LO 12.5 Record Transactions Incurred in Preparing Payroll

Have you ever looked at your paycheck and wondered where all the money went? Well, it did not disappear; the money was used to contribute required and optional financial payments to various entities.

Payroll can be one of the largest expenses and potential liabilities for a business. Payroll liabilities include employee salaries and wages, and deductions for taxes, benefits, and employer contributions. In this section, we explain these elements of payroll and the required journal entries.

Employee Compensation and Deductions

As an employee working in a business, you receive compensation for your work. This pay could be a monthly salary or hourly wages paid periodically. The amount earned by the employee before any reductions in pay occur is considered gross income (pay). These reductions include involuntary and voluntary deductions. The remaining balance after deductions is considered net income (pay), or “take-home-pay.” The take-home-pay is what employees receive and deposit in their bank accounts.

Involuntary Deductions

Involuntary deductions are withholdings that neither the employer nor the employee have control over and are required by law.

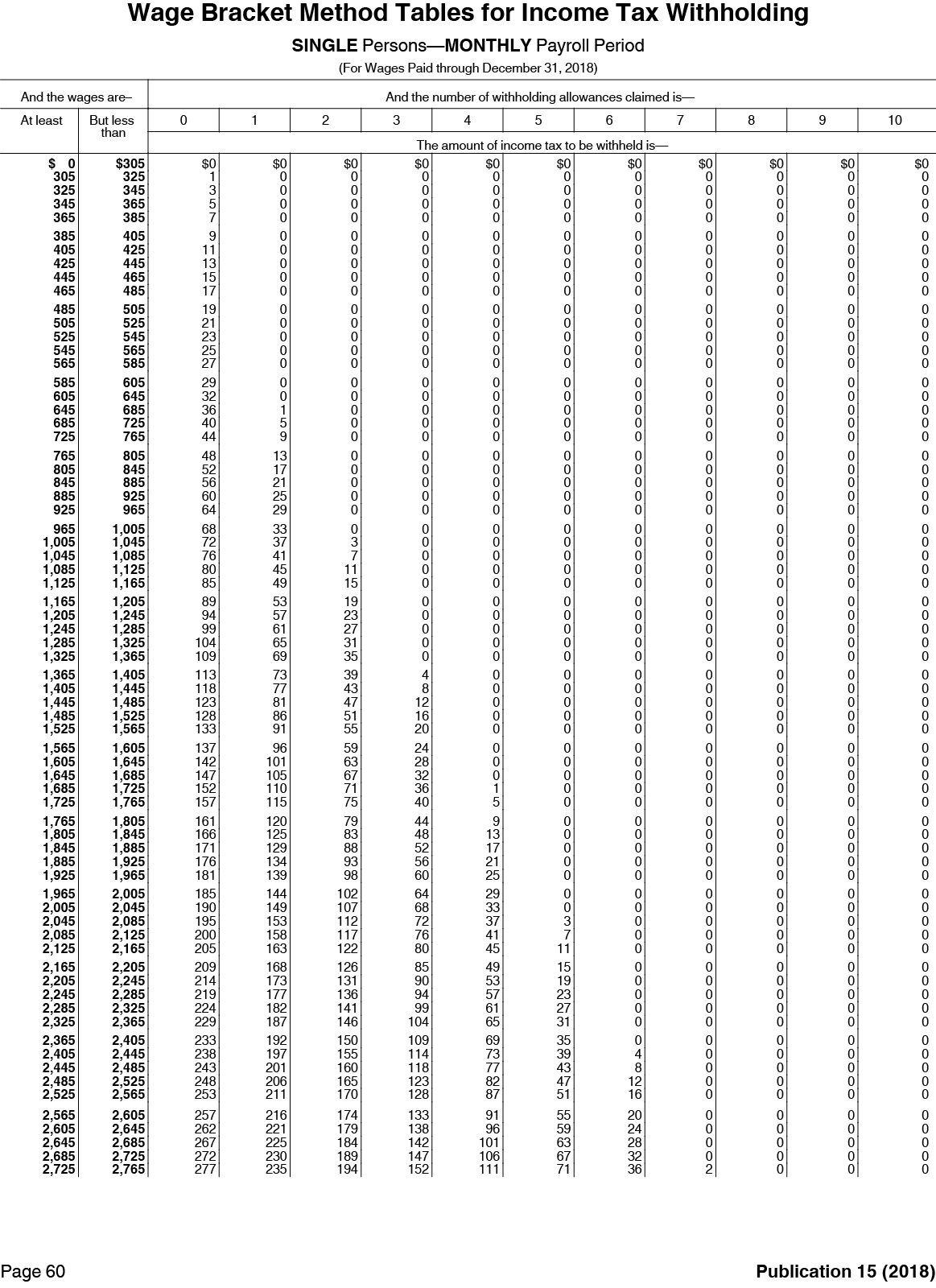

Federal, state, and local income taxes are considered involuntary deductions. Income taxes imposed are different for every employee and are based on their W-4 Form, the Employee’s Withholding Allowance Certificate. An employee will fill in his or her marital status, number of allowances requested, and any additional reduction amounts. The employer will use this information to determine the federal income tax withholding amount from each paycheck. State income tax withholding may also use W-4 information or the state’s withholdings certificate. The federal income tax withholding and state income tax withholding amounts can be established with tax tables published annually by the Internal Revenue Service (IRS) (see (Figure)) and state government offices, respectively. Some states though do not require an income tax withholding, since they do not impose a state income tax. Federal and state income liabilities are held in payable accounts until disbursement to the governmental bodies that administer the tax compliance process for their particular governmental entity.

While not a common occurrence, local income tax withholding is applied to those living or working within a jurisdiction to cover schooling, social services, park maintenance, and law enforcement. If local income taxes are withheld, these remain current liabilities until paid.

Other involuntary deductions involve Federal Insurance Contribution Act (FICA) taxes for Social Security and Medicare. FICA mandates employers to withhold taxes from employee wages “to provide benefits for retirees, the disabled, and children.” The Social Security tax rate is 6.2% of employee gross wages. As of 2017, there is a maximum taxable earnings amount of $127,200. Meaning, only the first $127,200 of each employee’s gross wages has the Social Security tax applied. In 2018, the maximum taxable earnings amount increased to $128,400. The Medicare tax rate is 1.45% of employee gross income. There is no taxable earnings cap for Medicare tax. The two taxes combined equal 7.65% (6.2% + 1.45%). Both the employer and the employee pay the two taxes on behalf of the employee.

More recent health-care legislation, the Affordable Care Act (ACA), requires an additional medicare tax withholding from employee pay of 0.9% for individuals who exceed an income threshold based on their filing status (married, single, or head of household, for example). This Additional Medicare Tax withholding is only applied to employee payroll.

Last, involuntary deductions may also include child support payments, IRS federal tax levies, court-ordered wage garnishments, and bankruptcy judgments. All involuntary deductions are an employer’s liability until they are paid.

Voluntary Deductions

In addition to involuntary deductions, employers may withhold certain voluntary deductions from employee wages. Voluntary deductions are not required to be removed from employee pay unless the employee designates reduction of these amounts. Voluntary deductions may include, but are not limited to, health-care coverage, life insurance, retirement contributions, charitable contributions, pension funds, and union dues. Employees can cover the full cost of these benefits or they may cost-share with the employer.

Health-care coverage is a requirement for many businesses to provide as a result of the ACA. Employers may provide partial benefit coverage and request the employee to pay the remainder. For example, the employer would cover 30% of health-care cost, and 70% would be the employee’s responsibility.

Retirement contributions may include those made to an employer-sponsored plan, such as a defined contribution plan, which “shelters” the income in a 401(k) or a 403(b). In simple terms, a defined contribution plan allows an employee to voluntarily contribute a specified amount or percentage of his or her pretax wages to a special account in order to defer the tax on those earnings. Usually, a portion of the employee’s contribution is matched by his or her employer; employers often use this as an incentive to attract and keep highly skilled and valuable employees. Only when the employee eventually withdraws funds from the plan will he or she be required to pay the tax on those earnings. Because the amount contributed to the plan is not immediately taxed by the IRS, it enables the employee to accumulate funds for his or her retirement. This deferred income may be excluded from the employee’s current federal taxable income but not FICA taxes. All voluntary deductions are considered employer liabilities until remitted. For more in-depth information on retirement planning, and using a 401(k) or a 403(b), refer to Appendix C.

As with involuntary deductions, voluntary deductions are held as a current liability until paid. When payroll is disbursed, journal entries are required.

CONCEPTS IN PRACTICE

Should you save for retirement now or wait? As a student, you may be inclined to put off saving for retirement for many reasons. You may not be in a financial position to do so, you believe Social Security will be enough to cover your needs, or you may not have even thought about it up to this point.

According to a 2012 survey from the Bureau of Labor Statistics, of those who had access to a defined contribution plan, only 68% of employees contributed to their retirement plan. Many employees wait until their mid-thirties or forties to begin saving, and this can delay retirement, or may leave the retiree unable to cover his or her annual expenses. Some pitfalls contributing to this lack of saving are short-term negative spending practices such as high-interest loan debt, credit card purchases, and discretionary spending (optional expenses such as eating out or entertainment). To avoid these hazards, you should

- Analyze your spending habits and make changes where possible.

- Develop a financial plan with the help of a finance specialist.

- Join a defined contribution plan and stick with the plan (do not withdraw funds early).

- Try to contribute at least as much as your employer is willing to match.

- Consider other short-term savings options like bonds, or high-interest bank accounts.

- Have a specific savings goal for your retirement account. For example, many financial advisors recommend saving at least 15% of your monthly income for retirement. However, they usually include both the employee’s contribution and the employer’s. For example, assume that the company matches each dollar invested by the employee with a $0.50 contribution from the employer, up to 8% for the employee. In this case, if the employee contributes 8% and the company provides 4%, that takes the employee to 80% of the recommended goal (12% of the recommended 15%).

Remember, the longer you wait to begin investing, the more you will have to save later on to have enough for retirement.

Journal Entries to Report Employee Compensation and Deductions

We continue to use Sierra Sports as our example company to prepare journal entries.

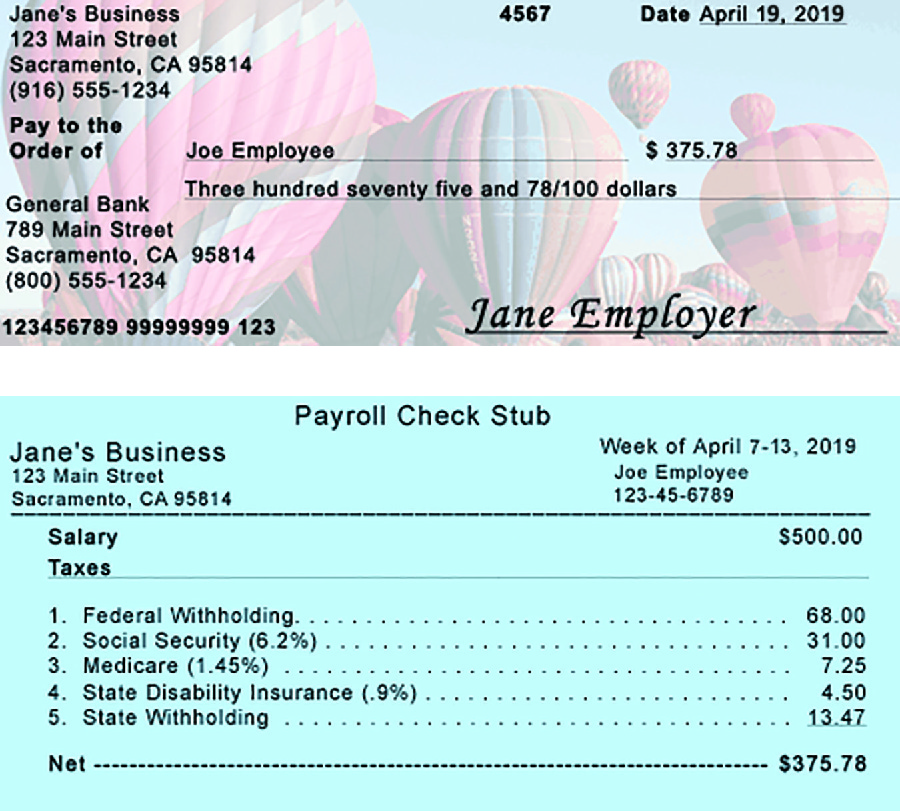

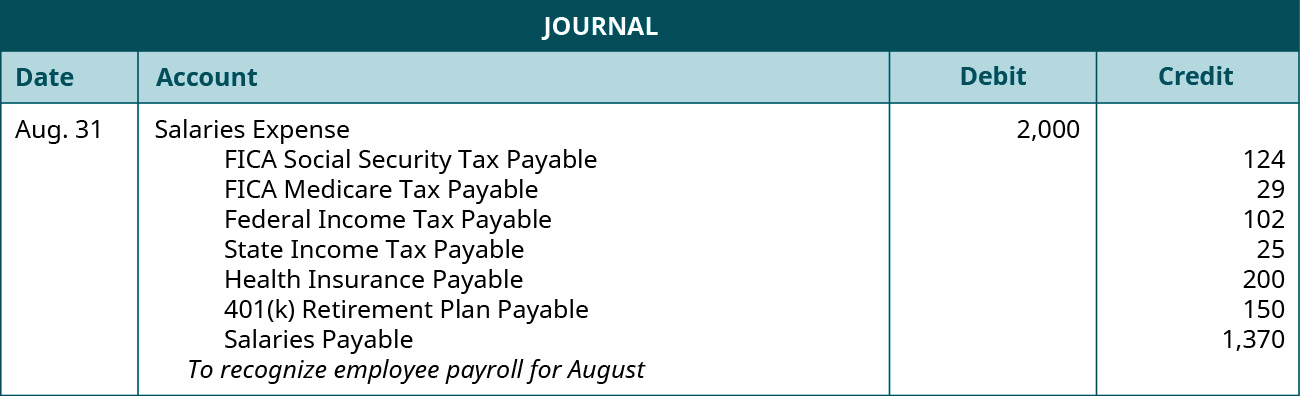

Sierra Sports employs several people, but our focus is on one specific employee for this example. Billie Sanders works for Sierra Sports and earns a salary each month of $2,000. She claims two withholdings allowances (see (Figure)). This amount is paid on the first of the following month. Withholdings for federal and state income taxes are assessed in the amount of $102 and $25, respectively. FICA Social Security is taxed at the 6.2% rate, and FICA Medicare is taxed at the 1.45% rate. Billie has voluntary deductions for health insurance and a 401(k) retirement contribution. She is responsible for 40% of her $500 health-care insurance premium; Sierra Sports pays the remaining 60% (as explained in employer payroll). The 401(k) contributions total $150. The first entry records the salaries liability during the month of August.

Salaries Expense is an equity account used to recognize the accumulated (accrued) expense to the business during August (increase on the debit side). Salaries Expense represents the employee’s gross income (pay) before any deductions. Each deduction liability is listed in its own account; this will help for ease of payment to the different entities. Note that Health Insurance Payable is in the amount of $200, which is 40% of the employee’s responsibility for the premium ($500 × 0.40 = $200). Salaries Payable represents net income (pay) or the “take-home pay” for Billie. Salaries Payable is $1,370, which is found by taking gross income and subtracting the sum of the liabilities ($2,000 – $630 = $1,370). Since salaries are not paid until the first of the following month, this liability will remain during the month of August. All liabilities (payables) increase due to the company’s outstanding debt (increase on the credit side).

The second entry records cash payment of accumulated salaries on September 1.

Payment to Billie Sanders occurs on September 1. The payment is for salaries accumulated from the month of August. The payment decreases Salaries Payable (debit side) since the liability was paid and decreases Cash (credit side), because cash is the asset used for payment.

LINK TO LEARNING

Employer Compensation and Deductions

At this point you might be asking yourself, “why am I having to pay all of this money and my employer isn’t?” Your employer also has a fiscal and legal responsibility to contribute and match funds to certain payroll liability accounts.

Involuntary Payroll Taxes

Employers must match employee contributions to FICA Social Security (6.2% rate) on the first $127,200 of employee wages for 2017, and FICA Medicare (1.45% rate) on all employee earnings. Withholdings for these taxes are forwarded to the same place as employee contributions; thus, the same accounts are used when recording journal entries.

Employers are required by law to pay into an unemployment insurance system that covers employees in case of job disruption due to factors outside of their control (job elimination from company bankruptcy, for example). The tax recognizing this required payment is the Federal Unemployment Tax Act (FUTA)[/pb_glossary]. FUTA is at a rate of 6%. This tax applies to the initial $7,000 of each employee’s wages earned during the year. This rate may be reduced by as much as 5.4% as a credit for paying into state unemployment on time, producing a lower rate of 0.6%. The [pb_glossary id="1718"]State Unemployment Tax Act (SUTA) is similar to the FUTA process, but tax rates and minimum taxable earnings vary by state.

Voluntary Benefits Provided by the Employer

Employers offer competitive advantages (benefits) to employees in an effort to improve job satisfaction and increase employee morale. There is no statute mandating the employer cover these benefits financially. Some possible benefits are health-care coverage, life insurance, contributions to retirement plans, paid sick leave, paid maternity/paternity leave, and vacation compensation.

Paid sick leave, paid maternity/paternity leave, and vacation compensation help employees take time off when needed or required by providing a stipend while the employee is away. This compensation is often comparable to the wages or salary for the covered period. Some companies have policies that require vacation and paid sick leave to be used within the year or the employee risks losing that benefit in the current period. These benefits are considered estimated liabilities since it is not clear when, if, or how much the employee will use them. Let’s now see the process for journalizing employer compensation and deductions.

Journal Entries to Report Employer Compensation and Deductions

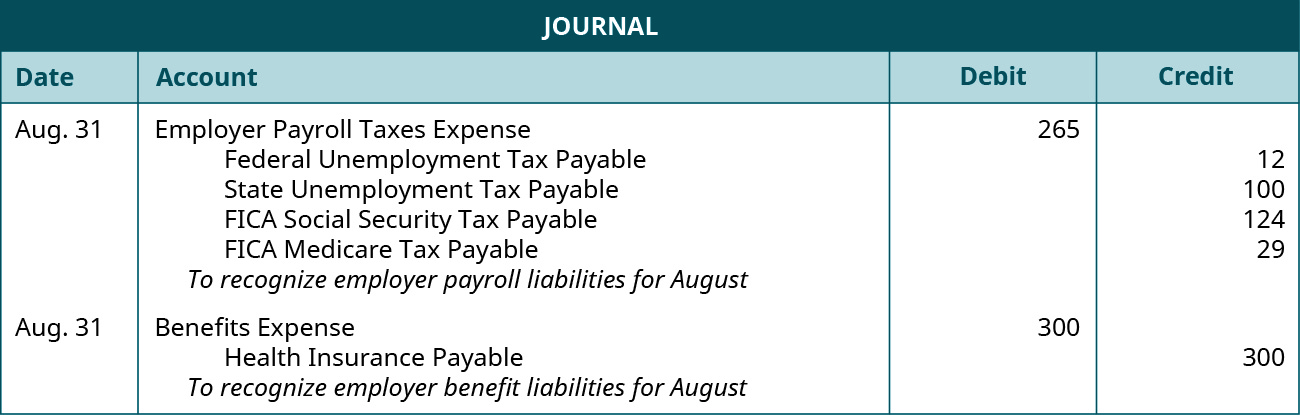

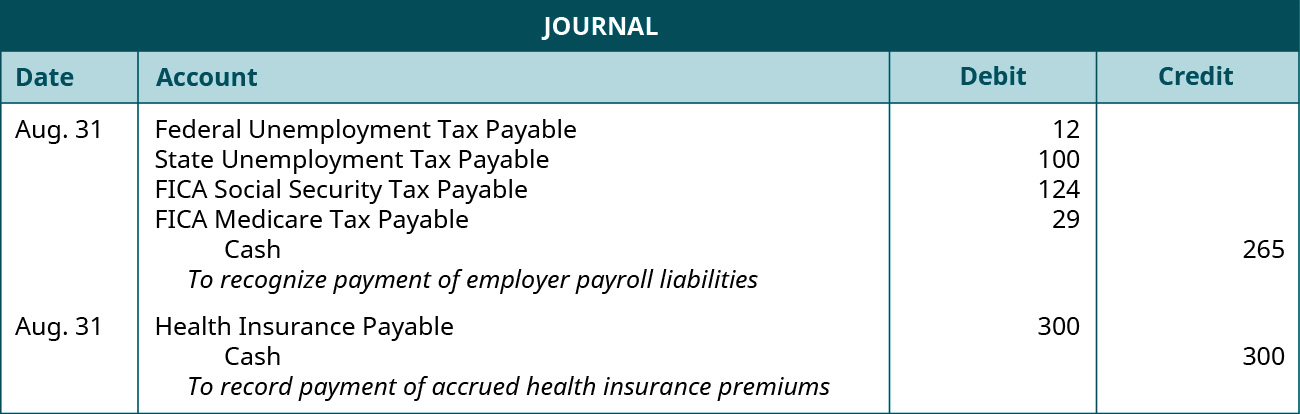

In addition to the employee payroll entries for Billie Sanders, Sierra Sports has an obligation to contribute taxes to federal unemployment, state unemployment, FICA Social Security, and FICA Medicare. They are also responsible for 60% of Billie’s health insurance premium payment. Assume Sierra Sports receives the FUTA credit and is only taxed at the rate of 0.6%, and SUTA taxes are $100. August is Billie Sanders’ first month of pay for the year. The following entry represents the employer payroll liabilities and expense for the month of August. The second entry records the health insurance premium liability.

Employer Payroll Tax Expense is the equity account used to recognize payroll expenses during the period (increases on the debit side). The amount of $265 is the sum of all liabilities from that period. Notice that FICA Social Security Tax Payable and FICA Medicare Tax Payable were used in the employee payroll entry earlier and again here in the employer payroll. You only need to use one account if the payments are for the same recipient and purpose. The amounts of Social Security ($124) and Medicare ($29) taxes withheld match the amounts withheld from employee payroll. Federal Unemployment Tax Payable and State Unemployment Tax Payable recognize the liabilities for federal and state unemployment deductions, respectively. The federal unemployment tax ($12) is computed by multiplying the federal unemployment tax rate of 0.6% by $2,000. These liability accounts increase (credit side) when the amount owed increases.

The second entry recognizes the liability created from providing the voluntary benefit, health insurance coverage. Voluntary and involuntary employer payroll items should be separated. It is also important to separate estimated liabilities from certain voluntary benefits due to their uncertainty. Benefits Expense recognizes the health insurance expense from August. Health Insurance Payable recognizes the outstanding liability for health-care coverage covered by the employer ($500 × 60% = $300).

The following entries represent payment of the employer payroll and benefit liabilities in the following period.

When payment occurs, all payable accounts decrease (debit) because the company paid all taxes and benefits owed for those liabilities. Cash is the accepted form of payment at the payee organizations (Social Security Administration, and health plan administrator, for example).

LINK TO LEARNING

KEY TAKEAWAYS

Key Concepts and Summary

- An employee’s net income (pay) results from gross income (pay) minus any involuntary and voluntary deductions. Employee payroll deductions may include federal, state, and local income taxes; FICA Social Security; FICA Medicare; and voluntary deductions such as health insurance, retirement plan contributions, and union dues.

- When recording employee payroll liabilities, Salaries Expense, Salaries Payable, and all payables for income taxes, Social Security, Medicare, and voluntary deductions, are reported. When the company pays the accrued salaries, Salaries Payable is reduced, as is cash.

- Employers are required to match employee withholdings for Social Security and Medicare. They must also remit FUTA and SUTA taxes, as well as voluntary deductions and benefits provided to employees.

- When recording employer payroll liabilities, Employer Payroll Taxes Expense and all payables associated with FUTA, SUTA, Social Security, Medicare, and voluntary deductions are required. When the company pays all employer liabilities, each payable and cash account decreases.

Glossary

- Additional Medicare Tax

- requirement for employers to withhold 0.9% from employee pay for individuals who exceed an income threshold based on their filing status

- defined contribution plans

- money set aside and held in account for employee’s retirement with possible contribution from employers

- federal income tax withholding

- amount withheld from employee pay based on employee responses given on Form W-4

- Federal Unemployment Tax Act (FUTA)

- response to a law requiring employers to pay into a federal unemployment insurance system that covers employees in case of job disruption due to factors outside of their control

- Federal Insurance Contribution Act (FICA) tax

- involuntary tax mandated by FICA that requires employers to withhold taxes from employee wages “to provide benefits for retirees, the disabled, and children”

- gross income (pay)

- amount earned by the employee before any reductions in pay occur due to involuntary and voluntary deductions

- involuntary deduction

- withholding that neither the employer nor the employee have control over, and is required by law

- local income tax withholding

- applied to those living or working within a jurisdiction to cover schooling, social services, park maintenance, and law enforcement

- Medicare tax rate

- currently 1.45% of employee gross income with no taxable earnings cap

- net income (pay)

- (also, take home pay) remaining employee earnings balance after involuntary and voluntary deductions from employee pay

- Social Security tax rate

- currently 6.2% of employees gross wage earnings with a maximum taxable earnings amount of $127,200 in 2017 and $128,400 in 2018

- state income tax withholding

- reduction to employee pay determined by responses given on Form W-4, or on a state withholdings certificate

- State Unemployment Tax Act (SUTA)

- response to a law requiring employers to pay into a state unemployment insurance system that covers employees in case of job disruption due to factors outside of their control

- vacation compensation

- stipend provided by the employer to employees when they take time off for vacation

- voluntary deduction

- not required to be removed from employee pay unless the employee designates reduction of this amount

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

amount earned by the employee before any reductions in pay occur due to involuntary and voluntary deductions

(also, take home pay) remaining employee earnings balance after involuntary and voluntary deductions from employee pay

withholding that neither the employer nor the employee have control over, and is required by law

amount withheld from employee pay based on employee responses given on Form W-4

reduction to employee pay determined by responses given on Form W-4, or on a state withholdings certificate

applied to those living or working within a jurisdiction to cover schooling, social services, park maintenance, and law enforcement

involuntary tax mandated by FICA that requires employers to withhold taxes from employee wages “to provide benefits for retirees, the disabled, and children”

currently 6.2% of employees gross wage earnings with a maximum taxable earnings amount of $127,200 in 2017 and $128,400 in 2018

currently 1.45% of employee gross income with no taxable earnings cap

requirement for employers to withhold 0.9% from employee pay for individuals who exceed an income threshold based on their filing status

not required to be removed from employee pay unless the employee designates reduction of this amount

money set aside and held in account for employee’s retirement with possible contribution from employers

response to a law requiring employers to pay into a federal unemployment insurance system that covers employees in case of job disruption due to factors outside of their control

stipend provided by the employer to employees when they take time off for vacation