LO 3.4 Analyze Business Transactions Using the Accounting Equation and Show the Impact of Business Transactions on Financial Statements

You gained a basic understanding of both the basic and expanded accounting equations, and looked at examples of assets, liabilities, and stockholder’s equity in Define and Examine the Expanded Accounting Equation and Its Relationship to Analyzing Transactions. Now, we can consider some of the transactions a business may encounter. We can review how each transaction would affect the basic accounting equation and the corresponding financial statements.

As discussed in Define and Describe the Initial Steps in the Accounting Cycle, the first step in the accounting cycle is to identify and analyze transactions. Each original source must be evaluated for financial implications. Meaning, will the information contained on this original source affect the financial statements? If the answer is yes, the company will then analyze the information for how it affects the financial statements. For example, if a company receives a cash payment from a customer, the company needs to know how to record the cash payment in a meaningful way to keep its financial statements up to date.

YOUR TURN

You are the accountant for a small computer programming company. You must record the following transactions. What values do you think you will use for each transaction?

- The company purchased a secondhand van to be used to travel to customers. The sellers told you they believe it is worth $12,500 but agreed to sell it to your company for $11,000. You believe the company got a really good deal because the van has a $13,000 Blue Book value.

- Your company purchased its office building five years ago for $175,000. Values of real estate have been rising quickly over the last five years, and a realtor told you the company could easily sell it for $250,000 today. Since the building is now worth $250,000, you are contemplating whether you should increase its value on the books to reflect this estimated current market value.

- Your company has performed a task for a customer. The customer agreed to a minimum price of $2,350 for the work, but if the customer has absolutely no issues with the programming for the first month, the customer will pay you $2,500 (which includes a bonus for work well done). The owner of the company is almost 100% sure she will receive $2,500 for the job done. You have to record the revenue earned and need to decide how much should be recorded.

- The owner of the company believes the most valuable asset for his company is the employees. The service the company provides depends on having intelligent, hardworking, dependable employees who believe they need to deliver exactly what the customer wants in a reasonable amount of time. Without the employees, the company would not be so successful. The owner wants to know if she can include the value of her employees on the balance sheet as an asset.

Solution

- The van must be recorded on the books at $11,000 per the cost principle. That is the price that was agreed to between a willing buyer and seller.

- The cost principle states that you must record an asset on the books for the price you bought it for and then leave it on the books at that value unless there is a specific rule to the contrary. The company purchased the building for $175,000. It must stay on the books at $175,000. Companies are not allowed to increase the value of an asset on their books just because they believe it is worth more.

- You must record the revenue at $2,350 per the rules of conservatism. We do not want to record revenue at $2,500 when we are not absolutely 100% sure that is what we will earn. Recording it at $2,500 might mislead our statement users to think we have earned more revenue than we really have.

- Even though the employees are a wonderful asset for the company, they cannot be included on the balance sheet as an asset. There is no way to assign a monetary value in US dollars to our employees. Therefore, we cannot include them in our assets.

Reviewing and Analyzing Transactions

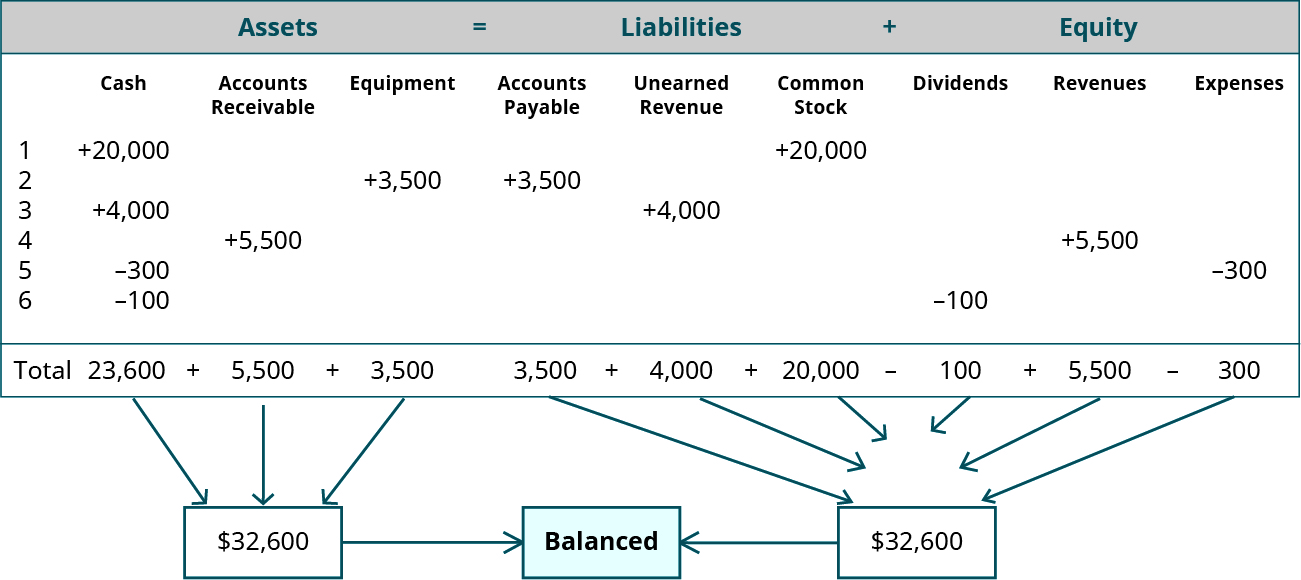

Let us assume our business is a service-based company. We use Lynn Sanders’ small printing company, Printing Plus, as our example. The following are several transactions from this business’s current month:

- Receives $20,000 cash and issues shares of common stock.

- Purchases equipment on account for $3,500, payment due within the month.

- Receives $4,000 cash in advance from a customer for services not yet provided.

- Provides $5,500 in services to a customer who asks to be billed for the services.

- Pays a $300 utility bill with cash.

- Distributed $100 cash in dividends to stockholders.

We now analyze each of these transactions, paying attention to how they impact the accounting equation and corresponding financial statements.

Transaction 1: Receives $20,000 cash and issues shares of common stock.

Analysis: Looking at the accounting equation, we know cash is an asset and common stock is stockholder’s equity. When a company collects cash, this will increase assets because cash is coming into the business. When a company issues common stock, this will increase a stockholder’s equity because the company is receiving assets from owners.

Remember that the accounting equation must remain balanced, and assets need to equal liabilities plus equity. On the asset side of the equation, we show an increase of $20,000. On the liabilities and equity side of the equation, there is also an increase of $20,000, keeping the equation balanced. Changes to assets, specifically cash, will increase assets on the balance sheet and increase cash on the statement of cash flows. Changes to stockholder’s equity, specifically common stock, will increase stockholder’s equity on the balance sheet.

Transaction 2: Purchases equipment on account for $3,500, payment due within the month.

Analysis: We know that the company purchased equipment, which is an asset. We also know that the company purchased the equipment on account, meaning it did not pay for the equipment immediately and asked for payment to be billed instead and paid later. Since the company owes money and has not yet paid, this is a liability, specifically labeled as accounts payable. There is an increase to assets because the company has equipment it did not have before. There is also an increase to liabilities because the company now owes money. The more money the company owes, the more that liability will increase.

The accounting equation remains balanced because there is a $3,500 increase on the asset side, and a $3,500 increase on the liability and equity side. This change to assets will increase assets on the balance sheet. The change to liabilities will increase liabilities on the balance sheet.

Transaction 3: Receives $4,000 cash in advance from a customer for services not yet rendered.

Analysis: We know that the company collected cash, which is an asset. This collection of $4,000 increases assets because money is coming into the business.

The company has yet to provide the service. According to the revenue recognition principle, the company cannot recognize that revenue until it provides the service. Therefore, the company has a liability to the customer to provide the service and must record the liability as unearned revenue. The liability of $4,000 worth of services increases because the company has more unearned revenue than previously.

The equation remains balanced, as assets and liabilities increase. The balance sheet would experience an increase in assets and an increase in liabilities.

Transaction 4: Provides $5,500 in services to a customer who asks to be billed for the services.

Analysis: The customer asked to be billed for the service, meaning the customer did not pay with cash immediately. The customer owes money and has not yet paid, signaling an accounts receivable. Accounts receivable is an asset that is increasing in this case. This customer obligation of $5,500 adds to the balance in accounts receivable.

The company did provide the services. As a result, the revenue recognition principle requires recognition as revenue, which increases equity for $5,500. The increase to assets would be reflected on the balance sheet. The increase to equity would affect three statements. The income statement would see an increase to revenues, changing net income (loss). Net income (loss) is computed into retained earnings on the statement of retained earnings. This change to retained earnings is shown on the balance sheet under stockholder’s equity.

Transaction 5: Pays a $300 utility bill with cash.

Analysis: The company paid with cash, an asset. Assets are decreasing by $300 since cash was used to pay for this utility bill. The company no longer has that money.

Utility payments are generated from bills for services that were used and paid for within the accounting period, thus recognized as an expense. The expense decreases equity by $300. The decrease to assets, specifically cash, affects the balance sheet and statement of cash flows. The decrease to equity as a result of the expense affects three statements. The income statement would see a change to expenses, changing net income (loss). Net income (loss) is computed into retained earnings on the statement of retained earnings. This change to retained earnings is shown on the balance sheet under stockholder’s equity.

Transaction 6: Distributed $100 cash in dividends to stockholders.

Analysis: The company paid the distribution with cash, an asset. Assets decrease by $100 as a result. Dividends affect equity and, in this case, decrease equity by $100. The decrease to assets, specifically cash, affects the balance sheet and statement of cash flows. The decrease to equity because of the dividend payout affects the statement of retained earnings by reducing ending retained earnings, and the balance sheet by reducing stockholder’s equity.

Let’s summarize the transactions and make sure the accounting equation has remained balanced. Shown are each of the transactions.

As you can see, assets total $32,600, while liabilities added to equity also equal $32,600. Our accounting equation remains balanced. In Use Journal Entries to Record Transactions and Post to T-Accounts, we add other elements to the accounting equation and expand the equation to include individual revenue and expense accounts.

YOUR TURN

Debbie’s Dairy Farm had the following transactions:

- Debbie ordered shelving worth $750.

- Debbie’s selling price on a gallon of milk is $3.00. She finds out that most local stores are charging $3.50. Based on this information, she decides to increase her price to $3.25. She has an employee put a new price sticker on each gallon.

- A customer buys a gallon of milk paying cash.

- The shelving is delivered with an invoice for $750.

Which events will be recorded in the accounting system?

Solution

- Debbie did not yet receive the shelving—it has only been ordered. As of now there is no new asset owned by the company. Since the shelving has not yet been delivered, Debbie does not owe any money to the other company. Debbie will not record the transaction.

- Changing prices does not have an impact on the company at the time the price is changed. All that happened was that a new price sticker was placed on the milk. Debbie still has all the milk and has not received any money. Debbie will not record the transaction.

- Debbie now has a transaction to record. She has received cash and the customer has taken some of her inventory of milk. She has an increase in one asset (cash) and a decrease in another asset (inventory.) She also has earned revenue.

- Debbie has taken possession of the shelving and is the legal owner. She also has an increase in her liabilities as she accepted delivery of the shelving but has not paid for it. Debbie will record this transaction.

KEY TAKEAWAYS

Key Concepts and Summary

- Both the basic and the expanded accounting equations are useful in analyzing how any transaction affects a company’s financial statements.

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting