LO 12.4 Prepare Journal Entries to Record Short-Term Notes Payable

If you have ever taken out a payday loan, you may have experienced a situation where your living expenses temporarily exceeded your assets. You need enough money to cover your expenses until you get your next paycheck. Once you receive that paycheck, you can repay the lender the amount you borrowed, plus a little extra for the lender’s assistance.

There is an ebb and flow to business that can sometimes produce this same situation, where business expenses temporarily exceed revenues. Even if a company finds itself in this situation, bills still need to be paid. The company may consider a short-term note payable to cover the difference.

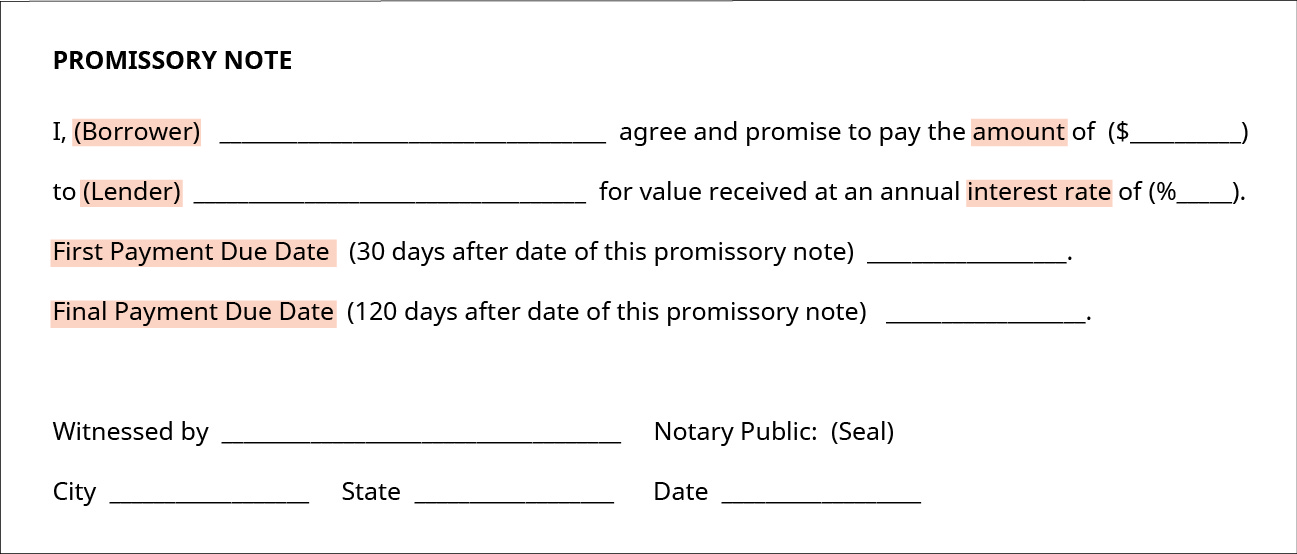

A short-term note payable is a debt created and due within a company’s operating period (less than a year). Some key characteristics of this written promise to pay (see (Figure)) include an established date for repayment, a specific payable amount, interest terms, and the possibility of debt resale to another party. A short-term note is classified as a current liability because it is wholly honored within a company’s operating period. This payable account would appear on the balance sheet under Current Liabilities.

Debt sale to a third party is a possibility with any loan, which includes a short-term note payable. The terms of the agreement will state this resale possibility, and the new debt owner honors the agreement terms of the original parties. A lender may choose this option to collect cash quickly and reduce the overall outstanding debt.

We now consider two short-term notes payable situations; one is created by a purchase, and the other is created by a loan.

THINK IT THROUGH

A common practice for government entities, particularly schools, is to issue short-term (promissory) notes to cover daily expenditures until revenues are received from tax collection, lottery funds, and other sources. School boards approve the note issuances, with repayments of principal and interest typically met within a few months.

The goal is to fully cover all expenses until revenues are distributed from the state. However, revenues distributed fluctuate due to changes in collection expectations, and schools may not be able to cover their expenditures in the current period. This leads to a dilemma—whether or not to issue more short-term notes to cover the deficit.

Short-term debt may be preferred over long-term debt when the entity does not want to devote resources to pay interest over an extended period of time. In many cases, the interest rate is lower than long-term debt, because the loan is considered less risky with the shorter payback period. This shorter payback period is also beneficial with amortization expenses; short-term debt typically does not amortize, unlike long-term debt.

What would you do if you found your school in this situation? Would you issue more debt? Are there alternatives? What are some positives and negatives to the promissory note practice?

Recording Short-Term Notes Payable Created by a Purchase

A short-term notes payable created by a purchase typically occurs when a payment to a supplier does not occur within the established time frame. The supplier might require a new agreement that converts the overdue accounts payable into a short-term note payable (see (Figure)), with interest added. This gives the company more time to make good on outstanding debt and gives the supplier an incentive for delaying payment. Also, the creation of the note payable creates a stronger legal position for the owner of the note, since the note is a negotiable legal instrument that can be more easily enforced in court actions.

To illustrate, let’s revisit Sierra Sports’ purchase of soccer equipment on August 1. Sierra Sports purchased $12,000 of soccer equipment from a supplier on credit. Credit terms were 2/10, n/30, invoice date August 1. Let’s assume that Sierra Sports was unable to make the payment due within 30 days. On August 31, the supplier renegotiates terms with Sierra and converts the accounts payable into a written note, requiring full payment in two months, beginning September 1. Interest is now included as part of the payment terms at an annual rate of 10%. The conversion entry from an account payable to a Short-Term Note Payable in Sierra’s journal is shown.

Accounts Payable decreases (debit) and Short-Term Notes Payable increases (credit) for the original amount owed of $12,000. When Sierra pays cash for the full amount due, including interest, on October 31, the following entry occurs.

Since Sierra paid the full amount due, Short-Term Notes Payable decreases (debit) for the principal amount of the debt. Interest Expense increases (debit) for two months of interest accumulation. Interest Expense is found from our earlier equation, where Interest = Principal × Annual interest rate × Part of year ($12,000 × 10% × [2/12]), which is $200. Cash decreases (credit) for $12,200, which is the principal plus the interest due.

The other short-term note scenario is created by a loan.

Recording Short-Term Notes Payable Created by a Loan

A short-term notes payable created by a loan transpires when a business incurs debt with a lender (Figure). A business may choose this path when it does not have enough cash on hand to finance a capital expenditure immediately but does not need long-term financing. The business may also require an influx of cash to cover expenses temporarily. There is a written promise to pay the principal balance and interest due on or before a specific date. This payment period is within a company’s operating period (less than a year). Consider a short-term notes payable scenario for Sierra Sports.

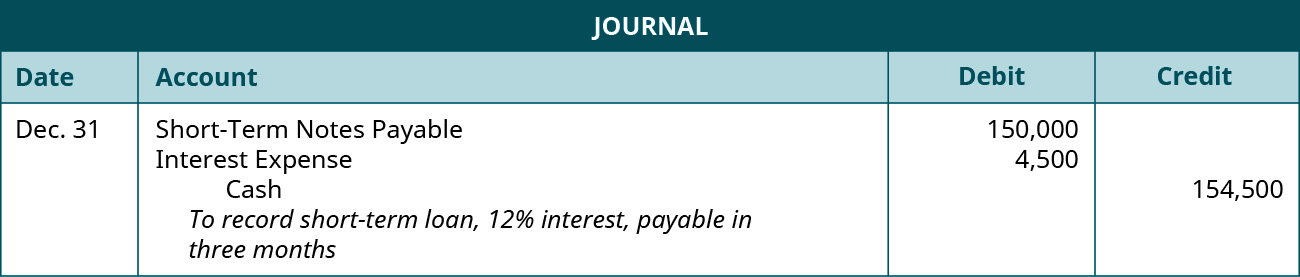

Sierra Sports requires a new apparel printing machine after experiencing an increase in custom uniform orders. Sierra does not have enough cash on hand currently to pay for the machine, but the company does not need long-term financing. Sierra borrows $150,000 from the bank on October 1, with payment due within three months (December 31), at a 12% annual interest rate. The following entry occurs when Sierra initially takes out the loan.

Cash increases (debit) as does Short-Term Notes Payable (credit) for the principal amount of the loan, which is $150,000. When Sierra pays in full on December 31, the following entry occurs.

Short-Term Notes Payable decreases (a debit) for the principal amount of the loan ($150,000). Interest Expense increases (a debit) for $4,500 (calculated as $150,000 principal × 12% annual interest rate × [3/12 months]). Cash decreases (a credit) for the principal amount plus interest due.

LINK TO LEARNING

KEY TAKEAWAYS

Key Concepts and Summary

- Short-term notes payable is a debt created and due within a company’s operating period (less than a year). This debt includes a written promise to pay principal and interest.

- If a company does not pay for its purchases within a specified time frame, a supplier will convert the accounts payable into a short-term note payable with interest. When the company pays the amount owed, short-term notes payable and Cash will decrease, while interest expense increases.

- A company may borrow from a bank because it does not have enough cash on hand to pay for a capital expenditure or cover temporary expenses. The loan will consist of short-term repayment with interest, affecting short-term notes payable, cash, and interest expense.

Glossary

- short-term note payable

- debt created and due within a company’s operating period (less than a year)

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

debt created and due within a company’s operating period (less than a year)