LO 9.1 Explain the Revenue Recognition Principle and How It Relates to Current and Future Sales and Purchase Transactions

You own a small clothing store and offer your customers cash, credit card, or in-house credit payment options. Many of your customers choose to pay with a credit card or charge the purchase to their in-house credit accounts. This means that your store is owed money in the future from either the customer or the credit card company, depending on payment method. Regardless of credit payment method, your company must decide when to recognize revenue. Do you recognize revenue when the sale occurs or when cash payment is received? When do you recognize the expenses associated with the sale? How are these transactions recognized?

Accounting Principles and Assumptions Regulating Revenue Recognition

Revenue and expense recognition timing is critical to transparent financial presentation. GAAP governs recognition for publicly traded companies. Even though GAAP is required only for public companies, to display their financial position most accurately, private companies should manage their financial accounting using its rules. Two principles governed by GAAP are the revenue recognition principle and the matching principle. Both the revenue recognition principle and the matching principle give specific direction on revenue and expense reporting.

The revenue recognition principle, which states that companies must recognize revenue in the period in which it is earned, instructs companies to recognize revenue when a four-step process is completed. This may not necessarily be when cash is collected. Revenue can be recognized when all of the following criteria have been met:

- There is credible evidence that an arrangement exists.

- Goods have been delivered or services have been performed.

- The selling price or fee to the buyer is fixed or can be reasonably determined.

- There is reasonable assurance that the amount owed to the seller is collectible.

The accrual accounting method aligns with this principle, and it records transactions related to revenue earnings as they occur, not when cash is collected. The revenue recognition principle may be updated periodically to reflect more current rules for reporting.

For example, a landscaping company signs a $600 contract with a customer to provide landscaping services for the next six months (assume the landscaping workload is distributed evenly throughout the six months). The customer sets up an in-house credit line with the company, to be paid in full at the end of the six months. The landscaping company records revenue earnings each month and provides service as planned. To align with the revenue recognition principle, the landscaping company will record one month of revenue ($100) each month as earned; they provided service for that month, even though the customer has not yet paid cash for the service.

Let’s say that the landscaping company also sells gardening equipment. It sells a package of gardening equipment to a customer who pays on credit. The landscaping company will recognize revenue immediately, given that they provided the customer with the gardening equipment (product), even though the customer has not yet paid cash for the product.

Accrual accounting also incorporates the matching principle (otherwise known as the expense recognition principle), which instructs companies to record expenses related to revenue generation in the period in which they are incurred. The principle also requires that any expense not directly related to revenues be reported in an appropriate manner. For example, assume that a company paid $6,000 in annual real estate taxes. The principle has determined that costs cannot effectively be allocated based on an individual month’s sales; instead, it treats the expense as a period cost. In this case, it is going to record 1/12 of the annual expense as a monthly period cost. Overall, the “matching” of expenses to revenues projects a more accurate representation of company financials. When this matching is not possible, then the expenses will be treated as period costs.

For example, when the landscaping company sells the gardening equipment, there are costs associated with that sale, such as the costs of materials purchased or shipping charges. The cost is reported in the same period as revenue associated with the sale. There cannot be a mismatch in reporting expenses and revenues; otherwise, financial statements are presented unfairly to stakeholders. Misreporting has a significant impact on company stakeholders. If the company delayed reporting revenues until a future period, net income would be understated in the current period. If expenses were delayed until a future period, net income would be overstated.

Let’s turn to the basic elements of accounts receivable, as well as the corresponding transaction journal entries.

ETHICAL CONSIDERATIONS

Because each industry typically has a different method for recognizing income, revenue recognition is one of the most difficult tasks for accountants, as it involves a number of ethical dilemmas related to income reporting. To provide an industry-wide approach, Accounting Standards Update No. 2014-09 and other related updates were implemented to clarify revenue recognition rules. The American Institute of Certified Public Accountants (AICPA) announced that these updates would replace U.S. GAAP’s current industry-specific revenue recognition practices with a principle-based approach, potentially affecting both day-to-day business accounting and the execution of business contracts with customers.1 The AICPA and the International Federation of Accountants (IFAC) require professional accountants to act with due care and to remain abreast of new accounting rules and methods of accounting for different transactions, including revenue recognition.

The IFAC emphasizes the role of professional accountants working within a business in ensuring the quality of financial reporting: “Management is responsible for the financial information produced by the company. As such, professional accountants in businesses therefore have the task of defending the quality of financial reporting right at the source where the numbers and figures are produced!”2 In accordance with proper revenue recognition, accountants do not recognize revenue before it is earned.

CONCEPTS IN PRACTICE

Gift cards have become an essential part of revenue generation and growth for many businesses. Although they are practical for consumers and low cost to businesses, navigating revenue recognition guidelines can be difficult. Gift cards with expiration dates require that revenue recognition be delayed until customer use or expiration. However, most gift cards now have no expiration date. So, when do you recognize revenue?

Companies may need to provide an estimation of projected gift card revenue and usage during a period based on past experience or industry standards. There are a few rules governing reporting. If the company determines that a portion of all of the issued gift cards will never be used, they may write this off to income. In some states, if a gift card remains unused, in part or in full, the unused portion of the card is transferred to the state government. It is considered unclaimed property for the customer, meaning that the company cannot keep these funds as revenue because, in this case, they have reverted to the state government.

Short-Term Revenue Recognition Examples

As mentioned, the revenue recognition principle requires that, in some instances, revenue is recognized before receiving a cash payment. In these situations, the customer still owes the company money. This money owed to the company is a type of receivable for the company and a payable for the company’s customer.

A receivable is an outstanding amount owed from a customer. One specific receivable type is called accounts receivable. Accounts receivable is an outstanding customer debt on a credit sale. The company expects to receive payment on accounts receivable within the company’s operating period (less than a year). Accounts receivable is considered an asset, and it typically does not include an interest payment from the customer. Some view this account as extending a line of credit to a customer. The customer would then be sent an invoice with credit payment terms. If the company has provided the product or service at the time of credit extension, revenue would also be recognized.

For example, Billie’s Watercraft Warehouse (BWW) sells various watercraft vehicles. They extend a credit line to customers purchasing vehicles in bulk. A customer bought 10 Jet Skis on credit at a sales price of $100,000. The cost of the sale to BWW is $70,000. The following journal entries occur.

Accounts Receivable increases (debit) and Sales Revenue increases (credit) for $100,000. Accounts Receivable recognizes the amount owed from the customer, but not yet paid. Revenue recognition occurs because BWW provided the Jet Skis and completed the earnings process. Cost of Goods Sold increases (debit) and Merchandise Inventory decreases (credit) for $70,000, the expense associated with the sale. By recording both a sale and its related cost entry, the matching principle requirement is met.

When the customer pays the amount owed, the following journal entry occurs.

Cash increases (debit) and Accounts Receivable decreases (credit) for the full amount owed. If the customer made only a partial payment, the entry would reflect the amount of the payment. For example, if the customer paid only $75,000 of the $100,000 owed, the following entry would occur. The remaining $25,000 owed would remain outstanding, reflected in Accounts Receivable.

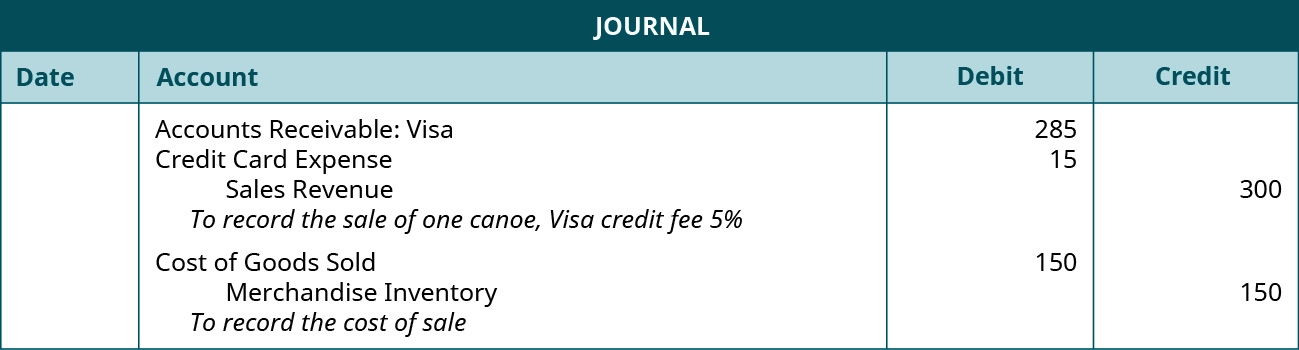

Another credit transaction that requires recognition is when a customer pays with a credit card (Visa and MasterCard, for example). This is different from credit extended directly to the customer from the company. In this case, the third-party credit card company accepts the payment responsibility. This reduces the risk of nonpayment, increases opportunities for sales, and expedites payment on accounts receivable. The tradeoff for the company receiving these benefits from the credit card company is that a fee is charged to use this service. The fee can be a flat figure per transaction, or it can be a percentage of the sales price. Using BWW as the example, let’s say one of its customers purchased a canoe for $300, using his or her Visa credit card. The cost to BWW for the canoe is $150. Visa charges BWW a service fee equal to 5% of the sales price. At the time of sale, the following journal entries are recorded.

Accounts Receivable: Visa increases (debit) for the sale amount ($300) less the credit card fee ($15), for a $285 Accounts Receivable balance due from Visa. BWW’s Credit Card Expense increases (debit) for the amount of the credit card fee ($15; 300 × 5%), and Sales Revenue increases (credit) for the original sales amount ($300). BWW recognizes revenue as earned for this transaction because it provided the canoe and completed the earnings process. Cost of Goods Sold increases (debit) and Merchandise Inventory decreases (credit) for $150, the expense associated with the sale. As with the previous example, by recording both a sale and cost entry, the matching principle requirement is met. When Visa pays the amount owed to BWW, the following entry occurs in BWW’s records.

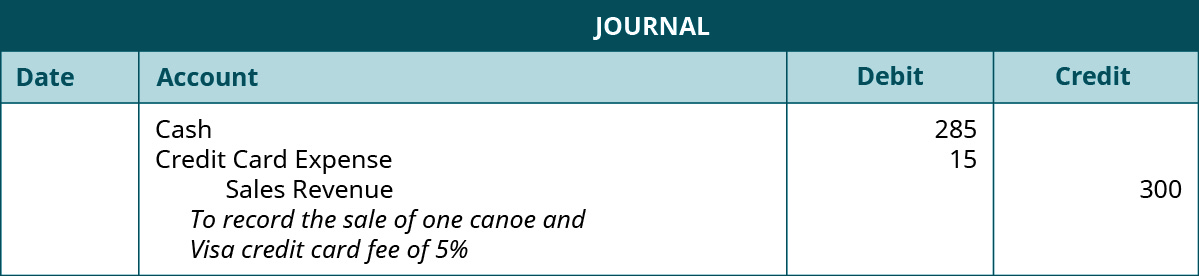

Cash increases (debit) and Accounts Receivable: Visa decreases (credit) for the full amount owed, less the credit card fee. Once BWW receives the cash payment from Visa, it may use those funds in other business activities.

An alternative to the journal entries shown is that the credit card company, in this case Visa, gives the merchant immediate credit in its cash account for the $285 due the merchant, without creating an account receivable. If that policy were in effect for this transaction, the following single journal entry would replace the prior two journal entry transactions. In the immediate cash payment method, an account receivable would not need to be recorded and then collected. The separate journal entry—to record the costs of goods sold and to reduce the canoe inventory that reflects the $150 cost of the sale—would still be the same.

Here’s a final credit transaction to consider. A company allows a sales discount on a purchase if a customer charges a purchase but makes the payment within a stated period of time, such as 10 or 15 days from the point of sale. In such a situation, a customer would see credit terms in the following form: 2/10, n/30. This particular example shows that a customer who pays his or her account within 10 days will receive a 2% discount. Otherwise, the customer will have 30 days from the date of the purchase to pay in full, but will not receive a discount. Both sales discounts and purchase discounts were addressed in detail in Merchandising Transactions.

YOUR TURN

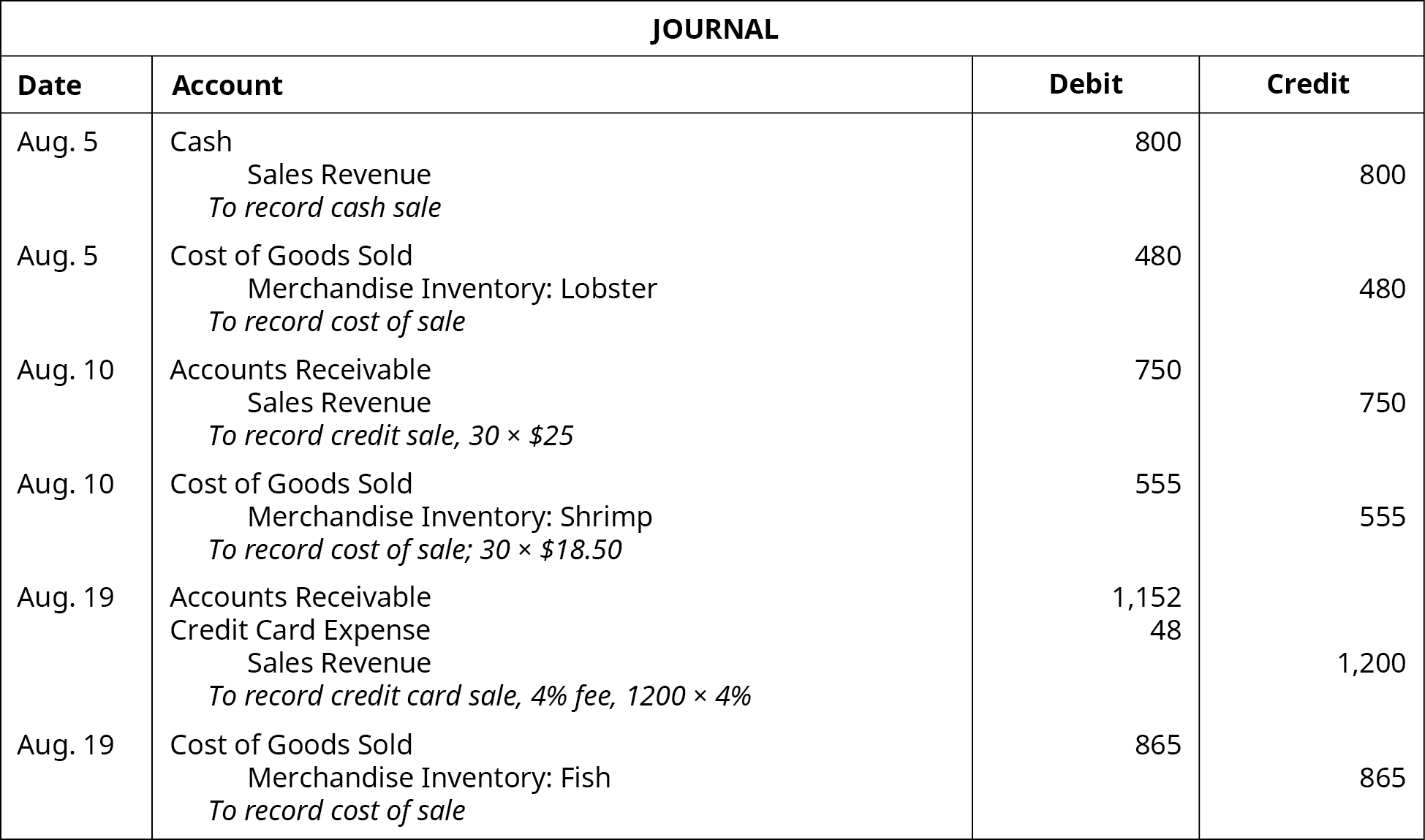

Maine Lobster Market (MLM) provides fresh seafood products to customers. It allows customers to pay with cash, an in-house credit account, or a credit card. The credit card company charges Maine Lobster Market a 4% fee, based on credit sales using its card. From the following transactions, prepare journal entries for Maine Lobster Market.

| Aug. 5 | Pat paid $800 cash for lobster. The cost to MLM was $480. |

| Aug. 10 | Pat purchased 30 pounds of shrimp at a sales price per pound of $25. The cost to MLM was $18.50 per pound and is charged to Pat’s in-store account. |

| Aug. 19 | Pat purchased $1,200 of fish with a credit card. The cost to MLM is $865. |

Solution

YOUR TURN

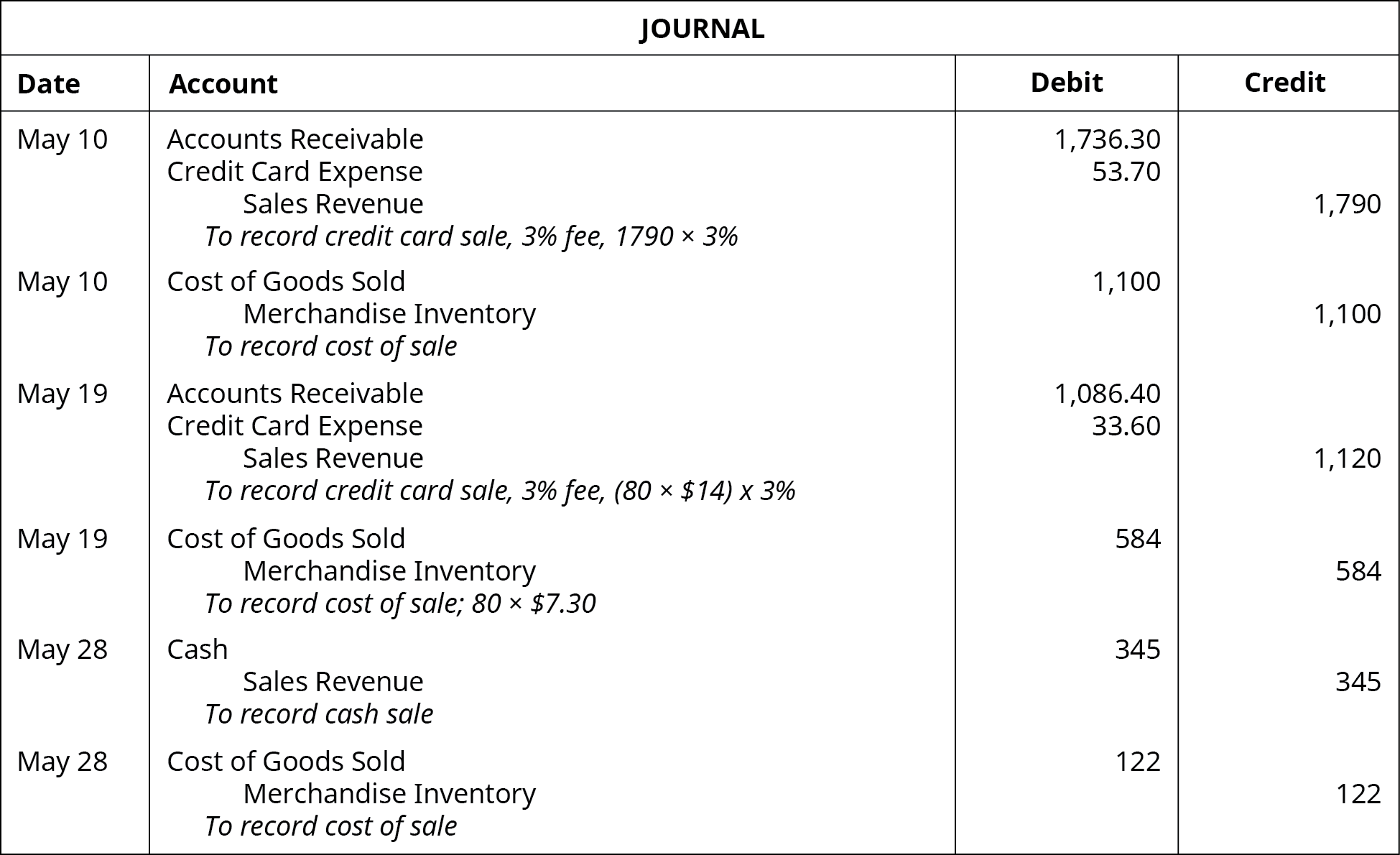

Jamal’s Music Supply allows customers to pay with cash or a credit card. The credit card company charges Jamal’s Music Supply a 3% fee, based on credit sales using its card. From the following transactions, prepare journal entries for Jamal’s Music Supply.

| May 10 | Kerry paid $1,790 for music supplies with a credit card. The cost to Jamal’s Music Supply was $1,100. |

| May 19 | Kerry purchased 80 drumstick pairs at a sales price per pair of $14 with a credit card. The cost to Jamal’s Music Supply was $7.30 per pair. |

| May 28 | Kerry purchased $345 of music supplies with cash. The cost to Jamal’s Music Supply was $122. |

Solution

KEY TAKEAWAYS

Key Concepts and Summary

- According to the revenue recognition principle, a company will recognize revenue when a product or service is provided to a client. The revenue must be reported in the period when the earnings process completes.

- According to the matching principle, expenses must be matched with revenues in the period in which they are incurred. A mismatch in revenues and expenses can lead to financial statement misreporting.

- When a customer pays for a product or service on a line of credit, the Accounts Receivable account is used. Accounts receivable must satisfy the following criteria: the customer owes money and has yet to pay, the amount is due in less than a company’s operating cycle, and the account usually does not incur interest.

- When a customer purchases a product or service on credit, using an in-house account, Accounts Receivable increases and Sales Revenue increases. When the customer pays the amount due, Accounts Receivable decreases and Cash increases.

- When a customer purchases a product or service with a third-party credit card, such as Visa, Accounts Receivable increases, Credit Card Expense increases, and Sales Revenue increases. When the credit card company pays the amount due, Accounts Receivable decreases and Cash increases for the original sales price less the credit card usage fee.

Glossary

- accounts receivable

- categories or groupings used to record transactions and prepare financial statements

- accrual accounting

- records transactions related to revenue earnings as they occur, not when cash is collected

- GAAP

- (also known as Generally Accepted Accounting Principles) the concepts, standards, and rules established by the Financial Accounting Standards Board (FASB) that guide the preparation and presentation of financial statements

- matching principle

- (also, expense recognition principle) records expenses related to revenue generation in the period in which they are incurred

- receivable

- outstanding amount owed from a customer

- revenue recognition principle

- principle stating that company must recognize revenue in the period in which it is earned; it is not considered earned until a product or service has been provided

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

(Generally Accepted Accounting Principles) common set of rules, standards, and procedures that publicly traded companies must follow when composing their financial statements

principle stating that company must recognize revenue in the period in which it is earned; it is not considered earned until a product or service has been provided

records transactions related to revenue earnings as they occur, not when cash is collected

(also, expense recognition principle) records expenses related to revenue generation in the period in which they are incurred

outstanding amount owed from a customer

outstanding customer debt on a credit sale, typically receivable within a short time period