LO 7.5 Explain How Budgets Are Used to Evaluate Goals

As you’ve learned, an advantage of budgeting is evaluating performance. Having a strong understanding of their budgets helps managers keep track of expenses and work toward the company’s goals. Companies need to understand their revenue and expense details to develop budgets as a tool for planning operations and cash flow. Part of understanding revenue and expenses is evaluating the prior year. Did the company earn the expected profit? Could it have earned a higher profit? What expenses or revenues were not on the budget? Critically evaluating the actual results versus the estimated budgetary results can help management plan for the future. Variance analysis helps the manager analyze its results. It does not necessarily find a problem, but it does indicate where a problem may exist. The same is true for favorable variances as well as unfavorable variances. A favorable variance occurs when revenue is higher than budgeted or expenses are lower than budgeted. An unfavorable variance is when revenue is lower than budgeted or expenses are higher than budgeted.

| Comparing Favorable to Unfavorable Variances | |

|---|---|

| Favorable | Unfavorable |

| Actual Sales > Budgeted Sales | Actual Sales < Budgeted Sales |

| Actual Expenses < Budgeted Expenses | Actual Expenses > Budgeted expenses |

It is easy to understand that an unfavorable variance may be a problem. But that is not always true, as a higher labor rate may mean the company has a higher quality employee who is able to waste less material. Likewise, having a favorable variance indicates that more revenue was earned or less expenses were incurred but further analysis can indicate if costs were cut too far and better materials should have been purchased.

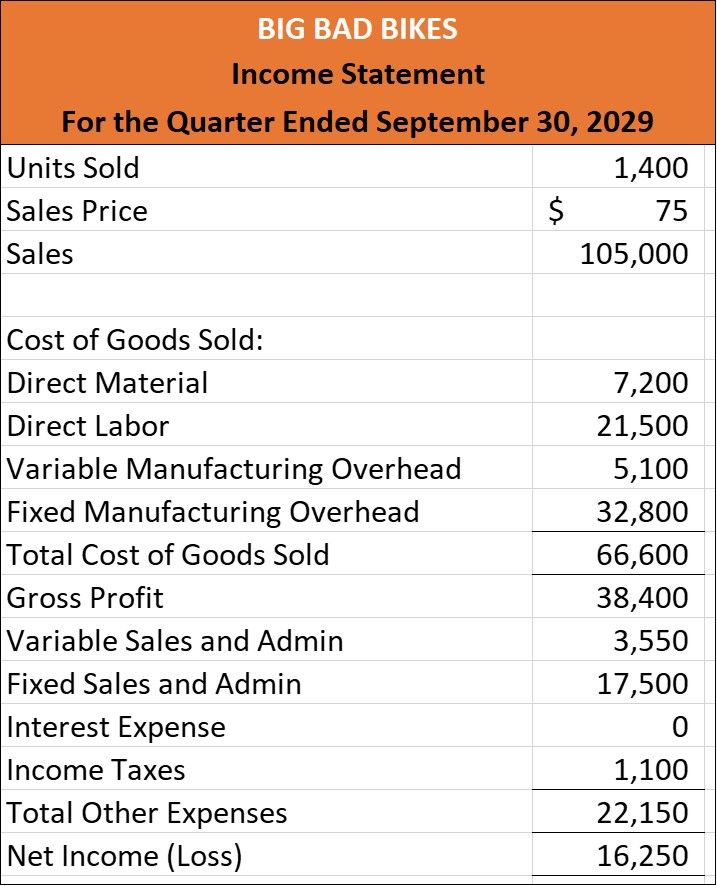

If a company has only a static budget, meaningful comparisons are difficult. Analyzing the sales for Bid Bad Bikes will illustrate whether there was a profit and how net income impacts the company. In the third quarter, Big Bad Bikes sold 1,400 trainers and had third quarter net income of $16,250 as shown below.

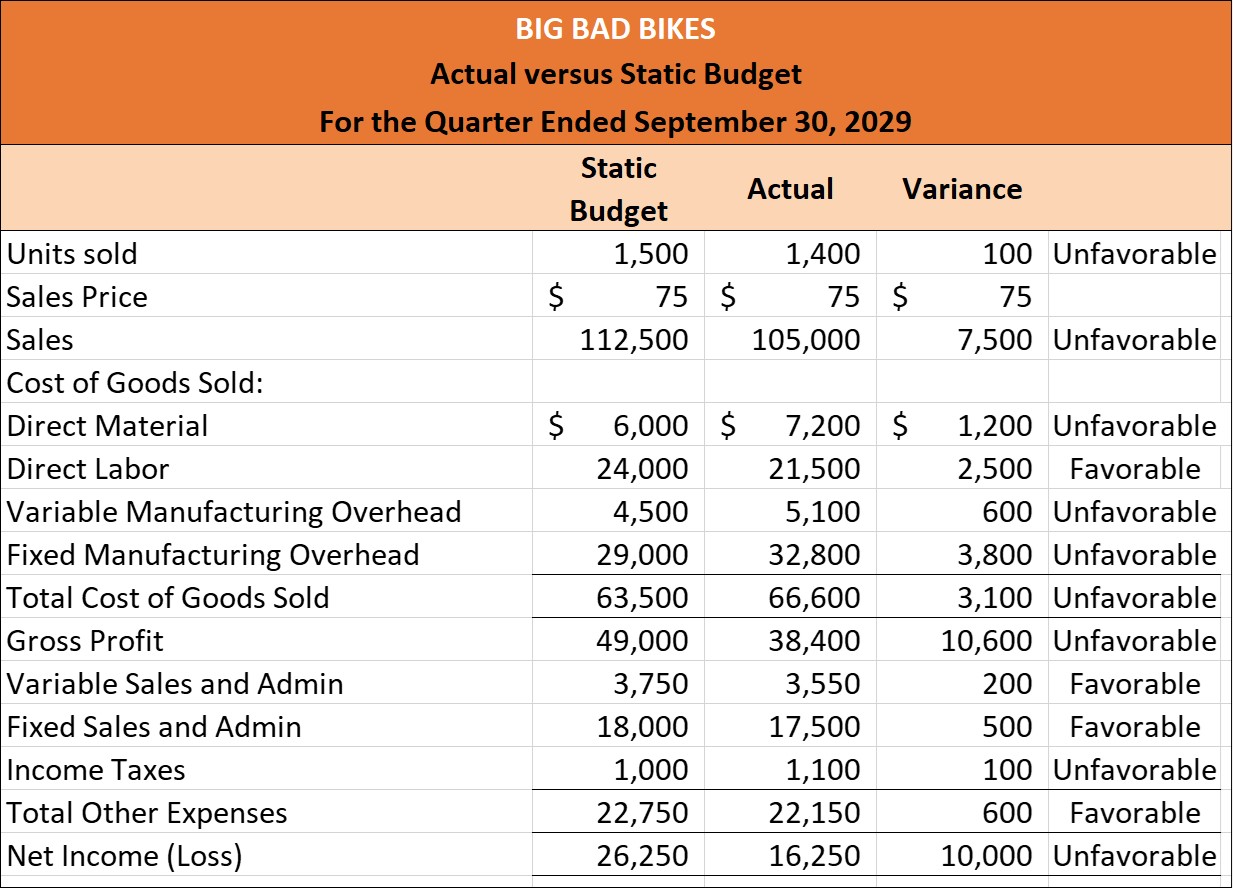

The company earned a profit during the third quarter, but what does that mean to the company? Simply having net income instead of a net loss does not help plan for the future. The third quarter static budget was for the sale of 1,500 units. Comparing that budget to the actual results shows whether there is a favorable variance or an unfavorable variance. A comparison of the actual costs with the budget for the third quarter, as shown below, shows unfavorable variances related to revenue, but some favorable and unfavorable variances related to expenses.

How do those results advise management when evaluating the company’s performance? It is difficult to look at one variance and make a conclusion about the company or its management. However, the variances can help narrow down the areas that need addressing because they differ from the budgeted amount. For example, looking at the variance when using a static budget does not indicate the amount of the variance results because they sold 100 fewer units than budgeted. The variance for direct labor is favorable, but it should be if production was less than the budget. A static budget does not evaluate whether costs for 1,400 were appropriate for production of those 1,400 units.

Using a static budget to evaluate performance affects the bottom line as well as the individual expenses. The net income for the sale of 1,400 units is less than the budgeted net income for 1,500 units, but it does not indicate whether expenses were appropriate for 1,400 units. If there had been 1,600 units sold, the expenses would be more than the budgeted amount, but sales would be higher. Would it be fair to evaluate a manager’s control over their expenses using a static budget?

ETHICAL CONSIDERATIONS

Why is ethics training important? An organization that bases a manager’s evaluation and pay on how close to the budget the division performs may inadvertently encourage that manager to act unethically in order to get a pay raise. Many employees manipulate the budget process to enhance their earnings by garnering bonuses based upon questionably ethical behavior and improper financial reporting. Generally, this unethical behavior involves either manipulating the numbers in the budget or modifying the timing of reports to apply income to a different budget period. Kenton Walker and Gary Fleischman studied ethics in budgeting and determined that certain ethics-related structures in a business created a better operational environment.

The study found that the existence of formal ethical codes, ethics training, good management role models, and social pressure to be disclosing within an organization can be a deterrent to budget manipulation by employees. The authors recommended: “Therefore, organizations should carefully cultivate an ethical atmosphere that is sensitive to the pressures employees may feel to game the budget through actions that involve cheating and/or manipulating earnings targets to maximize bonuses.” 1 The study concluded that requiring organizational ethics training that includes role playing helps teach ethical behavior in budgeting and other areas of business. Ethics training never goes out so style.

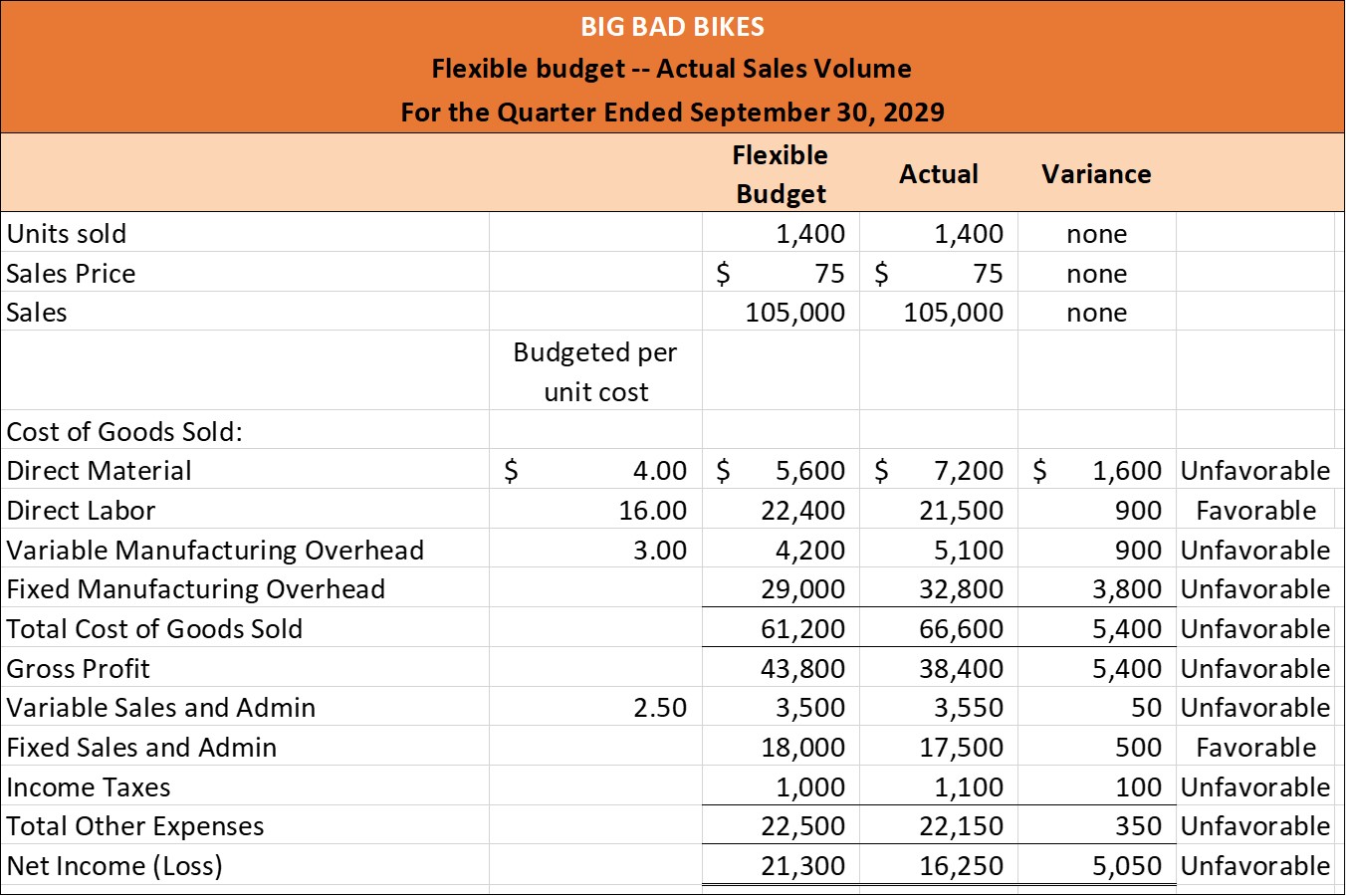

Here is BBB’s flexible budget for 2029 quarter 3, based on actual number of units sold.

Evaluating the expenses on a flexible budget computed for the number of units sold would provide an indication of management’s ability to control expenses. As shown below, some expenses have a favorable variance, while others have an unfavorable variance. This type of variance analysis provides more information than static budget variances to evaluate management and help prepare the next year’s budget. For example, the direct materials in the flexible budget comparison shows an unfavorable variance, meaning the actual direct materials expense was more than budgeted for the production of 1,400 units. What we don’t know is whether the unfavorable variance was caused by BBB having to pay more than $1.25 per unit of material, or if each unit of product required more than 3.2 pounds of material, or some combination of both. Of course, we have tools to help us tease apart the components of the flexible budget variances. More about this in another chapter.

THINK IT THROUGH

You are beginning your own business and developed a budget based on modest sales and expense assumptions. The actual results are very close to the budget at the end of the first and second months. During the third month, both cash collected and paid differ significantly from the budget. What could be the cause and what should you do?

LINK TO LEARNING

KEY TAKEAWAYS

Key Concepts and Summary

- Management’s evaluations of the actual results versus the estimated budgetary results help plan for the future.

- Favorable variances occur when sales are higher or expenses are lower than budgeted.

- Unfavorable variances occur when sales are lower or expenses are higher than budgeted.

Footnotes

- 1 Kenton B. Walker, et al. “Toeing the Line: The Ethics of Manipulating Budgets and Earnings.” Management Accounting Quarterly 14, no. 3 (Spring 2013). https://www.imanet.org/-/media/f4869589d9d444de8c211d245a0192ff.ashx

Adapted from Principles of Accounting, Volume 2: Managerial Accounting (c) 2019 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-managerial-accounting