LO 16.3 Prepare the Statement of Cash Flows Using the Indirect Method

The statement of cash flows is prepared by following these steps:

Step 1: Determine Net Cash Flows from Operating Activities

Using the indirect method, operating net cash flow is calculated as follows:

- Begin with net income from the income statement.

- Add back noncash expenses, such as depreciation, amortization, and depletion.

- Remove the effect of gains and/or losses from disposal of long-term assets, as cash from the disposal of long-term assets is shown under investing cash flows.

- Adjust for changes in current assets and liabilities to remove accruals from operating activities.

Step 2: Determine Net Cash Flows from Investing Activities

Investing net cash flow includes cash received and cash paid relating to long-term assets.

Step 3: Present Net Cash Flows from Financing Activities

Financing net cash flow includes cash received and cash paid relating to long-term liabilities and equity.

Step 4: Reconcile Total Net Cash Flows to Change in Cash Balance during the Period

To reconcile beginning and ending cash balances:

- The net cash flows from the first three steps are combined to be total net cash flow.

- The beginning cash balance is presented from the prior year balance sheet.

- Total net cash flow added to the beginning cash balance equals the ending cash balance.

Step 5: Present Noncash Investing and Financing Transactions

Transactions that do not affect cash but do affect long-term assets, long-term debt, and/or equity are disclosed, either as a notation at the bottom of the statement of cash flow, or in the notes to the financial statements.

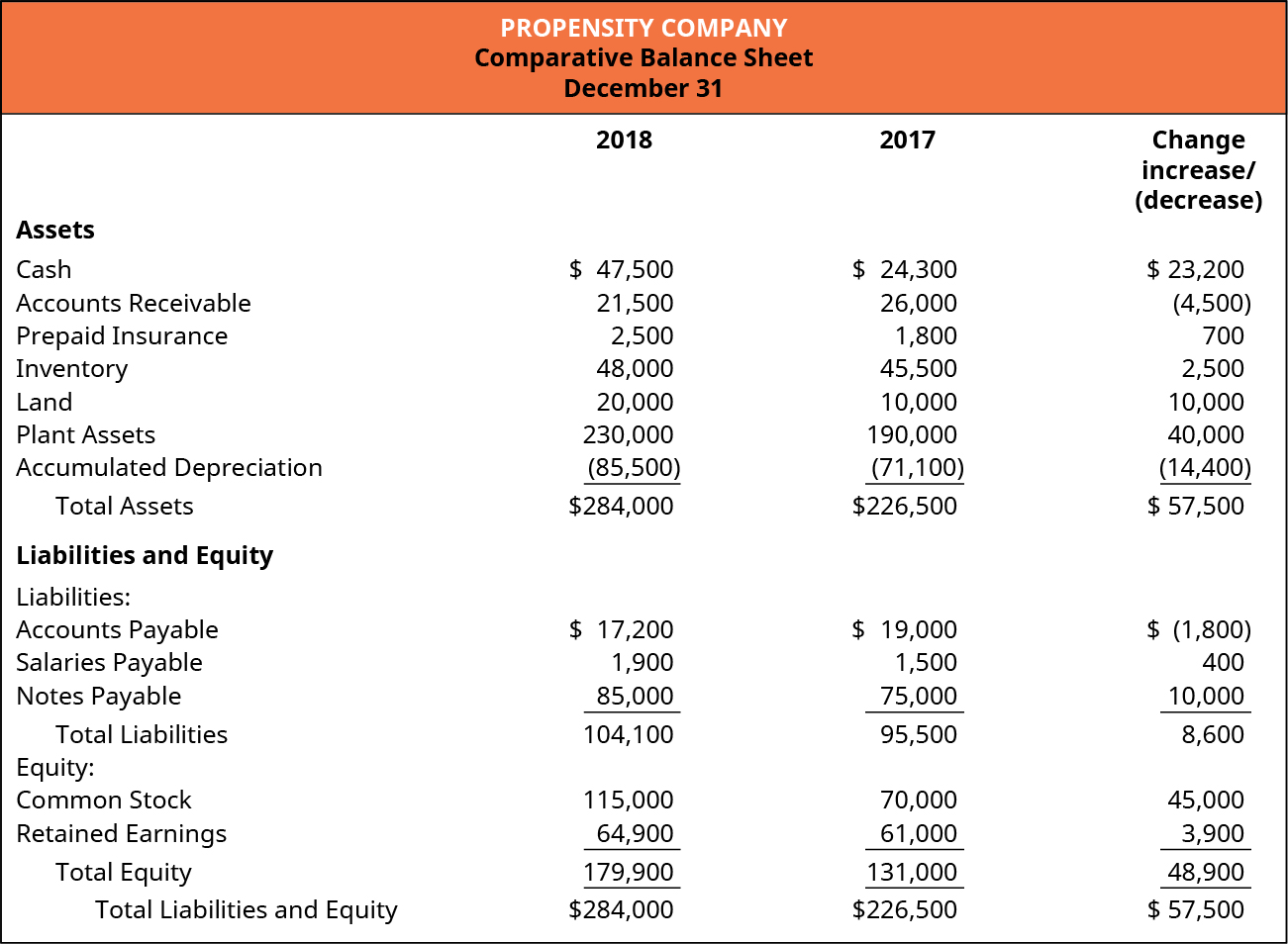

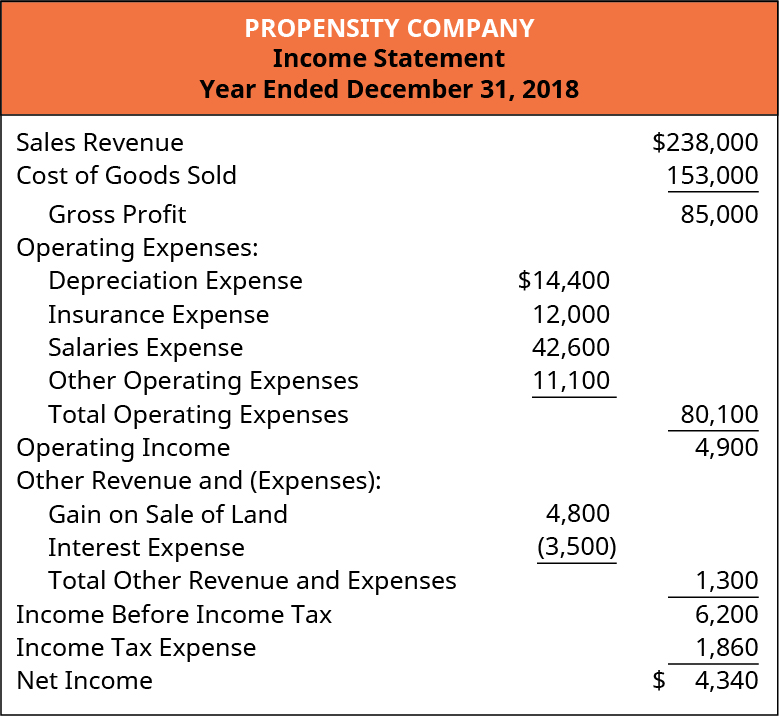

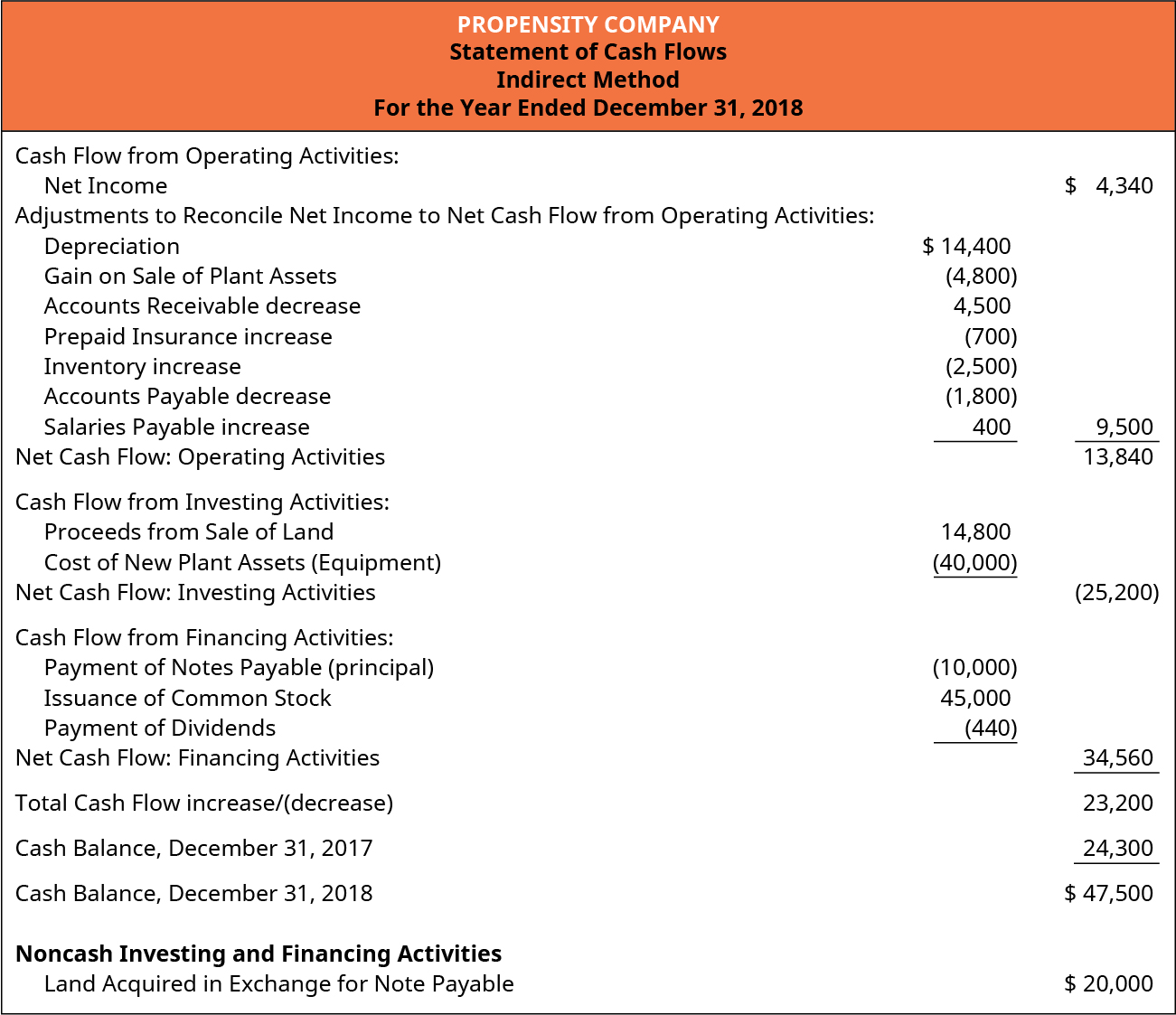

The remainder of this section demonstrates preparation of the statement of cash flows of the company whose financial statements are shown in (Figure), (Figure), and (Figure).

Additional Information:

- Propensity Company sold land with an original cost of $10,000, for $14,800 cash.

- A new parcel of land was purchased for $20,000, in exchange for a note payable.

- Plant assets were purchased for $40,000 cash.

- Propensity declared and paid a $440 cash dividend to shareholders.

- Propensity issued common stock in exchange for $45,000 cash.

Prepare the Operating Activities Section of the Statement of Cash Flows Using the Indirect Method

In the following sections, specific entries are explained to demonstrate the items that support the preparation of the operating activities section of the Statement of Cash Flows (Indirect Method) for the Propensity Company example financial statements.

- Begin with net income from the income statement.

- Add back noncash expenses, such as depreciation, amortization, and depletion.

- Reverse the effect of gains and/or losses from investing activities.

- Adjust for changes in current assets and liabilities, to reflect how those changes impact cash in a way that is different than is reported in net income.0

Start with Net Income

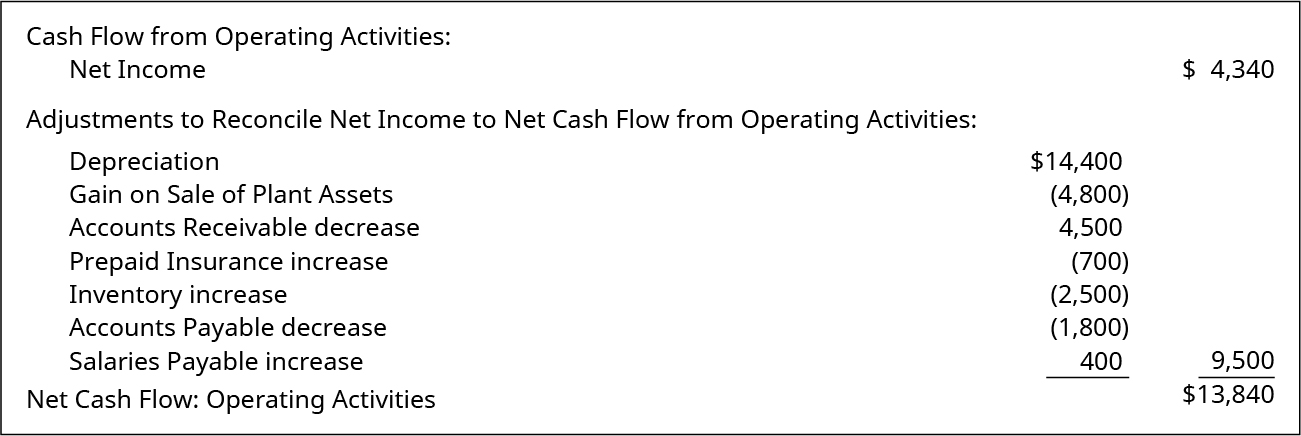

The operating activities cash flow is based on the company’s net income, with adjustments for items that affect cash differently than they affect net income. The net income on the Propensity Company income statement for December 31, 2018, is $4,340. On Propensity’s statement of cash flows, this amount is shown in the Cash Flows from Operating Activities section as Net Income.

Add Back Noncash Expenses

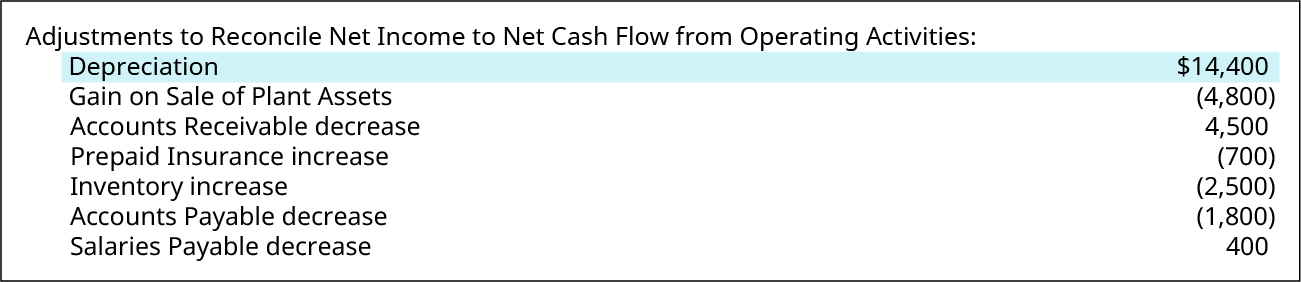

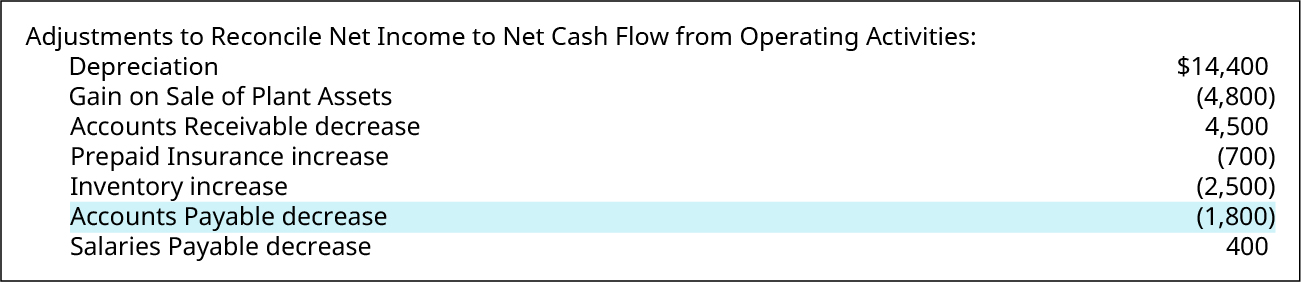

Net income includes deductions for noncash expenses. To reconcile net income to cash flow from operating activities, these noncash items must be added back, because no cash was expended relating to that expense. The sole noncash expense on Propensity Company’s income statement, which must be added back, is the depreciation expense of $14,400. On Propensity’s statement of cash flows, this amount is shown in the Cash Flows from Operating Activities section as an adjustment to reconcile net income to net cash flow from operating activities.

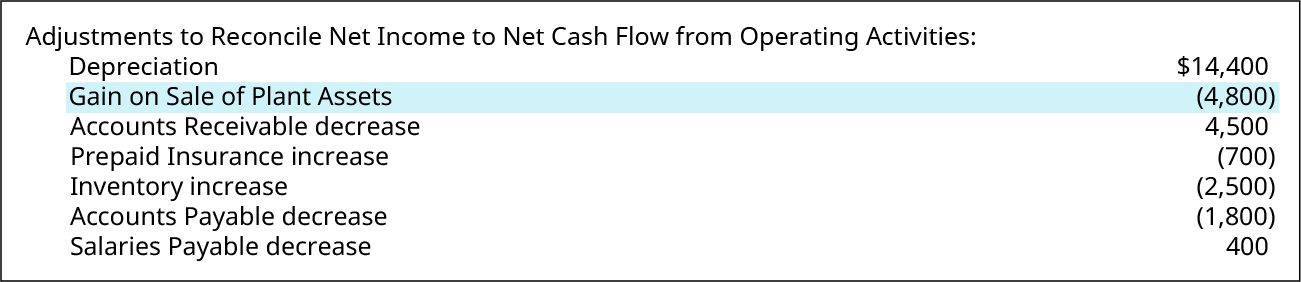

Reverse the Effect of Gains and/or Losses

Gains and/or losses on the disposal of long-term assets are included in the calculation of net income, but cash obtained from disposing of long-term assets is a cash flow from an investing activity. Because the disposition gain or loss is not related to normal operations, the adjustment needed to arrive at cash flow from operating activities is a reversal of any gains or losses that are included in the net income total. A gain is subtracted from net income and a loss is added to net income to reconcile to cash from operating activities. Propensity’s income statement for the year 2018 includes a gain on sale of land, in the amount of $4,800, so a reversal is accomplished by subtracting the gain from net income. On Propensity’s statement of cash flows, this amount is shown in the Cash Flows from Operating Activities section as Gain on Sale of Plant Assets.

Adjust for Changes in Current Assets and Liabilities

Because the Balance Sheet and Income Statement reflect the accrual basis of accounting, whereas the statement of cash flows considers the incoming and outgoing cash transactions, there are continual differences between (1) cash collected and paid and (2) reported revenue and expense on these statements. Changes in the various current assets and liabilities can be determined from analysis of the company’s comparative balance sheet, which lists the current period and previous period balances for all assets and liabilities. The following four possibilities offer explanations of the type of difference that might arise, and demonstrate examples from Propensity Company’s statement of cash flows, which represent typical differences that arise relating to these current assets and liabilities.

Increase in Noncash Current Assets

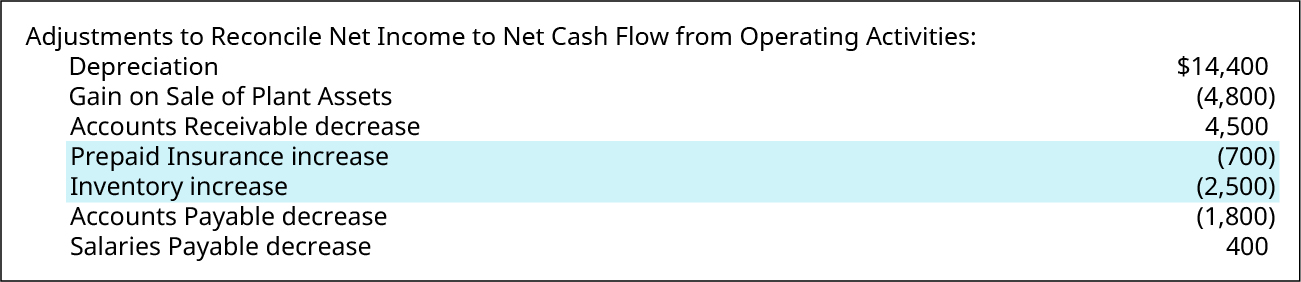

Increases in current assets indicate a decrease in cash, because either (1) cash was paid to generate another current asset, such as inventory, or (2) revenue was accrued, but not yet collected, such as accounts receivable. In the first scenario, the use of cash to increase the current assets is not reflected in the net income reported on the income statement. In the second scenario, revenue is included in the net income on the income statement, but the cash has not been received by the end of the period. In both cases, current assets increased and net income was reported on the income statement greater than the actual net cash impact from the related operating activities. To reconcile net income to cash flow from operating activities, subtract increases in current assets.

Propensity Company had two instances of increases in current assets. One was an increase of $700 in prepaid insurance, and the other was an increase of $2,500 in inventory. In both cases, the increases can be explained as additional cash that was spent, but which was not reflected in the expenses reported on the income statement.

Decrease in Noncash Current Assets

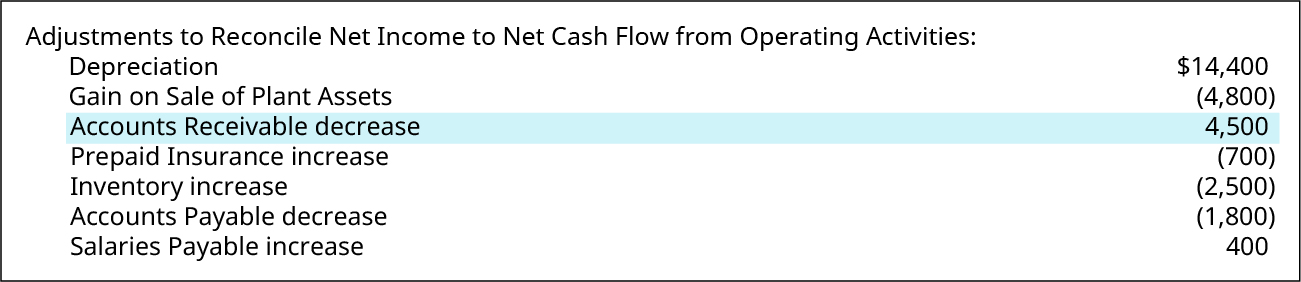

Decreases in current assets indicate lower net income compared to cash flows from (1) prepaid assets and (2) accrued revenues. For decreases in prepaid assets, using up these assets shifts these costs that were recorded as assets over to current period expenses that then reduce net income for the period. Cash was paid to obtain the prepaid asset in a prior period. Thus, cash from operating activities must be increased to reflect the fact that these expenses reduced net income on the income statement, but cash was not paid this period. Secondarily, decreases in accrued revenue accounts indicates that cash was collected in the current period but was recorded as revenue on a previous period’s income statement. In both scenarios, the net income reported on the income statement was lower than the actual net cash effect of the transactions. To reconcile net income to cash flow from operating activities, add decreases in current assets.

Propensity Company had a decrease of $4,500 in accounts receivable during the period, which normally results only when customers pay the balance, they owe the company at a faster rate than they charge new account balances. Thus, the decrease in receivable identifies that more cash was collected than was reported as revenue on the income statement. Thus, an addback is necessary to calculate the cash flow from operating activities.

Current Operating Liability Increase

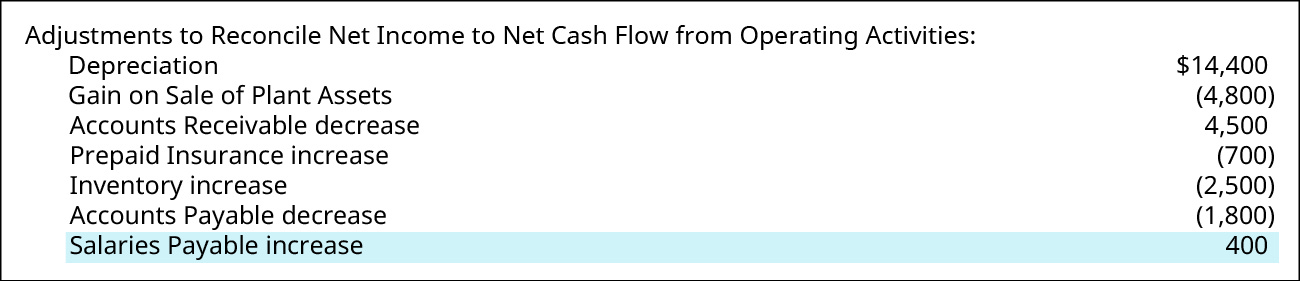

Increases in current liabilities indicate an increase in cash, since these liabilities generally represent (1) expenses that have been accrued, but not yet paid, or (2) deferred revenues that have been collected, but not yet recorded as revenue. In the case of accrued expenses, costs have been reported as expenses on the income statement, whereas the deferred revenues would arise when cash was collected in advance, but the revenue was not yet earned, so the payment would not be reflected on the income statement. In both cases, these increases in current liabilities signify cash collections that exceed net income from related activities. To reconcile net income to cash flow from operating activities, add increases in current liabilities.

Propensity Company had an increase in the current operating liability for salaries payable, in the amount of $400. The payable arises, or increases, when an expense is recorded but the balance due is not paid at that time. An increase in salaries payable therefore reflects the fact that salaries expenses on the income statement are greater than the cash outgo relating to that expense. This means that net cash flow from operating is greater than the reported net income, regarding this cost.

Current Operating Liability Decrease

Decreases in current liabilities indicate a decrease in cash relating to (1) accrued expenses, or (2) deferred revenues. In the first instance, cash would have been expended to accomplish a decrease in liabilities arising from accrued expenses, yet these cash payments would not be reflected in the net income on the income statement. In the second instance, a decrease in deferred revenue means that some revenue would have been reported on the income statement that was collected in a previous period. As a result, cash flows from operating activities must be decreased by any reduction in current liabilities, to account for (1) cash payments to creditors that are higher than the expense amounts on the income statement, or (2) amounts collected that are lower than the amounts reflected as income on the income statement. To reconcile net income to cash flow from operating activities, subtract decreases in current liabilities.

Propensity Company had a decrease of $1,800 in the current operating liability for accounts payable. The fact that the payable decreased indicates that Propensity paid enough payments during the period to keep up with new charges, and also to pay down on amounts payable from previous periods. Therefore, the company had to have paid more in cash payments than the amounts shown as expense on the Income Statements, which means net cash flow from operating activities is lower than the related net income.

Analysis of Change in Cash

Although the net income reported on the income statement is an important tool for evaluating the success of the company’s efforts for the current period and their viability for future periods, the practical effectiveness of management is not adequately revealed by the net income alone. The net cash flows from operating activities adds this essential facet of information to the analysis, by illuminating whether the company’s operating cash sources were adequate to cover their operating cash uses. When combined with the cash flows produced by investing and financing activities, the operating activity cash flow indicates the feasibility of continuance and advancement of company plans.

Determining Net Cash Flow from Operating Activities (Indirect Method)

Net cash flow from operating activities is the net income of the company, adjusted to reflect the cash impact of operating activities. Positive net cash flow generally indicates adequate cash flow margins exist to provide continuity or ensure survival of the company. The magnitude of the net cash flow, if large, suggests a comfortable cash flow cushion, while a smaller net cash flow would signify an uneasy comfort cash flow zone. When a company’s net cash flow from operations reflects a substantial negative value, this indicates that the company’s operations are not supporting themselves and could be a warning sign of possible impending doom for the company. Alternatively, a small negative cash flow from operating might serve as an early warning that allows management to make needed corrections, to ensure that cash sources are increased to amounts in excess of cash uses, for future periods.

For Propensity Company, beginning with net income of $4,340, and reflecting adjustments of $9,500, delivers a net cash flow from operating activities of $13,840.

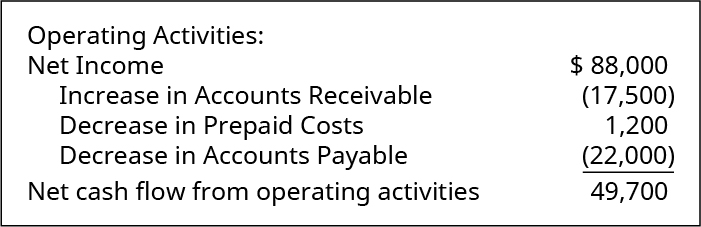

YOUR TURN

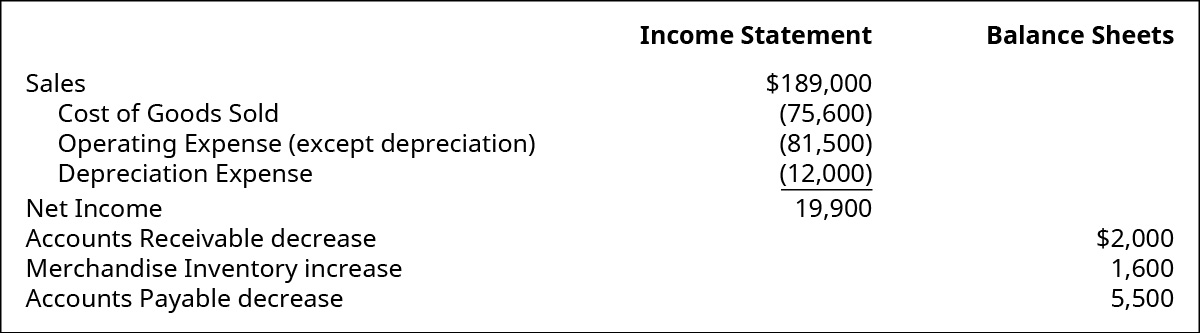

Assume you own a specialty bakery that makes gourmet cupcakes. Excerpts from your company’s financial statements are shown.

How much cash flow from operating activities did your company generate?

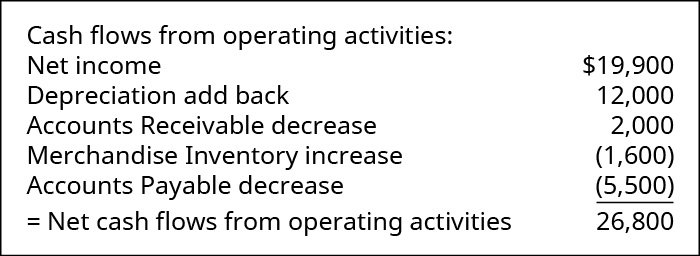

Solution

THINK IT THROUGH

Assume that you are the chief financial officer of a company that provides accounting services to small businesses. You are called upon by the board of directors to explain why your cash balance did not increase much from the beginning of 2018 until the end of 2018, since the company produced a reasonably strong profit for the year, with a net income of $88,000. Further assume that there were no investing or financing transactions, and no depreciation expense for 2018. What is your response? Provide the calculations to back up your answer.

Prepare the Investing and Financing Activities Sections of the Statement of Cash Flows

Preparation of the investing and financing sections of the statement of cash flows is an identical process for both the direct and indirect methods, since only the technique used to arrive at net cash flow from operating activities is affected by the choice of the direct or indirect approach. The following sections discuss specifics regarding preparation of these two nonoperating sections, as well as notations about disclosure of long-term noncash investing and/or financing activities. Changes in the various long-term assets, long-term liabilities, and equity can be determined from analysis of the company’s comparative balance sheet, which lists the current period and previous period balances for all assets and liabilities.

Investing Activities

Cash flows from investing activities always relate to long-term asset transactions and may involve increases or decreases in cash relating to these transactions. The most common of these activities involve purchase or sale of property, plant, and equipment, but other activities, such as those involving investment assets and notes receivable, also represent cash flows from investing. Changes in long-term assets for the period can be identified in the Noncurrent Assets section of the company’s comparative balance sheet, combined with any related gain or loss that is included on the income statement.

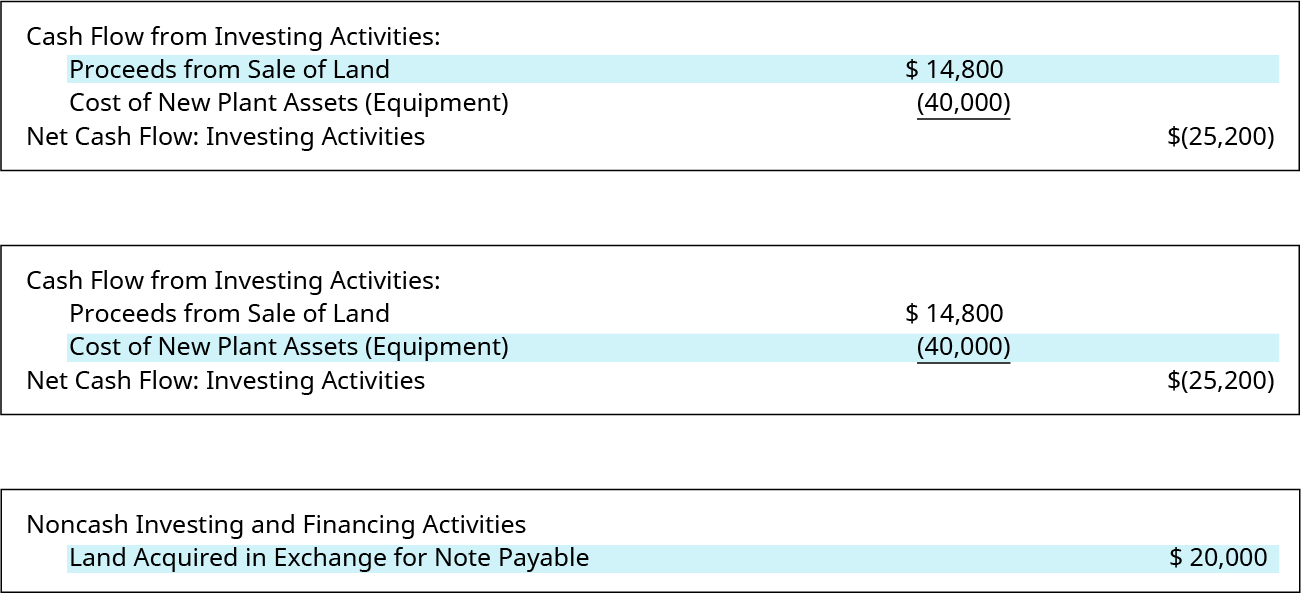

In the Propensity Company example, the investing section included two transactions involving long-term assets, one of which increased cash, while the other one decreased cash, for a total net cash flow from investing of ($25,200). Analysis of Propensity Company’s comparative balance sheet revealed changes in land and plant assets. Further investigation identified that the change in long-term assets arose from three transactions:

- Investing activity: A tract of land that had an original cost of $10,000 was sold for $14,800.

- Investing activity: Plant assets were purchased, for $40,000 cash.

- Noncash investing and financing activity: A new parcel of land was acquired, in exchange for a $20,000 note payable.

Details relating to the treatment of each of these transactions are provided in the following sections.

Investing Activities Leading to an Increase in Cash

Increases in net cash flow from investing usually arise from the sale of long-term assets. The cash impact is the cash proceeds received from the transaction, which is not the same amount as the gain or loss that is reported on the income statement. Gain or loss is computed by subtracting the asset’s net book value from the cash proceeds. Net book value is the asset’s original cost, less any related accumulated depreciation. Propensity Company sold land, which was carried on the balance sheet at a net book value of $10,000, representing the original purchase price of the land, in exchange for a cash payment of $14,800. The data set explained these net book value and cash proceeds facts for Propensity Company. However, had these facts not been stipulated in the data set, the cash proceeds could have been determined by adding the reported $4,800 gain on the sale to the $10,000 net book value of the asset given up, to arrive at cash proceeds from the sale.

Investing Activities Leading to a Decrease in Cash

Decreases in net cash flow from investing normally occur when long-term assets are purchased using cash. For example, in the Propensity Company example, there was a decrease in cash for the period relating to a simple purchase of new plant assets, in the amount of $40,000.

Financing Activities

Cash flows from financing activities always relate to either long-term debt or equity transactions and may involve increases or decreases in cash relating to these transactions. Stockholders’ equity transactions, like stock issuance, dividend payments, and treasury stock buybacks are very common financing activities. Debt transactions, such as issuance of bonds payable or notes payable, and the related principal payback of them, are also frequent financing events. Changes in long-term liabilities and equity for the period can be identified in the Noncurrent Liabilities section and the Stockholders’ Equity section of the company’s Comparative Balance Sheet, and in the retained earnings statement.

In the Propensity Company example, the financing section included three transactions. One long-term debt transaction decreased cash. Two transactions related to equity, one of which increased cash, while the other one decreased cash, for a total net cash flow from financing of $34,560. Analysis of Propensity Company’s Comparative Balance Sheet revealed changes in notes payable and common stock, while the retained earnings statement indicated that dividends were distributed to stockholders. Further investigation identified that the change in long-term liabilities and equity arose from three transactions:

- Financing activity: Principal payments of $10,000 were paid on notes payable.

- Financing activity: New shares of common stock were issued, in the amount of $45,000.

- Financing activity: Dividends of $440 were paid to shareholders.

Specifics about each of these three transactions are provided in the following sections.

Financing Activities Leading to an Increase in Cash

Increases in net cash flow from financing usually arise when the company issues share of stock, bonds, or notes payable to raise capital for cash flow. Propensity Company had one example of an increase in cash flows, from the issuance of common stock.

Financing Activities Leading to a Decrease in Cash

Decreases in net cash flow from financing normally occur when (1) long-term liabilities, such as notes payable or bonds payable are repaid, (2) when the company reacquires some of its own stock (treasury stock), or (3) when the company pays dividends to shareholders. In the case of Propensity Company, the decreases in cash resulted from notes payable principal repayments and cash dividend payments.

Noncash Investing and Financing Activities

Sometimes transactions can be very important to the company, yet not involve any initial change to cash. Disclosure of these noncash investing and financing transactions can be included in the notes to the financial statements, or as a notation at the bottom of the statement of cash flows, after the entire statement has been completed. These noncash activities usually involve one of the following scenarios:

- exchanges of long-term assets for long-term liabilities or equity, or

- exchanges of long-term liabilities for equity.

Propensity Company had a noncash investing and financing activity, involving the purchase of land (investing activity) in exchange for a $20,000 note payable (financing activity).

Summary of Investing and Financing Transactions on the Cash Flow Statement

Investing and financing transactions are critical activities of business, and they often represent significant amounts of company equity, either as sources or uses of cash. Common activities that must be reported as investing activities are purchases of land, equipment, stocks, and bonds, while financing activities normally relate to the company’s funding sources, namely, creditors and investors. These financing activities could include transactions such as borrowing or repaying notes payable, issuing or retiring bonds payable, or issuing stock or reacquiring treasury stock, to name a few instances.

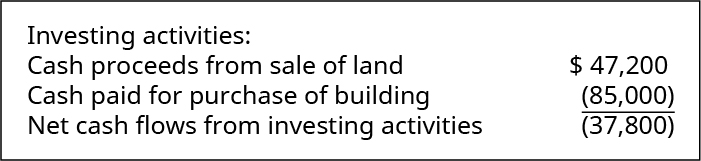

YOUR TURN

Assume your specialty bakery makes gourmet cupcakes and has been operating out of rented facilities in the past. You owned a piece of land that you had planned to someday use to build a sales storefront. This year your company decided to sell the land and instead buy a building, resulting in the following transactions.

What are the cash flows from investing activities relating to these transactions?

Solution

Note: Interest earned on investments is an operating activity.

KEY TAKEAWAYS

Key Concepts and Summary

- Preparing the operating section of statement of cash flows by the indirect method starts with net income from the income statement and adjusts for items that affect cash flows differently than they affect net income.

- Multiple levels of adjustments are required to reconcile accrual-based net income to cash flows from operating activities.

- The investing section of statement of cash flows relates to changes in long-term assets.

- The financing section of statement of cash flows relates to changes in long-term liabilities and changes in equity.

- Company activities that reflect changes in long-term assets, long-term liabilities, or equity, but have no cash impact, require special reporting treatment, as noncash investing and financing transactions.

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting