LO 11.1 Distinguish between Tangible and Intangible Assets

Assets are items a business owns.1 For accounting purposes, assets are categorized as current versus long term, and tangible versus intangible. Assets that are expected to be used by the business for more than one year are considered long-term assets. They are not intended for resale and are anticipated to help generate revenue for the business in the future. Some common long-term assets are computers and other office machines, buildings, vehicles, software, computer code, and copyrights. Although these are all considered long-term assets, some are tangible and some are intangible.

Tangible Assets

An asset is considered a tangible asset when it is an economic resource that has physical substance—it can be seen and touched. Tangible assets can be either short term, such as inventory and supplies, or long term, such as land, buildings, and equipment. To be considered a long-term tangible asset, the item needs to be used in the normal operation of the business for more than one year, not be near the end of its useful life, and the company must have no plan to sell the item in the near future. The useful life is the time period over which an asset cost is allocated. Long-term tangible assets are known as fixed assets.

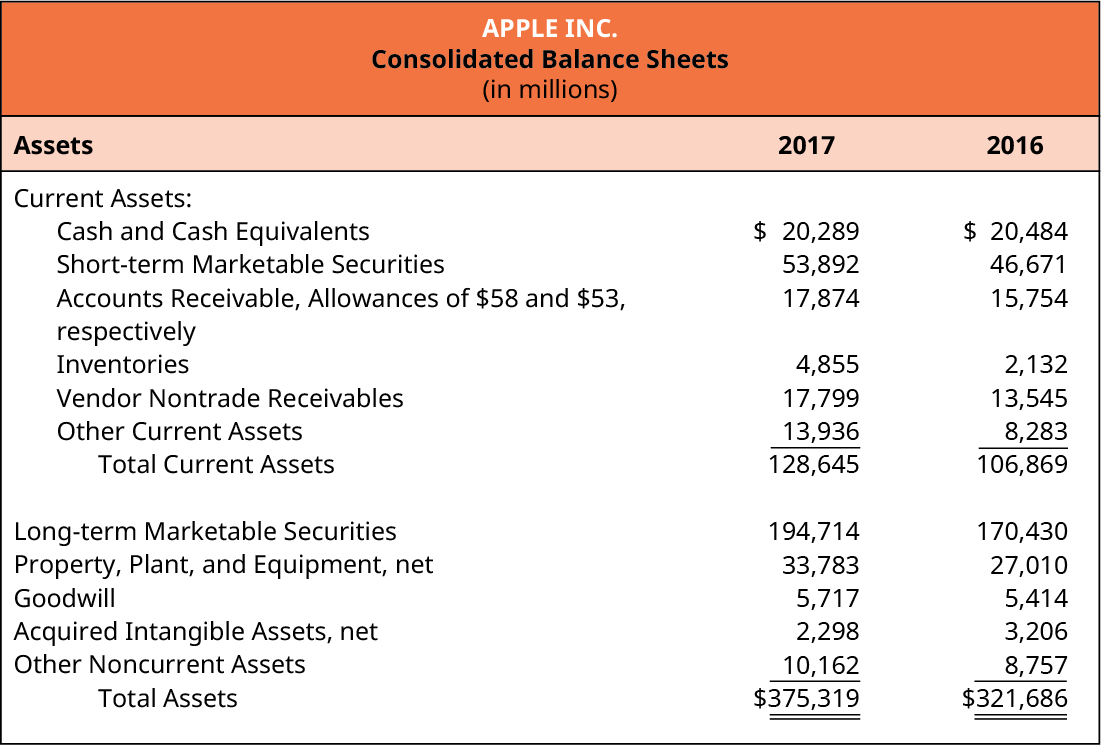

Businesses typically need many different types of these assets to meet their objectives. These assets differ from the company’s products. For example, the computers that Apple Inc. intends to sell are considered inventory (a short-term asset), whereas the computers Apple’s employees use for day-to-day operations are long-term assets. In Liam’s case, the new silk-screening machine would be considered a long-term tangible asset as he plans to use it over many years to help him generate revenue for his business. Long-term tangible assets are listed as noncurrent assets on a company’s balance sheet. Typically, these assets are listed under the category of Property, Plant, and Equipment (PP&E), but they may be referred to as fixed assets or plant assets.

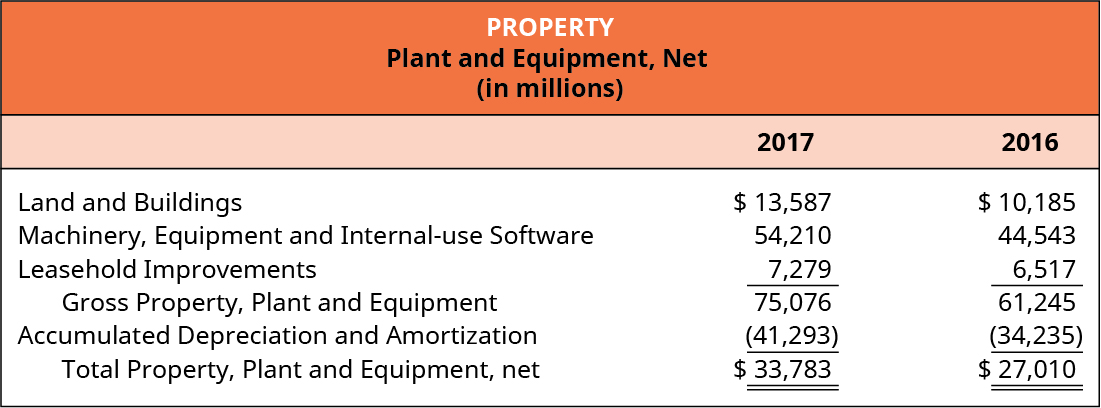

Apple Inc. lists a total of $33,783,000,000 in total Property, Plant and Equipment (net) on its 2017 consolidated balance sheet (see (Figure)).2 As shown in the figure, this net total includes land and buildings, machinery, equipment and internal-use software, and leasehold improvements, resulting in a gross PP&E of $75,076,000,000—less accumulated depreciation and amortization of $41,293,000,000—to arrive at the net amount of $33,783,000,000.

LINK TO LEARNING

Intangible Assets

Companies may have other long-term assets used in the operations of the business that they do not intend to sell, but that do not have physical substance; these assets still provide specific rights to the owner and are called intangible assets. These assets typically appear on the balance sheet following long-term tangible assets (see (Figure).)3 Examples of intangible assets are patents, copyrights, franchises, licenses, goodwill, sometimes software, and trademarks ((Figure)). Because the value of intangible assets is very subjective, it is usually not shown on the balance sheet until there is an event that indicates value objectively, such as the purchase of an intangible asset.

A company often records the costs of developing an intangible asset internally as expenses, not assets, especially if there is ambiguity in the expense amounts or economic life of the asset. However, there are also conditions under which the costs can be allocated over the anticipated life of the asset. (The treatment of intangible asset costs can be quite complex and is taught in advanced accounting courses.)

| Types of Intangible Assets | |

|---|---|

| Asset | Useful Life |

| Patents | Twenty years |

| Trademarks | Renewable every ten years |

| Copyrights | Seventy years beyond death of creator |

| Goodwill | Indefinite |

THINK IT THROUGH

Your company has recently hired a star scientist who has a history of developing new technologies. The company president is excited with the new hire, and questions you, the company accountant, why the scientist cannot be recorded as an intangible asset, as the scientist will probably provide more value to the company in the future than any of its other assets. Discuss why the scientist, and employees in general, who often provide the greatest value for a company, are not recorded as intangible assets.

Patents

A patent is a contract that provides a company exclusive rights to produce and sell a unique product. The rights are granted to the inventor by the federal government and provide exclusivity from competition for twenty years. Patents are common within the pharmaceutical industry as they provide an opportunity for drug companies to recoup the significant financial investment on research and development of a new drug. Once the new drug is produced, the company can sell it for twenty years with no direct competition.

THINK IT THROUGH

Jane works in product development for a technology company. She just heard that her employer is slashing research and development costs. When she asks why, the marketing senior vice president tells her that current research and development costs are reducing net income in the current year for a potential but unknown benefit in future years, and that management is concerned about the effect on stock price. Jane wonders why research and development costs are not capitalized so that the cost would be matched with the future revenues. Why do you think research and development costs are not capitalized?

Trademarks and Copyrights

A company’s trademark is the exclusive right to the name, term, or symbol it uses to identify itself or its products. Federal law allows companies to register their trademarks to protect them from use by others. Trademark registration lasts for ten years with optional 10-year renewable periods. This protection helps prevent impersonators from selling a product similar to another or using its name. For example, a burger joint could not start selling the “Big Mac.” Although it has no physical substance, the exclusive right to a term or logo has value to a company and is therefore recorded as an asset.

A copyright provides the exclusive right to reproduce and sell artistic, literary, or musical compositions. Anyone who owns the copyright to a specific piece of work has exclusive rights to that work. Copyrights in the United States last seventy years beyond the death of the original author. While you might not be overly interested in what seems to be an obscure law, it actually directly affects you and your fellow students. It is one of the primary reasons that your copy of the Collected Works of William Shakespeare costs about $40 in your bookstore or online, while a textbook, such as Principles of Biology or Principles of Accounting, can run in the hundreds of dollars.

Goodwill

Goodwill is a unique intangible asset. Goodwill refers to the value of certain favorable factors that a business possesses that allows it to generate a greater rate of return or profit. Such factors include superior management, a skilled workforce, quality products or service, great geographic location, and overall reputation. Companies typically record goodwill when they acquire another business in which the purchase price is in excess of the fair value of the identifiable net assets. The difference is recorded as goodwill on the purchaser’s balance sheet. For example, the goodwill of $5,717,000,000 that we see on Apple’s consolidated balance sheets for 2017 (see (Figure)) was created when Apple purchased another business for a purchase price exceeding the book value of its net assets.

YOUR TURN

Your cousin started her own business and wants to get a small loan from a local bank to expand production in the next year. The bank has asked her to prepare a balance sheet, and she is having trouble classifying the assets properly. Help her sort through the list below and note the assets that are tangible long-term assets and those that are intangible long-term assets.

- Cash

- Patent

- Accounts Receivable

- Land

- Investments

- Software

- Inventory

- Note Receivable

- Machinery

- Equipment

- Marketable Securities

- Owner Capital

- Copyright

- Building

- Accounts Payable

- Mortgage Payable

Solution

Tangible long-term assets include land, machinery, equipment, and building. Intangible long-term assets include patent, software, and copyright.

KEY TAKEAWAYS

Key Concepts and Summary

- Tangible assets are assets that have physical substance.

- Long-term tangible assets are assets used in the normal course of operation of businesses that last for more than one year and are not intended to be resold.

- Examples of long-term tangible assets are land, building, and machinery.

- Intangible assets lack physical substance but often have value and legal rights and protections, and therefore are still assets to the firm.

- Examples of intangible assets are patents, trademarks, copyrights, and goodwill.

Footnotes

- 1 The Financial Accounting Standards Board (FASB) defines assets as “probable future economic benefits obtained or controlled by a particular entity as a result of past transactions or events” (SFAC No. 6, p. 12).

- 2 Apple, Inc. U.S. Securities and Exchange Commission 10-K Filing. November 3, 2017. http://pdf.secdatabase.com/2624/0000320193-17-000070.pdf

- 3 Apple, Inc. U.S. Securities and Exchange Commission 10-K Filing. November 3, 2017. http://pdf.secdatabase.com/2624/0000320193-17-000070.pdf

Glossary

- copyright

- exclusive rights to reproduce and sell an artistic, literary, or musical asset

- fixed asset

- tangible long-term asset

- goodwill

- value of certain favorable factors that a business possesses that allows it to generate a greater rate of return or profit; includes price paid for an acquired company above the fair value of its identifiable net assets

- intangible asset

- asset with financial value but no physical presence; examples include copyrights, patents, goodwill, and trademarks

- long-term asset

- asset used ongoing in the normal course of business for more than one year that is not intended to be resold

- patent

- contract providing exclusive rights to produce and sell a unique product without competition for twenty years

- tangible asset

- asset that has physical substance

- trademark

- exclusive right to a name, term, or symbol a company uses to identify itself or its products

- useful life

- time period over which an asset cost is allocated

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

same as "non-current asset" -- asset used ongoing in the normal course of business for more than one year that is not intended to be resold

asset that has physical substance

time period over which an asset cost is allocated

tangible long-term asset

asset with financial value but no physical presence; examples include copyrights, patents, goodwill, and trademarks

contract providing exclusive rights to produce and sell a unique product without competition for twenty years

exclusive right to a name, term, or symbol a company uses to identify itself or its products

exclusive rights to reproduce and sell an artistic, literary, or musical asset

value of certain favorable factors that a business possesses that allows it to generate a greater rate of return or profit; includes price paid for an acquired company above the fair value of its identifiable net assets