LO 3.5 Use Journal Entries to Record Transactions and Post to T-Accounts

When we introduced lefts and rights based on the accounting equation (debits and credits), you learned about the usefulness of T-accounts as a graphic representation of any account in the general ledger. But before transactions are posted to the T-accounts, they are first recorded using special forms known as journals.

Journals

Accountants use special forms called journals to keep track of their business transactions. A journal is the first place information is entered into the accounting system. A journal is often referred to as the book of original entry because it is the place the information originally enters into the system. A journal keeps a historical account of all recordable transactions with which the company has engaged. In other words, a journal is similar to a diary for a business. When you enter information into a journal, we say you are journalizing the entry. Journaling the entry is the second step in the accounting cycle. Here is a picture of a journal.

You can see that a journal has columns labeled debit and credit (left and right). Let’s look at how we use a journal.

When filling in a journal, there are some rules you need to follow to improve journal entry organization.

Formatting When Recording Journal Entries

- Include a date of when the transaction occurred.

- The left (debit) account title(s) always come first and on the left.

- The right (credit) account title(s) always come after all debit titles are entered, and on the right.

- The titles of the accounts on the right will be indented below the accounts on the left.

- You will have at least one left (debit) (possibly more).

- You will always have at least one right (credit) (possibly more).

- The dollar value of the lefts (debits) must equal the dollar value of the rights (credits) or else the equation will go out of balance.

- You will write a short description after each journal entry.

- Skip a row after the description before starting the next journal entry.

An example journal entry format is as follows. It is not taken from previous examples but is intended to stand alone.

Note that this example has only one left account and one right account, which is considered a simple entry. A compound entry is when there is more than one account listed under the left and/or right column of a journal entry (as seen in the following).

Notice that for this entry, the rules for recording journal entries have been followed. There is a date of April 1, 2018, the left account titles are listed first with Cash and Supplies, the right account title of Common Stock is indented after the left account titles, there are at least one left (debit) and one right (credit), the left (debit) amounts equal the right (credit) amount, and there is a short description of the transaction.

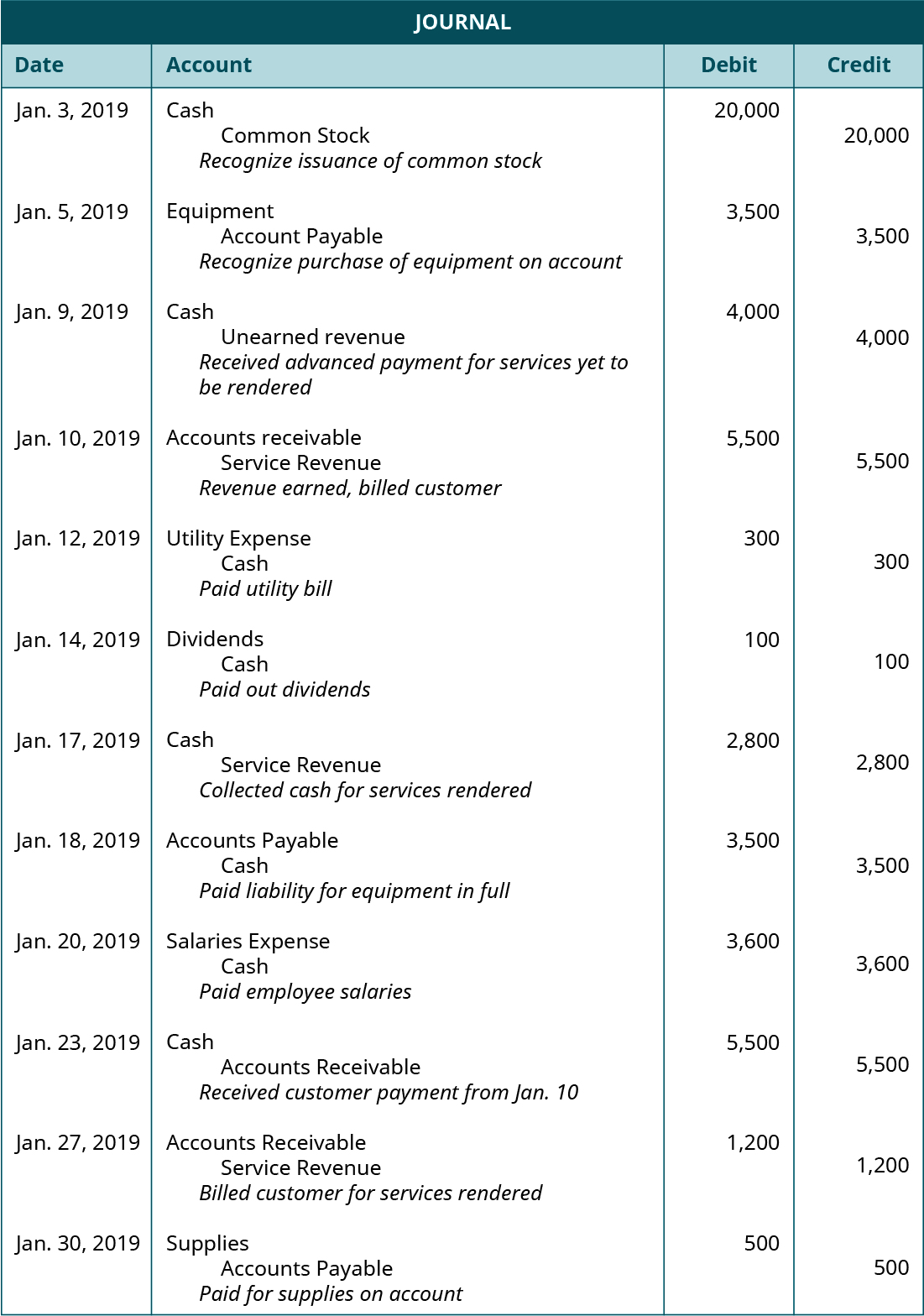

Let’s now look at a few transactions from Printing Plus and record their journal entries.

Recording Transactions

We now return to our company example of Printing Plus, Lynn Sanders’ printing service company. We will analyze and record each of the transactions for her business and discuss how this impacts the financial statements. Some of the listed transactions have been ones we have seen throughout this chapter. More detail for each of these transactions is provided, along with a few new transactions.

- On January 3, 2019, issues $20,000 shares of common stock for cash.

- On January 5, 2019, purchases equipment on account for $3,500, payment due within the month.

- On January 9, 2019, receives $4,000 cash in advance from a customer for services not yet rendered.

- On January 10, 2019, provides $5,500 in services to a customer who asks to be billed for the services.

- On January 12, 2019, pays a $300 utility bill with cash.

- On January 14, 2019, distributed $100 cash in dividends to stockholders.

- On January 17, 2019, receives $2,800 cash from a customer for services rendered.

- On January 18, 2019, paid in full, with cash, for the equipment purchase on January 5.

- On January 20, 2019, paid $3,600 cash in salaries expense to employees.

- On January 23, 2019, received cash payment in full from the customer on the January 10 transaction.

- On January 27, 2019, provides $1,200 in services to a customer who asks to be billed for the services.

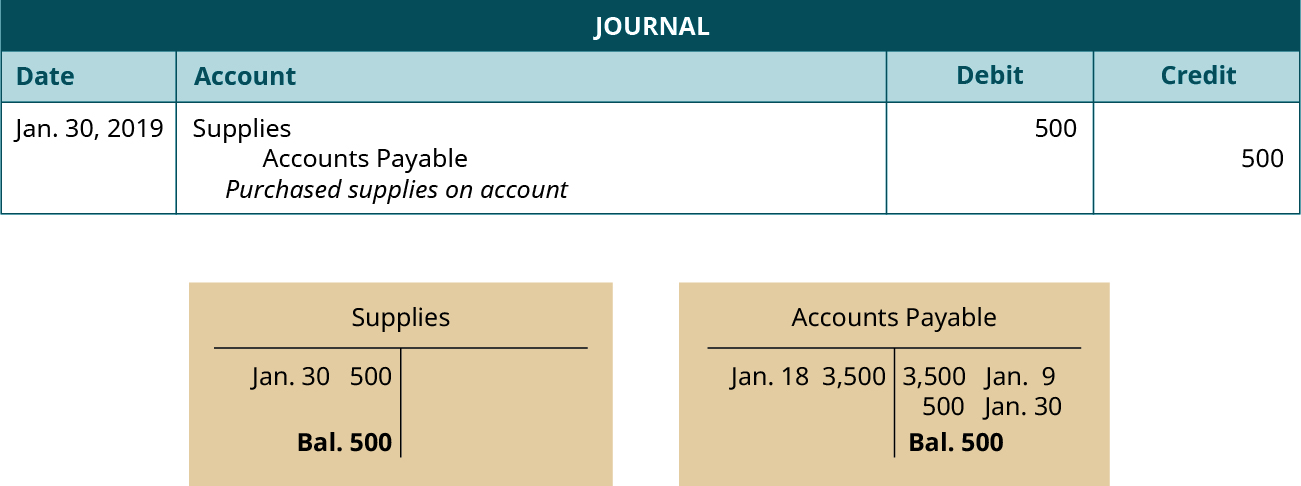

- On January 30, 2019, purchases supplies on account for $500, payment due within three months.

Transaction 1: On January 3, 2019, issues $20,000 shares of common stock for cash.

Analysis:

- This is a transaction that needs to be recorded, as Printing Plus has received money, and the stockholders have invested in the firm.

- Printing Plus now has more cash. Cash is an asset, which in this case is increasing. Cash increases on the left/debit side.

- When the company issues stock, stockholders purchase common stock, yielding a higher common stock figure than before issuance. The common stock account is increasing and affects equity. Looking at the expanded accounting equation, we see that Common Stock increases on the right/credit side.

Impact on the financial statements: Both of these accounts are balance sheet accounts. You will see total assets increase and total stockholders’ equity will also increase, both by $20,000. With both totals increasing by $20,000, the accounting equation, and therefore our balance sheet, will be in balance. There is no effect on the income statement from this transaction as there were no revenues or expenses recorded.

Transaction 2: On January 5, 2019, purchases equipment on account for $3,500, payment due within the month.

Analysis:

- In this case, equipment is an asset that is increasing. It increases because Printing Plus now has more equipment than it did before. Assets increase on the left/debit side; therefore, the Equipment account would show a $3,500 left/debit.

- The company did not pay for the equipment immediately. Lynn asked to be sent a bill for payment at a future date. This creates a liability for Printing Plus, who owes the supplier money for the equipment. Accounts Payable is used to recognize this liability. This liability is increasing, as the company now owes money to the supplier. A liability account increases on the right/credit side; therefore, Accounts Payable will increase on the right/credit side in the amount of $3,500.

Impact on the financial statements: Since both accounts in the entry are balance sheet accounts, you will see no effect on the income statement.

Transaction 3: On January 9, 2019, receives $4,000 cash in advance from a customer for services not yet rendered.

Analysis:

- Cash was received, thus increasing the Cash account. Cash is an asset that increases on the left/debit side.

- Printing Plus has not yet provided the service, meaning it cannot recognize the revenue as earned. The company has a liability to the customer until it provides the service. The Unearned Revenue account would be used to recognize this liability. This is a liability the company did not have before, thus increasing this account. Liabilities increase on the right/credit side; thus, Unearned Revenue will recognize the $4,000 on the right/credit side.

Impact on the financial statements: Since both accounts in the entry are balance sheet accounts, you will see no effect on the income statement.

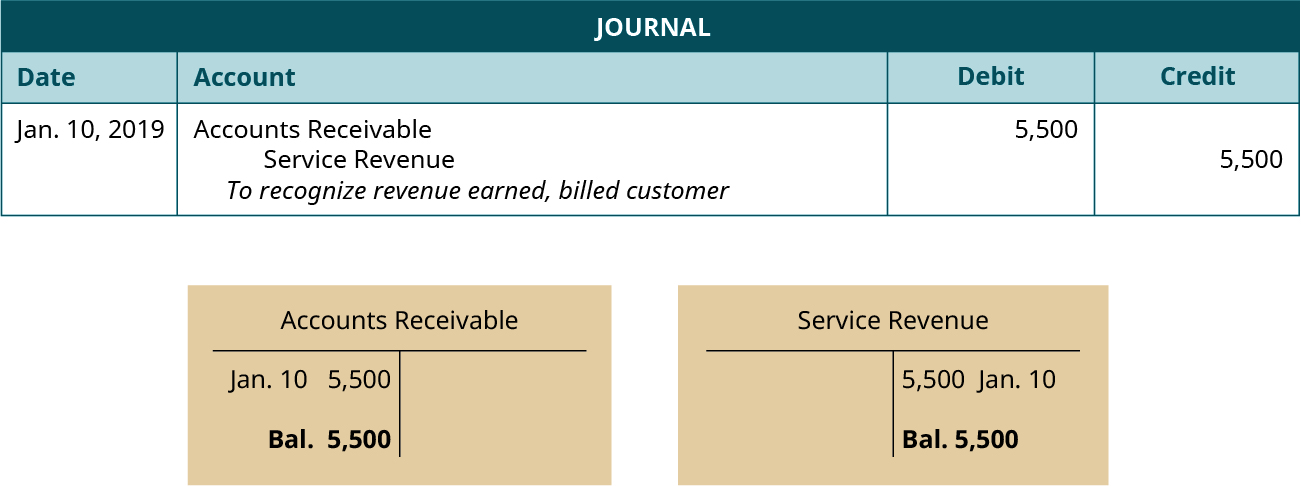

Transaction 4: On January 10, 2019, provides $5,500 in services to a customer who asks to be billed for the services.

Analysis:

- The company provided service to the client; therefore, the company may recognize the revenue as earned (revenue recognition principle), which increases revenue. Service Revenue is a revenue account affecting equity. Revenue accounts increase on the right/credit side; thus, Service Revenue will show an increase of $5,500 on the right/credit side.

- The customer did not immediately pay for the services and owes Printing Plus payment. This money will be received in the future, increasing Accounts Receivable. Accounts Receivable is an asset account. Asset accounts increase on the left/debit side. Therefore, Accounts Receivable will increase for $5,500 on the left/debit side.

Impact on the financial statements: You have revenue of $5,500. Revenue is reported on your income statement. The more revenue you have, the more net income (earnings) you will have. The more earnings you have, the more retained earnings you will keep. Retained earnings is a stockholders’ equity account, so total equity will increase $5,500. Accounts receivable is going up so total assets will increase by $5,500. The accounting equation, and therefore the balance sheet, remain in balance.

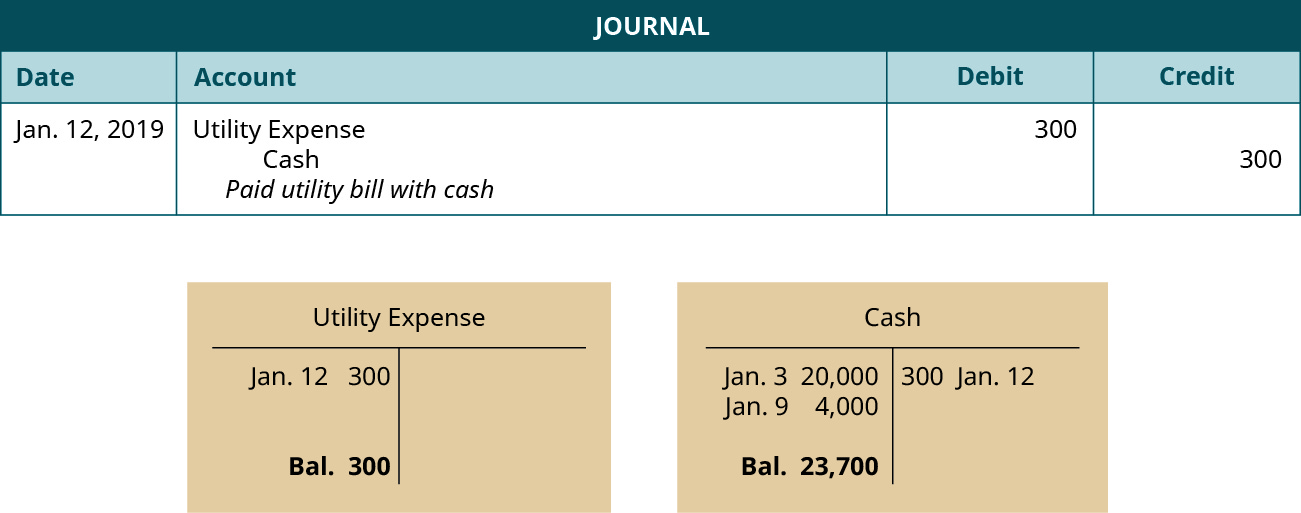

Transaction 5: On January 12, 2019, pays a $300 utility bill with cash.

Analysis:

- Cash was used to pay the utility bill, which means cash is decreasing. Cash is an asset that decreases on the right/credit side.

- Paying a utility bill creates an expense for the company. Utility Expense increases, and does so on the left/debit side of the accounting equation.

Impact on the financial statements: You have an expense of $300. Expenses are reported on your income statement. More expenses lead to a decrease in net income (earnings). The fewer earnings you have, the fewer retained earnings you will end up with. Retained earnings is a stockholders’ equity account, so total equity will decrease by $300. Cash is decreasing, so total assets will decrease by $300, impacting the balance sheet.

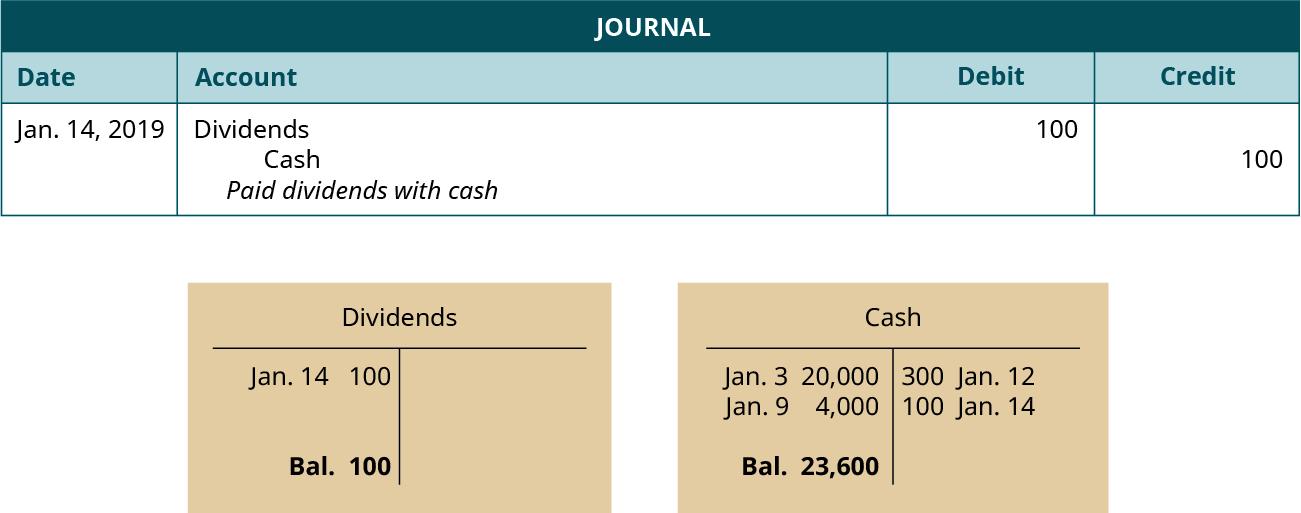

Transaction 6: On January 14, 2019, distributed $100 cash in dividends to stockholders.

Analysis:

- Cash was used to pay the dividends, which means cash is decreasing. Cash is an asset that decreases on the right/credit side.

- Dividends distribution occurred, which increases the Dividends account. Dividends is a part of stockholder’s equity and is recorded on the left/debit side. This left/debit entry has the effect of reducing stockholder’s equity.

Impact on the financial statements: You have dividends of $100. An increase in dividends leads to a decrease in stockholders’ equity (retained earnings). Cash is decreasing, so total assets will decrease by $100, impacting the balance sheet.

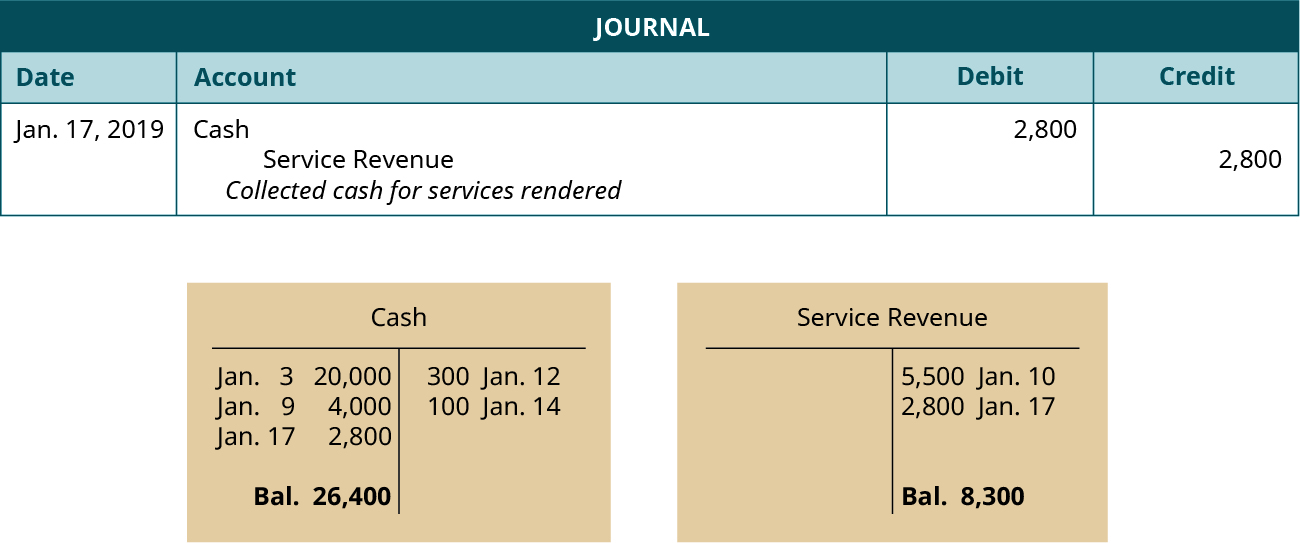

Transaction 7: On January 17, 2019, receives $2,800 cash from a customer for services rendered.

Analysis:

- The customer used cash as the payment method, thus increasing the amount in the Cash account. Cash is an asset that is increasing, and it does so on the left/debit side.

- Printing Plus provided the services, which means the company can recognize revenue as earned in the Service Revenue account. Service Revenue increases equity; therefore, Service Revenue increases on the right/credit side.

Impact on the financial statements: Revenue is reported on the income statement. More revenue will increase net income (earnings), thus increasing retained earnings. Retained earnings is a stockholders’ equity account, so total equity will increase $2,800. Cash is increasing, which increases total assets on the balance sheet.

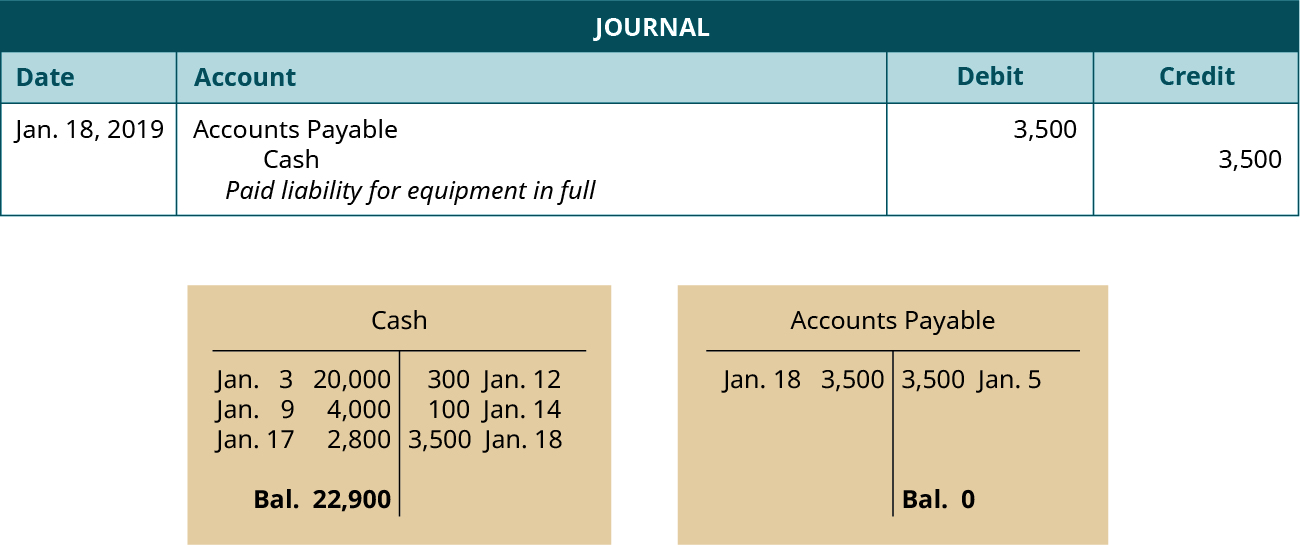

Transaction 8: On January 18, 2019, paid in full, with cash, for the equipment purchase on January 5.

Analysis:

- Cash is decreasing because it was used to pay for the outstanding liability created on January 5. Cash is an asset and will decrease on the right/credit side.

- Accounts Payable recognized the liability the company had to the supplier to pay for the equipment. Since the company is now paying off the debt it owes, this will decrease Accounts Payable. Liabilities decrease on the left/debit side; therefore, Accounts Payable will decrease on the left/debit side by $3,500.

Impact on the financial statements: Since both accounts in the entry are balance sheet accounts, you will see no effect on the income statement.

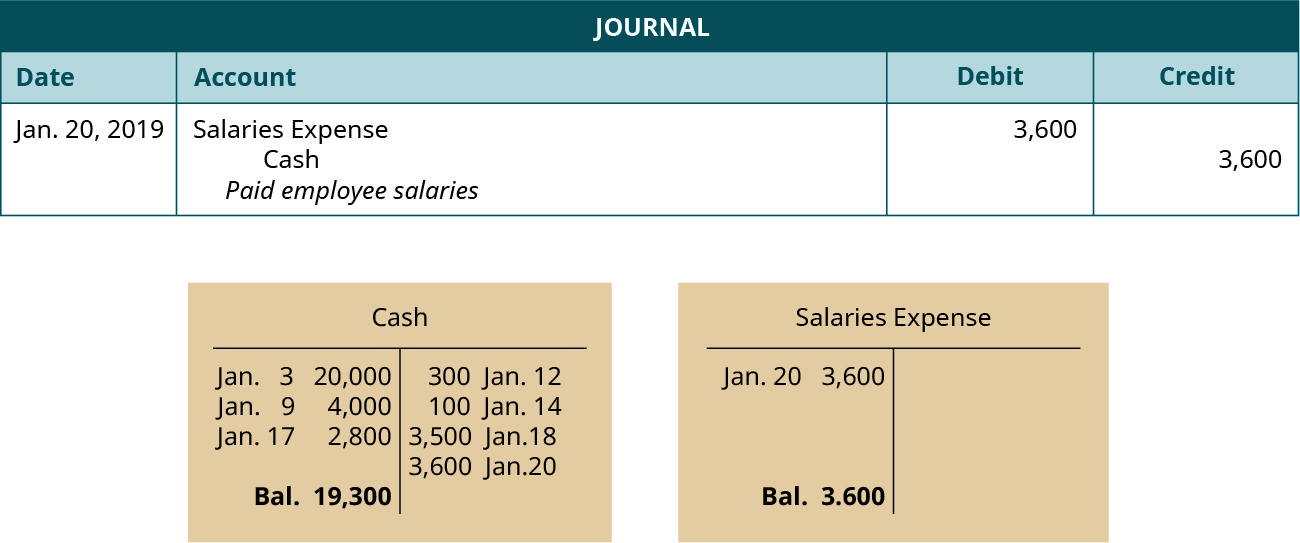

Transaction 9: On January 20, 2019, paid $3,600 cash in salaries expense to employees.

Analysis:

- Cash was used to pay for salaries, which decreases the Cash account. Cash is an asset that decreases on the right/credit side.

- Salaries are an expense to the business for employee work. This will increase Salaries Expense, affecting equity. Expenses increase on the left/debit side; thus, Salaries Expense will increase on the left/debit side.

Impact on the financial statements: You have an expense of $3,600. Expenses are reported on the income statement. More expenses lead to a decrease in net income (earnings). The fewer earnings you have, the fewer retained earnings you will end up with. Retained earnings is a stockholders’ equity account, so total equity will decrease by $3,600. Cash is decreasing, so total assets will decrease by $3,600, impacting the balance sheet.

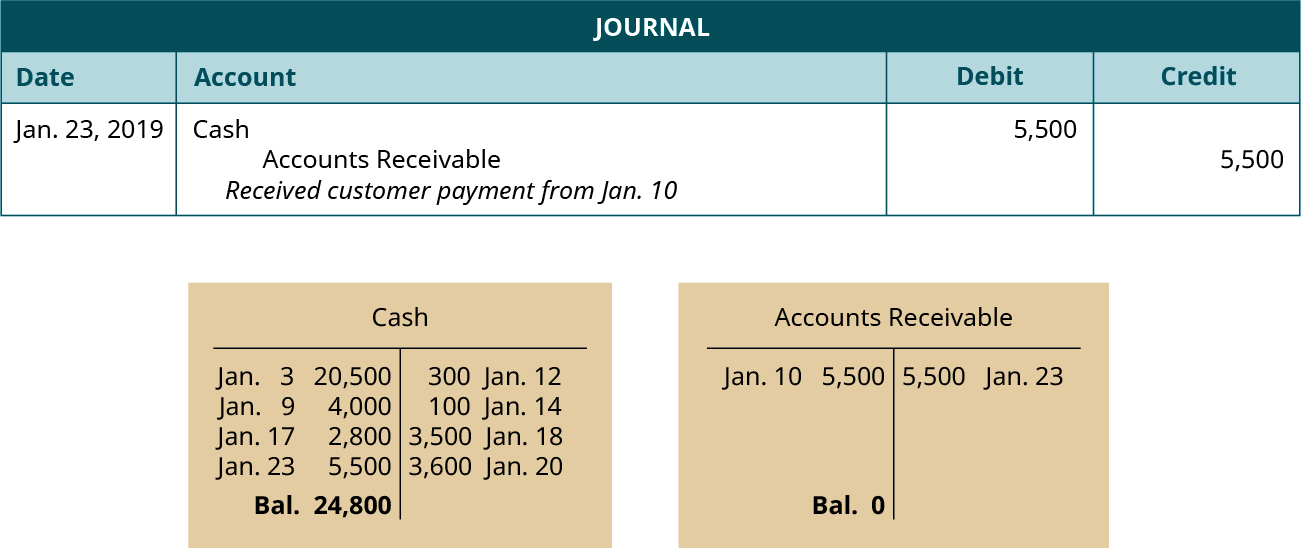

Transaction 10: On January 23, 2019, received cash payment in full from the customer on the January 10 transaction.

Analysis:

- Cash was received, thus increasing the Cash account. Cash is an asset, and assets increase on the left/debit side.

- Accounts Receivable was originally used to recognize the future customer payment; now that the customer has paid in full, Accounts Receivable will decrease. Accounts Receivable is an asset, and assets decrease on the right/credit side.

Impact on the financial statements: In this transaction, there was an increase to one asset (Cash) and a decrease to another asset (Accounts Receivable). This means total assets change by $0, because the increase and decrease to assets in the same amount cancel each other out. There are no changes to liabilities or stockholders’ equity, so the equation is still in balance. Since there are no revenues or expenses affected, there is no effect on the income statement.

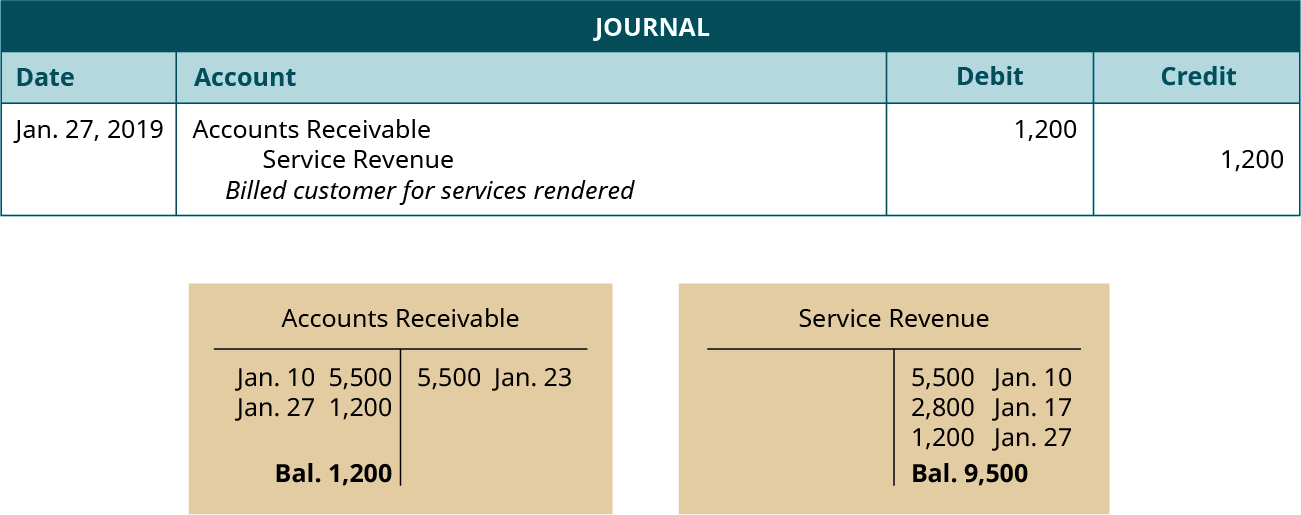

Transaction 11: On January 27, 2019, provides $1,200 in services to a customer who asks to be billed for the services.

Analysis:

- The customer does not pay immediately for the services but is expected to pay at a future date. This creates an Accounts Receivable for Printing Plus. The customer owes the money, which increases Accounts Receivable. Accounts Receivable is an asset, and assets increase on the left/debit side.

- Printing Plus provided the service, thus earning revenue. Service Revenue would increase on the right/credit side.

Impact on the financial statements: Revenue is reported on the income statement. More revenue will increase net income (earnings), thus increasing retained earnings. Retained earnings is a stockholders’ equity account, so total equity will increase $1,200. Cash is increasing, which increases total assets on the balance sheet.

Transaction 12: On January 30, 2019, purchases supplies on account for $500, payment due within three months.

Analysis:

- The company purchased supplies, which are assets to the business until used. Supplies is increasing, because the company has more supplies than it did before. Supplies is an asset that is increasing on the left/debit side.

- Printing Plus did not pay immediately for the supplies and asked to be billed for the supplies, payable at a later date. This creates a liability for the company, Accounts Payable. This liability increases Accounts Payable; thus, Accounts Payable increases on the right/credit side.

Impact on the financial statements: There is an increase to a liability and an increase to assets. These accounts both impact the balance sheet but not the income statement.

The complete journal for these transactions is as follows:

We now look at the next step in the accounting cycle, step 3: post journal information to the ledger.

CONTINUING APPLICATION AT WORK

Colfax Market is a small corner grocery store that carries a variety of staple items such as meat, milk, eggs, bread, and so on. As a smaller grocery store, Colfax does not offer the variety of products found in a larger supermarket or chain. However, it records journal entries in a similar way.

Grocery stores of all sizes must purchase product and track inventory. While the number of entries might differ, the recording process does not. For example, Colfax might purchase food items in one large quantity at the beginning of each month, payable by the end of the month. Therefore, it might only have a few accounts payable and inventory journal entries each month. Larger grocery chains might have multiple deliveries a week, and multiple entries for purchases from a variety of vendors on their accounts payable weekly.

This similarity extends to other retailers, from clothing stores to sporting goods to hardware. No matter the size of a company and no matter the product a company sells, the fundamental accounting entries remain the same.

Posting to the General Ledger

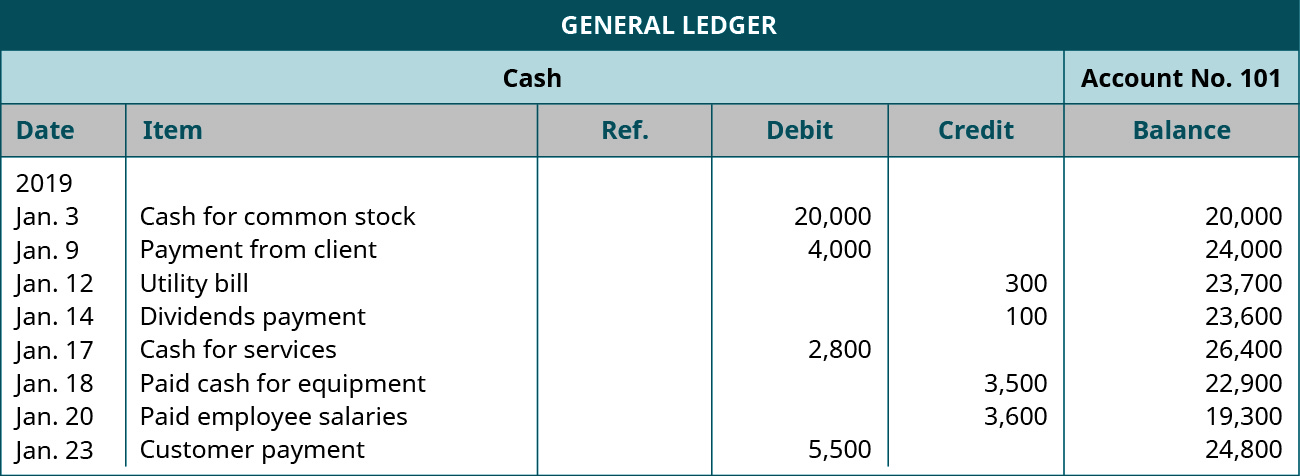

Recall that the general ledger is a record of each account and its balance. Reviewing journal entries individually can be tedious and time consuming. The general ledger is helpful in that a company can easily extract account and balance information. Here is a small section of a general ledger.

You can see at the top is the name of the account “Cash,” as well as the assigned account number “101.” Remember, all asset accounts will start with the number 1. The date of each transaction related to this account is included, a possible description of the transaction, and a reference number if available. There are debit and credit columns, storing the financial figures for each transaction, and a balance column that keeps a running total of the balance in the account after every transaction.

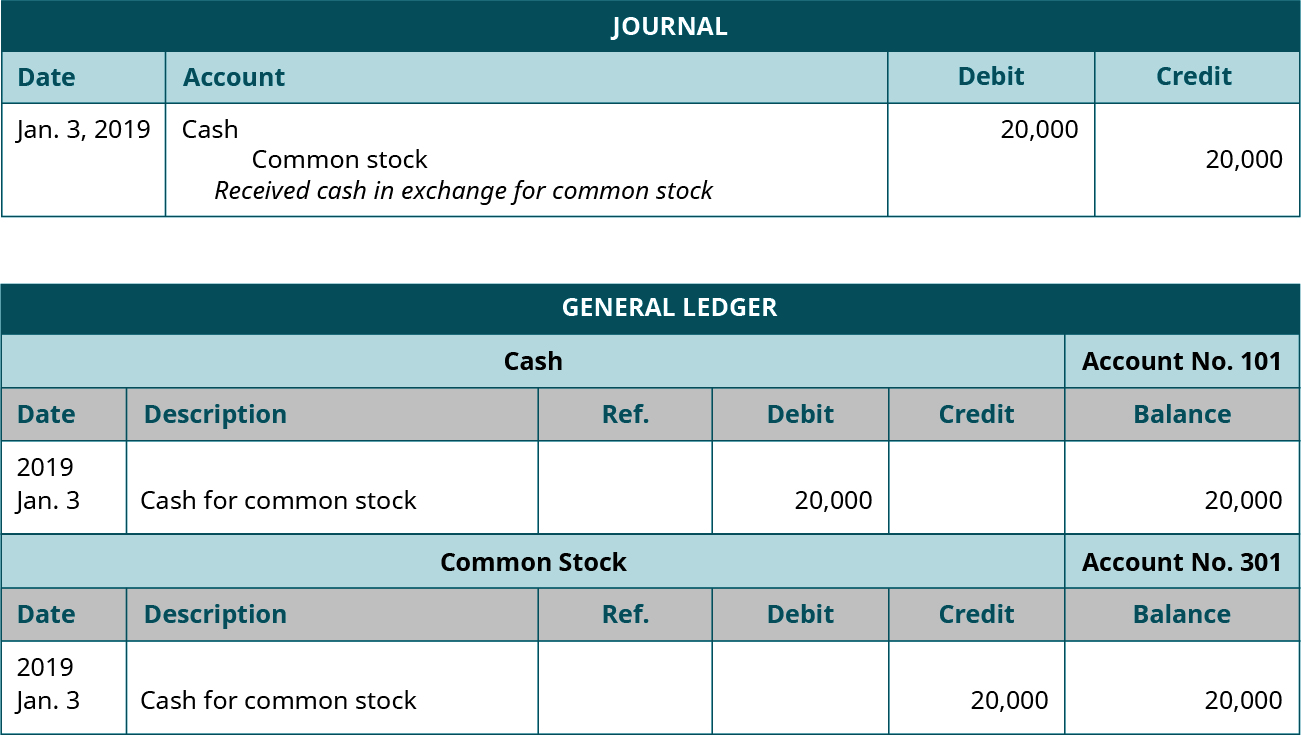

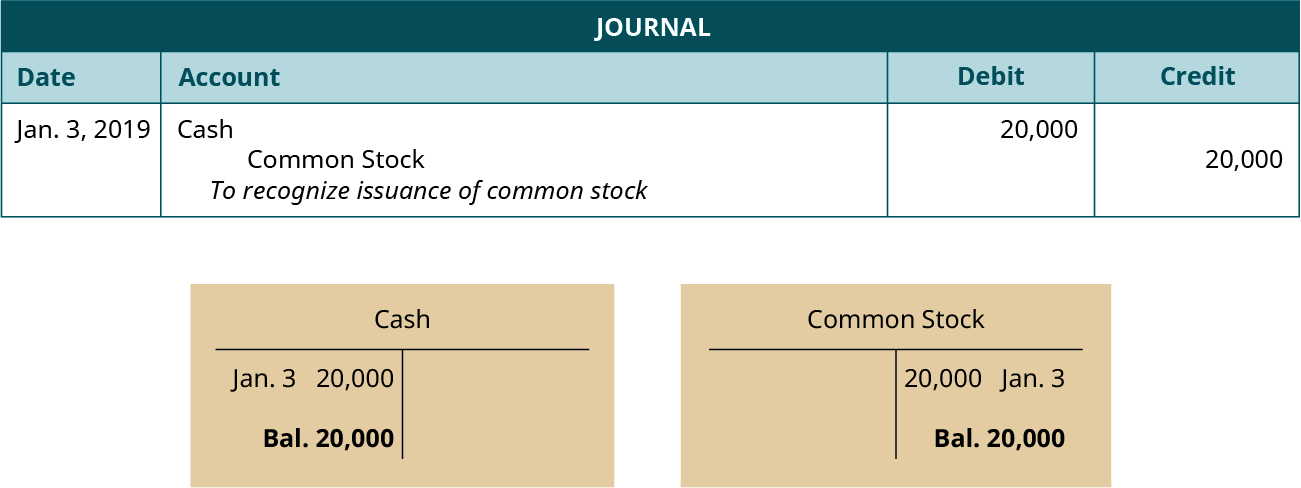

Let’s look at one of the journal entries from Printing Plus and fill in the corresponding ledgers.

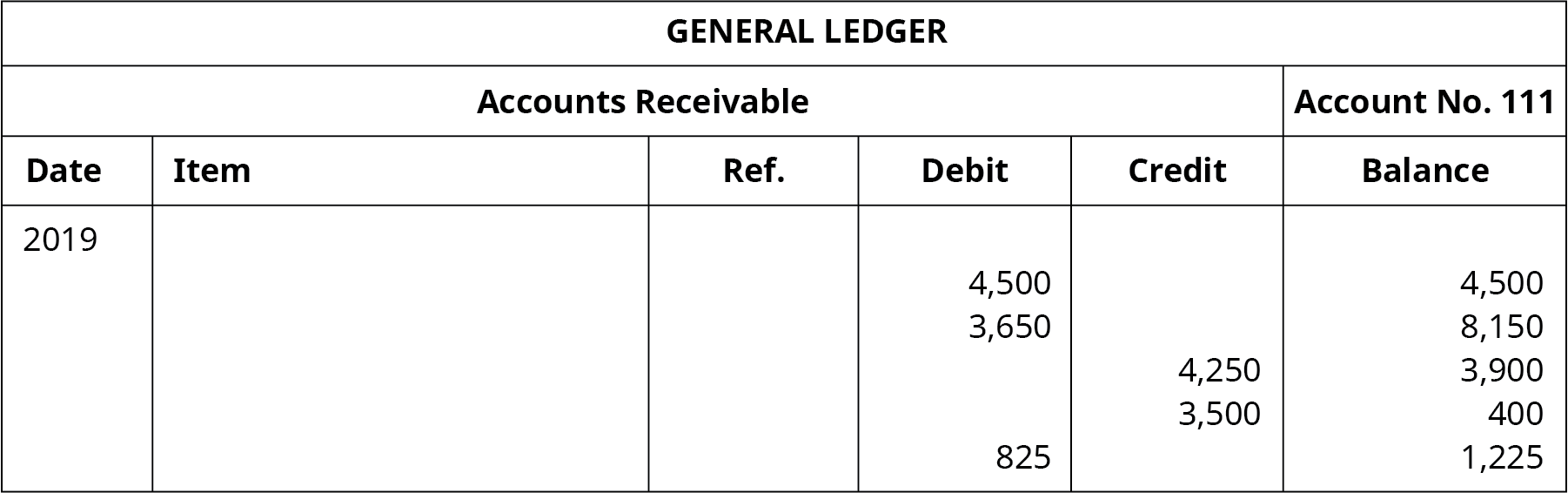

As you can see, there is one ledger account for Cash and another for Common Stock. Cash is labeled account number 101 because it is an asset account type. The date of January 3, 2019, is in the far left column, and a description of the transaction follows in the next column. Cash had a left/debit of $20,000 in the journal entry, so $20,000 is transferred to the general ledger in the left/debit side of the transaction columns. The balance in this account is currently $20,000, because no other transactions have affected this account yet.

Common Stock has the same date and description. Common Stock had a right/credit of $20,000 in the journal entry, and that information is transferred to the general ledger account in the right/credit side of the transaction columns. The balance at that time in the Common Stock ledger account is $20,000.

Another key element to understanding the general ledger, and the third step in the accounting cycle, is how to calculate balances in ledger accounts.

LINK TO LEARNING

Calculating Account Balances

When calculating balances in ledger accounts, one must take into consideration which side of the account increases and which side decreases. To find the account balance, you must find the difference between the sum of all figures on the side that increases and the sum of all figures on the side that decreases.

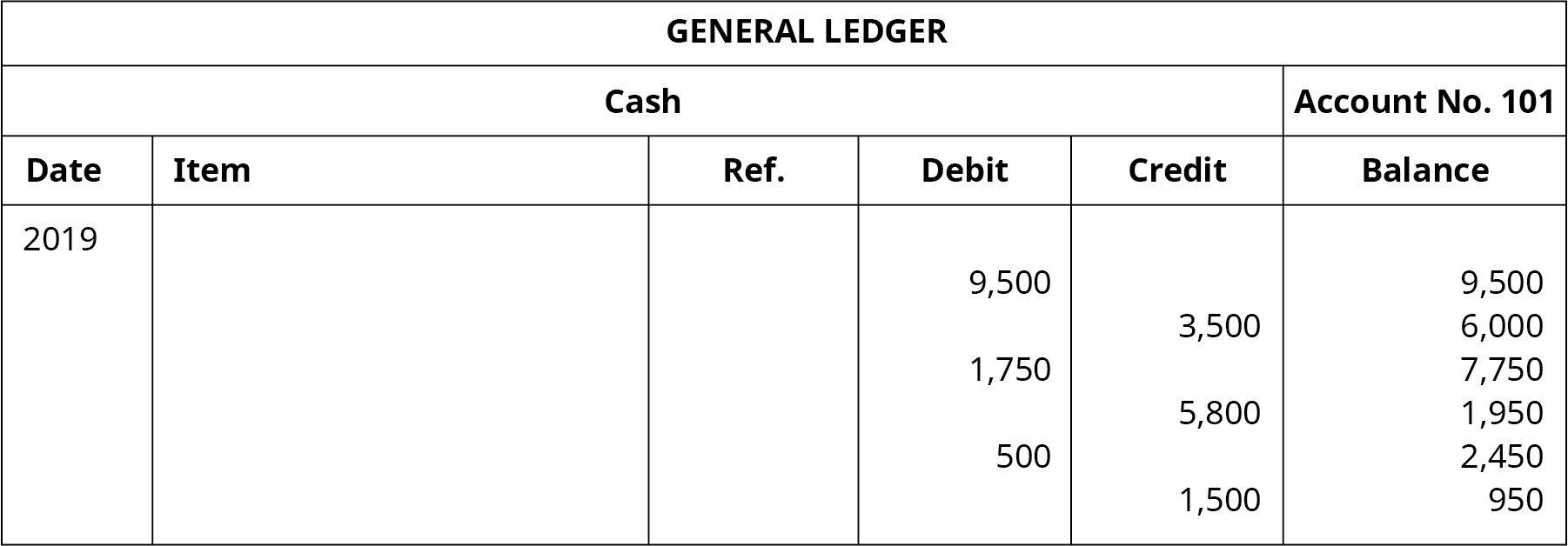

For example, the Cash account is an asset. We know from the accounting equation that assets increase on the left/debit side and decrease on the right/credit side. If there was a left/debit of $5,000 and a right/credit of $3,000 in the Cash account, we would find the difference between the two, which is $2,000 (5,000 – 3,000). The left/debit is the larger of the two sides ($5,000 on the left/debit side as opposed to $3,000 on the right/credit side), so the Cash account has a left/debit balance of $2,000.

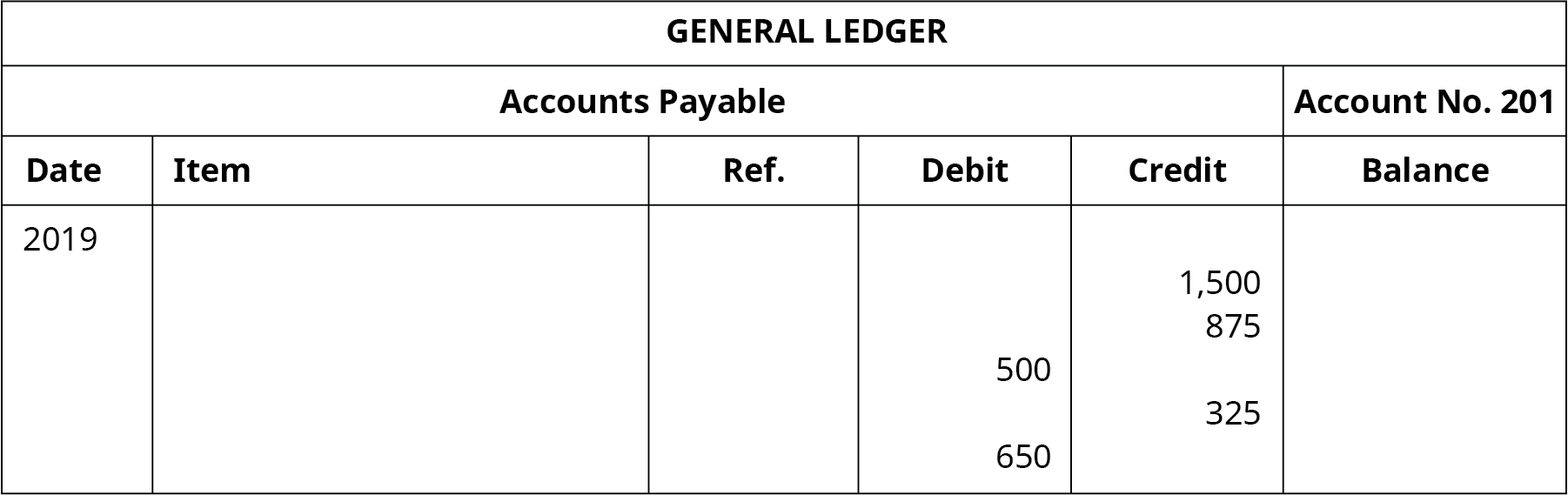

Another example is a liability account, such as Accounts Payable, which increases on the right/credit side and decreases on the left/debit side. If there were a $4,000 right/credit and a $2,500 left/debit, the difference between the two is $1,500. The right/credit is the larger of the two sides ($4,000 on the right/credit side as opposed to $2,500 on the left/debit side), so the Accounts Payable account has a right/credit balance of $1,500.

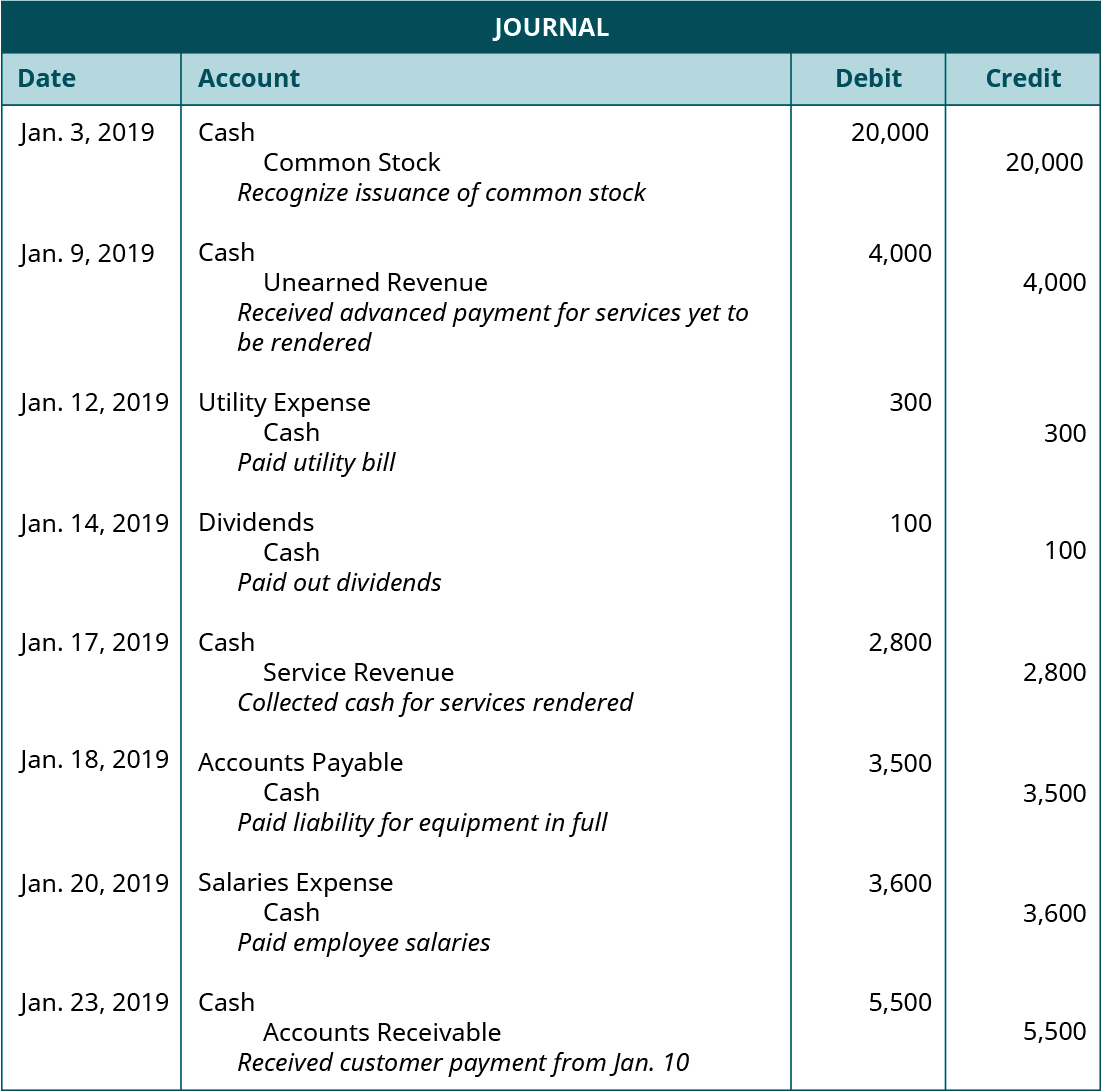

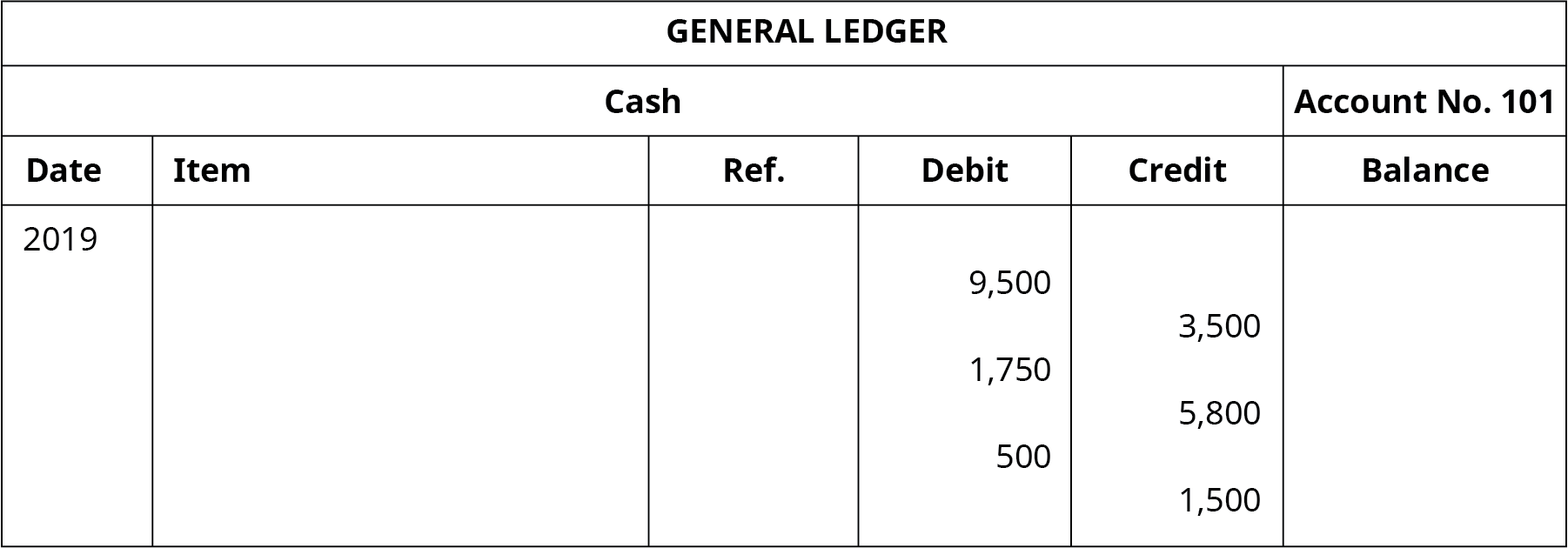

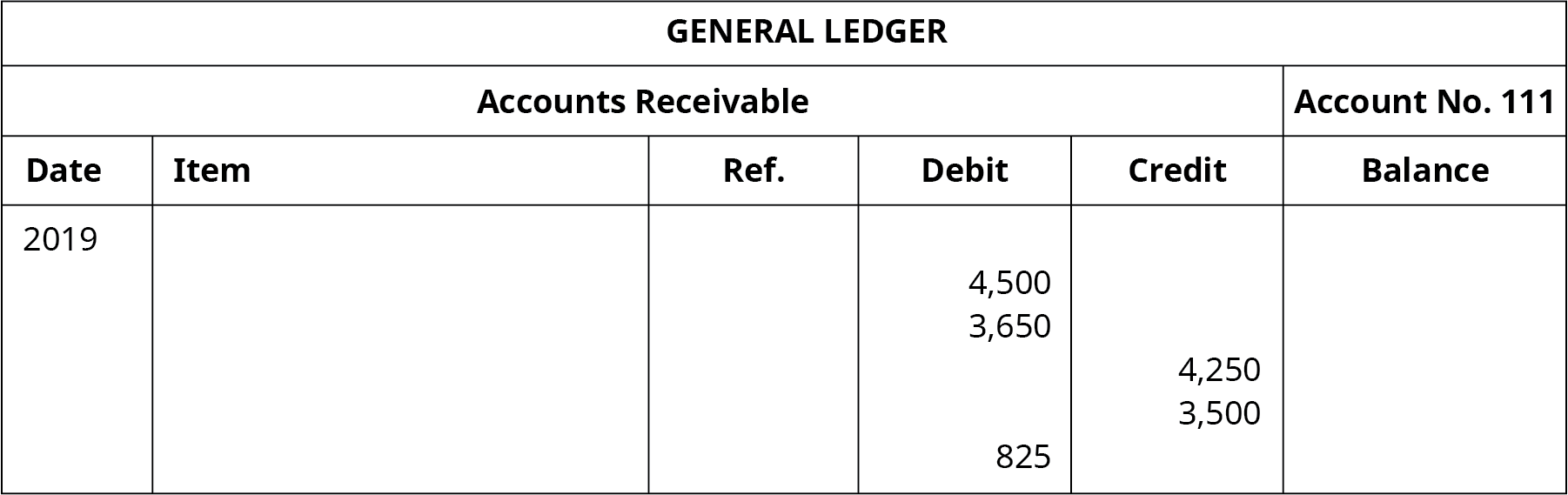

The following are selected journal entries from Printing Plus that affect the Cash account. We will use the Cash ledger account to calculate account balances.

The general ledger account for Cash would look like the following:

In the last column of the Cash ledger account is the running balance. This shows where the account stands after each transaction, as well as the final balance in the account. How do we know on which side, debit or credit, to input each of these balances? Let’s consider the general ledger for Cash.

On January 3, there was a debit balance of $20,000 in the Cash account. On January 9, a debit of $4,000 was included. Since both are on the debit side, they will be added together to get a balance on $24,000 (as is seen in the balance column on the January 9 row). On January 12, there was a credit of $300 included in the Cash ledger account. Since this figure is on the credit side, this $300 is subtracted from the previous balance of $24,000 to get a new balance of $23,700. The same process occurs for the rest of the entries in the ledger and their balances. The final balance in the account is $24,800.

Checking to make sure the final balance figure is correct; one can review the figures in the debit and credit columns. In the debit column for this cash account, we see that the total is $32,300 (20,000 + 4,000 + 2,800 + 5,500). The credit column totals $7,500 (300 + 100 + 3,500 + 3,600). The difference between the debit and credit totals is $24,800 (32,300 – 7,500). The balance in this Cash account is a debit of $24,800. Having a debit balance in the Cash account is the normal balance for that account.

Posting to the T-Accounts

The third step in the accounting cycle is to post journal information to the ledger. To do this we can use a T-account format. A company will take information from its journal and post to this general ledger. Posting refers to the process of transferring data from the journal to the general ledger. It is important to understand that T-accounts are only used for illustrative purposes in a textbook, classroom, or business discussion. They are not official accounting forms. Companies will use ledgers for their official books, not T-accounts.

Let’s look at the journal entries for Printing Plus and post each of those entries to their respective T-accounts.

The following are the journal entries recorded earlier for Printing Plus.

Transaction 1: On January 3, 2019, issues $20,000 shares of common stock for cash.

In the journal entry, Cash has a debit of $20,000. This is posted to the Cash T-account on the debit side (left side). Common Stock has a credit balance of $20,000. This is posted to the Common Stock T-account on the credit side (right side).

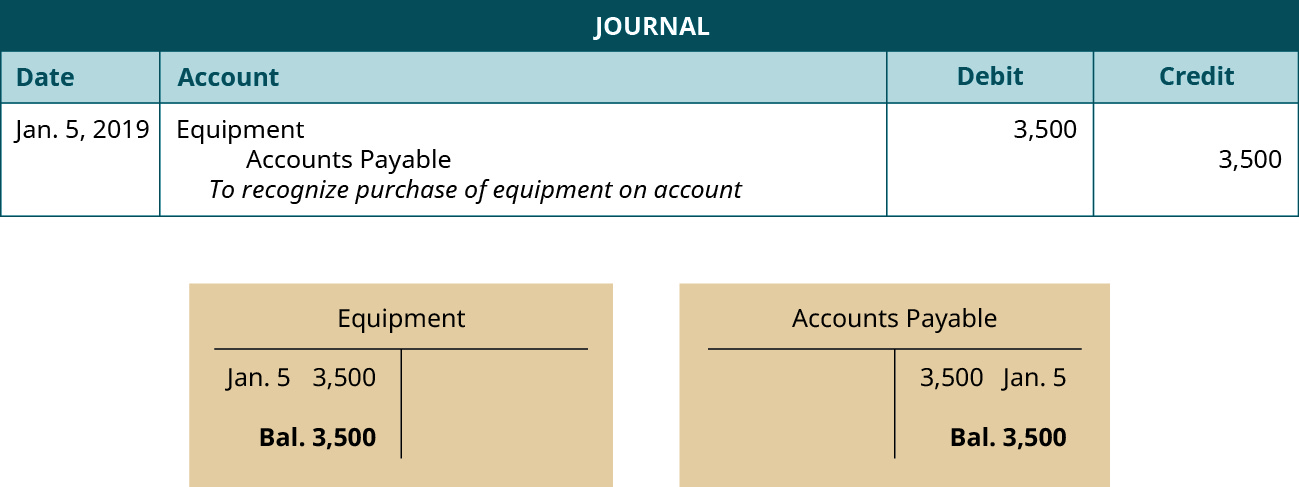

Transaction 2: On January 5, 2019, purchases equipment on account for $3,500, payment due within the month.

In the journal entry, Equipment has a debit of $3,500. This is posted to the Equipment T-account on the debit side. Accounts Payable has a credit balance of $3,500. This is posted to the Accounts Payable T-account on the credit side.

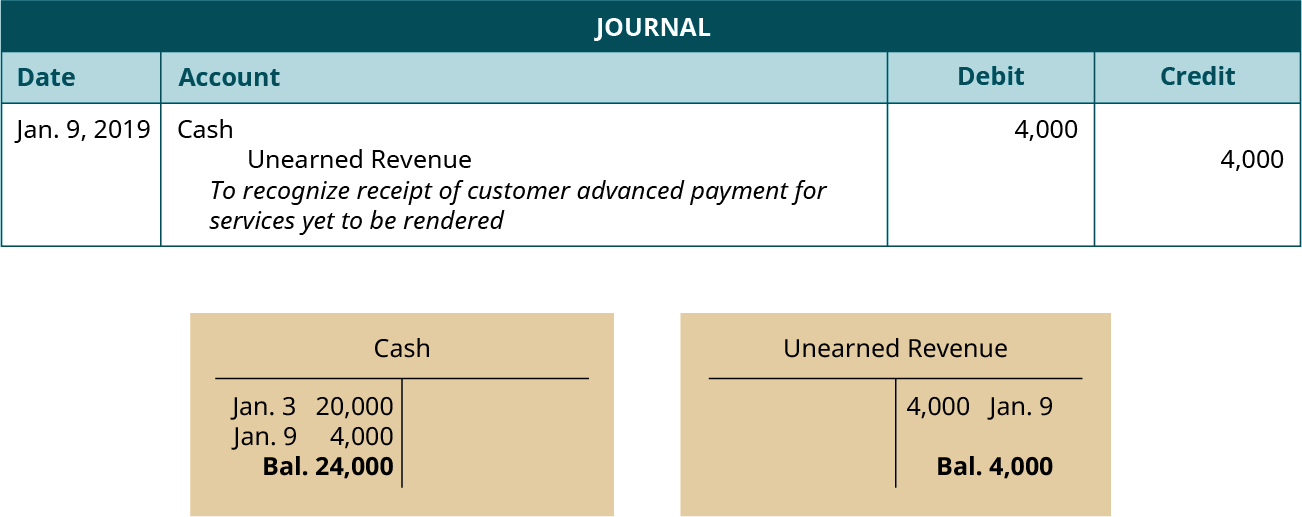

Transaction 3: On January 9, 2019, receives $4,000 cash in advance from a customer for services not yet rendered.

In the journal entry, Cash has a debit of $4,000. This is posted to the Cash T-account on the debit side. You will notice that the transaction from January 3 is listed already in this T-account. The next transaction figure of $4,000 is added directly below the $20,000 on the debit side. Unearned Revenue has a credit balance of $4,000. This is posted to the Unearned Revenue T-account on the credit side.

Transaction 4: On January 10, 2019, provides $5,500 in services to a customer who asks to be billed for the services.

In the journal entry, Accounts Receivable has a debit of $5,500. This is posted to the Accounts Receivable T-account on the debit side. Service Revenue has a credit balance of $5,500. This is posted to the Service Revenue T-account on the credit side.

Transaction 5: On January 12, 2019, pays a $300 utility bill with cash.

In the journal entry, Utility Expense has a debit balance of $300. This is posted to the Utility Expense T-account on the debit side. Cash has a credit of $300. This is posted to the Cash T-account on the credit side. You will notice that the transactions from January 3 and January 9 are listed already in this T-account. The next transaction figure of $300 is added on the credit side.

Transaction 6: On January 14, 2019, distributed $100 cash in dividends to stockholders.

In the journal entry, Dividends has a debit balance of $100. This is posted to the Dividends T-account on the debit side. Cash has a credit of $100. This is posted to the Cash T-account on the credit side. You will notice that the transactions from January 3, January 9, and January 12 are listed already in this T-account. The next transaction figure of $100 is added directly below the January 12 record on the credit side.

Transaction 7: On January 17, 2019, receives $2,800 cash from a customer for services rendered.

In the journal entry, Cash has a debit of $2,800. This is posted to the Cash T-account on the debit side. You will notice that the transactions from January 3, January 9, January 12, and January 14 are listed already in this T-account. The next transaction figure of $2,800 is added directly below the January 9 record on the debit side. Service Revenue has a credit balance of $2,800. This too has a balance already from January 10. The new entry is recorded under the Jan 10 record, posted to the Service Revenue T-account on the credit side.

Transaction 8: On January 18, 2019, paid in full, with cash, for the equipment purchase on January 5.

On this transaction, Cash has a credit of $3,500. This is posted to the Cash T-account on the credit side beneath the January 14 transaction. Accounts Payable has a debit of $3,500 (payment in full for the Jan. 5 purchase). You notice there is already a credit in Accounts Payable, and the new record is placed directly across from the January 5 record.

Transaction 9: On January 20, 2019, paid $3,600 cash in salaries expense to employees.

On this transaction, Cash has a credit of $3,600. This is posted to the Cash T-account on the credit side beneath the January 18 transaction. Salaries Expense has a debit of $3,600. This is placed on the debit side of the Salaries Expense T-account.

Transaction 10: On January 23, 2019, received cash payment in full from the customer on the January 10 transaction.

On this transaction, Cash has a debit of $5,500. This is posted to the Cash T-account on the debit side beneath the January 17 transaction. Accounts Receivable has a credit of $5,500 (from the Jan. 10 transaction). The record is placed on the credit side of the Accounts Receivable T-account across from the January 10 record.

Transaction 11: On January 27, 2019, provides $1,200 in services to a customer who asks to be billed for the services.

On this transaction, Accounts Receivable has a debit of $1,200. The record is placed on the debit side of the Accounts Receivable T-account underneath the January 10 record. Service Revenue has a credit of $1,200. The record is placed on the credit side of the Service Revenue T-account underneath the January 17 record.

Transaction 12: On January 30, 2019, purchases supplies on account for $500, payment due within three months.

On this transaction, Supplies has a debit of $500. This will go on the debit side of the Supplies T-account. Accounts Payable has a credit of $500. You notice there are already figures in Accounts Payable, and the new record is placed directly underneath the January 5 record.

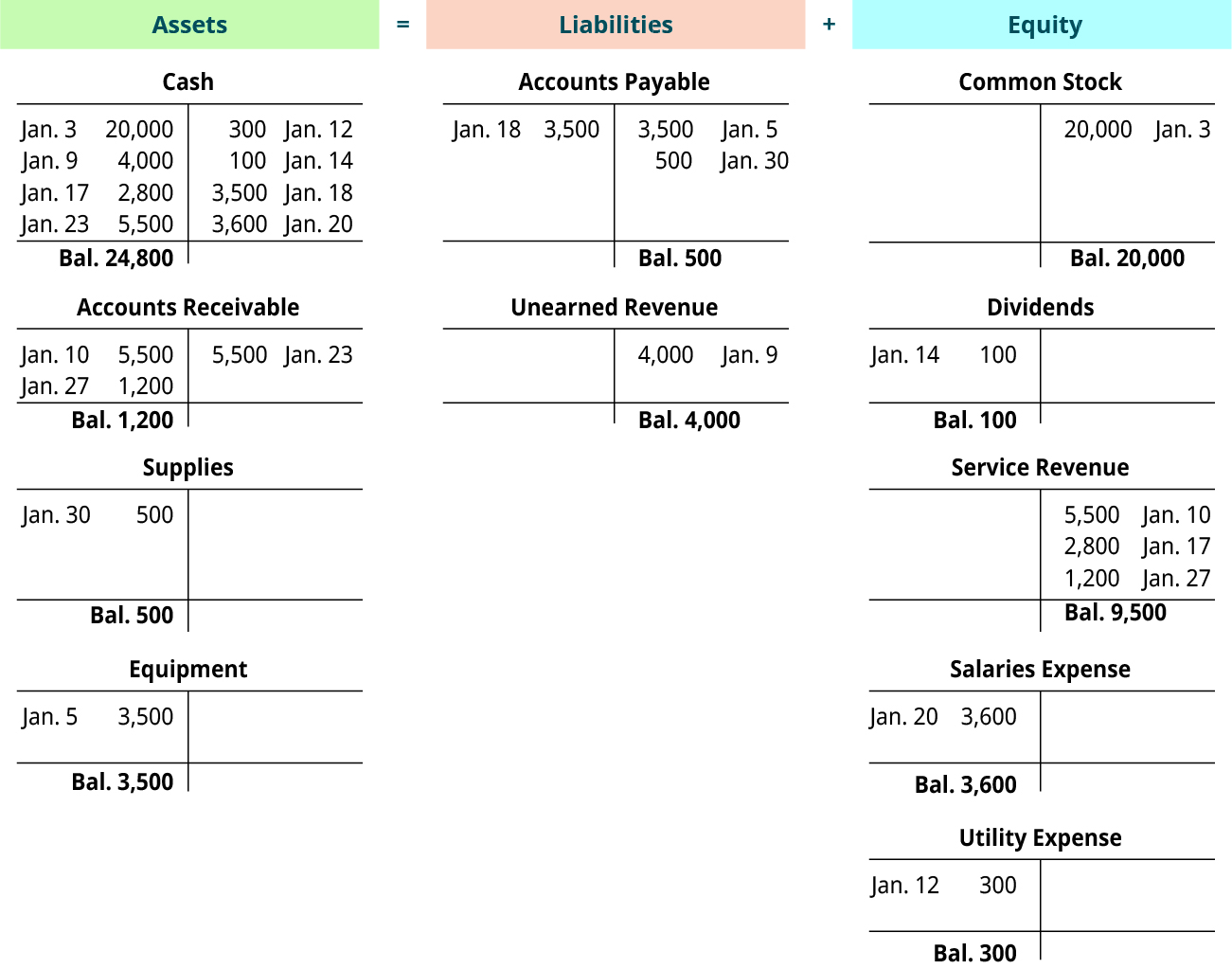

T-Accounts Summary

Once all journal entries have been posted to T-accounts, we can check to make sure the accounting equation remains balanced. A summary showing the T-accounts for Printing Plus is presented in (Figure).

The sum on the assets side of the accounting equation equals $30,000, found by adding together the final balances in each asset account (24,800 + 1,200 + 500 + 3,500). To find the total on the liabilities and equity side of the equation, we need to find the difference between debits and credits. Credits on the liabilities and equity side of the equation total $34,000 (500 + 4,000 + 20,000 + 9,500). Debits on the liabilities and equity side of the equation total $4,000 (100 + 3,600 + 300). The difference $34,000 – $4,000 = $30,000. Thus, the equation remains balanced with $30,000 on the asset side and $30,000 on the liabilities and equity side. Now that we have the T-account information, and have confirmed the accounting equation remains balanced, we can create the unadjusted trial balance.

YOUR TURN

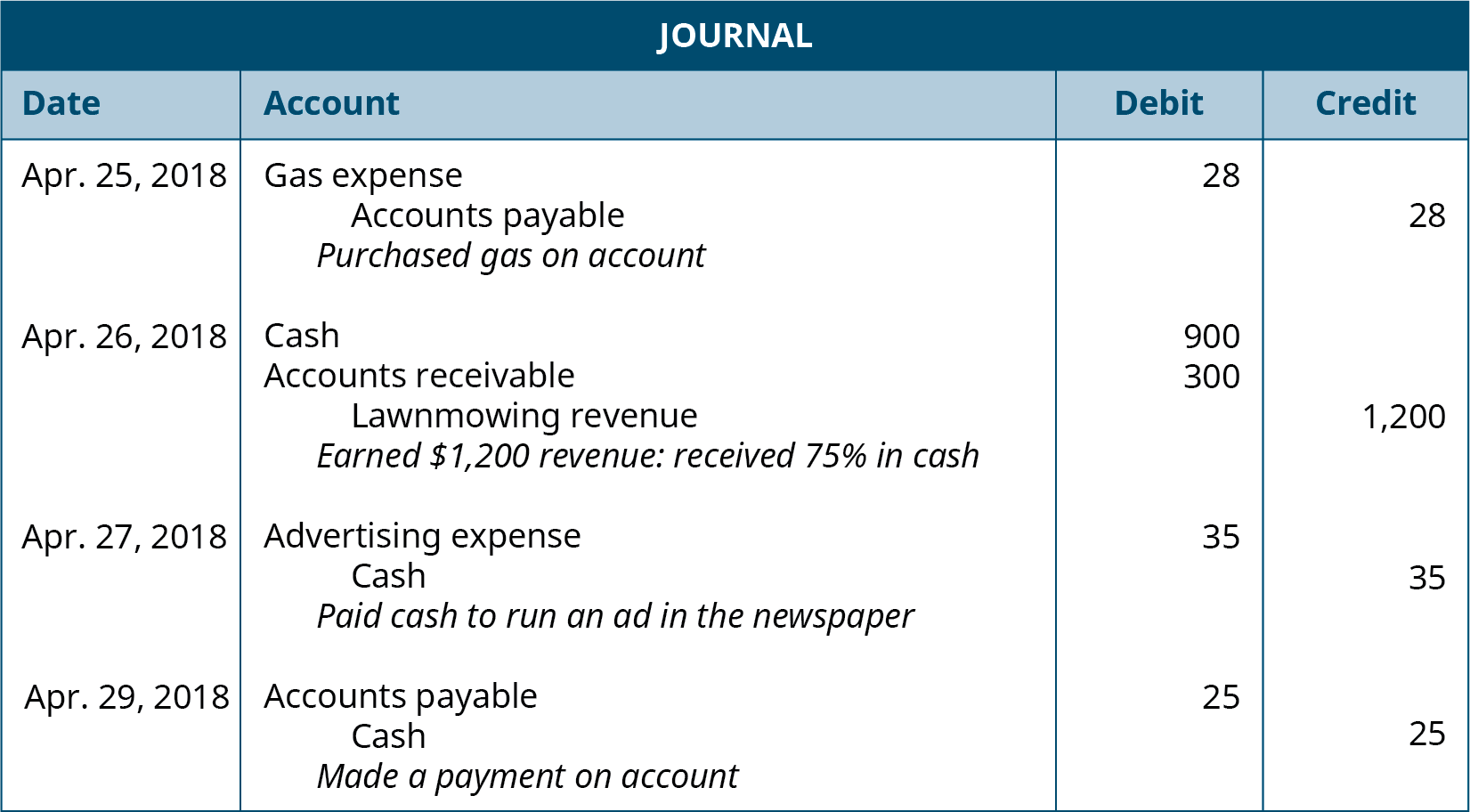

You have the following transactions the last few days of April.

| Apr. 25 | You stop by your uncle’s gas station to refill both gas cans for your company, Watson’s Landscaping. Your uncle adds the total of $28 to your account. |

| Apr. 26 | You record another week’s revenue for the lawns mowed over the past week. You earned $1,200. You received cash equal to 75% of your revenue. |

| Apr. 27 | You pay your local newspaper $35 to run an advertisement in this week’s paper. |

| Apr. 29 | You make a $25 payment on account. |

- Prepare the necessary journal entries for these four transactions.

- Explain why you debited and credited the accounts you did.

- What will be the new balance in each account used in these entries?

Solution

April 25

- You have incurred more gas expense. This means you have an increase in the total amount of gas expense for April. Expenses go up with debit entries. Therefore, you will debit gas expense.

- You purchased the gas on account. This will increase your liabilities. Liabilities increase with credit entries. Credit accounts payable to increase the total in the account.

April 26

- You have received more cash from customers, so you want the total cash to increase. Cash is an asset, and assets increase with debit entries, so debit cash.

- You also have more money owed to you by your customers. You have performed the services, your customers owe you the money, and you will receive the money in the future. Debit accounts receivable as asset accounts increase with debits.

- You have mowed lawns and earned more revenue. You want the total of your revenue account to increase to reflect this additional revenue. Revenue accounts increase with credit entries, so credit lawn-mowing revenue.

April 27

- Advertising is an expense of doing business. You have incurred more expenses, so you want to increase an expense account. Expense accounts increase with debit entries. Debit advertising expense.

- You paid cash for the advertising. You have less cash, so credit the cash account. Cash is an asset, and asset account totals decrease with credits.

April 29

- You paid “on account.” Remember that “on account” means a service was performed or an item was received without being paid for. The customer asked to be billed. You were the customer in this case. You made a purchase of gas on account earlier in the month, and at that time you increased accounts payable to show you had a liability to pay this amount sometime in the future. You are now paying down some of the money you owe on that account. Since you paid this money, you now have less of a liability so you want to see the liability account, accounts payable, decrease by the amount paid. Liability accounts decrease with debit entries.

- You paid, which means you gave cash (or wrote a check or electronically transferred) so you have less cash. To decrease the total cash, credit the account because asset accounts are reduced by recording credit entries.

YOUR TURN

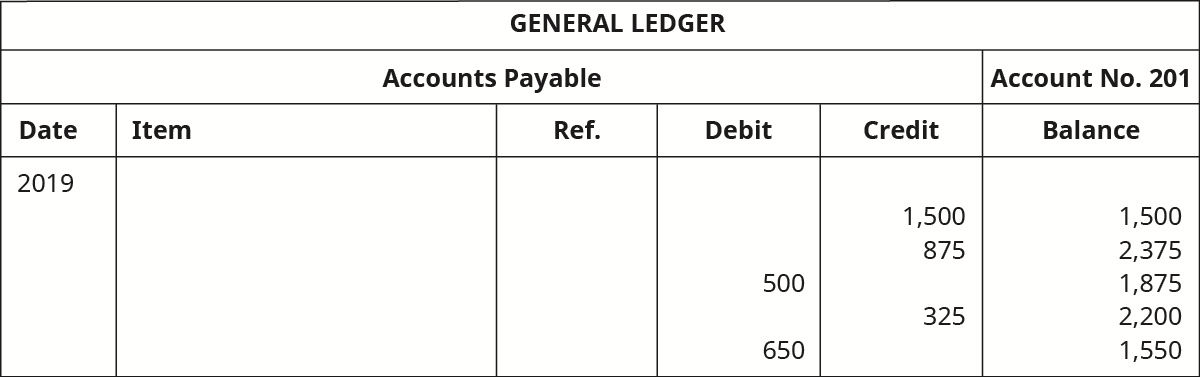

Calculate the balances in each of the following accounts. Do they all have the normal balance they should have? If not, which one? How do you know this?

Solution

THINK IT THROUGH

Gift cards have become an important topic for managers of any company. Understanding who buys gift cards, why, and when can be important in business planning. Also, knowing when and how to determine that a gift card will not likely be redeemed will affect both the company’s balance sheet (in the liabilities section) and the income statement (in the revenues section).

According to a 2017 holiday shopping report from the National Retail Federation, gift cards are the most-requested presents for the eleventh year in a row, with 61% of people surveyed saying they are at the top of their wish lists.1CEB TowerGroup projects that total gift card volume will reach $160 billion by 2018.2

How are all of these gift card sales affecting one of America’s favorite specialty coffee companies, Starbucks?

In 2014 one in seven adults received a Starbucks gift card. On Christmas Eve alone $2.5 million gift cards were sold. This is a rate of 1,700 cards per minute.3

The following discussion about gift cards is taken from Starbucks’s 2016 annual report:

When an amount is loaded onto a stored value card we recognize a corresponding liability for the full amount loaded onto the card, which is recorded within stored value card liability on our consolidated balance sheets. When a stored value card is redeemed at a company-operated store or online, we recognize revenue by reducing the stored value card liability. When a stored value card is redeemed at a licensed store location, we reduce the corresponding stored value card liability and cash, which is reimbursed to the licensee. There are no expiration dates on our stored value cards, and in most markets, we do not charge service fees that cause a decrement to customer balances. While we will continue to honor all stored value cards presented for payment, management may determine the likelihood of redemption, based on historical experience, is deemed to be remote for certain cards due to long periods of inactivity. In these circumstances, unredeemed card balances may be recognized as breakage income. In fiscal 2016, 2015, and 2014, we recognized breakage income of $60.5 million, $39.3 million, and $38.3 million, respectively.4

As of October 1, 2017, Starbucks had a total of $1,288,500,000 in stored value card liability.

KEY TAKEAWAYS

Key Concepts and Summary

- Journals are the first place where information is entered into the accounting system, which is why they are often referred to as books of original entry.

- Journalizing transactions transfers information from accounting equation analysis to a record of each transaction.

- There are several formatting rules for journalizing transactions that include where to put debits and credits, which account titles come first, the need for a date and inclusion of a brief description.

- Step 3 in the accounting cycle posts journal information to the general ledger (T-accounts). Final balances in each account must be calculated before transfer to the trial balance occurs.

Glossary

- book of original entry

- journal is often referred to as this because it is the place the information originally enters into the system

- compound entry

- more than one account is listed under the left/debit column and/or right/credit column of a journal entry

- journal

- record of all transactions

- journalizing

- entering information into a journal; second step in the accounting cycle

- simple entry

- only one left/debit account and one right/credit account are listed under the left/debit and right/credit columns of a journal entry

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

journal is often referred to as this because it is the place the information originally enters into the system

record of all transactions, in date sequence

entering information into a journal

only one debit account and one credit account are listed in the debit and credit columns of a journal entry

more than one account is listed in the debit and/or credit column of a journal entry