LO 9.3 Determine the Efficiency of Receivables Management Using Financial Ratios

You received an unexpected tax refund this year and want to invest the money in a profitable and growing company. After conducting research, you determine that it is important for a company to collect on outstanding debt quickly, while showing a willingness to offer customers credit options to increase sales opportunities, among other things. You are new to investing, so where do you begin?

Stakeholders, such as investors, lenders, and management, look to financial statement data to make informed decisions about a company’s financial position. They will look at each statement—as well as ratio analysis—for trends, industry comparisons, and past performance to help make financing determinations. Because you are reviewing companies for quick debt collection, as well as credit extension to boost sales, you would consider receivables ratios to guide your decision. Discuss the Role of Accounting for Receivables in Earnings Management will explain and demonstrate two popular ratios—the accounts receivable turnover ratio and the number of days’ sales in receivables ratio—used to evaluate a company’s receivables experiences.

It is important to remember, however, that for a comprehensive evaluation of a company’s true potential as an investment, you need to consider other types of ratios, in addition to the receivables ratios. For example, you might want to look at the company’s profitability, solvency, and liquidity performances using ratios. (See Appendix A for more information on ratios.)

Basic Functions of the Receivables Ratios

Receivables ratios show company performance in relation to current debt collection, as well as credit policy effect on sales growth. One receivables ratio is called the accounts receivable turnover ratio. This ratio determines how many times (i.e., how often) accounts receivable are collected during an operating period and converted to cash (see below). A higher number of times indicates that receivables are collected quickly. This quick cash collection may be viewed as a positive occurrence, because liquidity improves, and the company may reinvest in its business sooner when the value of the dollar has more buying power (time value of money). The higher number of times may also be a negative occurrence, signaling that credit extension terms are too tight, and it may exclude qualified consumers from purchasing. Excluding these customers means that they may take their business to a competitor, thus reducing potential sales.

In contrast, a lower number of times indicates that receivables are collected at a slower rate. A slower collection rate could signal that lending terms are too lenient; management might consider tightening lending opportunities and more aggressively pursuing outstanding debt. The lower turnover also shows that the company has cash tied up in receivable longer, thus hindering its ability to reinvest this cash in other current projects. The lower turnover rate may signal a high level of bad debt accounts. The determination of a high or low turnover rate really depends on the standards of the company’s industry.

Another receivables ratio one must consider is the number of days’ sales in receivables ratio. This ratio is similar to accounts receivable turnover in that it shows the expected days it will take to convert accounts receivable into cash. The reflected outcome is in number of days, rather than in number of times.

Companies often have outstanding debt that requires scheduled payments. If it takes longer for a company to collect on outstanding receivables, this means it may not be able to meet its current obligations. It helps to know the number of days it takes to go through the accounts receivable collection cycle so a company can plan its debt repayments; this receivables ratio also signals how efficient its collection procedures are. As with the accounts receivable turnover ratio, there are positive and negative elements with a smaller and larger amount of days; in general, the fewer number of collection days on accounts receivable, the better.

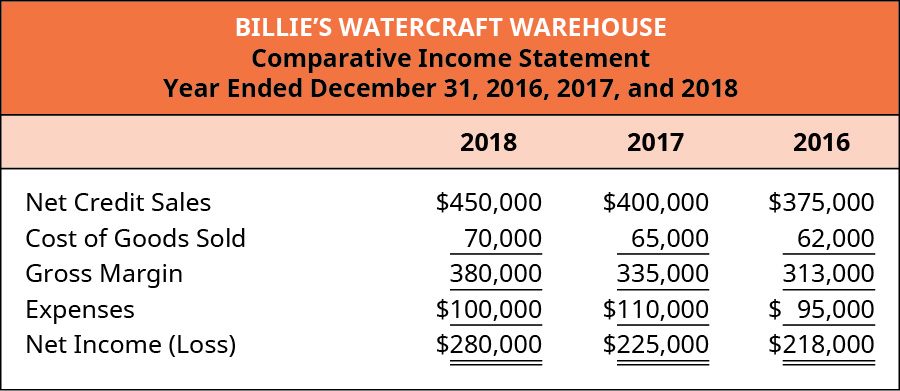

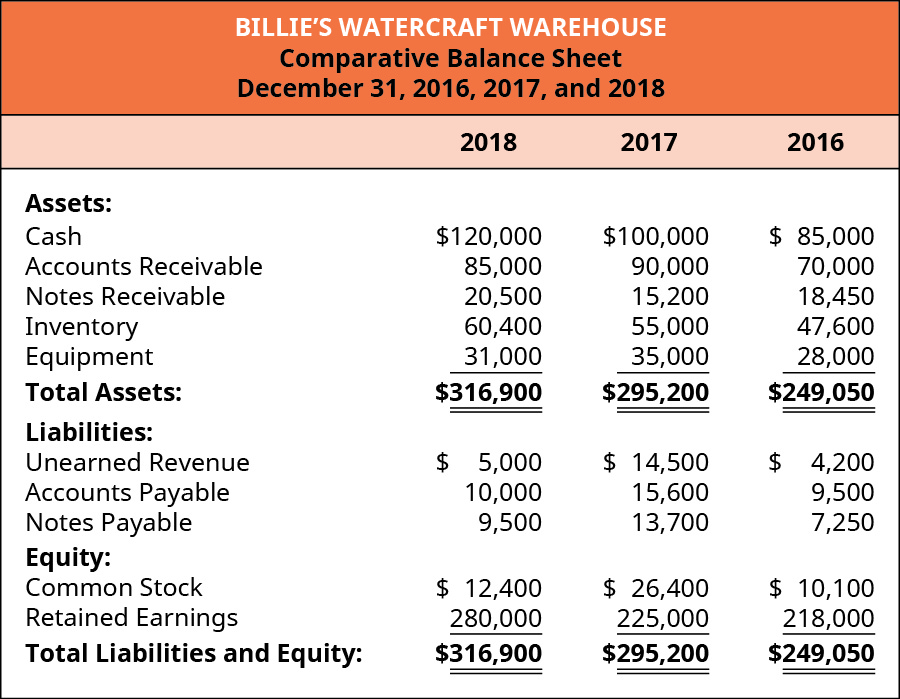

To illustrate the use of these ratios to make financial decisions, let’s use Billie’s Watercraft Warehouse (BWW) as the example. Included are the comparative income statement and the comparative balance sheet for BWW, followed by competitor ratio information, for the years 2016, 2017, and 2018 as shown below.

| Comparison of Ratios: Industry Competitor to BWW | ||

|---|---|---|

| Year | Accounts Receivable Turnover Ratio | Number of Days’ Sales in Receivables Ratio |

| 2016 | 4.89 times | 80 days |

| 2017 | 4.92 times | 79.23 days |

| 2018 | 5.25 times | 76.44 days |

YOUR TURN

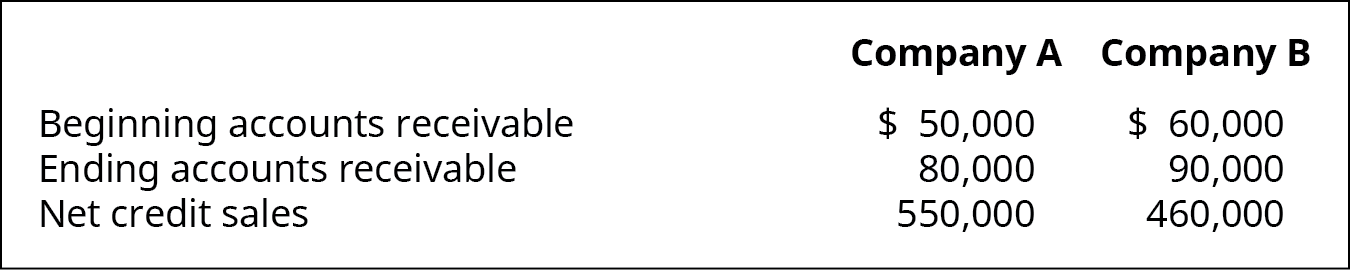

You are an investor looking to contribute financially to either Company A or Company B. The following select financial information follows.

Based on the information provided:

- Compute the accounts receivable turnover ratio

- Compute the number of days’ sales in receivables ratio for both Company A and Company B (round all answers to two decimal places)

- Interpret the outcomes, stating which company you would invest in and why

Solution

Company A: ART = 8.46 times, Days’ Sales = 43.14 days, Company B: ART = 6.13 times, Days’ Sales = 59.54 days. Upon initial review of this limited information, Company A seems to be the better choice, since their turnover ratio is higher and the collection time is lower with 43.14 days. One might want more information on trends for each company with these ratios and a comparison to others in the same industry. More information is needed before making an informed decision.

Accounts Receivable Turnover Ratio

The ratio to determine accounts receivable turnover is as follows.

Net credit sales are sales made on credit only; cash sales are not included because they do not produce receivables. However, many companies do not report credit sales separate from cash sales, so “net sales” may be substituted for “net credit sales” in this case. Beginning and ending accounts receivable refer to the beginning and ending balances in accounts receivable for the period. The beginning accounts receivable balance is the same figure as the ending accounts receivable balance from the prior period.

Use this formula to compute BWW’s accounts receivable turnover for 2017 and 2018.

The accounts receivable turnover ratio for 2017 is 5 times ($400,000/$80,000). [Net credit sales for 2017 are $400,000, and Average accounts receivable = ($70,000 + $90,000) / 2 = $80,000]

The accounts receivable turnover ratio for 2018 is 5.14 times (rounded to two decimal places). [Net credit sales for 2018 are $450,000, and Average accounts receivable = ($90,000 + $85,000) / 2 = $87,500]

The outcome for 2017 means that the company turns over receivables (converts receivables into cash) 5 times during the year. The outcome for 2018 shows that BWW converts cash at a quicker rate of 5.14 times. There is a trend increase from 2017 to 2018. BWW sells various watercraft. These products tend to have a higher sales price, making a customer more likely to pay with credit. This can also increase the length of debt repayment. Comparing to another company in the industry, BWW’s turnover rate is standard. To increase the turnover rate, BWW can consider extending credit to more customers who the company has determined will pay on a quicker basis or schedule, or BWW can more aggressively pursue the outstanding debt from current customers.

Number of Days’ Sales in Receivables Ratio

The ratio to determine number of days’ sales in receivables is as follows.

The numerator is 365, the number of days in the year. Because the accounts receivable turnover ratio determines an average accounts receivable figure, the outcome for the days’ sales in receivables is also an average number. Using this formula, compute BWW’s number of days’ sales in receivables ratio for 2017 and 2018.

The ratio for 2017 is 73 days (365/5), and for 2018 is 71.01 days (365/5.14), rounded. This means it takes 73 days in 2017 and 71.01 days in 2018 to complete the collection cycle, which is a decrease from 2017 to 2018. A downward trend is a positive for the company, and BWW outperforms the competition slightly. This is good because BWW can use the cash toward other business expenditures, or the downward trend could signal that the company needs to loosen credit terms or more aggressively collect outstanding accounts.

Looking at both ratios, BWW seems well positioned within the industry, and a potential investor or lender may be more apt to contribute financially to the organization with this continued positive trend.

LINK TO LEARNING

KEY TAKEAWAYS

Summary

- Receivable ratios are best used to determine quick debt collection and lending practices. An investor, lender, or management may use these ratios—in conjunction with financial statement review, past performance, industry standards, and trends—to make an informed financial decision.

- The accounts receivable turnover ratio shows how many times receivables are collected during a period and converted to cash. The ratio is found by taking net credit sales and dividing by average accounts receivable for the period.

- The number of days’ sales in receivables ratio shows the expected number of days it will take to convert accounts receivable into cash. The ratio is found by taking 365 days and dividing by the accounts receivable turnover ratio.

Glossary

- accounts receivable turnover ratio

- how many times accounts receivable is collected during an operating period and converted to cash

- number of days’ sales in receivables

- expected days it will take to convert accounts receivable into cash

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

how many times accounts receivable is collected during an operating period and converted to cash

expected days it will take to convert accounts receivable into cash