LO 9.6 Explain How Notes Receivable and Accounts Receivable Differ

So far, our discussion of receivables has focused solely on accounts receivable. Companies, however, can expand their business models to include more than one type of receivable. This receivable expansion allows a company to attract a more diverse clientele and increase asset potential to further grow the business.

As you’ve learned, accounts receivable is typically a more informal arrangement between a company and customer that is resolved within a year and does not include interest payments. In contrast, notes receivable (an asset) is a more formal legal contract between the buyer and the company, which requires a specific payment amount at a predetermined future date. The length of contract is typically over a year, or beyond one operating cycle. There is also generally an interest requirement because the financial loan amount may be larger than accounts receivable, and the length of contract is possibly longer. A note can be requested or extended in exchange for products and services or in exchange for cash (usually in the case of a financial lender). Several characteristics of notes receivable further define the contract elements and scope of use.

| Key Feature Comparison of Accounts Receivable and Notes Receivable | |

|---|---|

| Accounts Receivable | Notes Receivable |

|

|

THINK IT THROUGH

You are the owner of a retail health food store and have several large companies with whom you do business. Many competitors in your industry are vying for your customers’ business. For each sale, you issue a notes receivable to the company, with an interest rate of 10% and a maturity date 18 months after the issue date. Each note has a minimum principal amount of $500,000.

Let’s say one of these companies is unable to pay in the established timeframe and dishonors the note. What would you do? How does this dishonored note affect your company both financially and nonfinancially? If your customer wanted to renegotiate the terms of the agreement, would you agree? If so, what would be the terms?

Characteristics of Notes Receivable

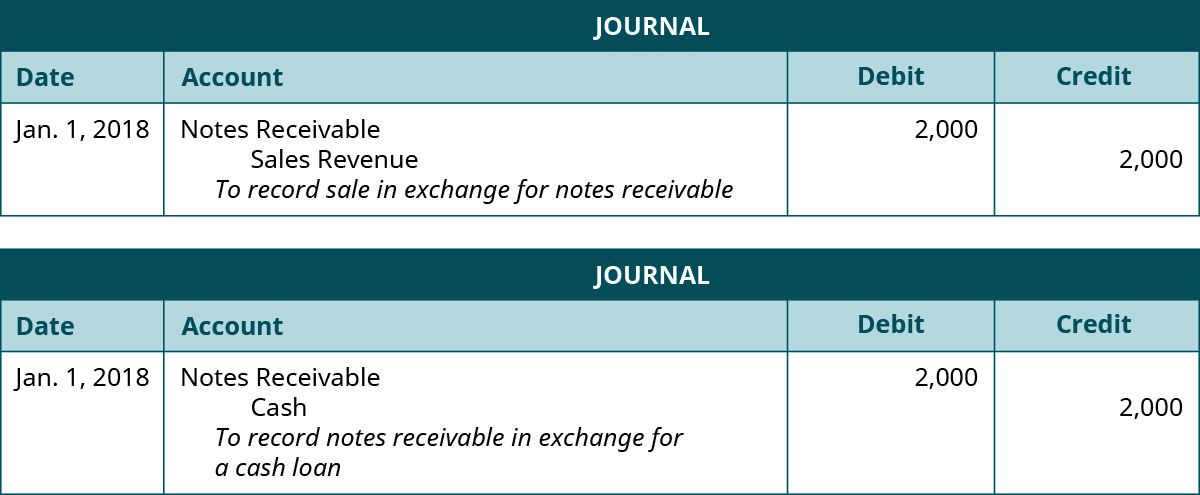

Notes receivable (note receivable)have several defining characteristics that include principal, length of contract terms, and interest. The principal of a note is the initial loan amount, not including interest, requested by the customer. If a customer approaches a lender, requesting $2,000, this amount is the principal. The date on which the security agreement is initially established is the issue date. A note’s maturity date is the date at which the principal and interest become due and payable. The maturity date is established in the initial note contract. For example, when the previously mentioned customer requested the $2,000 loan on January 1, 2018, terms of repayment included a maturity date of 24 months. This means that the loan will mature in two years, and the principal and interest are due at that time. The following journal entries occur at the note’s established start date. The first entry shows a note receivable in exchange for a product or service, and the second entry illustrates the note from the point of view that a $2,000 loan was issued by a financial institution to a customer (borrower).

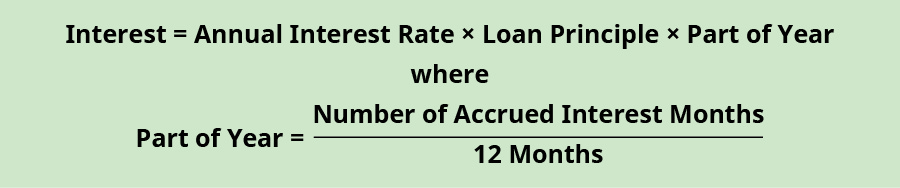

Before realization of the maturity date, the note is accumulating interest revenue for the lender. Interest is a monetary incentive to the lender that justifies loan risk. An annual interest rate is established with the loan terms. The interest rate is the part of a loan charged to the borrower, expressed as an annual percentage of the outstanding loan amount. Interest is accrued daily, and this accumulation must be recorded periodically (each month for example). The Revenue Recognition Principle requires that the interest revenue accrued is recorded in the period when earned. Periodic interest accrued is recorded in Interest Revenue and Interest Receivable. To calculate interest, the company can use the following formulas. The following example uses months but the calculation could also be based on a 365-day year.

Another common way to state the interest formula is Interest = Principal × Rate × Time. From the previous example, the company offered a $2,000 note with a maturity date of 24 months. The annual interest rate on the loan is 10%. Each period the company needs to record an entry for accumulated interest during the period. In this example, the first year’s interest revenue accumulation is computed as 10% × $2,000 × (12/12) = $200. The $200 is recognized in Interest Revenue and Interest Receivable.

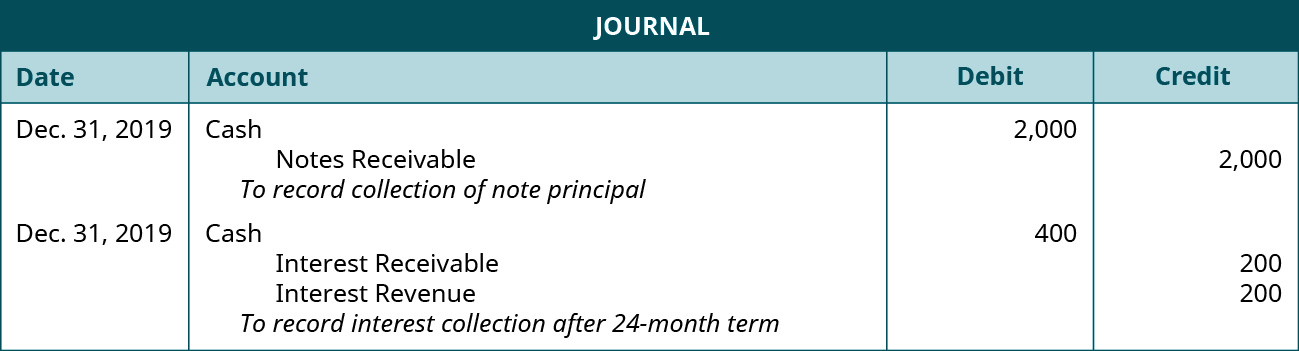

When interest is due at the end of the note (24 months), the company may record the collection of the loan principal and the accumulated interest. These transactions can be recorded as one entry or two. The first set of entries show collection of principal, followed by collection of the interest.

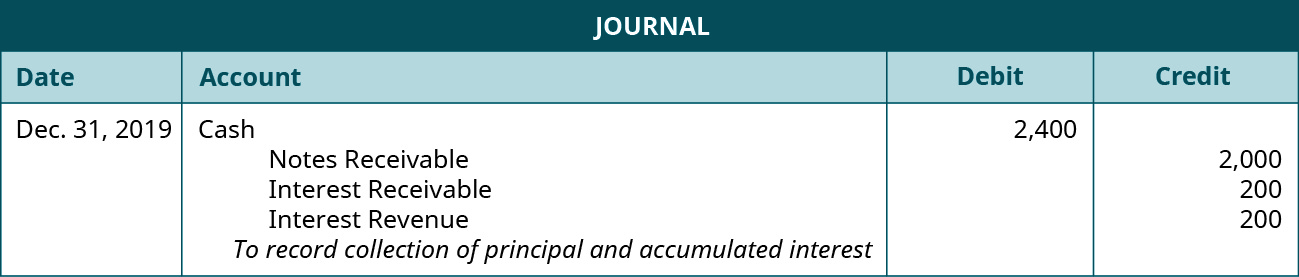

Interest revenue from year one had already been recorded in 2018, but the interest revenue from 2019 is not recorded until the end of the note term. Thus, Interest Revenue is increasing (credit) by $200, the remaining revenue earned but not yet recognized. Interest Receivable decreasing (credit) reflects the 2018 interest owed from the customer that is paid to the company at the end of 2019. The second possibility is one entry recognizing principal and interest collection.

If the note term does not exceed one accounting period, the entry showing note collection may not reflect interest receivable. For example, let’s say the company’s note maturity date was 12 months instead of 24 (payment in full occurs December 31, 2018). The entry to record collection of the principal and interest follows.

The examples provided account for collection of the note in full on the maturity date, which is considered an honored note. But what if the customer does not pay within the specified contract length? This situation is considered a dishonored note. A lender will still pursue collection of the note but will not maintain a long-term receivable on its books. Instead, the lender will convert the notes receivable and interest due into an account receivable. Sometimes a company will classify and label the uncollected account as a Dishonored Note Receivable. Using our example, if the company was unable to collect the $2,000 from the customer at the 12-month maturity date, the following entry would occur.

If it is still unable to collect, the company may consider selling the receivable to a collection agency. When this occurs, the collection agency pays the company a fraction of the note’s value, and the company would write off any difference as a factoring (third-party debt collection) expense. Let’s say that our example company turned over the $2,200 accounts receivable to a collection agency on March 5, 2019 and received only $500 for its value. The difference between $2,200 and $500 of $1,700 is the factoring expense.

Notes receivable can convert to accounts receivable, as illustrated, but accounts receivable can also convert to notes receivable. The transition from accounts receivable to notes receivable can occur when a customer misses a payment on a short-term credit line for products or services. In this case, the company could extend the payment period and require interest.

For example, a company may have an outstanding account receivable in the amount of $1,000. The customer negotiates with the company on June 1 for a six-month note maturity date, 12% annual interest rate, and $250 cash up front. The company records the following entry at contract establishment.

This examines a note from the lender’s perspective; see Current Liabilities for an in-depth discussion on the customer’s liability with a note (payable).

Illustrated Examples of Notes Receivable

To illustrate notes receivable scenarios, let’s return to Billie’s Watercraft Warehouse (BWW) as the example. BWW has a customer, Waterways Corporation, that tends to have larger purchases that require an extended payment period. On January 1, 2018, Waterways purchased merchandise in the amount of $250,000. BWW agreed to lend the $250,000 purchase cost (sales price) to Waterways under the following conditions. First, BWW agrees to accept a note payable issued by Waterways. The conditions of the note are that the principal amount is $250,000, the maturity date on the note is 24 months, and the annual interest rate is 12%. On January 1, 2018, BWW records the following entry.

Notes Receivable: Waterways increases (debit), and Sales Revenue increases (credit) for the principal amount of $250,000. On December 31, 2018, BWW records interest accumulated on the note for 12 months.

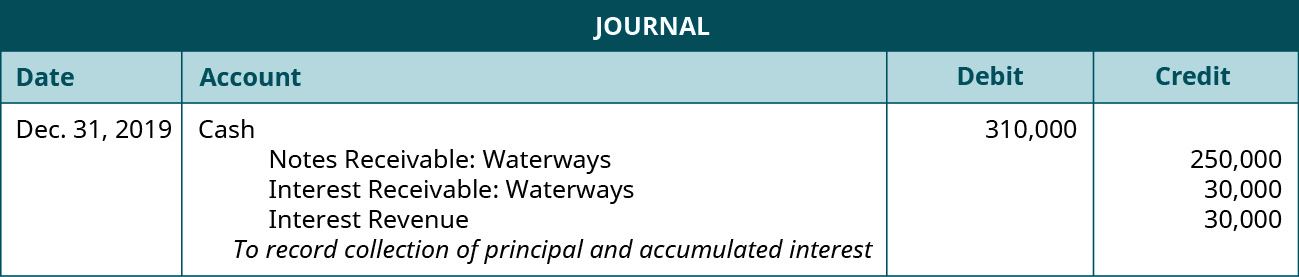

Interest Receivable: Waterways increases (debit) as does Interest Revenue (credit) for 12 months of interest computed as $250,000 × 12% × (12/12). On December 31, 2019, Waterways Corporation honors the note; BWW records this collection as a single entry.

Cash increases (debit) for the principal and interest total of $310,000, Notes Receivable: Waterways decreases (credit) for the principal amount of $250,000, Interest Receivable: Waterways decreases (credit) for the 2018 accumulated interest amount of $30,000, and Interest Revenue increases (credit) for the 2019 interest collection amount of $30,000.

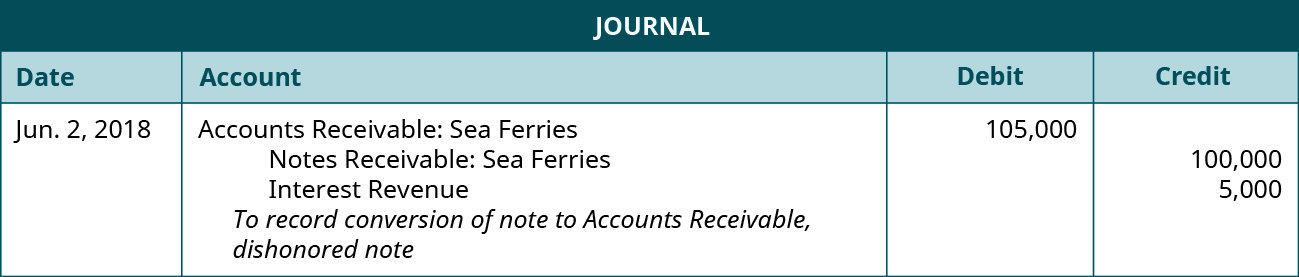

BWW does business with Sea Ferries Inc. BWW issued Sea Ferries a note in the amount of $100,000 on January 1, 2018, with a maturity date of six months, at a 10% annual interest rate. On July 2, BWW determined that Sea Ferries dishonored its note and recorded the following entry to convert this debt into accounts receivable.

Accounts Receivable: Sea Ferries increases (debit) for the principal note amount plus interest, Notes Receivable: Sea Ferries decreases (credit) for the principal amount due, and Interest Revenue increases (credit) for interest earned at maturity. Interest is computed as $100,000 × 10% × (6/12). On September 1, 2018, BWW determines that Sea Ferries’s account will be uncollectible and sells the balance to a collection agency for a total of $35,000.

Cash increases (debit) for the agreed-upon discounted value of $35,000, Factoring Expense increases (debit) for the outstanding amount and the discounted sales price, and Accounts Receivable: Sea Ferries decreases (credit) for the original amount owed.

Alliance Cruises is a customer of BWW with an outstanding accounts receivable balance of $50,000. Alliance is unable to pay in full on schedule, so it negotiates with BWW on March 1 to convert its accounts receivable into a notes receivable. BWW agrees to the following terms: six-month note maturity date, 18% annual interest rate, and $10,000 cash up front. BWW records the following entry at contract establishment.

Cash increases (debit) for the up-front collection of $10,000, Notes Receivable: Alliance increases (debit) for the principal amount on the note of $40,000, and Accounts Receivable: Alliance decreases (credit) for the original amount Alliance owed of $50,000.

LINK TO LEARNING

KEY TAKEAWAYS

Summary

- Accounts receivable is an informal agreement between customer and company, with collection occurring in less than a year, and no interest requirement. In contrast, notes receivable is a legal contract, with collection occurring typically over a year, and interest requirements.

- The terms of a note contract establish the principal collection amount, maturity date, and annual interest rate.

- Interest is computed as the principal amount multiplied by the part of the year, multiplied by the annual interest rate. The entry to record accumulated interest increases interest receivable and interest revenue.

- An honored note means collection occurred on time and in full. Recording an honored note includes an increase to cash and interest revenue, and a decrease to interest receivable and notes receivable.

- A dishonored note means collection did not occur on time or in full. In this case, a note and the accumulated interest would be converted to accounts receivable.

- When a company cannot collect on account, the company may consider selling the receivable to a collection agency. They will sell the receivable at a fraction of the value in order to apply resources elsewhere.

- If a customer cannot pay its accounts receivable on time, it may renegotiate terms that include a note and interest, thereby converting the accounts receivable to notes receivable. in this case, accounts receivable decreases, and notes receivable and cash increase.

Glossary

- interest

- monetary incentive to the lender, which justifies loan risk; interest is paid to the lender by the borrower

- interest rate

- part of a loan charged to the borrower, expressed as an annual percentage of the outstanding loan amount

- issue date

- point at which the security agreement is initially established

- maturity date

- date a bond or note becomes due and payable

- note receivable

- formal legal contract between the buyer and the company, which requires a specific payment amount at a predetermined future date, usually includes interest, and is payable beyond a company’s operating cycle

- principal

- initial borrowed amount of a loan, not including interest; also, face value or maturity value of a bond (the amount to be paid at maturity)

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

formal legal contract between the buyer and the company, which requires a specific payment amount at a predetermined future date, usually includes interest, and is payable beyond a company’s operating cycle

initial borrowed amount of a loan, not including interest; also, face value or maturity value of a bond (the amount to be paid at maturity)

point at which the security agreement is initially established

date a bond or note becomes due and payable

monetary incentive to the lender, which justifies loan risk; interest is paid to the lender by the borrower

part of a loan charged to the borrower, expressed as an annual percentage of the outstanding loan amount