LO 6.5 Discuss and Record Transactions Applying the Two Commonly Used Freight-In Methods

When you buy merchandise online, shipping charges are usually one of the negotiated terms of the sale. As a consumer, anytime the business pays for shipping, it is welcomed. For businesses, shipping charges bring both benefits and challenges, and the terms negotiated can have a significant impact on inventory operations.

IFRS CONNECTION

Companies applying US GAAP as well as those applying IFRS can choose either a perpetual or periodic inventory system to track purchases and sales of inventory. While the tracking systems do not differ between the two methods, they have differences in when sales transactions are reported. If goods are shipped FOB shipping point, under IFRS, the total selling price of the item would be allocated between the item sold (as sales revenue) and the shipping (as shipping revenue). Under US GAAP, the seller can elect whether the shipping costs will be an additional component of revenue (separate performance obligation) or whether they will be considered fulfillment costs (expensed at the time shipping as shipping expense). In an FOB destination scenario, the shipping costs would be considered a fulfillment activity and expensed as incurred rather than be treated as a part of revenue under both IFRS and US GAAP.

Example

Wally’s Wagons sells and ships 20 deluxe model wagons to Sam’s Emporium for $5,000. Assume $400 of the total costs represents the costs of shipping the wagons and consider these two scenarios: (1) the wagons are shipped FOB shipping point or (2) the wagons are shipped FOB destination. If Wally’s is applying IFRS, the $400 shipping is considered a separate performance obligation, or shipping revenue, and the other $4,600 is considered sales revenue. Both revenues are recorded at the time of shipping and the $400 shipping revenue is offset by a shipping expense. If Wally’s used US GAAP instead, they would choose between using the same treatment as described under IFRS or considering the costs of shipping to be costs of fulfilling the order and expense those costs at the time they are incurred. In this latter case, Wally’s would record Sales Revenue of $5,000 at the time the wagons are shipped and $400 as shipping expense at the time of shipping. Notice that in both cases, the total net revenues are the same $4,600, but the distribution of those revenues is different, which impacts analyses of sales revenue versus total revenues. What happens if the wagons are shipped FOB destination instead? Under both IFRS and US GAAP, the $400 shipping would be treated as an order fulfillment cost and recorded as an expense at the time the goods are shipped. Revenue of $5,000 would be recorded at the time the goods are received by Sam’s emporium.

Financial Statement Presentation of Cost of Goods Sold

IFRS allows greater flexibility in the presentation of financial statements, including the income statement. Under IFRS, expenses can be reported in the income statement either by nature (for example, rent, salaries, depreciation) or by function (such as COGS or Selling and Administrative). US GAAP has no specific requirements regarding the presentation of expenses, but the SEC requires that expenses be reported by function. Therefore, it may be more challenging to compare merchandising costs (cost of goods sold) across companies if one company’s income statement shows expenses by function and another company shows them by nature.

The Basics of Freight-in Versus Freight-out Costs

Shipping is determined by contract terms between a buyer and seller. There are several key factors to consider when determining who pays for shipping, and how it is recognized in merchandising transactions. The establishment of a transfer point and ownership indicates who pays the shipping charges, who is responsible for the merchandise, on whose balance sheet the assets would be recorded, and how to record the transaction for the buyer and seller.

Ownership of inventory refers to which party owns the inventory at a particular point in time—the buyer or the seller. One particularly important point in time is the point of transfer, when the responsibility for the inventory transfers from the seller to the buyer. Establishing ownership of inventory is important to determine who pays the shipping charges when the goods are in transit as well as the responsibility of each party when the goods are in their possession. Goods in transit refers to the time in which the merchandise is transported from the seller to the buyer (by way of delivery truck, for example). One party is responsible for the goods in transit and the costs associated with transportation. Determining whether this responsibility lies with the buyer or seller is critical to determining the reporting requirements of the retailer or merchandiser.

Freight-in refers to the shipping costs for which the buyer is responsible when receiving shipment from a seller, such as delivery and insurance expenses. When the buyer is responsible for shipping costs, they recognize this as part of the purchase cost. This means that the shipping costs stay with the inventory until it is sold. The cost principle requires this expense to stay with the merchandise as it is part of getting the item ready for sale from the buyer’s perspective. The shipping expenses are held in inventory until sold, which means these costs are reported on the balance sheet in Merchandise Inventory. When the merchandise is sold, the shipping charges are transferred with all other inventory costs to Cost of Goods Sold on the income statement.

For example, California Business Solutions (CBS) may purchase computers from a manufacturer and part of the agreement is that CBS (the buyer) pays the shipping costs of $1,000. CBS would record the following entry to recognize freight-in.

Merchandise Inventory increases (debit), and Cash decreases (credit), for the entire cost of the purchase, including shipping, insurance, and taxes. On the balance sheet, the shipping charges would remain a part of inventory.

Freight-out refers to the costs for which the seller is responsible when shipping to a buyer, such as delivery and insurance expenses. When the seller is responsible for shipping costs, they recognize this as a delivery expense. The delivery expense is specifically associated with selling and not daily operations; thus, delivery expenses are typically recorded as a selling and administrative expense on the income statement in the current period.

For example, CBS may sell electronics packages to a customer and agree to cover the $100 cost associated with shipping and insurance. CBS would record the following entry to recognize freight-out.

Delivery Expense increases (debit) and Cash decreases (credit) for the shipping cost amount of $100. On the income statement, this $100 delivery expense will be grouped with Selling and Administrative expenses.

LINK TO LEARNING

Discussion and Application of FOB Destination

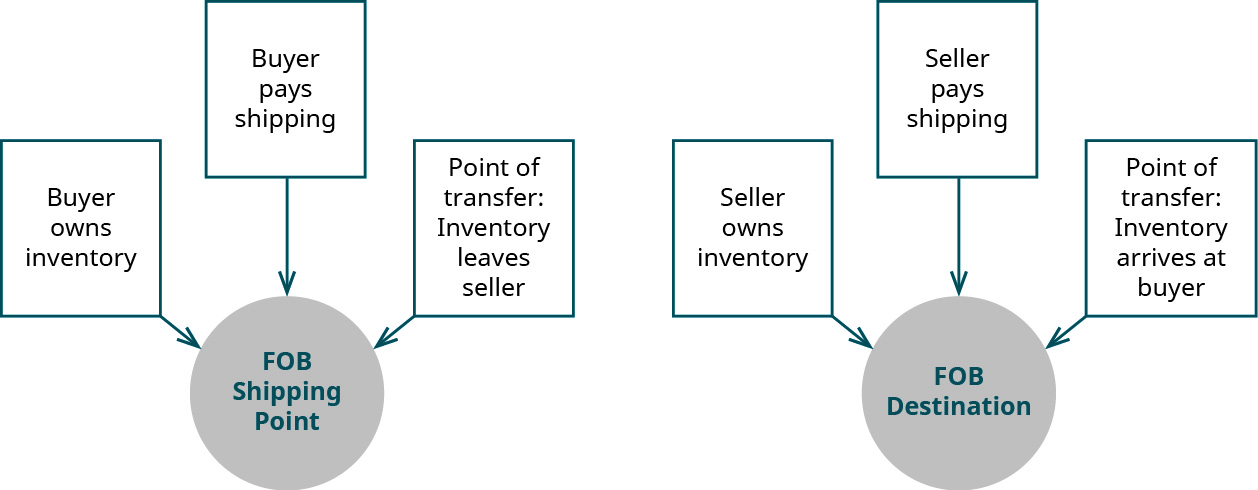

As you’ve learned, the seller and buyer will establish terms of purchase that include the purchase price, taxes, insurance, and shipping charges. So, who pays for shipping? On the purchase contract, shipping terms establish who owns inventory in transit, the point of transfer, and who pays for shipping. The shipping terms are known as “free on board,” or simply FOB. Some refer to FOB as the point of transfer, but really, it incorporates more than simply the point at which responsibility transfers. There are two FOB considerations: FOB Destination and FOB Shipping Point.

If FOB destination point is listed on the purchase contract, this means the seller pays the shipping charges (freight-out). This also means goods in transit belong to, and are the responsibility of, the seller. The point of transfer is when the goods reach the buyer’s place of business.

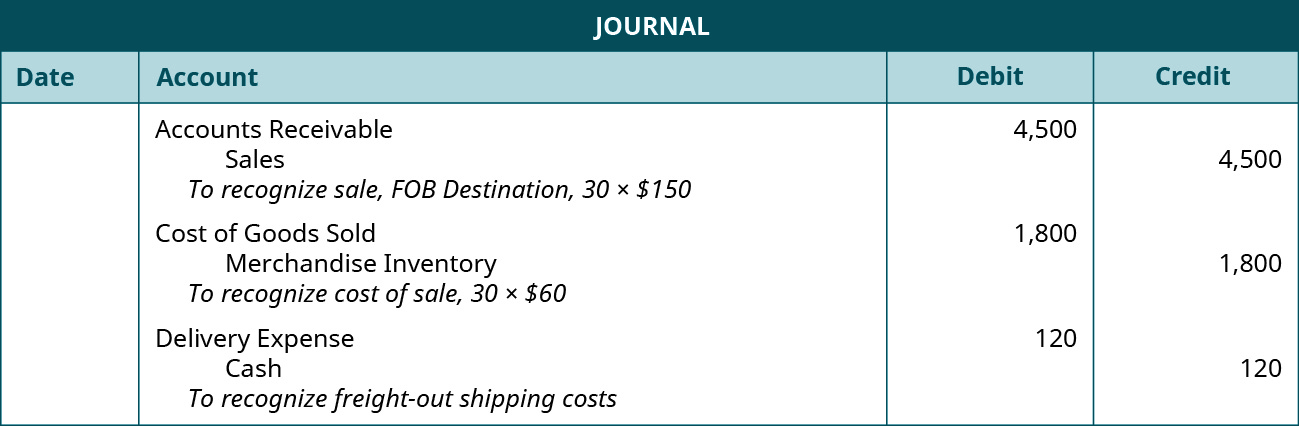

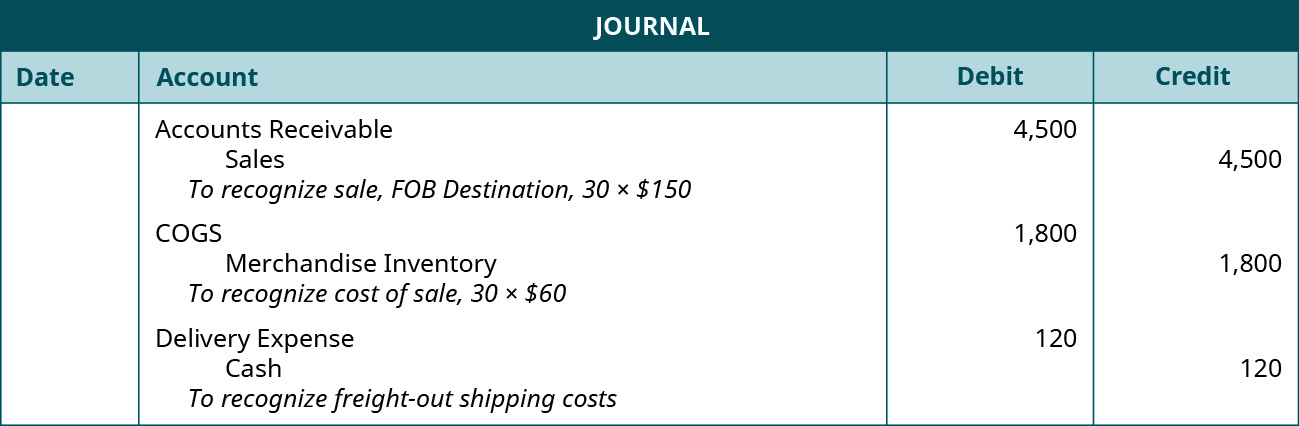

To illustrate, suppose CBS sells 30 landline telephones at $150 each on credit at a cost of $60 per phone. On the sales contract, FOB Destination is listed as the shipping terms, and shipping charges amount to $120, paid as cash directly to the delivery service. The following entries occur.

Accounts Receivable (debit) and Sales (credit) increases for the amount of the sale (30 × $150). Cost of Goods Sold increases (debit) and Merchandise Inventory decreases (credit) for the cost of sale (30 × $60). Delivery Expense increases (debit) and Cash decreases (credit) for the delivery charge of $120.

Discussion and Application of FOB Shipping Point

If FOB shipping point is listed on the purchase contract, this means the buyer pays the shipping charges (freight-in). This also means goods in transit belong to, and are the responsibility of, the buyer. The point of transfer is when the goods leave the seller’s place of business.

Suppose CBS buys 40 tablet computers at $60 each on credit. The purchase contract shipping terms list FOB Shipping Point. The shipping charges amount to an extra $5 per tablet computer. All other taxes, fees, and insurance are included in the purchase price of $60. The following entry occurs to recognize the purchase.

Merchandise Inventory increases (debit) and Accounts Payable increases (credit) by the amount of the purchase, including all shipping, insurance, taxes, and fees [(40 × $60) + (40 × $5)].

The Figure below shows a comparison of shipping terms.

THINK IT THROUGH

You are a seller and conduct business with several customers who purchase your goods on credit. Your standard contract requires an FOB Shipping Point term, leaving the buyer with the responsibility for goods in transit and shipping charges. One of your long-term customers asks if you can change the terms to FOB Destination to help them save money.

Do you change the terms, why or why not? What positive and negative implications could this have for your business, and your customer? What, if any, restrictions might you consider if you did change the terms?

KEY TAKEAWAYS

Key Concepts and Summary

- Establishing ownership of inventory is important because it helps determine who is responsible for shipping charges, goods in transit, and transfer points. Ownership also determines reporting requirements for the buyer and seller. The buyer is responsible for the merchandise, and the cost of shipping, insurance, purchase price, taxes, and fees are held in inventory in its Merchandise Inventory account. The buyer would record an increase (debit) to Merchandise Inventory and either a decrease to Cash or an increase to Accounts Payable (credit) depending on payment method.

- FOB Shipping Point means the buyer should record the merchandise as inventory when it leaves the seller’s location. FOB destination means the seller should continue to carry the merchandise in inventory until it reaches the buyer’s location. This becomes really important at year-end when each party is trying to determine their actual balance sheet inventory accounts.

- FOB Destination means the seller is responsible for the merchandise, and the cost of shipping is expensed immediately in the period as a delivery expense. The seller would record an increase (debit) to Delivery Expense, and a decrease to Cash (credit).

- In FOB Destination, the seller is responsible for the shipping charges and like expenses. The point of transfer is when the merchandise reaches the buyer’s place of business, and the seller owns the inventory in transit.

- In FOB Shipping Point, the buyer is responsible for the shipping charges and like expenses. The point of transfer is when the merchandise leaves the seller’s place of business, and the buyer owns the inventory in transit.

Glossary

- FOB destination point

- transportation terms whereby the seller transfers ownership and financial responsibility at the time of delivery

- FOB shipping point

- transportation terms whereby the seller transfers ownership and financial responsibility at the time of shipment

- freight-in

- buyer is responsible for when receiving shipment from a seller

- freight-out

- seller is responsible for when shipping to a buyer

- goods in transit

- time in which the merchandise is being transported from the seller to the buyer

- ownership of inventory

- which party owns the inventory at a particular point in time, the buyer or the seller

- point of transfer

- when the responsibility for the inventory transfers from the seller to the buyer

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

which party owns the inventory at a particular point in time, the buyer or the seller

when the responsibility for the inventory transfers from the seller to the buyer

time in which the merchandise is being transported from the seller to the buyer

buyer is responsible for when receiving shipment from a seller

seller is responsible for when shipping to a buyer

transportation terms whereby the seller transfers ownership and financial responsibility at the time of delivery

transportation terms whereby the seller transfers ownership and financial responsibility at the time of shipment