Units Transferred Out and Partially Completed (assign cost to units completed in department and to units in ending WIP in department)

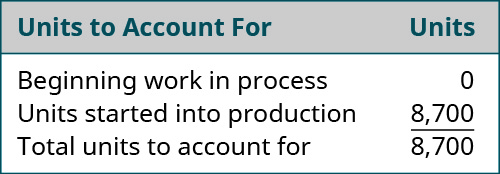

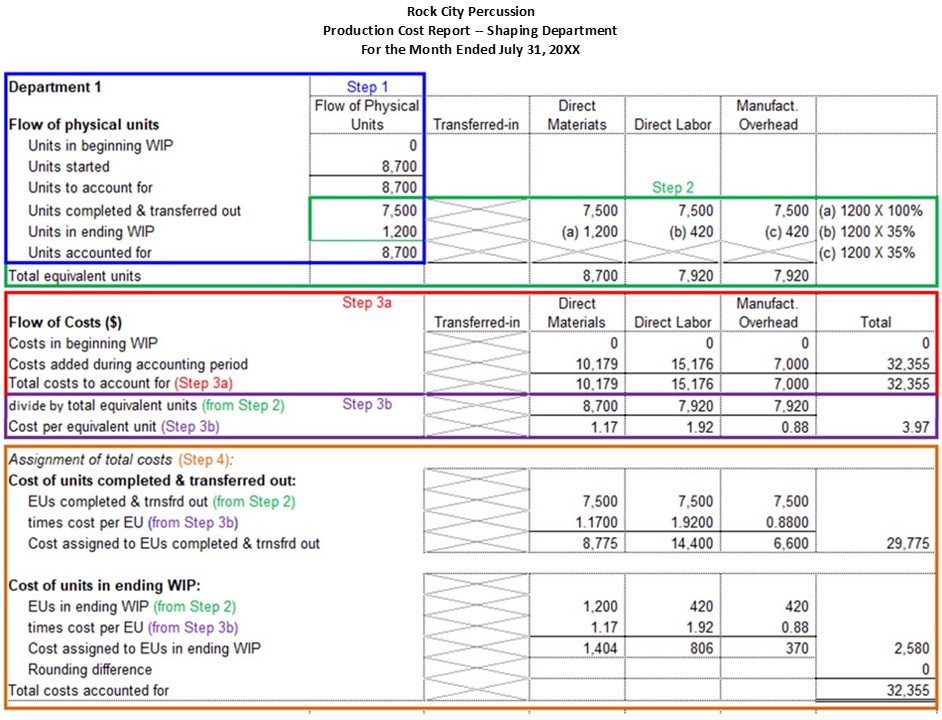

Step One: Reconcile Physical Units

In addition to the equivalent units, it is necessary to track the units completed as well as the units remaining in ending inventory. A similar process is used to account for the costs completed and transferred. Reconciling the number of units and the costs is part of the process costing system. The reconciliation involves the total of beginning inventory and units started into production. This total is called “units to account for,” while the total of beginning inventory costs and costs added to production is called “costs to be accounted for.” Knowing the total units or costs to account for is helpful since it also equals the units or costs transferred out plus the amount remaining in ending inventory.

When the new batch of hickory sticks was started on July 1, Rock City Percussion did not have any beginning inventory and started 8,700 units, so the total number of units to account for in the reconciliation is 8,700:

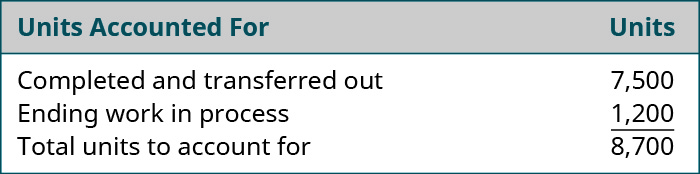

The shaping department completed 7,500 units and transferred them to the packaging department. No units were lost to spoilage, which consists of any units that are not fit for sale due to breakage or other imperfections. Since the maximum number of units that could possibly be completed is 8,700, the number of units in the shaping department’s ending inventory must be 1,200. The total of the 7,500 units completed and transferred out and the 1,200 units in ending inventory equal the 8,700 possible units in the shaping department.

Step Two: Calculate Equivalent Units

All of the materials have been added to the shaping department, but all of the conversion elements have not; the numbers of equivalent units for material costs and for conversion costs remaining in ending inventory are different. All of the units transferred to the next department must be 100% complete with regard to that department’s cost or they would not be transferred. So the number of units transferred is the same for material units and for conversion units. The process cost system must calculate the equivalent units of production for units completed (with respect to materials and conversion) and for ending work in process with respect to materials and conversion.

For the shaping department, the materials are 100% complete with regard to materials costs and 35% complete with regard to conversion costs. [Note: In a classroom setting, you will always be given the percent complete (35% in this case). But in the real world, estimating what percent of the labor and overhead are reflected in the work-in-process can be challenging depending on the nature of the production process.] The 7,500 units completed and transferred out to the packaging department must be 100% complete with regard to materials and conversion, so they make up 7,500 (7,500 ×100%) units. The 1,200 ending work in process units are 100% complete with regard to material so we have 1,200 (1,200 × 100%) equivalent units for material. The 1,200 ending work in process units are only 35% complete with regard to conversion costs and represent 420 (1,200 × 35%) equivalent units.

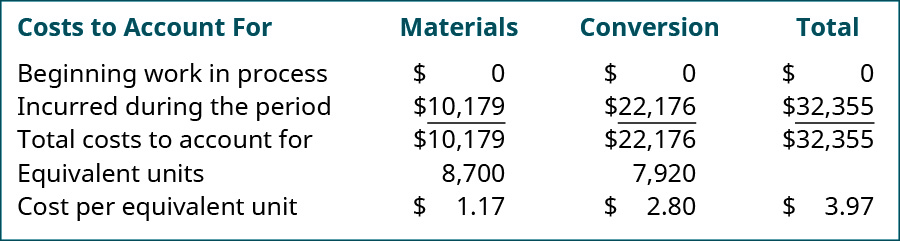

Step Three: Calculate Cost per Equivalent Unit

Once the equivalent units for materials and conversion are known, the cost per equivalent unit is computed in a similar manner as the units accounted for. The costs for material and conversion need to reconcile with the total beginning inventory and the costs incurred for the department during that month.

The total materials costs for the period (including any beginning inventory costs) is computed and divided by the equivalent units for materials. The same process is then completed for the total conversion costs. The total of the cost per unit for material ($1.17) and for conversion costs ($2.80) is the total cost of each unit transferred to the packaging department ($3.97).

Step Four: Allocate the Costs to the Units Transferred Out and to Units Partially Completed in the Shaping Department

Now you can determine the cost of the units transferred out and the cost of the units still in process in the shaping department. To calculate the goods transferred out, simply take the units transferred out times the sum of the two equivalent unit costs (materials and conversion) because all items transferred to the next department are complete with respect to materials and conversion, so each unit brings all its costs. But the ending WIP value is determined by taking the product of the work in process material units and the cost per equivalent unit for materials plus the product of the work in process conversion units and the cost per equivalent unit for conversion.

This information is accumulated in a production cost report. This report shows the costs used in the preparation of a product, including the cost per unit for materials and conversion costs, and the amount of work in process and finished goods inventory. A complete production cost report for the shaping department is illustrated in Figure 5.6 below.

Your Turn

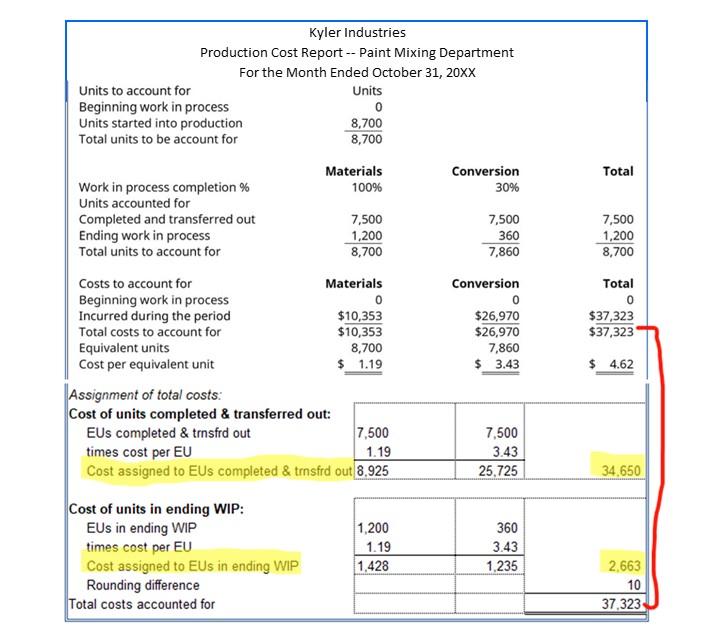

Kyler Industries started a new batch of paint on October 1. The new batch consists of 8,700 cans of paint, of which 7,500 was completed and transferred to finished goods. During October, the manufacturing process recorded the following expenses: direct materials of $10,353; direct labor of $17,970; and applied overhead of $9,000. The inventory still in process is 100% complete with respect to materials and 30% complete with respect to conversion. What is the cost of inventory transferred out and work in process? Assume that there is no beginning work in process inventory.

(Solution below)

Solution to Kyler Industries:

KEY TAKEAWAYS

Key Concepts and Summary

-

- Process costing has a work in process inventory account for each department.

- Equivalent units of production for materials may differ from the equivalent units for conversion costs.

- The total units to account for is the number of units in the beginning work in process inventory plus the number of units started into production; this total also represents the sum of the number of units completed and the number of units in the ending work in process inventory.

- The cost per equivalent unit for materials is the total of the material costs for the beginning work in process inventory and the total of material costs incurred during the period.

- The cost per equivalent unit for conversion costs is the total of the conversion costs for the beginning work in process inventory and the total of conversion costs incurred during the period.

- The cost of units transferred to the next department is the number of units transferred times the total of the cost per equivalent unit of material plus the cost per equivalent unit for conversion costs.

Glossary

- production cost report

- shows the costs used in the preparation of a product, including the cost per unit for materials and conversion costs and the amount of work in process and finished goods inventory

- spoilage

- any units that are not fit for sale due to breakage or other imperfections