LO 2.3 Prepare an Income Statement, Statement of Retained Earnings, and Balance Sheet

One of the key factors for success for those beginning the study of accounting is to understand how the elements of the financial statements relate to each of the financial statements. That is, once the transactions are categorized into the elements, knowing what to do next is vital. This is the beginning of the process to create the financial statements. It is important to note that financial statements are discussed in the order in which the statements are presented.

Elements of the Financial Statements

When thinking of the relationship between the elements and the financial statements, we might think of a baking analogy: the elements represent the ingredients, and the financial statements represent the finished product. As with baking a cake (see Figure 1), knowing the ingredients (elements) and how each ingredient relates to the final product (financial statements) is vital to the study of accounting.

(Figure 1) Baking requires an understanding of the different ingredients, how the ingredients are used, and how the ingredients will impact the final product (a). If used correctly, the final product will be beautiful and, more importantly, delicious, like the cake shown in (b). In a similar manner, the study of accounting requires an understanding of how the accounting elements relate to the final product—the financial statements. (credit (a): modification of “U.S. Navy Culinary Specialist Seaman Robert Fritschie mixes cake batter aboard the amphibious command ship USS Blue Ridge (LCC 19) Aug. 7, 2013, while underway in the Solomon Sea 130807-N-NN332-044” by MC3 Jarred Harral/Wikimedia Commons, Public Domain; credit (b): modification of “Easter Cake with Colorful Topping” by Kaboompics .com/Pexels, CC0)

To help accountants prepare and users better understand financial statements, the profession has outlined what is referred to as elements of the financial statements, which are those categories or accounts that accountants use to record transactions and prepare financial statements. There are eight elements of the financial statements, and we have already discussed most of them.

- Revenue—value of goods and services the organization sold or provided.

- Expenses—costs of providing the goods or services for which the organization earns revenue.

- Assets—items the organization owns, controls, or has a claim to.

- Liabilities—amounts the organization owes to others (also called creditors).

- Equity—the net worth (or net assets) of the organization.

- Contributed capital (receive assets from owners)—cash or other assets received by the organization in exchange for an ownership interest.

- Dividends (distribute assets to owners)—cash, other assets, or ownership interest (equity) distributed to owners.

- Retained earnings–revenues remaining after expenses and dividends

Financial Statements for a Sample Company

Now it is time to bake the cake (i.e., prepare the financial statements). We have all of the ingredients (elements of the financial statements) ready, so let’s now return to the financial statements themselves. Let’s use as an example a fictitious company named Cheesy Chuck’s Classic Corn. This company is a small retail store that makes and sells a variety of gourmet popcorn treats. It is an exciting time because the store opened in the current month, June.

Assume that as part of your summer job with Cheesy Chuck’s, the owner—you guessed it, Chuck—has asked you to take over for a former employee who graduated college and will be taking an accounting job in New York City. In addition to your duties involving making and selling popcorn at Cheesy Chuck’s, part of your responsibility will be doing the accounting for the business. The owner, Chuck, heard that you are studying accounting and could really use your help, because he spends most of his time developing new popcorn flavors.

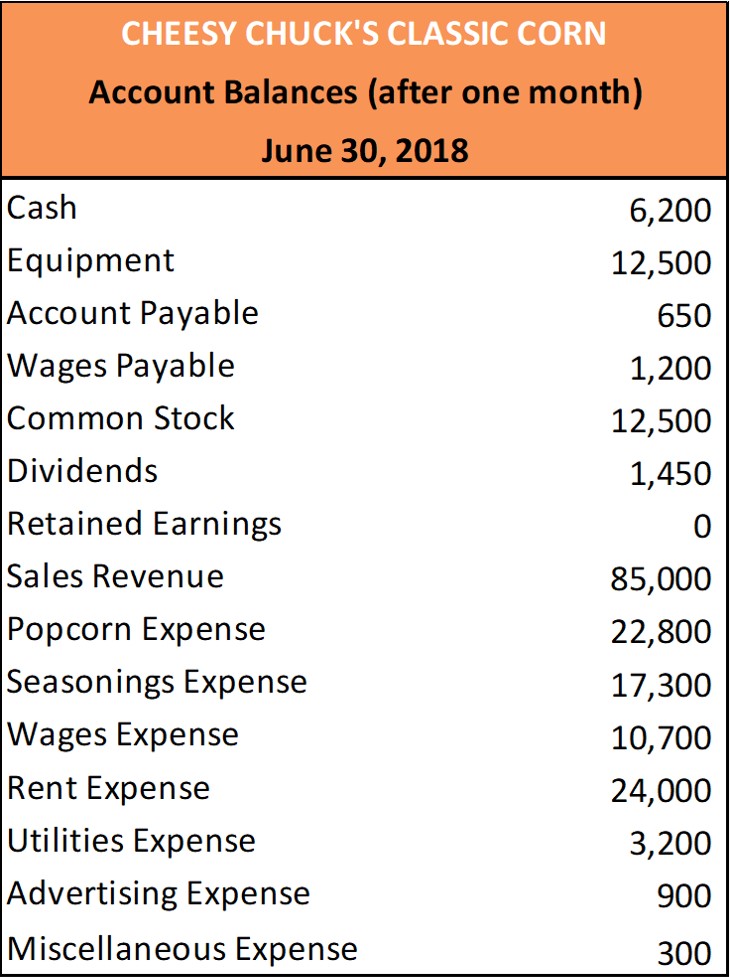

The former employee has done a nice job of keeping track of the accounting records, so you can focus on your first task of creating the June financial statements, which Chuck is eager to see. (Figure 2) shows the financial information (as of June 30) for Cheesy Chuck’s.

We should note that we are oversimplifying some of the things in this example. First, the amounts in the accounts were given. We did not explain how the amounts would be derived. This process is explained starting in Analyzing and Recording Transactions. Second, we are ignoring the timing of certain cash flows such as hiring, purchases, and other startup costs. In reality, businesses must invest cash to prepare the store, train employees, and obtain the equipment and inventory necessary to open. These costs will precede the selling of goods and services.

Income Statement

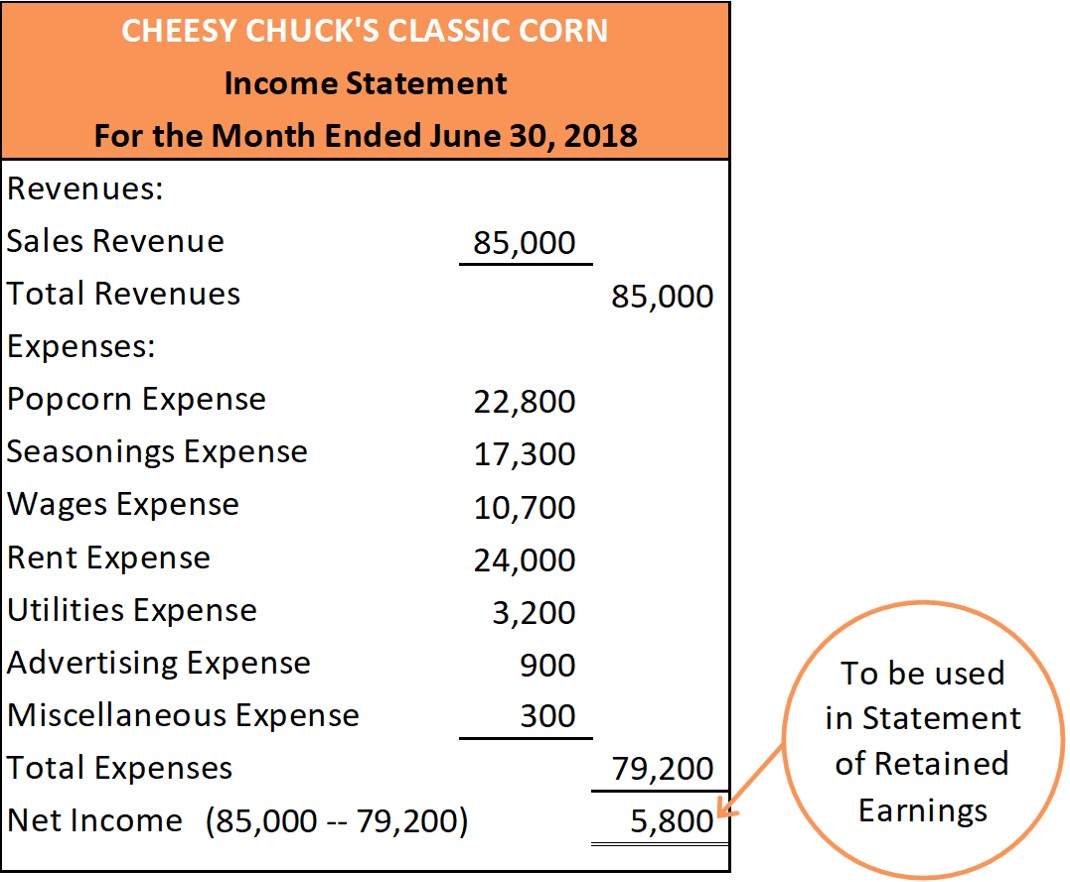

Let’s prepare the income statement so we can see how Cheesy Chuck’s performed for the month of June (remember, an income statement is for a period of time) See (Figure 3). Our first step is to determine how much the business has earned. For a given period of time, how much did the goods sold and services provided, sell for? These are the inflows to the business, and because the inflows relate to the primary purpose of the business (making and selling popcorn), we classify those items as Revenues, Sales, or Fees Earned. For this example, we use Sales Revenue. The revenue for Cheesy Chuck’s for the month of June is $85,000.

Next, we need to show the total expenses for Cheesy Chuck’s. Because Cheesy Chuck’s tracks different types of expenses, we need to add the amounts to calculate total expenses. If you added correctly, you get total expenses for the month of June of $79,200. The final step to create the income statement is to determine the amount of net income or net loss for Cheesy Chuck’s. Since revenues ($85,000) are greater than expenses ($79,200), Cheesy Chuck’s has a net income of $5,800 for the month of June.

(Figure 3) Income Statement for Cheesy Chuck’s Classic Corn. The income statement for Cheesy Chuck’s shows the business had Net Income of $5,800 for the month ended June 30. This amount will be used to prepare the next financial statement, the statement of retained earnings.

Financial statements are created using numerous standard conventions or practices. The standard conventions provide consistency and help assure financial statement users the information is presented in a similar manner, regardless of the organization issuing the financial statement. Let’s look at the standard conventions shown in the Cheesy Chuck’s income statement:

- The heading of the income statement includes three lines.

- The first line lists the business name.

- The middle line indicates the financial statement that is being presented (the report title).

- The last line indicates the time frame of the financial statement. Remember, the income statement is for a period of time (the month of June in our example).

- There are three columns.

- Going from left to right, the first column is the category heading or account (line labels).

- The second column is used to show detail amounts that will need to be summarized (expenses, in our example).

- The third column is a total (or summary) column. In this illustration, it is the column where subtotals are listed and net income is determined (subtracting Expenses from Revenues).

- A single underline beneath a value signals that adding or subtracting will be needed to get the next number. Final totals are indicated by a double underline. Notice the amount of Miscellaneous Expense ($300) is formatted with a single underline to indicate that a subtotal will follow. Similarly, the amount of “Net Income” ($5,800) is formatted with a double underline to indicate that it is the final value/total of the financial statement.

CONCEPTS IN PRACTICE

For the year ended December 31, 2016, McDonald’s had sales of $24.6 billion.1 The amount of sales is often used by the business as the starting point for planning the next year. No doubt, there are a lot of people involved in the planning for a business the size of McDonald’s. Two key people at McDonald’s are the purchasing manager and the sales manager (although they might have different titles). Let’s look at how McDonald’s 2016 sales amount might be used by each of these individuals. In each case, do not forget that McDonald’s is a global company.

A purchasing manager at McDonald’s, for example, is responsible for finding suppliers, negotiating costs, arranging for delivery, and many other functions necessary to have the ingredients ready for the stores to prepare the food for their customers. Expecting that McDonald’s will have over $24 billion of sales during 2017, how many eggs do you think the purchasing manager at McDonald’s would need to purchase for the year? According to the McDonald’s website, the company uses over two billion eggs a year.2 Take a moment to list the details that would have to be coordinated in order to purchase and deliver over two billion eggs to the many McDonald’s restaurants around the world.

A sales manager is responsible for establishing and attaining sales goals within the company. Assume that McDonald’s 2017 sales are expected to exceed the amount of sales in 2016. What conclusions would you make based on this information? What do you think might be influencing these amounts? What factors do you think would be important to the sales manager in deciding what action, if any, to take? Now assume that McDonald’s 2017 sales are expected to be below the 2016 sales level. What conclusions would you make based on this information? What do you think might be influencing these amounts? What factors do you think would be important to the sales manager in deciding what action, if any, to take?

Statement of Retained Earnings

Let’s create the statement of retained earnings for Cheesy Chuck’s for the month of June. Think of retained earnings as a pot where we combine 3 of the 4 things that affect equity. Equity (leftover assets) is increased when the business receives assets from owners (contributed capital) and when it earns (revenues). Equity is decreased when the business incurs expenses and when it distributes assets to owners (dividends). We will combine earnings, expenses, and distributions to owners (dividends) in the Retained Earnings pot. (Contributed capital — when the business receives assets from owners — is kept separate, but is still important!)

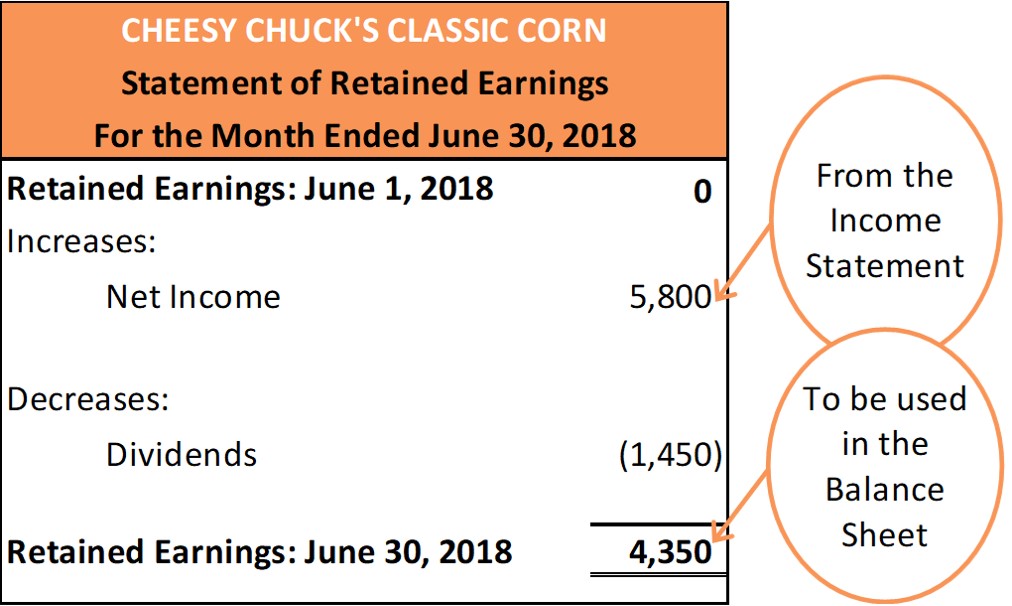

Retained earnings are the earnings (the revenues) that the business has left after expenses and dividends. First, we record the beginning balance in Retained Earnings — the amount in the pot at the beginning of the accounting period. See (Figure 4). We can see from the account balance list that the beginning balance in the Retained Earnings pot is zero. This should come as no surprise since Cheesy Chuck’s is a brand-new business.

Next, we dump in revenues and expenses, but keep in mind that while revenues increase Retained Earnings (equity), expenses decrease it. We could add the revenues and subtract the expenses, but we’ve already done that math . . . in the Income Statement. So we’ll take Net Income, $5,800, from the Income Statement and add it to our Retained Earnings pot. (If our Income Statement showed a Net Loss instead of Net Income, it would decrease our Retained Earnings when we tossed it into the pot and we’d subtract it.)

Next, we look at our list of account balances to see if there were Dividends which will decrease our Retained Earnings (equity). Remember that when we toss Dividends, $1,450, into the pot, our Retained Earnings decreases, so we’ll subtract to get the amount that’s left in the pot: $4,350 of retained earnings at the end of June.

Here is what happened to our Retained Earnings pot during June 2018:

Beginning Retained Earnings + Net Income – Distributions (Dividends) = Ending Retained Earnings

It is important to note that usually the beginning balance in the retained earnings pot will not be zero — this only happens when a business is brand new. Also, note that an organization will have either net income or net loss for the period, but not both. And this is a good time to recall the terminology used by accountants based on the legal structure of the particular business. If the business is organized as a corporation the distribution of assets to owners is called “dividends”. If the business is organized as a sole proprietorship or partnership, the distribution of assets to owners is called “withdrawals by owner” or “drawings by owner”. Regardless of the term used, any time a business distributes assets to owners, the equity of the business decreases.

(Figure 4) Statement of Retained Earnings for Cheesy Chuck’s Classic Corn. The statement of retained earnings demonstrates how much of the business’s earnings were retained over the period of time (the month of June in this case). Notice the amount of net income (or net loss) is brought from the income statement. In a similar manner, the ending retained earnings balance is carried forward to the balance sheet.

Notice the following about the statement of retained earnings for Cheesy Chuck’s:

- The format is similar to the format of the income statement (three lines for the heading).

- The statement follows a chronological order, starting with the first day of the month, accounting for the changes that occurred throughout the month, and ending with the final day of the month.

The statement uses the final number from the financial statement previously completed. In this case, the statement of retained earnings uses the net income (or net loss) amount from the income statement (Net Income, $5,800).

Balance Sheet

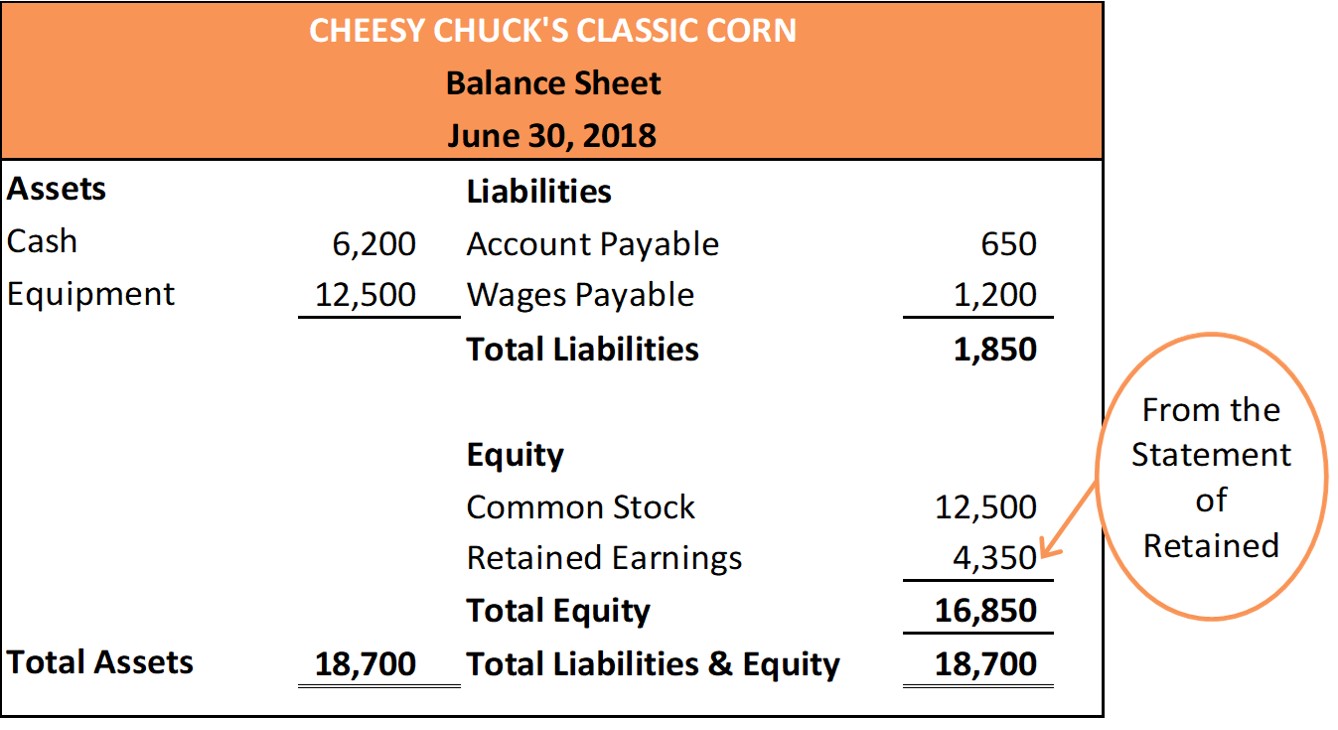

Let’s create a balance sheet for Cheesy Chuck’s for June 30. See (Figure 5). We’ll follow the basic accounting equation as we prepare the balance sheet. To begin, we look at the accounting records and determine what assets the business owns and the value of each. Cheesy Chuck’s has two assets: Cash ($6,200) and Equipment ($12,500). Adding the amount of assets gives a total asset value of $18,700.

Next, we determine the amount of money that Cheesy Chuck’s owes (liabilities). Cheesy Chuck’s has two liabilities. The first liability account listed in the records is Accounts Payable for $650. Accounts Payable is the amount that Cheesy Chuck’s must pay in the future to vendors (also called suppliers) for the ingredients to make the gourmet popcorn. The other liability is Wages Payable for $1,200. This is the amount that Cheesy Chuck’s must pay in the future to employees for work that has already been performed. Adding the two amounts gives us total liabilities of $1,850. (Here’s a hint as you develop your understanding of accounting: Liabilities often include the word “payable.” So, when you see “payable” in the account title, know these are amounts owed—liabilities.)

Finally, we determine the amount of equity the owner has in the business. Three of the four components of equity were combined in the statement of retained earnings (revenues, expenses, and dividends/distributions to owner) $4,350. The fourth component of equity is contributed capital (Common Stock) $12,500. So total equity is $16,850. Can you think of another way to confirm the amount of owner’s equity? Recall that equity is also called net assets (assets minus liabilities). If you take the total assets of Cheesy Chuck’s of $18,700 and subtract the total liabilities of $1,850, you get owner’s equity of $16,850.

(Figure 5) Balance Sheet for Cheesy Chuck’s Classic Corn. The balance sheet shows what the business owns (Assets), owes (Liabilities), and is worth (equity) on a given date. Notice the amount of Retained Earnings was brought forward from the statement of retained earnings.

Connecting the Income Statement and the Balance Sheet

Another way to think of the connection between the income statement and balance sheet (which is aided by the statement of retained earnings) is by using a sports analogy. The income statement summarizes the financial performance of the business for a given period of time. The income statement reports how the business performed financially each month—the firm earned either net income or net loss. This is similar to the outcome of a particular game—the team either won or lost.

The balance sheet summarizes the financial position of the business on a given date. Meaning, because of the financial performance over the past twelve months, for example, this is the financial position of the business as of December 31. Think of the balance sheet as being similar to a team’s overall win/loss record—to a certain extent a team’s strength can be perceived by its win/loss record.

However, because different companies have different sizes, you do not necessarily want to compare the balance sheets of two different companies. For example, you would not want to compare a local retail store with Walmart. In most cases you want to compare a company with its past balance sheet information.

Statement of Cash Flows

In Describe the Income Statement, Statement of Owner’s Equity, Balance Sheet, and Statement of Cash Flows, and How They Interrelate, we discussed the function of and the basic characteristics of the statement of cash flows. This fourth and final financial statement lists the cash inflows and cash outflows for the business for a period of time. It was created to fill in some informational gaps that existed in the other three statements (income statement, owner’s equity/retained earnings statement, and the balance sheet). A full demonstration of the creation of the statement of cash flows is presented in the Statement of Cash Flows chapter.

Creating Financial Statements: A Summary

Financial statements are reports that show how profitable a company has been and what it owns and owes. These reports are typically used by people both inside and outside of the company for decision-making. Here is a summary of the process we used to create the financial statements:

- Prepare the income statement

- Date shows the whole accounting period

- Revenues — Expenses = Net Inocme or (Net Loss)

- Shows how profitable (or unprofitable) the business was for the accounting period

- Prepare the statement of retained earnings

- Date shows the whole accounting period

- Beginning Retained Earnings + Net Income or – Net Loss – Dividends = Ending Retained Earnings

- Shows how Equity changed during the accounting period as a result of revenues, expenses, and dividends

- Prepare the balance sheet

- Date shows just the end of the accounting period

- Assets = Liabilities + Equity

- Shows what the business owns, owes and how much value is left for owners at the end of the accounting period

- Prepare the statement of cash flows

- Date shows the whole accounting period

- Sources of cash

- Uses of cash

- Shows where cash came from and how it was used during the accounting period

THINK IT THROUGH

In Why It Matters, we pointed out that accounting information from the financial statements can be useful to business owners. The financial statements provide feedback to the owners regarding the financial performance and financial position of the business, helping the owners to make decisions about the business.

Using the June financial statements, analyze Cheesy Chuck’s and prepare a brief presentation. Consider this from the perspective of the owner, Chuck. Describe the financial performance of and financial position of the business. What areas of the business would you want to analyze further to get additional information? What changes would you consider making to the business, if any, and why or why not?

ETHICAL CONSIDERATIONS

Accountants have an ethical duty to accurately report the financial results of their company and to ensure that the company’s annual reports communicate relevant information to stakeholders. If accountants and company management fail to do so, they may incur heavy penalties.

For example, in 2002 the Securities and Exchange Commission (SEC) charged the top management of Waste Management, Inc. with inflating profits by $1.7 billion to meet earnings targets in the period 1992–1997. An SEC press release alleged “that defendants fraudulently manipulated the company’s financial results to meet predetermined earnings targets. . . . They employed a multitude of improper accounting practices to achieve this objective.”3 The defendants in the case manipulated reports to defer or eliminate expenses, which fraudulently inflated their earnings. Because they failed to accurately report the financial results of their company, the top accountants and management of Waste Management, Inc. face charges.

Thomas C. Newkirk, the associate director of the SEC’s Division of Enforcement, stated, “For years, these defendants cooked the books, enriched themselves, preserved their jobs, and duped unsuspecting shareholders”4 The defendants, who included members of the company board and executives, benefited personally from their fraud in the millions of dollars through performance-based bonuses, charitable giving, and sale of company stock. The company’s accounting form, Arthur Andersen, abetted the fraud by identifying the improper practices but doing little to stop them.

IFRS CONNECTION

Understanding the elements that make up financial statements, the organization of those elements within the financial statements, and what information each statement relays is important, whether analyzing the financial statements of a US company or one from Honduras. Since most US companies apply generally accepted accounting principles (GAAP)5 as prescribed by the Financial Accounting Standards Board (FASB), and most international companies apply some version of the International Financial Reporting Standards (IFRS),6 knowing how these two sets of accounting standards are similar or different regarding the elements of the financial statements will facilitate analysis and decision-making.

Both IFRS and US GAAP have the same elements as components of financial statements: assets, liabilities, equity, income, and expenses. Equity, income, and expenses have similar subcategorization between the two types of GAAP (US GAAP and IFRS) as described. For example, income can be in the form of earned income (a lawyer providing legal services) or in the form of gains (interest earned on an investment account). The definition of each of these elements is similar between IFRS and US GAAP, but there are some differences that can influence the value of the account or the placement of the account on the financial statements. Many of these differences are discussed in detail later in this course when that element—for example, the nuances of accounting for liabilities—is discussed. Here is an example to illustrate how these minor differences in definition can impact placement within the financial statements when using US GAAP versus IFRS. ACME Car Rental Company typically rents its cars for a time of two years or 60,000 miles. At the end of whichever of these two measures occurs first, the cars are sold. Under both US GAAP and IFRS, the cars are noncurrent assets during the period when they are rented. Once the cars are being “held for sale,” under IFRS rules, the cars become current assets. However, under US GAAP, there is no specific rule as to where to list those “held for sale” cars; thus, they could still list the cars as noncurrent assets. As you learn more about the analysis of companies and financial information, this difference in placement on the financial statements will become more meaningful. At this point, simply know that financial analysis can include ratios, which is the comparison of two numbers, and thus any time you change the denominator or the numerator, the ratio result will change.

There are many similarities and some differences in the actual presentation of the various financial statements, but these are discussed in The Adjustment Process at which point these similarities and differences will be more meaningful and easier to follow.

KEY TAKEAWAYS

Key Concepts and Summary

- There are eight financial statement elements: revenues, expenses, assets, liabilities, equity, contributed capital (received assets from owners, dividends (distributions to owners), and retained earnings (combination of revenues, expenses, and dividends).

- There are standard conventions for the order of preparing financial statements (income statement, statement of retained earnings, balance sheet, and statement of cash flows) and for the format (three-line heading and columnar structure).

- Financial ratios, which are calculated using financial statement information, are often beneficial to aid in financial decision-making. Ratios allow for comparisons between businesses and determining trends between periods within the same business.

- Liquidity ratios assess the firm’s ability to convert assets into cash.

- Working Capital (Current Assets – Current Liabilities) is a liquidity ratio that measures a firm’s ability to meet current obligations.

- The Current Ratio (Current Assets/Current Liabilities) is similar to Working Capital but allows for comparisons between firms by determining the proportion of current assets to current liabilities.

Footnotes

- 1McDonald’s Corporation. U.S. Securities and Exchange Commission 10-K Filing. March 1, 2017. http://d18rn0p25nwr6d.cloudfront.net/CIK-0000063908/62200c2b-da82-4364-be92-79ed454e3b88.pdf

- 2McDonald’s. “Our Food. Your Questions. Breakfast.” n.d. https://www.mcdonalds.com/us/en-us/about-our-food/our-food-your-questions/breakfast.html

- 3U.S. Securities and Exchange Commission. “Waste Management Founder, Five Other Former Top Officers Sued for Massive Fraud.” March 26, 2002. https://www.sec.gov/news/headlines/wastemgmt6.htm

- 4U.S. Securities and Exchange Commission. “Waste Management Founder, Five Other Former Top Officers Sued for Massive Fraud.” March 26, 2002. https://www.sec.gov/news/headlines/wastemgmt6.htm

- 5Publicly traded companies in the United States must file their financial statements with the SEC, and those statements must be compiled using US GAAP. However, in some states, private companies can apply IFRS for SMEs (small and medium entities).

- 6The following site identifies which countries require IFRS, which use a modified version of IFRS, and which countries prohibit the use of IFRS. https://www.iasplus.com/en/resources/ifrs-topics/use-of-ifrs

Glossary

- accounting equation

- assets = liabilities + owner’s equity

- balance sheet

- financial statement that lists what the organization owns (assets), owes (liabilities), and is worth (equity) on a specific date

- elements of the financial statements

- categories or groupings used to record transactions and prepare financial statements

- income statement

- financial statement that measures the organization’s financial performance for a given period of time

- statement of cash flows

- financial statement listing the cash inflows and cash outflows for the business for a period of time

- statement of retained earnings

- financial statement for a corporation showing how the equity of the organization changed for a period of time as a result of revenues, expenses, and dividends (distributions to owners)

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

categories or groupings used to record transactions and prepare financial statements

financial statement that measures the organization’s financial performance for a given period of time

financial statement for a corporation showing how the equity of the organization changed for a period of time as a result of revenues, expenses, and dividends (distributions to owners)

financial statement that lists what the organization owns (assets), owes (liabilities), and is worth (equity) on a specific date

assets = liabilities + owner’s equity

financial statement listing the cash inflows and cash outflows for the business for a period of time