LO 4.3 Record and Post the Common Types of Adjusting Entries

Before beginning adjusting entry examples for Printing Plus, let’s consider some rules governing deferral and accrual adjusting entries:

- Every adjusting entry will have at least one income statement account and one balance sheet account.

- Cash will never be in an adjusting entry.

- The adjusting entry records the change in amount that occurred during the period.

What are “income statement” and “balance sheet” accounts? Income statement accounts include revenues and expenses. Balance sheet accounts are assets, liabilities, and contributed accounts, since they appear on a balance sheet. The second rule tells us that cash can never be in an adjusting entry for deferrals or accruals. This is true because paying or receiving cash triggers a journal entry. This means that every transaction with cash will be recorded at the time of the exchange. (Sometimes, Cash is used in other types of adjusting entries, but only as a result of a bank reconciliation.)

With an adjusting entry, the amount of change occurring during the period is recorded. For example, if the supplies account had a $300 balance at the beginning of the month and $100 is still available in the supplies account at the end of the month, the company would record an adjusting entry for the $200 used during the month (300 – 100). Similarly for unearned revenues, the company would record how much of the revenue was earned during the period.

CONCEPTS IN PRACTICE

Recording adjusting entries seems so cut and dry. It looks like you just follow the rules and all of the numbers come out 100 percent correct on all financial statements. But in reality this is not always the case. Just the fact that you have to make estimates in some cases, such as depreciation estimating residual value and useful life, tells you that numbers will not be 100 percent correct unless the accountant has ESP. Some companies engage in something called earnings management, where they follow the rules of accounting mostly but they stretch the truth a little to make it look like they are more profitable. Some companies do this by recording revenue before they should. Others leave assets on the books instead of expensing them when they should to decrease total expenses and increase profit.

Take Mexico-based home-building company Desarrolladora Homex S.A.B. de C.V. This company reported revenue earned on more than 100,000 homes they had not even build yet. The SEC’s complaint states that Homex reported revenues from a project site where every planned home was said to have been “built and sold by Dec. 31, 2011. Satellite images of the project site on March 12, 2012, show it was still largely undeveloped and the vast majority of supposedly sold homes remained unbuilt.”1

Is managing your earnings illegal? In some situations it is just an unethical stretch of the truth easy enough to do because of the estimates made in adjusting entries. You can simply change your estimate and insist the new estimate is really better when maybe it is your way to improve the bottom line, for example, changing your annual depreciation expense calculated on expensive plant assets from assuming a ten-year useful life, a reasonable estimated expectation, to a twenty-year useful life, not so reasonable but you insist your company will be able to use these assets twenty years while knowing that is a slim possibility. Doubling the useful life will cause 50% of the depreciation expense you would have had. This will make a positive impact on net income. This method of earnings management would probably not be considered illegal but is definitely a breach of ethics. In other situations, companies manage their earnings in a way that the SEC believes is actual fraud and charges the company with the illegal activity.

Let’s now consider new transaction information for Printing Plus.

Recording Common Types of Adjusting Entries

First, recall the transactions for Printing Plus discussed in Analyzing and Recording Transactions.

| Jan. 3, 2019 | issues $20,000 shares of common stock for cash |

| Jan. 5, 2019 | purchases equipment on account for $3,500, payment due within the month |

| Jan. 9, 2019 | receives $4,000 cash in advance from a customer for services not yet rendered |

| Jan. 10, 2019 | provides $5,500 in services to a customer who asks to be billed for the services |

| Jan. 12, 2019 | pays a $300 utility bill with cash |

| Jan. 14, 2019 | distributed $100 cash in dividends to stockholders |

| Jan. 17, 2019 | receives $2,800 cash from a customer for services rendered |

| Jan. 18, 2019 | paid in full, with cash, for the equipment purchase on January 5 |

| Jan. 20, 2019 | paid $3,600 cash in salaries expense to employees |

| Jan. 23, 2019 | received cash payment in full from the customer on the January 10 transaction |

| Jan. 27, 2019 | provides $1,200 in services to a customer who asks to be billed for the services |

| Jan. 30, 2019 | purchases supplies on account for $500, payment due within three months |

On January 31, 2019, Printing Plus makes adjusting entries for the following transactions.

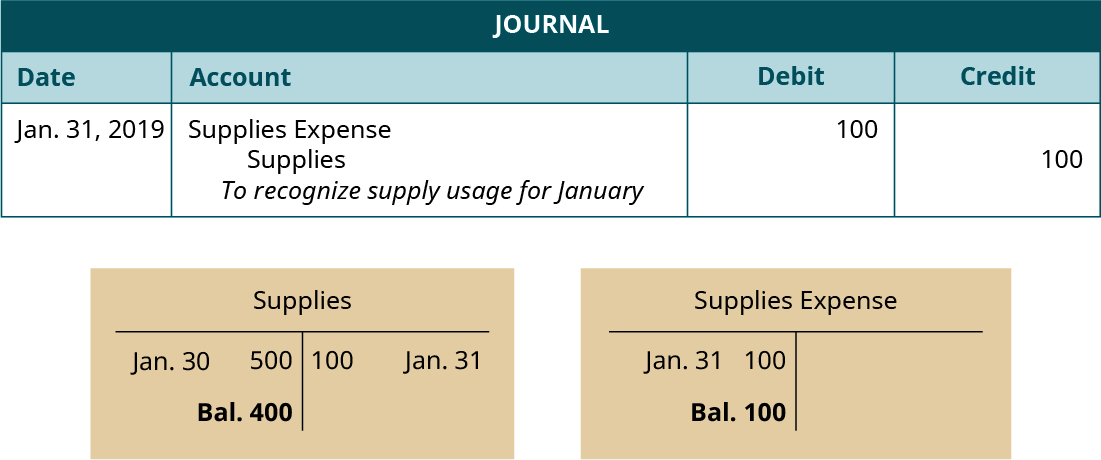

- On January 31, Printing Plus took an inventory of its supplies and discovered that $100 of supplies had been used during the month.

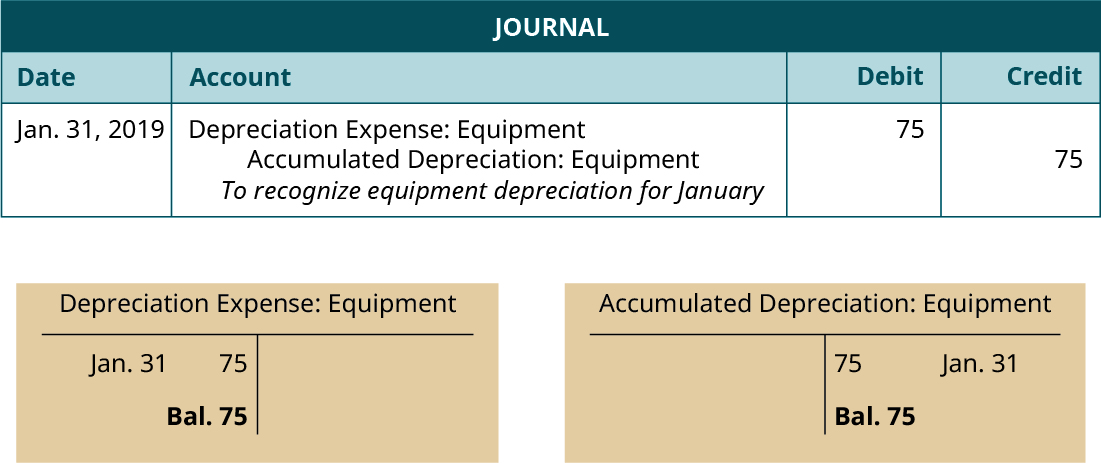

- The equipment purchased on January 5 depreciated $75 during the month of January.

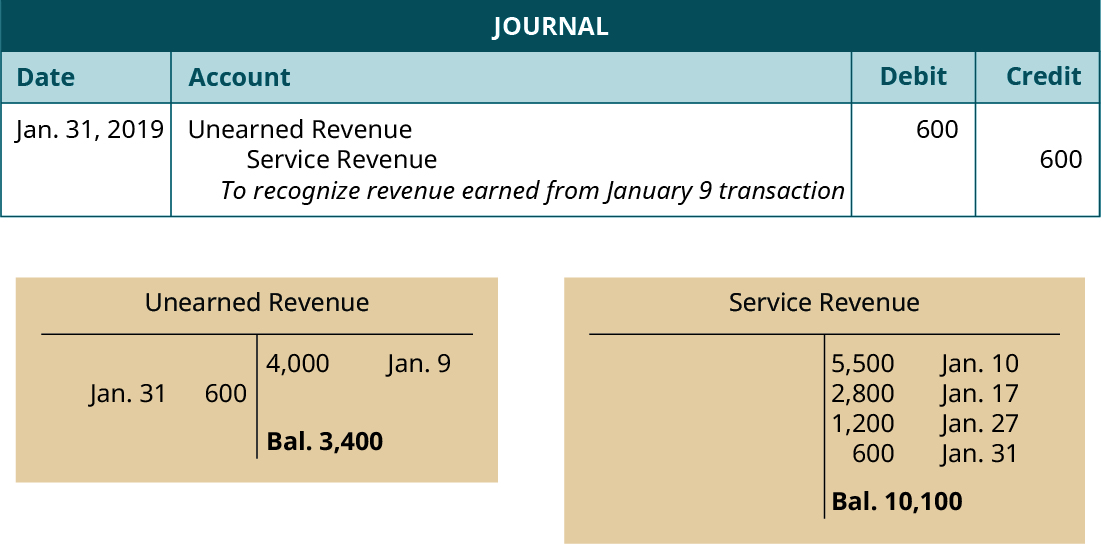

- Printing Plus performed $600 of services during January for the customer from the January 9 transaction.

- Reviewing the company bank statement, Printing Plus discovers $140 of interest earned during the month of January that was previously uncollected and unrecorded.

- Employees earned $1,500 in salaries for the period of January 21–January 31 that had been previously unpaid and unrecorded.

We now record the adjusting entries from January 31, 2019, for Printing Plus.

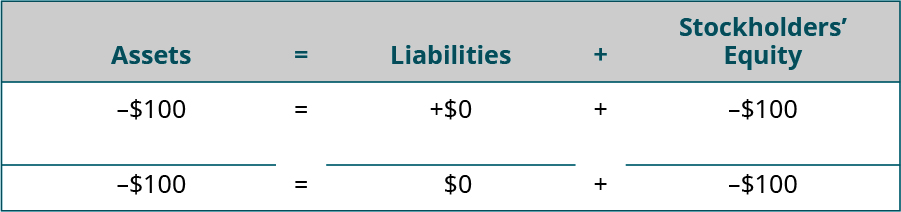

Transaction 13: On January 31, Printing Plus took an inventory of its supplies and discovered that $100 of supplies had been used during the month.

Analysis:

- $100 of supplies were used during January. Supplies is an asset that is decreasing (credit).

- Supplies is a type of prepaid expense that, when used, becomes an expense. Supplies Expense would increase (debit) for the $100 of supplies used during January.

Impact on the financial statements: Supplies is a balance sheet account, and Supplies Expense is an income statement account. This satisfies the rule that each adjusting entry will contain an income statement and balance sheet account. We see total assets decrease by $100 on the balance sheet. Supplies Expense increases overall expenses on the income statement, which reduces net income.

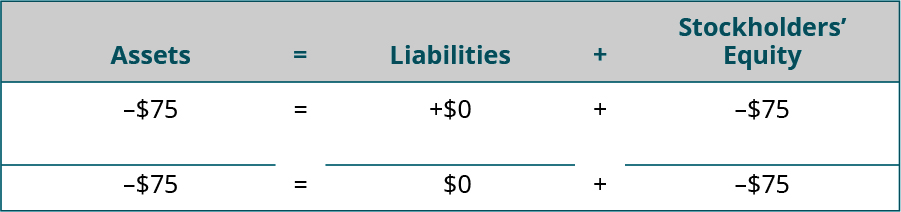

Transaction 14: The equipment purchased on January 5 depreciated $75 during the month of January.

Analysis:

- Of the Equipment cost, $3,500, $75 was used up during January. This depreciation will impact the Accumulated Depreciation–Equipment account and the Depreciation Expense–Equipment account. While we are not doing depreciation calculations here, you will come across more complex calculations in the future.

- Accumulated Depreciation–Equipment is a contra asset account (contrary to Equipment) and increases (credit) for $75.

- Depreciation Expense–Equipment is an expense account that is increasing (debit) for $75.

Impact on the financial statements: Accumulated Depreciation: Equipment is a contra account to Equipment. When calculating the book value of Equipment, Accumulated Depreciation–Equipment will be deducted from the original cost of the equipment. [Equipment $3,500 – Accumulated Depreciation $75 = book value $3,425] (Recall that the original cost of the equipment sits undisturbed in the Equipment account.) Therefore, total assets will decrease by $75 on the balance sheet. Depreciation Expense will increase overall expenses on the income statement, which reduces net income.

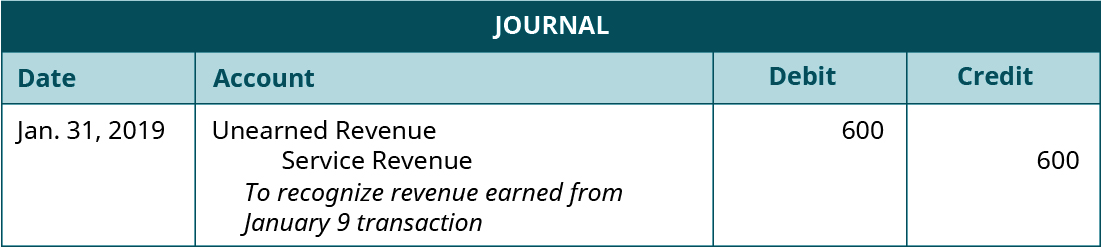

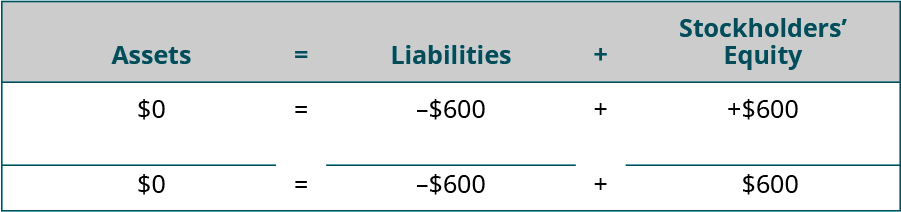

Transaction 15: Printing Plus performed $600 of services during January for the customer from the January 9 transaction.

Analysis:

- The customer from the January 9 transaction gave the company $4,000 in advanced payment for services. By the end of January the company had earned $600 of the advanced payment. This means that the company still has yet to provide $3,400 in services to that customer.

- Since some of the unearned revenue is now earned, Unearned Revenue would decrease. Unearned Revenue is a liability account and decreases on the debit side.

- The company can now recognize the $600 as earned revenue. Service Revenue increases (credit) for $600.

Impact on the financial statements: Unearned revenue is a liability account and will decrease total liabilities and equity by $600 on the balance sheet. Service Revenue will increase overall revenue on the income statement, which increases net income.

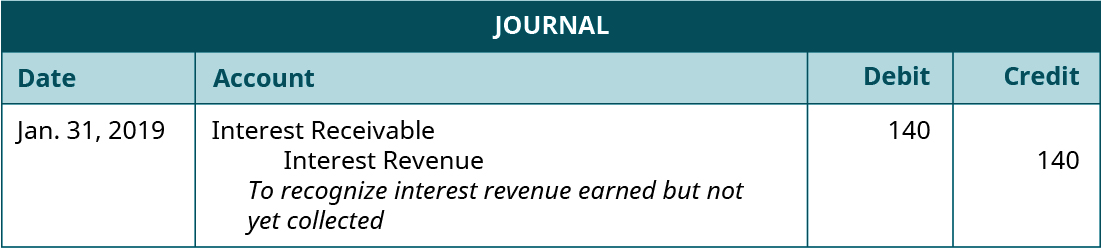

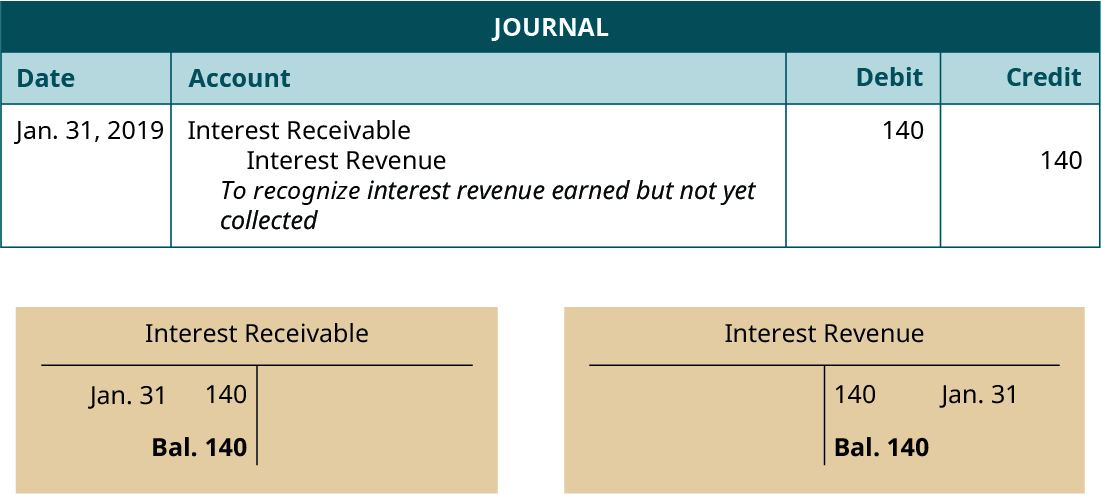

Transaction 16: Reviewing the company bank statement, Printing Plus discovers $140 of interest earned during the month of January that will be received at the end of the quarter, on March 31.

Analysis:

- Interest is revenue for the company on money kept in a savings account at the bank. The company only sees the bank statement at the end of the month and needs to record interest revenue that has not yet been collected or recorded.

- Interest Revenue is a revenue account that increases (credit) for $140.

- Since Printing Plus has yet to collect this interest revenue, it is considered a receivable. Interest Receivable increases (debit) for $140.

Impact on the financial statements: Interest Receivable is an asset account and will increase total assets by $140 on the balance sheet. Interest Revenue will increase overall revenue on the income statement, which increases net income.

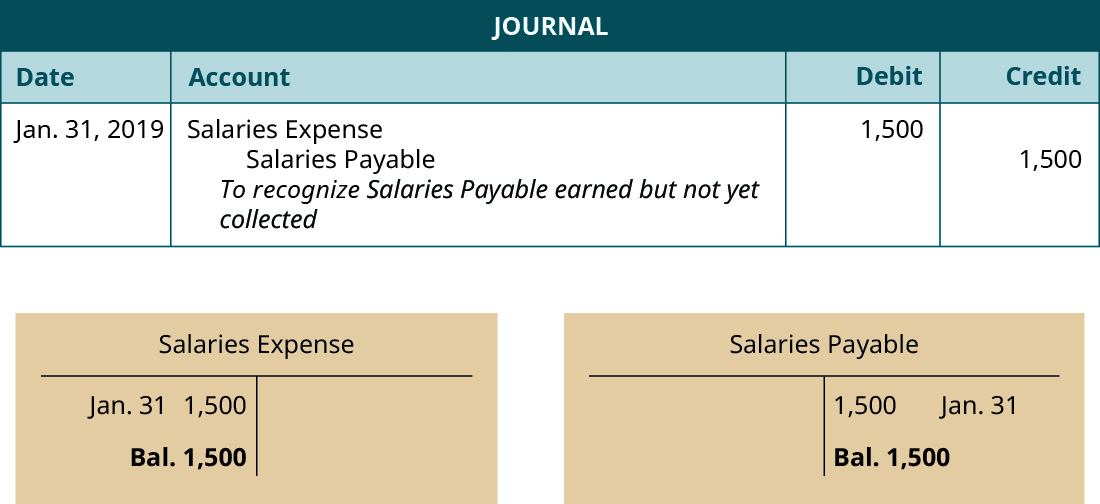

Transaction 17: Employees earned $1,500 in salaries for the period of January 21–January 31 that had been previously unpaid and unrecorded.

Analysis:

- Salaries have accumulated since January 21 and will not be paid in the current period. Since the salaries expense occurred in January, the expense recognition principle requires recognition in January.

- Salaries Expense is an expense account that is increasing (debit) for $1,500.

- Since the company has not yet paid salaries for this time period, Printing Plus owes the employees this money. This creates a liability for Printing Plus. Salaries Payable increases (credit) for $1,500.

Impact on the financial statements: Salaries Payable is a liability account and will increase total liabilities and equity by $1,500 on the balance sheet. Salaries expense will increase overall expenses on the income statement, which decreases net income.

Next we’ll explore how these adjusting entries impact the general ledger (T-accounts).

YOUR TURN

Label each of the following as a deferral or an accrual, and explain your answer.

- The company recorded supplies usage for the month.

- A customer paid in advance for services, and the company recorded revenue earned after providing service to that customer.

- The company recorded salaries that had been earned by employees but were previously unrecorded and have not yet been paid.

Solution

- The company is recording a deferred expense. The company was deferring the recognition of supplies from supplies expense until it had used the supplies.

- The company has deferred revenue. It deferred the recognition of the revenue until it was actually earned. The customer already paid the cash and is currently on the balance sheet as a liability.

- The company has an accrued expense. The company is bringing the salaries that have been incurred, added up since the last paycheck, onto the books for the first time during the adjusting entry. Cash will be given to the employees at a later time.

LINK TO LEARNING

Posting Adjusting Entries

Once you have journalized all of your adjusting entries, the next step is posting the entries to your ledger. Posting adjusting entries is no different than posting the regular daily journal entries. T-accounts will be the visual representation for the Printing Plus general ledger.

Transaction 13: On January 31, Printing Plus took an inventory of its supplies and discovered that $100 of supplies had been used during the month.

Journal entry and T-accounts:

In the journal entry, Supplies Expense has a debit of $100. This is posted to the Supplies Expense T-account on the debit side (left side). Supplies has a credit balance of $100. This is posted to the Supplies T-account on the credit side (right side). You will notice there is already a debit balance in this account from the purchase of supplies on January 30. The $100 is deducted from $500 to get a final debit balance of $400.

Transaction 14: The equipment purchased on January 5 depreciated $75 ($75 of the equipment cost was used up) during the month of January.

Journal entry and T-accounts:

In the journal entry, Depreciation Expense–Equipment has a debit of $75. This is posted to the Depreciation Expense–Equipment T-account on the debit side (left side). Accumulated Depreciation–Equipment has a credit balance of $75. This is posted to the Accumulated Depreciation–Equipment T-account on the credit side (right side).

Transaction 15: Printing Plus performed $600 of services during January for the customer from the January 9 transaction.

Journal entry and T-accounts:

In the journal entry, Unearned Revenue has a debit of $600. This is posted to the Unearned Revenue T-account on the debit side (left side). You will notice there is already a credit balance in this account from the January 9 customer payment. The $600 debit is subtracted from the $4,000 credit to get a final balance of $3,400 (credit). Service Revenue has a credit balance of $600. This is posted to the Service Revenue T-account on the credit side (right side). You will notice there is already a credit balance in this account from other revenue transactions in January. The $600 is added to the previous $9,500 balance in the account to get a new final credit balance of $10,100.

Transaction 16: Reviewing the company bank statement, Printing Plus discovers $140 of interest earned during the month of January that will not be received until the end of the quarter, March 31.

Journal entry and T-accounts:

In the journal entry, Interest Receivable has a debit of $140. This is posted to the Interest Receivable T-account on the debit side (left side). Interest Revenue has a credit balance of $140. This is posted to the Interest Revenue T-account on the credit side (right side).

Transaction 17: Employees earned $1,500 in salaries for the period of January 21–January 31 that had been previously unpaid and unrecorded.

Journal entry and T-accounts:

In the journal entry, Salaries Expense has a debit of $1,500. This is posted to the Salaries Expense T-account on the debit side (left side). You will notice there is already a debit balance in this account from the January 20 employee salary expense. The $1,500 debit is added to the $3,600 debit to get a final balance of $5,100 (debit). Salaries Payable has a credit balance of $1,500. This is posted to the Salaries Payable T-account on the credit side (right side).

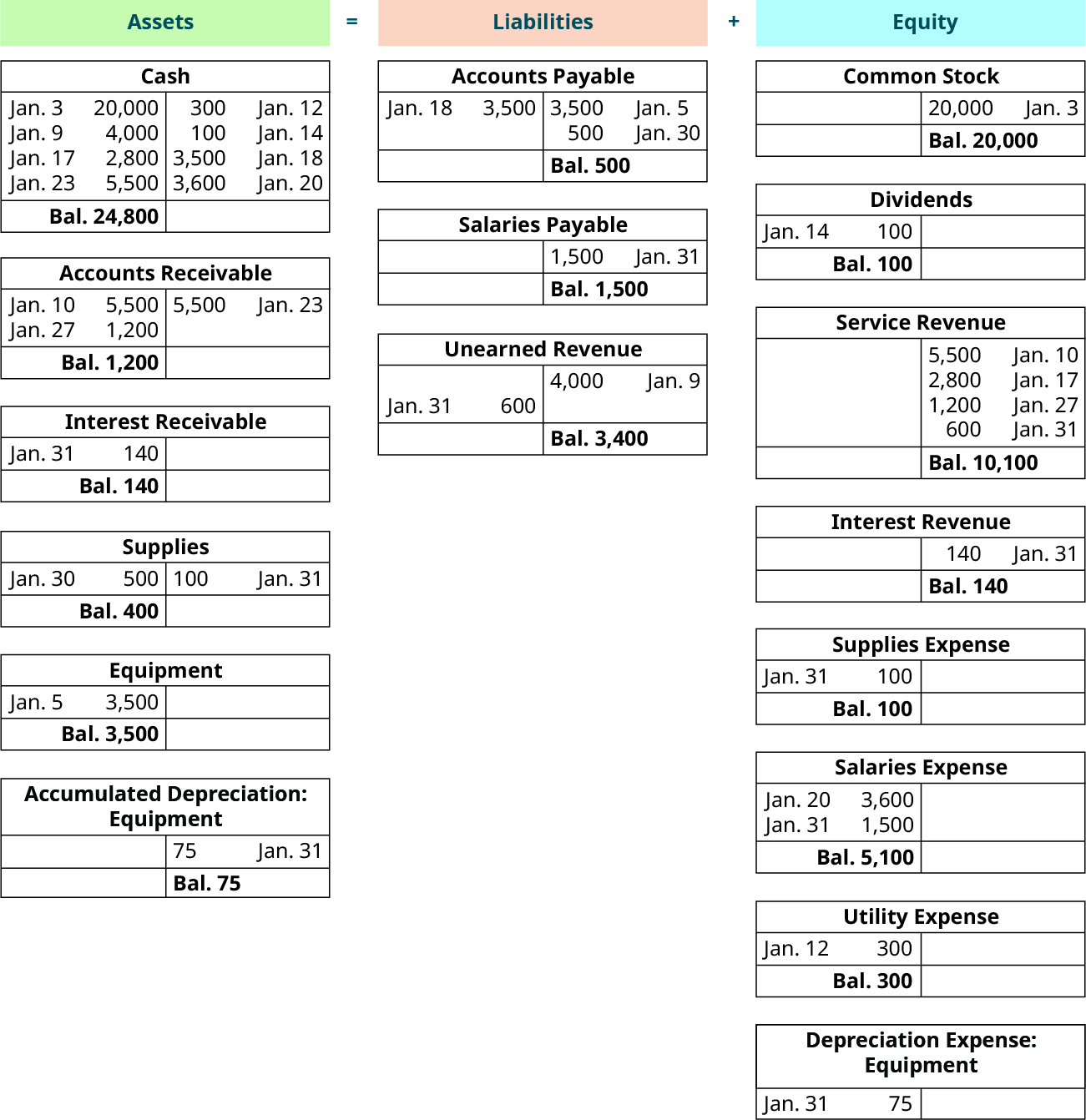

T-accounts Summary

Once all adjusting journal entries have been posted to T-accounts, we can check to make sure the accounting equation remains balanced. Following is a summary showing the T-accounts for Printing Plus including adjusting entries.

The sum on the assets side of the accounting equation equals $29,965, found by adding together the final balances in each asset account (24,800 + 1,200 + 140 + 400 + 3,500 – 75). To find the total on the liabilities and equity side of the equation, we need to find the difference between debits and credits. Credits on the liabilities and equity side of the equation total $35,640 (500 + 1,500 + 3,400 + 20,000 + 10,100 + 140). Debits on the liabilities and equity side of the equation total $5,675 (100 + 100 + 5,100 + 300 + 75). The difference between $35,640 – $5,675 = $29,965. Thus, the equation remains balanced with $29,965 on the asset side and $29,965 on the liabilities and equity side. Now that we have the T-account information, and have confirmed the accounting equation remains balanced, we can create the adjusted trial balance in our sixth step in the accounting cycle.

When posting any kind of journal entry to a general ledger, it is important to have an organized system for recording to avoid any account discrepancies and misreporting. To do this, companies can streamline their general ledger and remove any unnecessary processes or accounts. Check out this article “Encourage General Ledger Efficiency” from the Journal of Accountancy that discusses some strategies to improve general ledger efficiency.

KEY TAKEAWAYS

Key Concepts and Summary

- Rules for adjusting entries: The rules for recording adjusting entries are as follows: every adjusting entry will have one income statement account and one balance sheet account, cash will never be in an adjusting entry, and the adjusting entry records the change in amount that occurred during the period.

- Posting adjusting entries: Posting adjusting entries is the same process as posting general journal entries. The additional adjustments may add accounts to the end of the period or may change account balances from the earlier journal entry step in the accounting cycle.

Footnotes

- 1 U.S. Securities and Exchange Commission. “SEC Charges Mexico-Based Homebuilder in $3.3 Billion Accounting Fraud. Press Release.” March 3, 2017. https://www.sec.gov/news/pressrelease/2017-60.html

Glossary

- adjusted trial balance

- list of all accounts in the general ledger, including adjusting entries, which have nonzero balances

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

difference between the asset’s value (cost) and accumulated depreciation; also, value at which assets or liabilities are recorded in a company’s financial statements

list of all accounts in the general ledger, after adjusting entries have been posted for the accounting period