LO 3.6 Prepare a Trial Balance

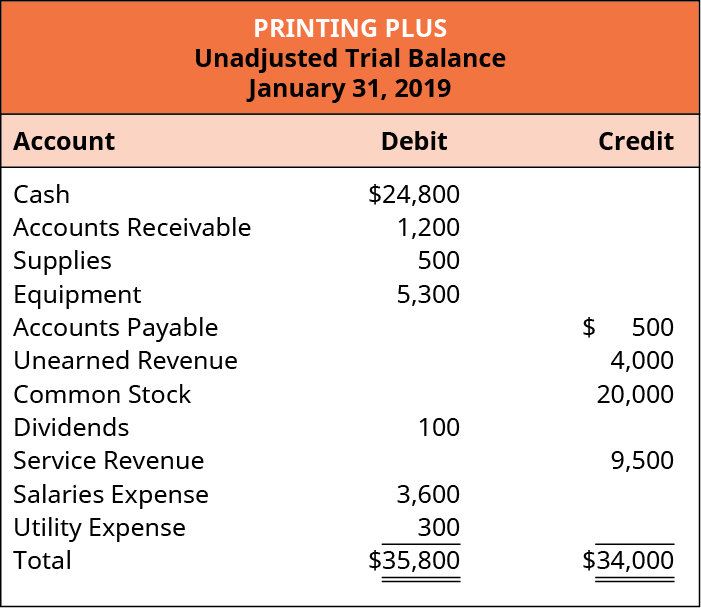

Once all the monthly transactions have been analyzed, journalized, and posted on a continuous day-to-day basis over the accounting period (a month in our example), we are ready to start working on preparing a trial balance (unadjusted). Preparing an unadjusted trial balance is the fourth step in the accounting cycle. A trial balance is a list of all accounts in the general ledger that have nonzero balances. A trial balance is an important step in the accounting process, because it helps identify any computational errors throughout the first three steps in the cycle.

Note that for this step, we are considering our trial balance to be unadjusted. The unadjusted trial balance in this section includes accounts before they have been adjusted. As you see in step 6 of the accounting cycle, we create another trial balance that is adjusted (see The Adjustment Process).

When constructing a trial balance, we must consider a few formatting rules, akin to those requirements for financial statements:

- The header must contain the name of the company, the label of a Trial Balance (Unadjusted), and the date.

- Accounts are listed in the accounting equation order with assets listed first followed by liabilities and finally equity.

- Amounts at the top of each debit and credit column should have a dollar sign.

- When amounts are added, the final figure in each column should be underscored.

- The totals at the end of the trial balance need to have dollar signs and be double-underscored.

Transferring information from T-accounts to the trial balance requires consideration of the final balance in each account. If the final balance in the ledger account (T-account) is a debit balance, you will record the total in the left column of the trial balance. If the final balance in the ledger account (T-account) is a credit balance, you will record the total in the right column.

Once all ledger accounts and their balances are recorded, the debit and credit columns on the trial balance are totaled to see if the figures in each column match each other. The final total in the debit column must be the same dollar amount that is determined in the final credit column. For example, if you determine that the final debit balance is $24,000 then the final credit balance in the trial balance must also be $24,000. If the two balances are not equal, there is a mistake in at least one of the columns.

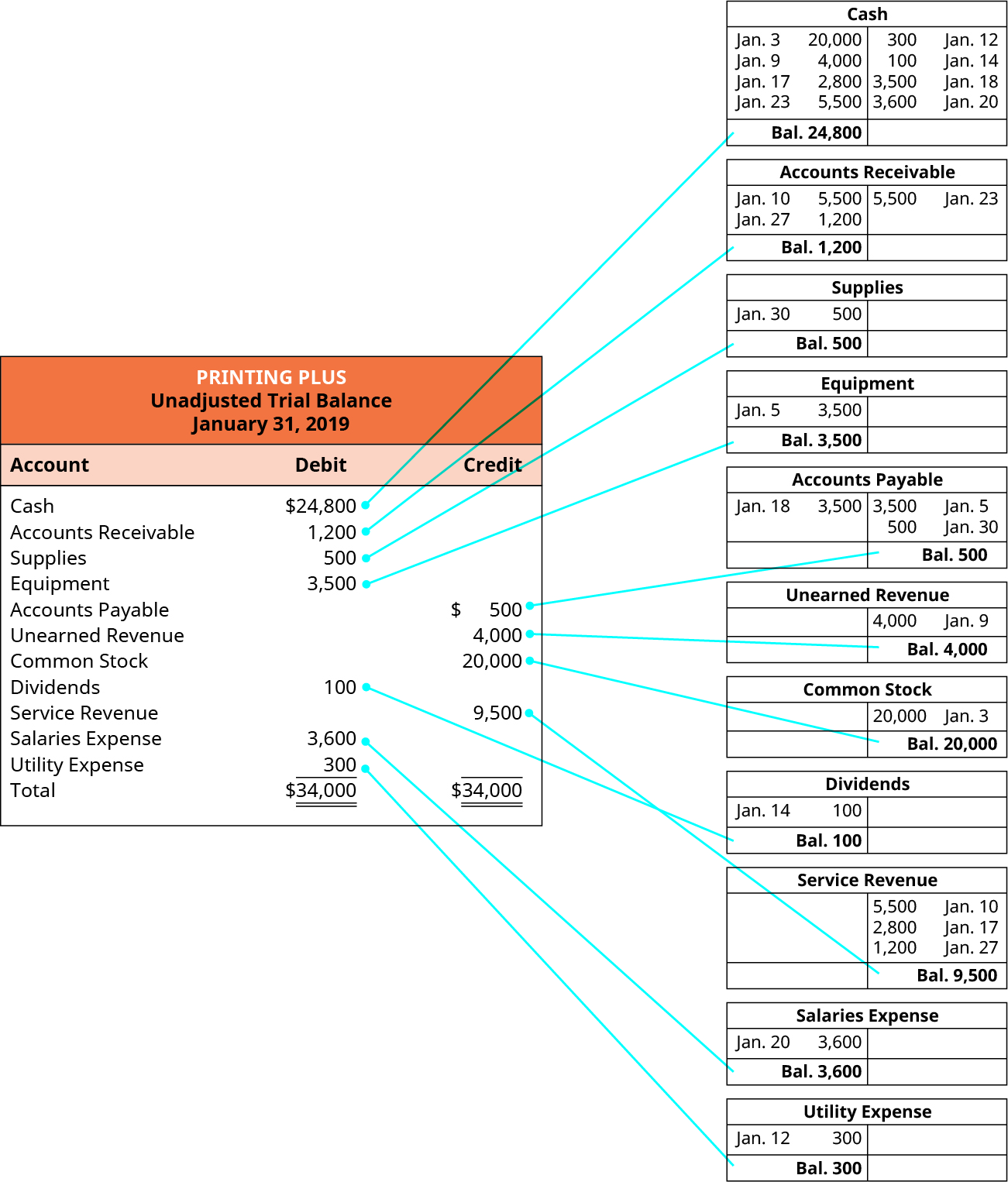

Let’s now take a look at the T-accounts and unadjusted trial balance for Printing Plus to see how the information is transferred from the T-accounts to the unadjusted trial balance.

For example, Cash has a final balance of $24,800 on the debit side. This balance is transferred to the Cash account in the debit column on the unadjusted trial balance. Accounts Receivable ($1,200), Supplies ($500), Equipment ($3,500), Dividends ($100), Salaries Expense ($3,600), and Utility Expense ($300) also have debit final balances in their T-accounts, so this information will be transferred to the debit column on the unadjusted trial balance. Accounts Payable ($500), Unearned Revenue ($4,000), Common Stock ($20,000) and Service Revenue ($9,500) all have credit final balances in their T-accounts. These credit balances would transfer to the credit column on the unadjusted trial balance.

Once all balances are transferred to the unadjusted trial balance, we will sum each of the debit and credit columns. The debit and credit columns both total $34,000, which means they are equal and in balance. However, just because the column totals are equal and in balance, we are still not guaranteed that a mistake is not present.

What happens if the columns are not equal?

CONCEPTS IN PRACTICE

One of the most well-known financial schemes is that involving the companies Enron Corporation and Arthur Andersen. Enron defrauded thousands by intentionally inflating revenues that did not exist. Arthur Andersen was the auditing firm in charge of independently verifying the accuracy of Enron’s financial statements and disclosures. This meant they would review statements to make sure they aligned with GAAP principles, assumptions, and concepts, among other things.

It has been alleged that Arthur Andersen was negligent in its dealings with Enron and contributed to the collapse of the company. Arthur Andersen was brought up on a charge of obstruction of justice for shredding important documents related to criminal actions by Enron. They were found guilty but had that conviction overturned. However, the damage was done, and the company’s reputation prevented it from operating as it had.1

Locating Errors

Sometimes errors may occur in the accounting process, and the trial balance can make those errors apparent when it does not balance.

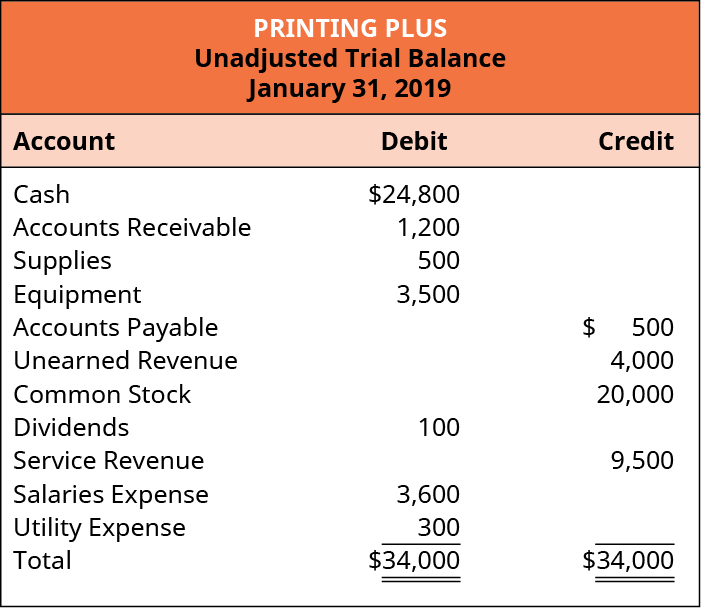

One way to find the error is to take the difference between the two totals and divide the difference by two. For example, let’s assume the following is the trial balance for Printing Plus.

You notice that the balances are not the same. Find the difference between the two totals: $34,100 – $33,900 = $200 difference. Now divide the difference by two: $200/2 = $100. Since the credit side has a higher total, look carefully at the numbers on the credit side to see if any of them are $100. The Dividends account has a $100 figure listed in the credit column. Dividends normally have a debit balance, but here it is a credit. Look back at the Dividends T-account to see if it was copied onto the trial balance incorrectly. If the answer is the same as the T-account, then trace it back to the journal entry to check for mistakes. You may discover in your investigation that you copied the number from the T-account incorrectly. Fix your error, and the debit total will go up $100 and the credit total down $100 so that they will both now be $34,000.

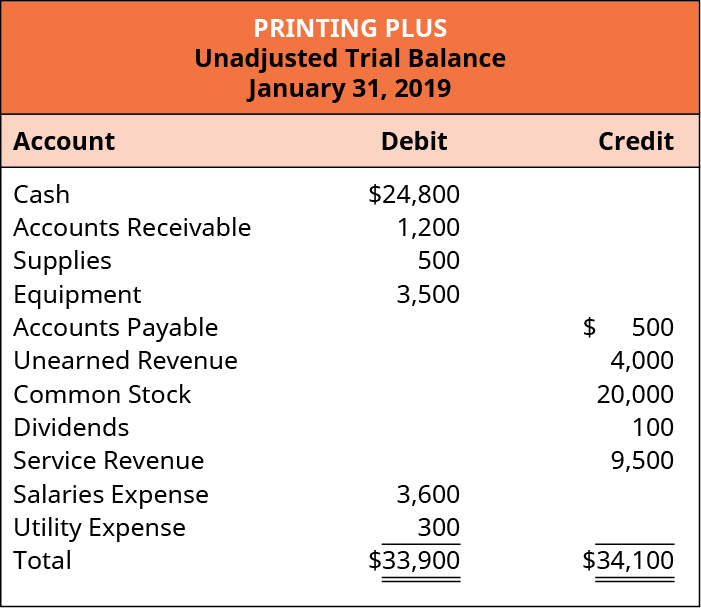

Another way to find an error is to take the difference between the two totals and divide by nine. If the outcome of the difference is a whole number, then you may have transposed a figure. For example, let’s assume the following is the trial balance for Printing Plus.

Find the difference between the two totals: $35,800 – 34,000 = $1,800 difference. This difference divided by nine is $200 ($1,800/9 = $200). Looking at the debit column, which has the higher total, we determine that the Equipment account had transposed figures. The account should be $3,500 and not $5,300. We transposed the three and the five.

What do you do if you have tried both methods and neither has worked? Unfortunately, you will have to go back through one step at a time until you find the error.

If a trial balance is in balance, does this mean that all of the numbers are correct? Not necessarily. We can have errors and still be mathematically in balance. It is important to go through each step very carefully and recheck your work often to avoid mistakes early on in the process.

After the unadjusted trial balance is prepared and it appears error-free, a company might look at its financial statements to get an idea of the company’s position before adjustments are made to certain accounts. A more complete picture of company position develops after adjustments occur, and an adjusted trial balance has been prepared. These next steps in the accounting cycle are covered in The Adjustment Process.

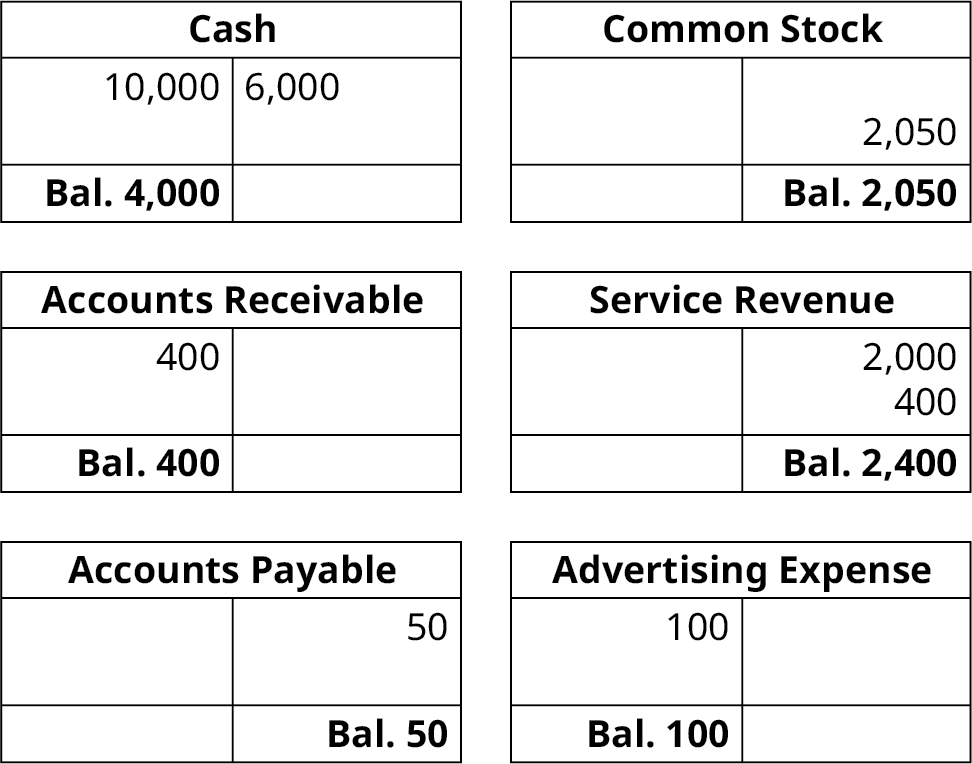

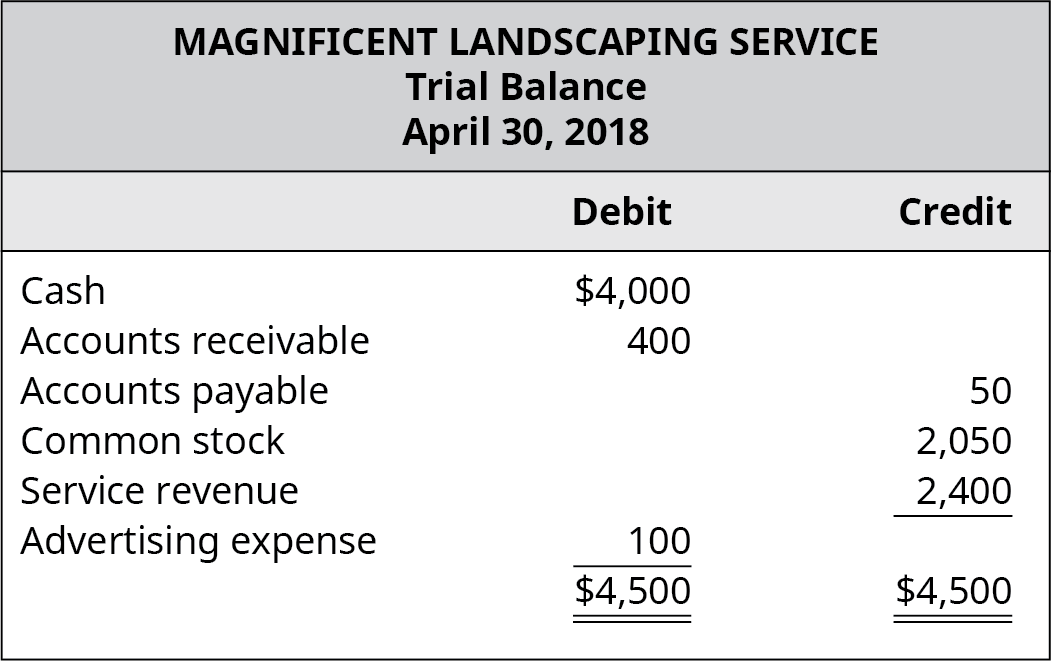

YOUR TURN

Complete the trial balance for Magnificent Landscaping Service using the following T-account final balance information for April 30, 2018.

Solution

THINK IT THROUGH

You own a small consulting business. Each month, you prepare a trial balance showing your company’s position. After preparing your trial balance this month, you discover that it does not balance. The debit column shows $2,000 more dollars than the credit column. You decide to investigate this error.

What methods could you use to find the error? What are the ramifications if you do not find and fix this error? How can you minimize these types of errors in the future?

KEY TAKEAWAYS

Key Concepts and Summary

- The trial balance contains a listing of all accounts in the general ledger with nonzero balances. Information is transferred from the T-accounts to the trial balance.

- Sometimes errors occur on the trial balance, and there are ways to find these errors. One may have to go through each step of the accounting process to locate an error on the trial balance.

Glossary

- trial balance

- list of all accounts in the general ledger that have nonzero balances

- unadjusted trial balance

- trial balance that includes accounts before they have been adjusted

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

list of all accounts in the general ledger

list of all accounts in the general ledger, before the adjusting entries have been posted for the accounting period