LO 6.4b — Analyze and Record Adjusting Entries for the Sale of Merchandise Using the Perpetual Inventory System

As you are now aware, accounting for selling merchandise can involve both the selling price and the cost of the merchandise sold, and sales discounts, returns, and allowances that stem from the original on-account or cash sales transaction. All of these factors contribute to the complexity of accounting for selling merchandise. Up to this point, we have assumed that all sales discounts, sales returns, and sales allowances occurred in the same year as the original sale. But of course this is not always the case in the real world. So we’ll need to make adjusting entries (requiring estimates) at the end of each year to ensure that the effects of the sales discounts, returns, and allowances are recorded in the same year as the original sale.

“Crossover” Sales-Related Transactions

Sales-related adjusting entries are necessitated by timing differences. For example, when a sale occurs in the current year, but the discount is enacted (taken by our customer) in the next year, we’ll need to make an adjusting entry to record the discount in the same year as the sale. When a sale is made in the current year, but we receive our merchandise back from our customer (a sales return) in the next year (or grant an allowance in the next year), we need to make an adjusting entry to record the sales return or allowance in the same year as the sale. We will refer to these transactions that require adjusting entries as “crossover” transactions. And, again, because we have to account for expected transactions before they occur, we’ll have to use estimates.

Timing Assumptions

To simplify our example, we will assume that the current year is 2028. So “next” year is 2029.

Overview of Adjusting Entries for Sales-Related Transactions

We will need three adjusting entries to ensure that sales discounts and sales returns are recorded in the same year as the original sale. (Good news! The adjusting entry for sales allowances is the same as one of the adjusting entries for sales returns.)

-

- Adjusting entry for crossover sales discounts

- Adjusting entry for crossover sales returns-revenue aspect (and sales allowances)

- Adjusting entry for crossover sales returns-cost aspect

Example: Adjusting entry for crossover sales discounts

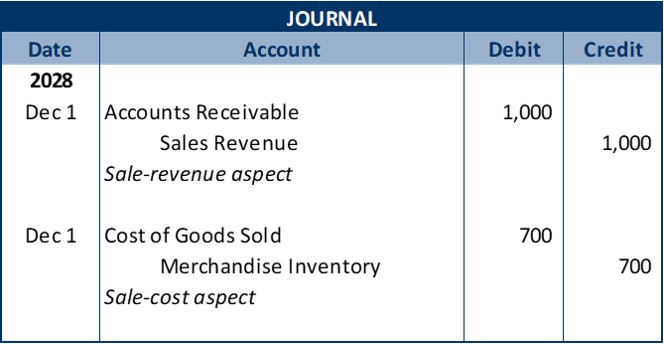

We’ll use ABC Inc. as our example, and assume that on December 1, 2028, we (ABC) sold merchandise for $1,000 to Fitness Center, terms 1/10, n/30. The merchandise cost us (ABC) $700. As you learned in the previous section, here are the entries we use to record both the revenue aspect and the cost aspect of the original sale:

XXXXX1

XXXXX1

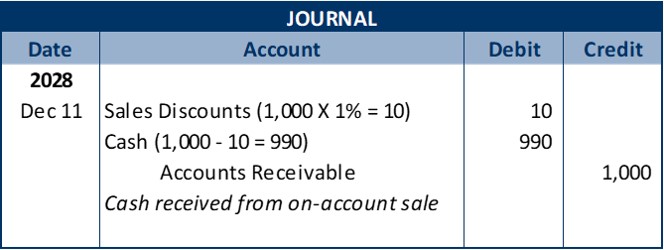

Then, if we assume that we received cash from Fitness Center on December 11, 2028, within the 10-day discount period, we would account for the cash and discount as follows:

XXXXX2

XXXXX2

BUT, what if we make the sale in 2028 and receive cash from Fitness Center in 2029?

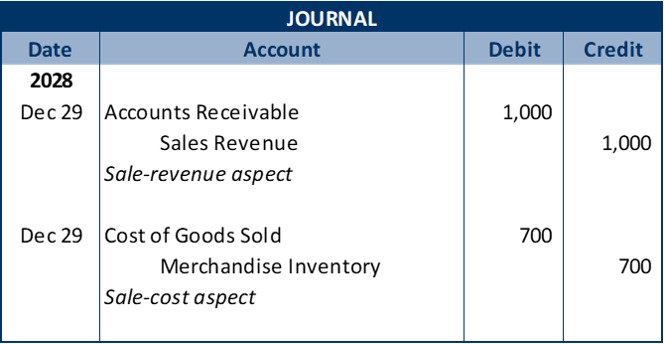

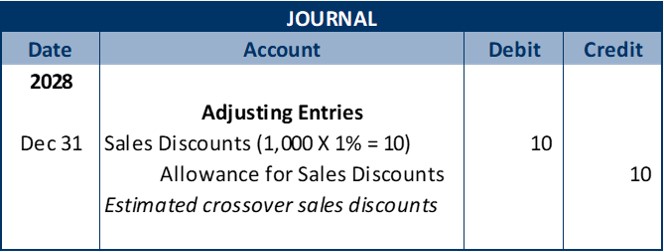

This time, we’ll assume that ABC made the sale to Fitness Center on December 29, 2028, still $1,000 selling price, terms 1/10, n/30 and ABC’s cost is still $700. So the only thing that changes in the original sale is the date. But in order to record the related sales discount, we’ll have to make an adjusting entry as of December 31, 2028.

XXXXX3

XXXXX3

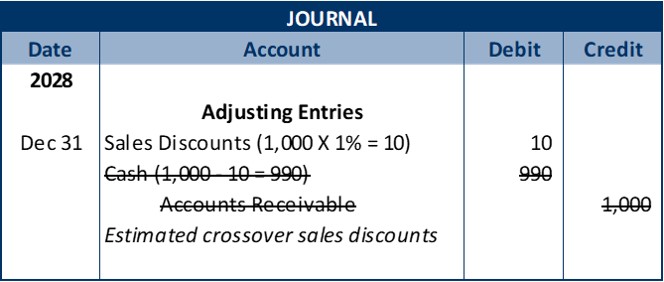

At the end of December 2028, we estimate the amount of sales discounts that will be taken in 2029, related to 2028 sales, and make an adjusting entry as of December 31, 2028. We still debit Sales Discounts — the whole point here is to record the sales discounts in 2028. But we cannot use the Cash account, because we have not received the cash, and we cannot use Accounts Receivable because our right to receive from Fitness Center has not changed as of December 31.

XXXXX4

XXXXX4

We need to indirectly decrease our accounts receivable for the amount of the sales discounts that Fitness Center will probably take. When we need to indirectly decrease an account, we use a contra account. In this case, since the account that we need to indirectly decrease is an asset, we’ll use a contra-asset account called Allowance for Sales Discounts. This contra-asset account will follow Accounts Receivable to the balance sheet, and the balance in the Allowance account will be subtracted from the balance in Accounts Receivable. (Remember that a contra-asset increases on the credit side, the opposite of regular assets, so we are increasing the Allowance for Sales Discounts account when we credit it.)

XXXXX5

XXXXX5

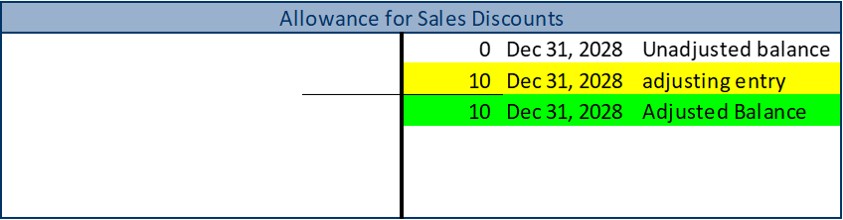

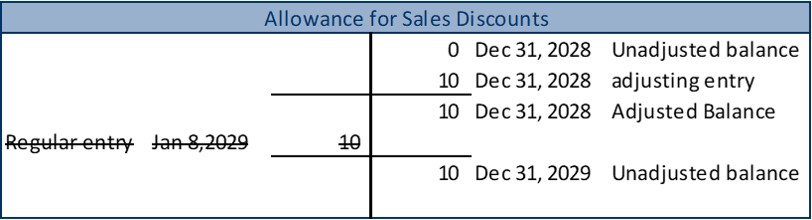

Here is the T-account for the Allowance for Sales Discounts. The account started with an unadjusted balance, of zero, then we post the $10 credit from our adjusting entry and get an adjusted credit balance as of December 31, 2028 of $10.

XXXXX6

XXXXX6

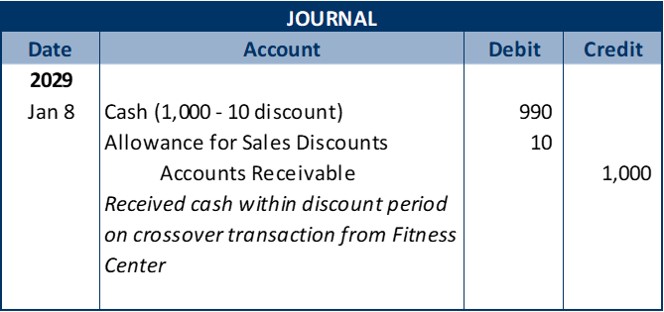

Then let’s assume that on January 8, 2029, Fitness Center sends us cash and takes the discount. We debit Cash and credit Accounts Receivable as usual. But instead of debiting Sales Discounts we debit (decrease) the Allowance for Sales Discounts. And we have accomplished our objective of recording the sales discount in 2028 when the sale occurred, even though the discount was actually enacted in 2029!

XXXXX7

XXXXX7

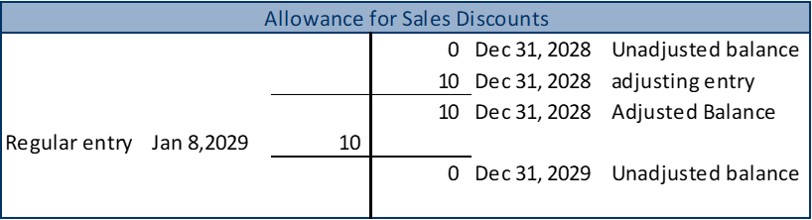

When we post this January 8, 2029 entry to our Allowance for Sales Discounts T-account, we are left with a zero balance. Since the Allowance account is only used for crossover transactions, we will not use the Allowance account again until we make the adjusting entry at the end of 2029.

XXXXX8

XXXXX8

BUT what if our estimated crossover sales discounts for 2028 are not exactly the same as actual crossover sales discounts enacted in 2029?

In fact, the odds are high that estimated and actual crossover sales discounts will not be equal. So let’s look at an example of what happens when we over-estimate 2028 crossover sales discounts.

We’ll still assume that we (ABC) made a sale on January 29, 2028, to Fitness Center for $1,000, terms 1/10, n/30. And our cost was $700. And we will still estimate that crossover sales discounts will be $10. So our regular and adjusting entries in 2028 remain unchanged:

XXXXX9

XXXXX9

XXXXX10

XXXXX10

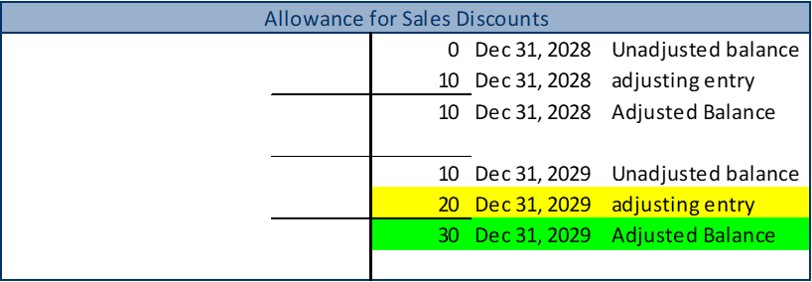

As before, we post the $10 credit to the Allowance for Sales Discounts T-account, and our adjusted balance as of December 31, 2028 is a credit of $10. But now let’s say that Fitness does not send us cash within the discount period, and instead pays us the full $1,000 on January 17, 2029. We debit cash and credit Accounts Receivable for the $1,000 and have no reason to touch the Allowance account. This means that the $10 credit balance sits in the Allowance account throughout 2029 and in fact is our December 31, 2029, unadjusted balance. (See T-account below.) As it turns out, we estimated more 2028 crossover sales discounts than we actually had in 2029, but no worries — we’ll compensate for our discrepancy when we do our estimation of crossover sales at the end of 2029.

XXXXX11

XXXXX11

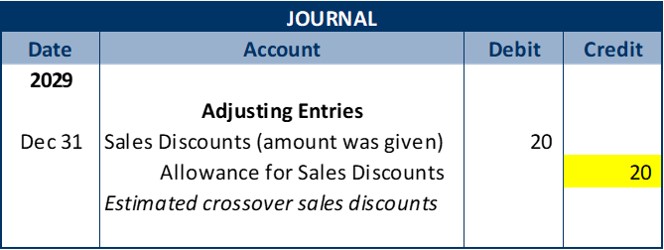

Fast forward to the end of 2029 . . . Once again ABC needs to estimate crossover sales discounts (discounts to be enacted in 2030, related to 2029 sales transactions). We (ABC) estimate that we’ll have $30 of crossover sales discounts related to 2029 sales transactions. You might be tempted to pop the $30 into the December 31, 2029 adjusting entry, but not so fast! Remember that we already have $10 in our Allowance account (from our over-estimate at the end of 2028). The $10 that’s already in the Allowance account means that we need to put just an additional $20 into the account with our adjusting entry to get the $30 balance that we need in the Allowance account.

XXXXX12

XXXXX12

XXXXX13

XXXXX13

To summarize, we need our estimated crossover sales discounts for 2029 ($30) to be the adjusted balance in the Allowance account. Since we already had a credit of $10 in the account our adjusting entry needs to put only $20 more (30 – 10 = 20) into the Allowance account. If we had underestimated crossover sales discounts for 2028, our Allowance account would have an unadjusted debit balance and we would add the underestimate to our 2029 estimate to get the amount for our December 31, 2029 adjusting entry.

You can use a 3-step approach to get the amount for the crossover sales discounts adjusting entry:

- Identify the unadjusted (current) balance in the Allowance for Sales Discounts account.

- Estimate crossover sales discounts related to current year sales transactions. (This is the adjusted “final” balance.)

- Calculate the amount that gets you from Step 1 to Step 2 — this is the amount for your adjusting entry.

XXXXX14

XXXXX14

This might be the first time you’ve encountered a situation where you know what the final balance needs to be, before you know how much the adjusting entry needs to be, but it will almost certainly not be the last time. Like anything else, the more you do it, the easier it gets.

Adjusting entry for crossover sales returns-revenue aspect and cost aspect

Accounting for crossover sales returns requires two adjusting entries — one for the revenue aspect and one for the cost aspect. But it is easier to make both adjusting entries together, so we’ll work through examples of both adjustments in this section. We’ll continue to use ABC Inc. as our example, and assume that on December 1, 2028, we (ABC) sold merchandise for $1,000 to Fitness Center, terms 1/10, n/30. The merchandise cost us (ABC) $700. Once again, here are the entries to record both the revenue aspect and cost aspect of the sale.

XXXXX15

XXXXX15

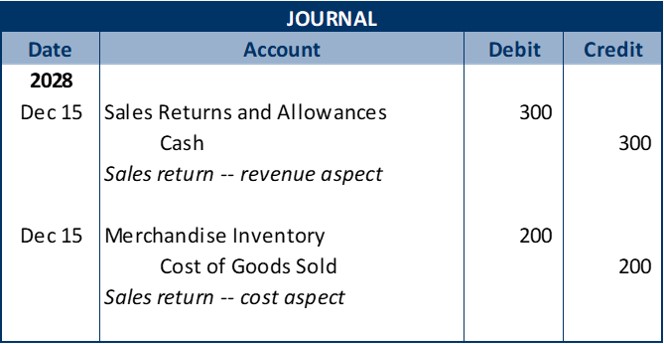

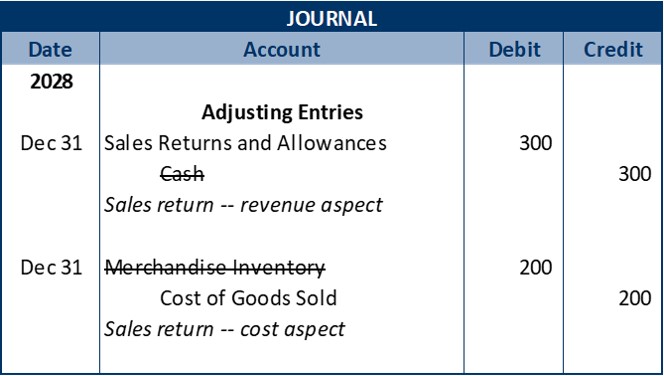

Next, we’ll assume that on December 15, 2028, Fitness Center returns some of the merchandise to us — merchandise that we sold for $300 (and that cost us, ABC, $200). As usual, we debit (increase) Sales Returns and Allowances and credit cash for the selling price, $300. And we debit (increase) Merchandise Inventory and credit (decrease) Cost of Goods Sold for the cost, $200.

XXXXX16

XXXXX16

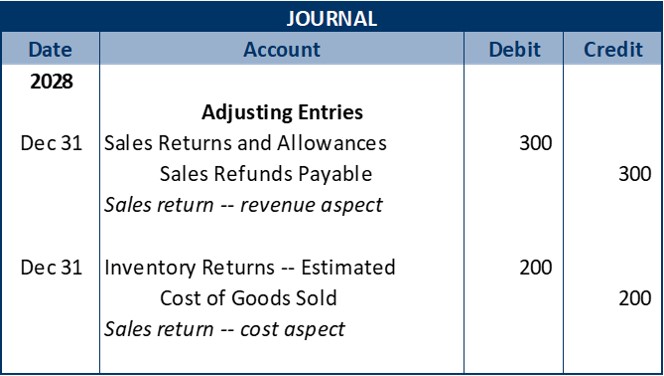

BUT, what if the return happened on January 25, 2029?

Since the sale occurred in 2028, and we need to record the related return in 2028, we’ll need to make an adjusting entry using our estimate of crossover returns for 2028 sales. We’ll still debit Sales Returns and Allowances for $300 and credit Cost of Goods Sold for $200 (in their respective adjusting entries). After all, recording in 2028 the revenue and cost aspects of the sales returns is the whole point of these adjusting entries. But we cannot use Cash or Merchandise Inventory since we have not actually paid any cash or received any merchandise by December 31, 2028.

XXXXX17

XXXXX17

So instead of crediting Cash, we’ll credit a liability account called Sales Refunds Payable to show that we owe the estimated $300 to customers for the crossover sales returns. Since Sales Refunds Payable is a regular liability account, we are increasing it when we record the credit of $300.

And since we cannot directly increase Merchandise Inventory until we actually get our merchandise back from Fitness Center, we have to indirectly increase inventory. When we need to indirectly decrease an account, we use a contra account. But when we need to indirectly increase an account, we use a second account of the same type. Since Merchandises Inventory is an asset, we’ll use another asset account, Inventory Returns -- Estimated.

XXXXX18

XXXXX18

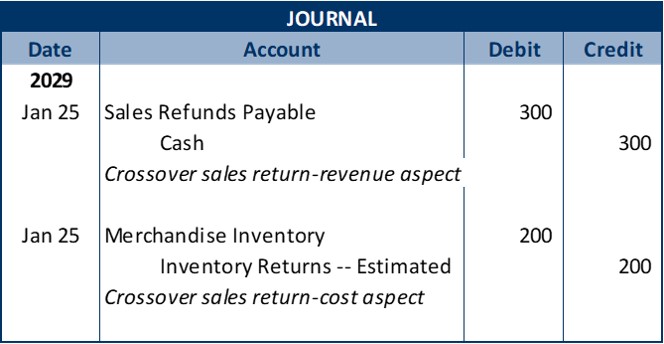

Then on January 25, 2029, when we (ABC) actually receive the merchandise back from Fitness Center, we debit (decrease) Sales Refunds Payable and credit Cash as we actually pay the refund to Fitness Center. And we debit (increase) Merchandise Inventory as we put the merchandise back on our shelves and credit (decrease) Inventory Returns — Estimated, since we can now record the actual crossover sales return.

XXXXX19

XXXXX19

BUT what if our estimated crossover sales returns for 2028 are not exactly the same as actual crossover sales returns enacted in 2029?

In fact, it is likely that our estimate will differ from actual crossover returns. Let’s look at an example of what happens when we overestimate 2028 crossover sales returns. We’ll continue to use the original sale to Fitness Center on December 1, and we’ll stick with the estimates in our December 31, 2028, adjusting entry. But now we will assume that we never received a sales return from Fitness Center. Here is what our Sales Refunds Payable and Inventory Returns — Estimated T-accounts look like so far.

XXXXX20

XXXXX20

Since we received no crossover sales returns in 2029, the 300$ is still in the Sales Refunds Payable account and the $200 is still in the Inventory Returns — Estimated account — in 2028, we overestimated crossover sales returns. But no worries, we will compensate for our discrepancy when we make our estimate for 2029 crossover sales returns.

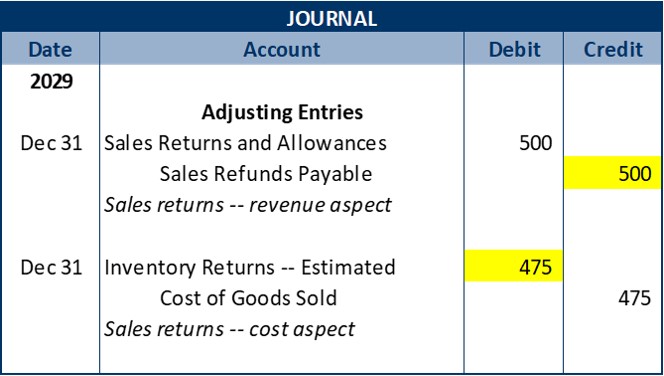

Fast forward to the end of 2029 . . . Once again ABC needs to estimate crossover sales returns (returns to be enacted in 2030, related to 2029 sales transactions). We (ABC) estimate that we’ll have $800 of crossover sales returns in 2030 related to 2029 sales transactions. We estimate that the cost of the merchandise that will be returned to us is $675. You might be tempted to pop the $800 and $675 into the December 31, 2029 adjusting entries but not so fast! Remember that we already have $300 in our Sales Refunds Payable account and $200 in our Inventory Returns — Estimated account (from our over-estimate at the end of 2028).

The $300 that’s already in the Sales Refunds Payable account means that we need to put just an additional $500 (800 – 300 = 500) into the account with our adjusting entry to get the $800 balance that we need in the Sales Refunds Payable account. And the $200 that’s already in the Inventory Returns — Estimated account means that we need to put just an additional $475 (675 -200 = 475) into the account to get the $675 balance that we need in the Inventory Returns — Estimated account.

In our “Adjusting entry for crossover sales discounts” example, we outlined a 3-step approach for getting the amount for the sales-related adjusting entries. The same 3 steps work here and are marked in the T-accounts below:

- Identify the unadjusted (current) balance in the account.

- Estimate crossover sales returns (revenue aspect and cost aspect) related to current year sales transactions. (This is the adjusted “final” balance.)

- Calculate the amount that gets you from Step 1 to Step 2 — this is the amount for your adjusting entry.

XXXXX21

XXXXX21

And here are the 2029 adjusting entries reflecting the amounts calculated above:

XXXXX22

XXXXX22

Note: If it had turned out that we underestimated crossover sales returns in the prior year, we would add the amount of the underestimate to our estimate for the current year to get the amount for our adjusting entry.

Another note: The adjusting entry for crossover sales allowances is the same as the revenue aspect of sales returns.

Glossary

- Allowance for Sales Discounts

- A contra-asset account used to indirectly decrease Accounts Receivable for “crossover” sales discounts — sales discounts enacted in the year after the original sales transaction occurred.

- Inventory Returns — Estimated

- an asset account used to indirectly increase Merchandise Inventory for crossover Sales Returns

- Sales Refunds Payable

- a liability account used for the revenue aspect of crossover sales returns (in place of decreasing Cash or Accounts Receivable)

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

A contra-asset account used to indirectly decrease Accounts Receivable for "crossover" sales discounts -- sales discounts enacted in the year after the original sales transaction occurred.

a liability account used for the revenue aspect of crossover sales returns (in place of decreasing Cash or Accounts Receivable)

an asset account used to indirectly increase Merchandise Inventory for crossover Sales Returns