LO 14.4 Compare and Contrast Owners’ Equity versus Retained Earnings

Owners’ equity represents the business owners’ share of the company. It is often referred to as net worth or net assets in the financial world and as stockholders’ equity or shareholders’ equity when discussing businesses operations of corporations. From a practical perspective, it represents everything a company owns (the company’s assets) minus all the company owes (its liabilities). While “owners’ equity” is used for all three types of business organizations (corporations, partnerships, and sole proprietorships), only sole proprietorships name the balance sheet account “owner’s equity” as the entire equity of the company belongs to the sole owner. Partnerships (to be covered more thoroughly in Partnership Accounting) often label this section of their balance sheet as “partners’ equity.” All three forms of business utilize different accounting for the respective equity transactions and use different equity accounts, but they all rely on the same relationship represented by the basic accounting equation ((Figure)).

Three Forms of Business Ownership

Businesses operate in one of three forms—sole proprietorships, partnerships, or corporations. Sole proprietorships utilize a single account in owners’ equity in which the owner’s investments and net income of the company are accumulated and distributions to the owner are withdrawn. Partnerships utilize a separate capital account for each partner, with each capital account holding the respective partner’s investments and the partner’s respective share of net income, with reductions for the distributions to the respective partners. Corporations differ from sole proprietorships and partnerships in that their operations are more complex, often due to size. Unlike these other entity forms, owners of a corporation usually change continuously.

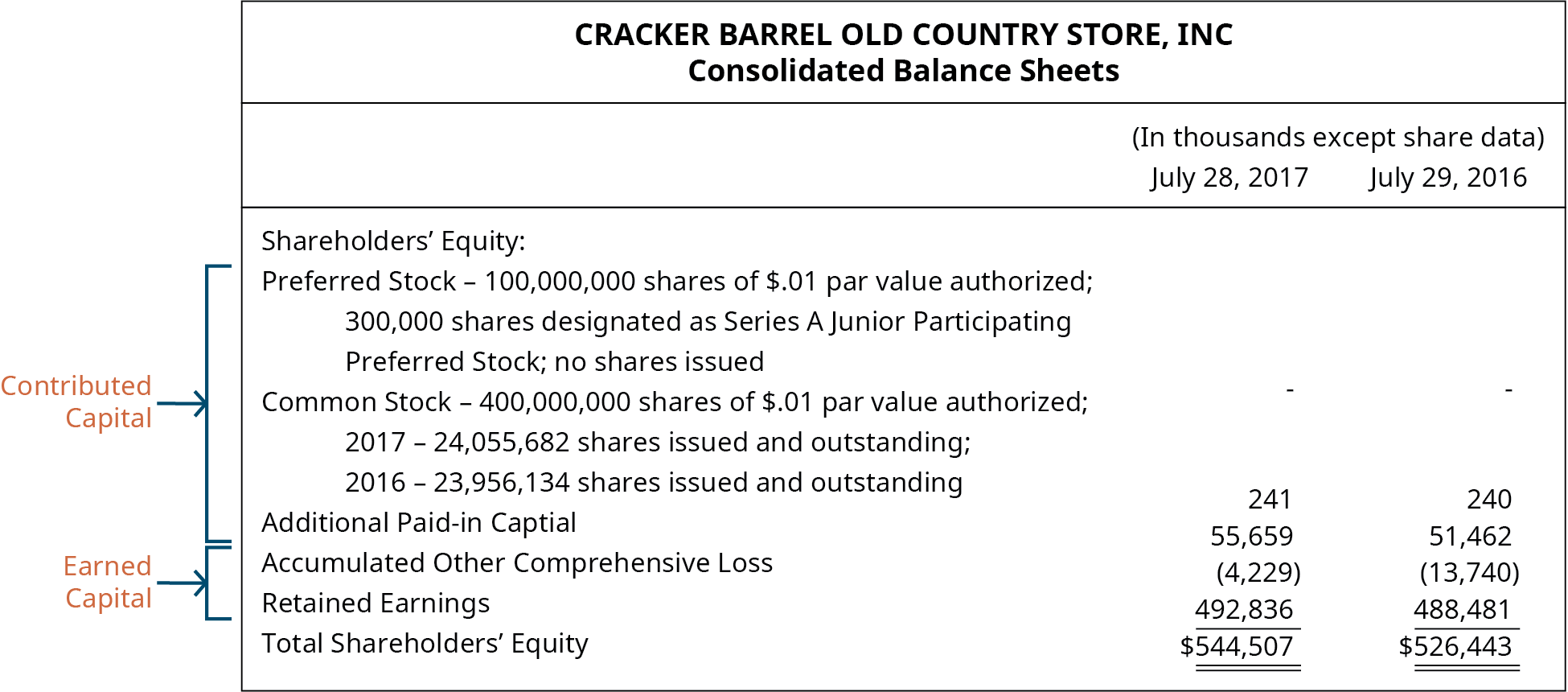

The stockholders’ equity section of the balance sheet for corporations contains two primary categories of accounts. The first is paid-in capital, or contributed capital—consisting of amounts paid in by owners. The second category is earned capital, consisting of amounts earned by the corporation as part of business operations. On the balance sheet, retained earnings is a key component of the earned capital section, while the stock accounts such as common stock, preferred stock, and additional paid-in capital are the primary components of the contributed capital section.

CONCEPTS IN PRACTICE

The stockholders’ equity section of Cracker Barrel Old Country Store, Inc.’s consolidated balance sheet as of July 28, 2017, and July 29, 2016, shows the company’s contributed capital and the earned capital accounts.1

Characteristics and Functions of the Retained Earnings Account

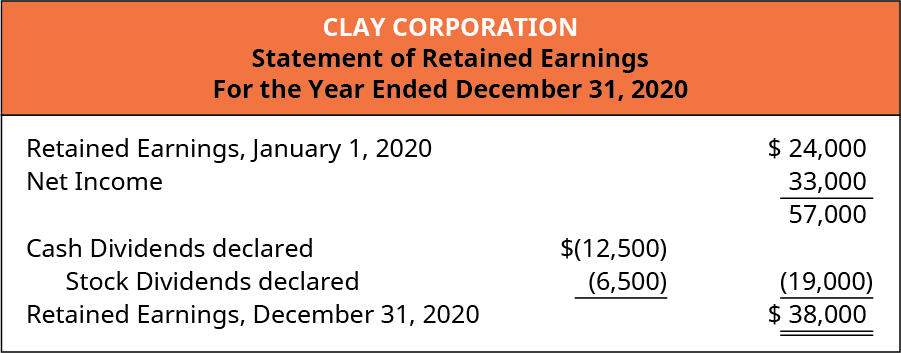

Retained earnings is the primary component of a company’s earned capital. It generally consists of the cumulative net income minus any cumulative losses less dividends declared. A basic statement of retained earnings is referred to as an analysis of retained earnings because it shows the changes in the retained earnings account during the period. A company preparing a full set of financial statements may choose between preparing a statement of retained earnings, if the activity in its stock accounts is negligible, or a statement of stockholders’ equity, for corporations with activity in their stock accounts. A statement of retained earnings for Clay Corporation for its second year of operations The figure below shows the company generated more net income than the amount of dividends it declared.

When the retained earnings balance drops below zero, this negative or debit balance is referred to as a deficit in retained earnings.

Restrictions to Retained Earnings

Retained earnings is often subject to certain restrictions. Restricted retained earnings is the portion of a company’s earnings that has been designated for a particular purpose due to legal or contractual obligations. Some of the restrictions reflect the laws of the state in which a company operates. Many states restrict retained earnings by the cost of treasury stock, which prevents the legal capital of the stock from dropping below zero. Other restrictions are contractual, such as debt covenants and loan arrangements; these exist to protect creditors, often limiting the payment of dividends to maintain a minimum level of earned capital.

Appropriations of Retained Earnings

A company’s board of directors may designate a portion of a company’s retained earnings for a particular purpose such as future expansion, special projects, or as part of a company’s risk management plan. The amount designated for a particular purpose is classified as appropriated retained earnings.

There are two options in accounting for appropriated retained earnings, both of which allow the corporation to inform the financial statement users of the company’s future plans. The first accounting option is to make no journal entry and disclose the amount of appropriation in the notes to the financial statement. The second option is to record a journal entry that transfers part of the unappropriated retained earnings into an Appropriated Retained Earnings account. To illustrate, assume that on March 3, Clay Corporation’s board of directors appropriates $12,000 of its retained earnings for future expansion. The company’s retained earnings account is first renamed as Unappropriated Retained Earnings. The journal entry decreases the Unappropriated Retained Earnings account with a debit and increases the Appropriated Retained Earnings account with a credit for $12,000.

The company will report the appropriate retained earnings in the earned capital section of its balance sheet. It should be noted that an appropriation does not set aside funds nor designate an income statement, asset, or liability effect for the appropriated amount. The appropriation simply designates a portion of the company’s retained earnings for a specific purpose, while signaling that the earnings are being retained in the company and are not available for dividend distributions.

Statement of Stockholders’ Equity

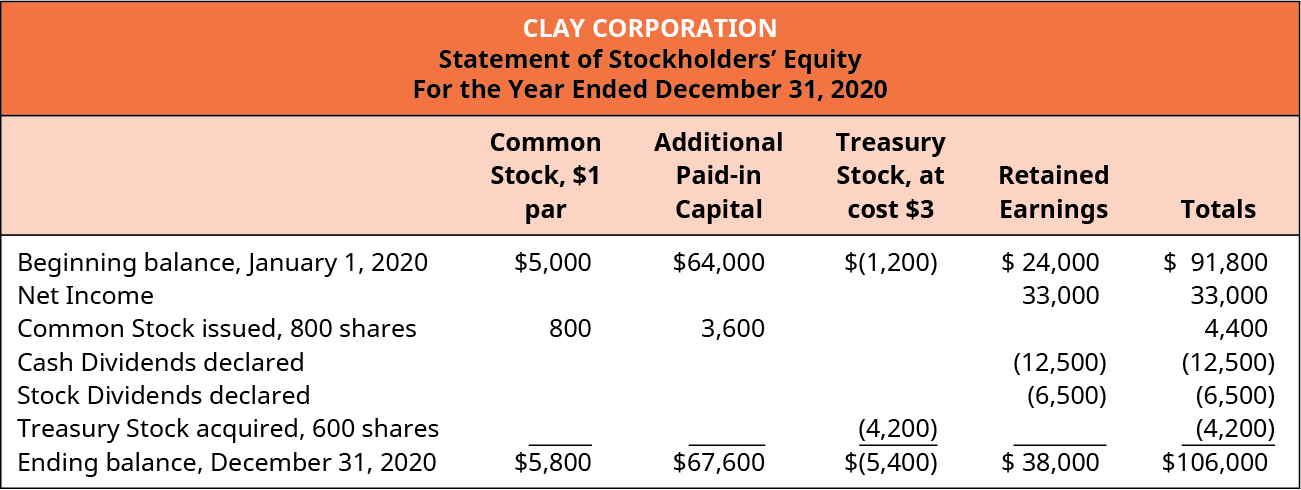

The statement of retained earnings is a subsection of the statement of stockholders’ equity. While the retained earnings statement shows the changes between the beginning and ending balances of the retained earnings account during the period, the statement of stockholders’ equity provides the changes between the beginning and ending balances of each of the stockholders’ equity accounts, including retained earnings. The format typically displays a separate column for each stockholders’ equity account, as shown for Clay Corporation below. The key events that occurred during the year—including net income, stock issuances, and dividends—are listed vertically. The stockholders’ equity section of the company’s balance sheet displays only the ending balances of the accounts and does not provide the activity or changes during the period.

Nearly all public companies report a statement of stockholders’ equity rather than a statement of retained earnings because GAAP requires disclosure of the changes in stockholders’ equity accounts during each accounting period. It is significantly easier to see the changes in the accounts on a statement of stockholders’ equity rather than as a paragraph note to the financial statements.

IFRS CONNECTION

Both U.S. GAAP and IFRS require the reporting of the various owners’ accounts. Under U.S. GAAP, these accounts are presented in a statement that is most often called the Statement of Stockholders’ Equity. Under IFRS, this statement is usually called the Statement of Changes in Equity. Some of the biggest differences between U.S. GAAP and IFRS that arise in reporting the various accounts that appear in those statements relate to either categorization or terminology differences.

U.S. GAAP divides owners’ accounts into two categories: contributed capital and retained earnings. IFRS uses three categories: share capital, accumulated profits and losses, and reserves. The first two IFRS categories correspond to the two categories used under U.S. GAAP. What about the third category, reserves? Reserves is a category that is used to report items such as revaluation surpluses from revaluing long-term assets (see the Long-Term Assets Feature Box: IFRS Connection for details), as well as other equity transactions such as unrealized gains and losses on available-for-sale securities and transactions that fall under Other Comprehensive Income (topics typically covered in more advanced accounting classes). U.S. GAAP does not use the term “reserves” for any reporting.

There are also differences in terminology between U.S. GAAP and IFRS shown below.

| Terminology Differences between U.S. GAAP and IFRS | |

|---|---|

| U.S. GAAP | IFRS |

| Common stock | Share capital |

| Preferred stock | Preference shares |

| Additional paid-in capital | Share premium |

| Stockholders | Shareholders |

| Retained earnings | Retained profits or accumulated profits |

| Retained earnings deficit | Accumulated losses |

All of this information pertains to publicly traded corporations, but what about corporations that are not publicly traded? Most corporations in the U.S. are not publicly traded, so do these corporations use U.S. GAAP? Some do; some do not. A non-public corporation can use cash basis, tax basis, or full accrual basis of accounting. Most corporations would use a full accrual basis of accounting such as U.S. GAAP. Cash and tax basis are most likely used only by sole proprietors or small partnerships.

However, U.S. GAAP is not the only full accrual method available to non-public corporations. Two alternatives are IFRS and a simpler form of IFRS, known as IFRS for Small and Medium Sized Entities, or SMEs for short. In 2008, the AICPA recognized the IASB as a standard setter of acceptable GAAP and designated IFRS and IFRS for SMEs as an acceptable set of generally accepted accounting principles. However, it is up to each State Board of Accountancy to determine if that state will allow the use of IFRS or IFRS for SMEs by non-public entities incorporated in that state.

What is a SME? Despite the use of size descriptors in the title, qualifying as a small or medium-sized entity has nothing to do with size. A SME is any entity that publishes general purpose financial statements for public use but does not have public accountability. In other words, the entity is not publicly traded. In addition, the entity, even if it is a partnership, cannot act as a fiduciary; for example, it cannot be a bank or insurance company and use SME rules.

Why might a non-public corporation want to use IFRS for SMEs? First, IFRS for SMEs contains fewer and simpler standards. IFRS for SMEs has only about 300 pages of requirements, whereas regular IFRS is over 2,500 pages and U.S. GAAP is over 25,000 pages. Second, IFRS for SMEs is only modified every three years. This means entities using IFRS for SMEs don’t have to frequently adjust their accounting systems and reporting to new standards, whereas U.S. GAAP and IFRS are modified more frequently. Finally, if a corporation transacts business with international businesses, or hopes to attract international partners, seek capital from international sources, or be bought out by an international company, then having their financial statements in IFRS form would make these transactions easier.

Prior Period Adjustments

Prior period adjustments are corrections of errors that appeared on previous periods’ financial statements. These errors can stem from mathematical errors, misinterpretation of GAAP, or a misunderstanding of facts at the time the financial statements were prepared. Many errors impact the retained earnings account whose balance is carried forward from the previous period. Since the financial statements have already been issued, they must be corrected. The correction involves changing the financial statement amounts to the amounts they would have been had no errors occurred, a process known as restatement. The correction may impact both balance sheet and income statement accounts, requiring the company to record a transaction that corrects both. Since income statement accounts are closed at the end of every period, the journal entry will contain an entry to the Retained Earnings account. As such, prior period adjustments are reported on a company’s statement of retained earnings as an adjustment to the beginning balance of retained earnings. By directly adjusting beginning retained earnings, the adjustment has no effect on current period net income. The goal is to separate the error correction from the current period’s net income to avoid distorting the current period’s profitability. In other words, prior period adjustments are a way to go back and correct past financial statements that were misstated because of a reporting error.

CONCEPTS IN PRACTICE

According to Kevin LaCroix, additional reporting requirements created by the Sarbanes Oxley Act prompted a surge in 2005 and 2006 of the number of companies that had to make corrections and reissue financial statements. However, since that time, the number of companies making corrections has dropped over 60%, partially due to the number of U.S. companies listed on stock exchanges, and partially due to tighter regulations. The severity of the errors that caused restatements has declined as well, primarily due to tighter regulation, which has forced companies to improve their internal controls.2

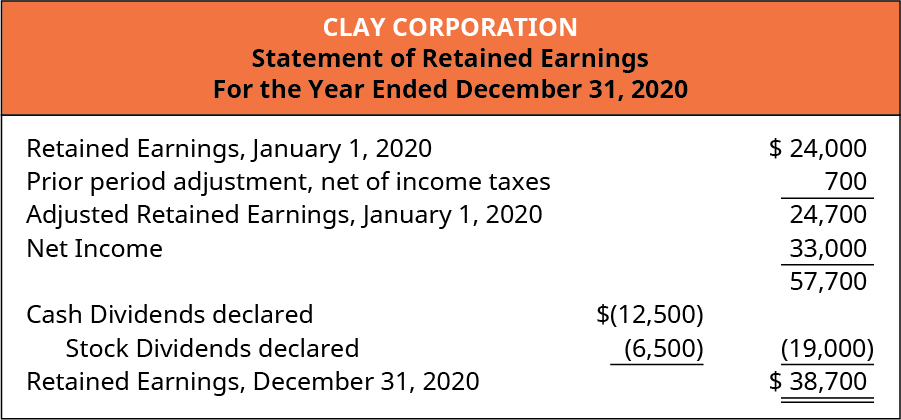

To illustrate how to correct an error requiring a prior period adjustment, assume that in early 2020, Clay Corporation’s controller determined it had made an error when calculating depreciation in the preceding year, resulting in an understatement of depreciation of $1,000. The entry to correct the error contains a decrease to Retained Earnings on the statement of retained earnings for $1,000. Depreciation expense would have been $1,000 higher if the correct depreciation had been recorded. The entry to Retained Earnings adds an additional debit to the total debits that were previously part of the closing entry for the previous year. The credit is to the balance sheet account in which the $1,000 would have been recorded had the correct depreciation entry occurred, in this case, Accumulated Depreciation.

Because the adjustment to retained earnings is due to an income statement amount that was recorded incorrectly, there will also be an income tax effect. The tax effect is shown in the statement of retained earnings in presenting the prior period adjustment. Assuming that Clay Corporation’s income tax rate is 30%, the tax effect of the $1,000 is a $300 (30% × $1,000) reduction in income taxes. The increase in expenses in the amount of $1,000 combined with the $300 decrease in income tax expense results in a net $700 decrease in net income for the prior period. The $700 prior period correction is reported as an adjustment to beginning retained earnings, net of income taxes, as shown below.

Generally accepted accounting principles (GAAP), the set of accounting rules that companies are required to follow for financial reporting, requires companies to disclose in the notes to the financial statements the nature of any prior period adjustment and the related impact on the financial statement amounts.

LINK TO LEARNING

CONCEPTS IN PRACTI CE

Tune into a financial news program like Squawk Box or Mad Money on CNBC or Bloomberg’s. Notice the terminology used to describe the corporations being analyzed. Notice the speed at which topics are discussed. Are these shows for the novice investor? How could this information impact potential investors?

LINK TO LEARNING

KEY TAKEAWAYS

Key Concepts and Summary

- Owner’s equity reflects an owner’s investment value in a company.

- The three forms of business utilize different accounts and transactions relative to owners’ equity.

- Retained earnings is the primary component of a company’s earned capital. It generally consists of the cumulative net income minus any cumulative losses less dividends declared. A statement of retained earnings shows the changes in the retained earnings account during the period.

- Restricted retained earnings is the portion of a company’s earnings that has been designated for a particular purpose due to legal or contractual obligations.

- A company’s board of directors may designate a portion of a company’s retained earnings for a particular purpose such as future expansion, special projects, or as part of a company’s risk management plan. The amount designated is classified as appropriated retained earnings.

- The statement of stockholders’ equity provides the changes between the beginning and ending balances of each of the stockholders’ equity accounts, including retained earnings.

- Prior period adjustments are corrections of errors that occurred on previous periods’ financial statements. They are reported on a company’s statement of retained earnings as an adjustment to the beginning balance.

Footnotes

- 1 Cracker Barrel. Cracker Barrel Old Country Store Annual Report 2017. September 22, 2017. http://investor.crackerbarrel.com/static-files/c05f90b8-1214-4f50-8508-d9a70301f51f

- 2 Kevin M. LaCroix. “Financial Statements Continue to Decline for U.S. Reporting Companies.” The D & O Diary. June 12, 2017. https://www.dandodiary.com/2017/06/articles/sox-generally/financial-restatements-continue-decline-u-s-reporting-companies/

Glossary

- appropriated retained earnings

- portion of a company’s retained earnings designated for a particular purpose such as future expansion, special projects, or as part of a company’s risk management plan

- contributed capital

- owner’s investment (cash and other assets) in the business, which typically comes in the form of common stock

- deficit in retained earnings

- negative or debit balance

- earned capital

- capital earned by the corporation as part of business operations

- owners’ equity

- business owners’ share of the company

- prior period adjustments

- corrections of errors that occurred on previous periods’ financial statements

- restatement

- correction of financial statement amounts due to an accounting error in a prior period

- restricted retained earnings

- portion of a company’s earnings that has been designated for a particular purpose due to legal or contractual obligations

- statement of stockholders’ equity

- provides the changes between the beginning and ending balances of each of the stockholders’ equity accounts during the period

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

(also, equity) business owners’ share of the company

business receives cash or other assets in exchange for ownership in the business (which may be in the form of common stock if the business is organized as a corporation)

capital earned by the corporation as part of business operations

negative or debit balance in retained earnings

portion of a company’s earnings that has been designated for a particular purpose due to legal or contractual obligations

portion of a company’s retained earnings designated for a particular purpose such as future expansion, special projects, or as part of a company’s risk management plan

provides the changes between the beginning and ending balances of each of the stockholders’ equity accounts during the period

corrections of errors that occurred on previous periods’ financial statements

correction of financial statement amounts due to an accounting error in a prior period