LO 5.3 Apply the Results from the Adjusted Trial Balance to Compute Current Ratio and Working Capital Balance, and Explain How These Measures Represent Liquidity

In The Adjustment Process, we were introduced to the idea of accrual-basis accounting, where revenues and expenses must be recorded in the accounting period in which they were earned or incurred, no matter when cash receipts or outlays occur. We also discussed cash-basis accounting, where income and expenses are recognized when receipts and disbursements occur. In this chapter, we go into more depth about why a company may choose accrual-basis accounting as opposed to cash-basis accounting.

LINK TO LEARNING

Cash Basis versus Accrual Basis Accounting

There are several reasons accrual-basis accounting is preferred to cash-basis accounting. Accrual-basis accounting is required by US generally accepted accounting principles (GAAP), as it typically provides a better sense of the financial well-being of a company. Accrual-based accounting information allows management to analyze a company’s progress, and management can use that information to improve their business. Accrual accounting is also used to assist companies in securing financing, because banks will typically require a company to provide accrual-basis financial income statements. The Internal Revenue Service might also require businesses to report using accrual basis information when preparing tax returns. In addition, companies with inventory must use accrual-based accounting for income tax purposes, though there are exceptions to the general rule.

So why might a company use cash-basis accounting? Companies that do not sell stock publicly can use cash-basis instead of accrual-basis accounting for internal-management purposes and externally, as long as the Internal Revenue Service does not prevent them from doing so, and they have no other reasons such as agreements per a bank loan. Cash-basis accounting is a simpler accounting system to use than an accrual-basis accounting system when tracking real-time revenues and expenses.

Let’s take a look at one example illustrating why accrual-basis accounting might be preferred to cash-basis accounting.

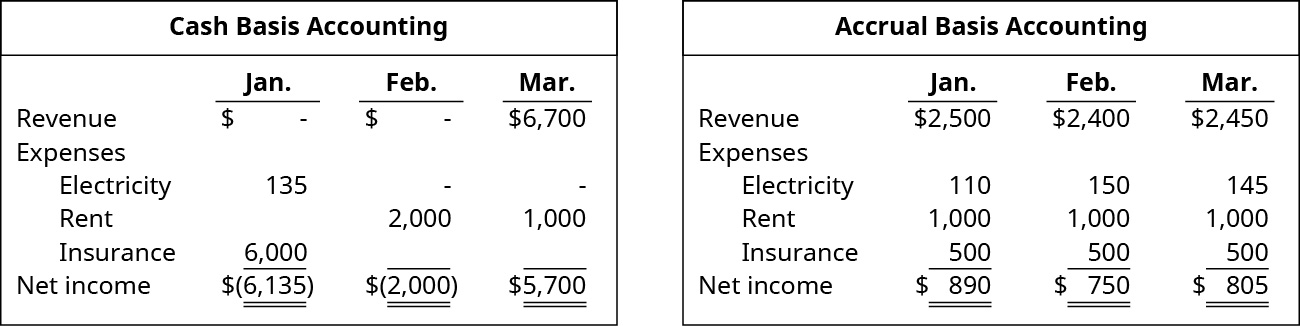

In the current year, a company had the following transactions:

| January to March Transactions | |

|---|---|

| Date | Transaction |

| Jan. 1 | Annual insurance policy purchased for $6,000 cash |

| Jan. 8 | Sent payment for December’s electricity bill, $135 |

| Jan. 15 | Performed services worth $2,500; customer asked to be billed |

| Jan. 31 | Electricity used during January is estimated at $110 |

| Feb. 16 | Realized you forgot to pay January’s rent, so sent two months’ rent, $2,000 |

| Feb. 20 | Performed services worth $2,400; customer asked to be billed |

| Feb. 28 | Electricity used during February is estimated at $150 |

| Mar. 2 | Paid March rent, $1,000 |

| Mar. 10 | Received all money owed from services performed in January and February |

| Mar. 14 | Performed services worth $2,450. Received $1,800 cash |

| Mar. 30 | Electricity used during March is estimated at $145 |

IFRS CONNECTION

Regardless of whether a company uses US GAAP or International Financial Reporting Standards (IFRS), the closing and post-closing processes are the same. However, the results generated by these processes are not the same. These differences can be seen most easily in the ratios formulated from the financial statement information and used to assess various financial qualities of a company.

You have learned about the current ratio, which is used to assess a company’s ability to pay debts as they come due. How could the use of IFRS versus US GAAP affect this ratio? US GAAP and IFRS most frequently differ on how certain transactions are measured, or on the timing of measuring and reporting that transaction. You will later learn about this in more detail, but for now we use a difference in inventory measurement to illustrate the effect of the two different sets of standards on the current ratio.

US GAAP allows for three different ways to measure ending inventory balances: first-in, first-out (FIFO); last-in, first-out (LIFO); and weighted average. IFRS only allows for FIFO and weighted average. If the prices of inventory being purchased are rising, the FIFO method will result in a higher value of ending inventory on the Balance Sheet than would the LIFO method.

Think about this in the context of the current ratio. Inventory is one component of current assets: the numerator of the ratio. The higher the current assets (numerator), the higher is the current ratio. Therefore, if you calculated the current ratio for a company that applied US GAAP, and then recalculated the ratio assuming the company used IFRS, you would get not only different numbers for inventory (and other accounts) in the financial statements, but also different numbers for the ratios.

This idea illustrates the impact the application of an accounting standard can have on the results of a company’s financial statements and related ratios. Different standards produce different results. Throughout the remainder of this course, you will learn more details about the similarities and differences between US GAAP and IFRS, and how these differences impact financial reporting.

Remember, in a cash-basis system you will record the revenue when the money is received no matter when the service is performed. There was no money received from customers in January or February, so the company, under a cash-basis system, would not show any revenue in those months. In March they received the $2,500 customers owed from January sales, $2,400 from customers for February sales, and $1,800 from cash sales in March. This is a total of $6,700 cash received from customers in March. Since the cash was received in March, the cash-basis system would record revenue in March.

In accrual accounting, we record the revenue as it is earned. There was $2,500 worth of service performed in January, so that will show as revenue in January. The $2,400 earned in February is recorded in February, and the $2,450 earned in March is recorded as revenue in March. Remember, it does not matter whether or not the cash came in.

For expenses, the cash-basis system is going to record an expense the day the payment leaves company hands. In January, the company purchased an insurance policy. The insurance policy is for the entire year, but since the cash went to the insurance company in January, the company will record the entire amount as an expense in January. The company paid the December electric bill in January. Even though the electricity was used to earn revenue in December, the company will record it as an expense in January. Electricity used in January, February, and March to help earn revenue in those months will show no expense because the bill has not been paid. The company forgot to pay January’s rent in January, so no rent expense is recorded in January. However, in February there is $2,000 worth of rent expense because the company paid for the two months in February.

Under accrual accounting, expenses are recorded when they are incurred and not when paid. Electricity used in a month to help earn revenue is recorded as an expense in that month whether the bill is paid or not. The same is true for rent expense. Insurance expense is spread out over 12 months, and each month 1/12 of the total insurance cost is expensed. The comparison of cash-basis and accrual-basis income statements is presented in (Figure).

CONCEPTS IN PRACTICE

One method used by everyone who evaluates financial statements is to calculate financial ratios. Financial ratios take numbers from your income statements and/or your balance sheet to evaluate important financial outcomes that will impact user decisions.

There are ratios to evaluate your liquidity, solvency, profitability, and efficiency. Liquidity ratios look at your ability to pay the debts that you owe in the near future. Solvency will show if you can pay your bills not only in the short term but also in the long term. Profitability ratios are calculated to see how much profit is being generated from a company’s sales. Efficiency ratios will be calculated to see how efficient a company is using its assets in running its business. You will be introduced to these ratios and how to interpret them throughout this course.

Compare the two sets of income statements. The cash-basis system looks as though no revenue was earned in the first two months, and expenses were excessive. Then in March it looks like the company earned a lot of revenue. How realistic is this picture? Now look at the accrual basis figures. Here you see a better picture of what really happened over the three months. Revenues and expenses stayed relatively even across periods.

This comparison can show the dangers of reporting in a cash-basis system. In a cash-basis system, the timing of cash flows can make the business look very profitable one month and not profitable the next. If your company was having a bad year and you do not want to report a loss, just do not pay the bills for the last month of the year and you can suddenly show a profit in a cash-basis system. In an accrual-basis system, it does not matter if you do not pay the bills, you still need to record the expenses and present an income statement that accurately portrays what is happening in your company. The accrual-basis system lends itself to more transparency and detail in reporting. This detail is carried over into what is known as a classified balance sheet.

The Classified Balance Sheet

A classified balance sheet presents information on your balance sheet in a more informative structure, where asset and liability categories are divided into smaller, more detailed sections. Classified balance sheets show more about the makeup of our assets and liabilities, allowing us to better analyze the current health of our company and make future strategic plans.

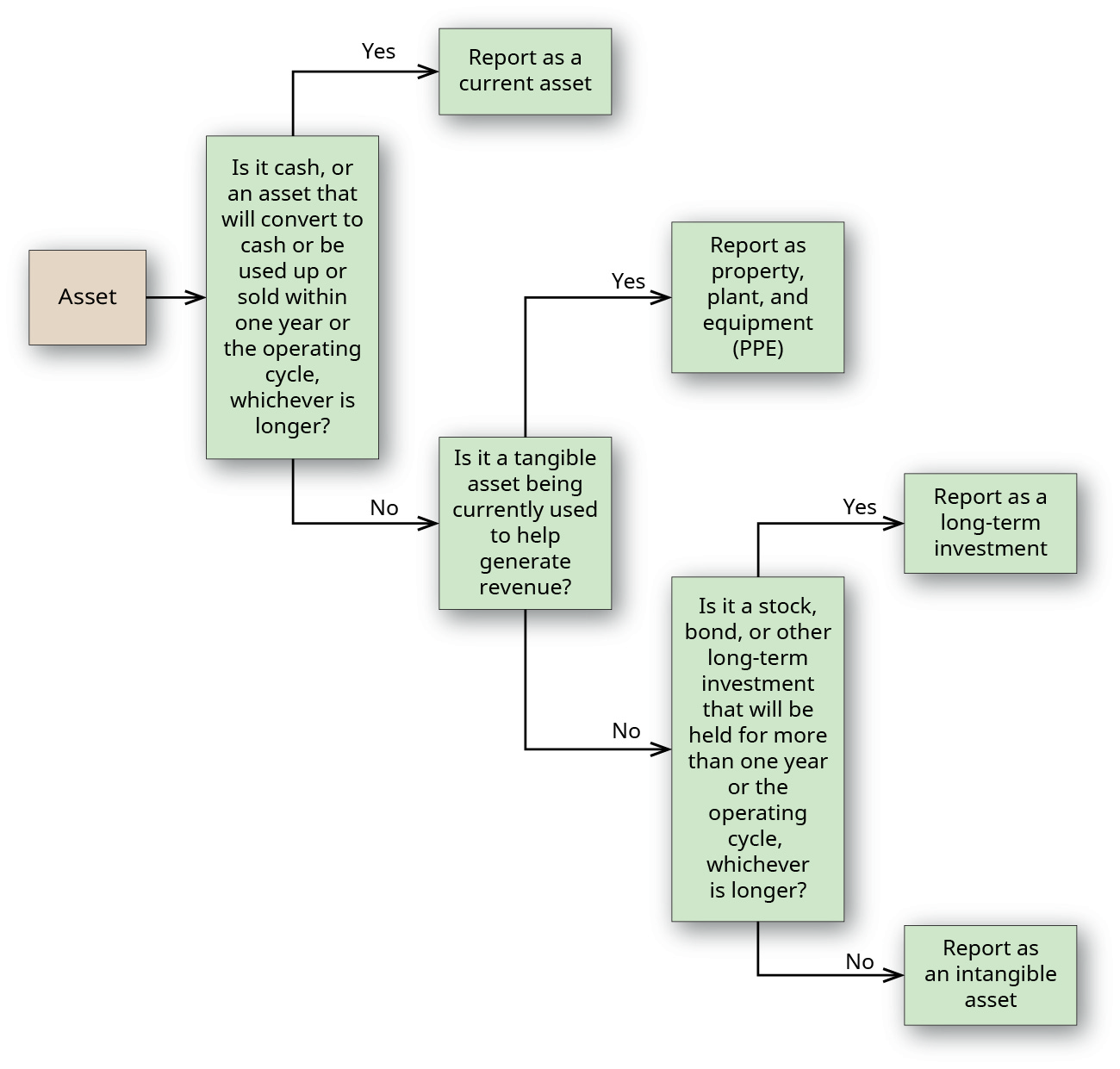

Assets can be categorized as current; property, plant, and equipment; long-term investments; intangibles; and, if necessary, other assets. As you learned in Introduction to Financial Statements, a current asset (also known as a short-term asset) is any asset that will be converted to cash, sold, or used up within one year, or one operating cycle, whichever is longer. An operating cycle is the amount of time it takes a company to use its cash to provide a product or service and collect payment from the customer ((Figure)). For a merchandising firm that sells inventory, an operating cycle is the time it takes for the firm to use its cash to purchase inventory, sell the inventory, and get its cash back from its customers.

LINK TO LEARNING

Newport News Shipbuilding is an American shipbuilder located in Newport News, Virginia. According to information provided by the company, the company has designed and built 30 aircraft carriers in the past 75 years. That is 30 carriers in 75 years. Newport News constructed the USS Gerald R. Ford. It took the company eight years to build the carrier, christening it in 2013. The ship then underwent rigorous testing until it was finally delivered to its home port, Naval Station Norfolk in 2017. That is 12 years after work commenced on the project.

With large shipbuilding projects that take many years to complete, the operating cycle for this type of company could expand beyond a year mark, and Newport News would use this longer operating cycle when dividing current and long-term assets and liabilities.

Learn more about Newport News and its parent company Huntington Ingalls Industries and see a time-lapse video of the construction of the carrier. You can easily tell the passage of time if you watch the snow come and go in the video.

If an asset does not meet the requirements of a current asset, then it is classified as a long-term (AKA noncurrent) asset. It can be further defined as property, plant, and equipment; a long-term investment; or an intangible asset ((Figure)). Property, plant, and equipment are tangible assets (those that have a physical presence) held for more than one operating cycle or one year, whichever is longer. A long-term investment is stocks, bonds, or other types of investments that management intends to hold for more than one operating cycle or one year, whichever is longer. Intangible assets do not have a physical presence but give the company a long-term future benefit. Some examples include patents, copyrights, and trademarks.

Liabilities are classified as either current liabilities or long-term (AKA noncurrent) liabilities. Liabilities also use the one year, or one operating cycle, for the cut-off between current and noncurrent. As we first discussed in Prepare financial statements using the adjusted trial balance, if the debt is due within one year or one operating cycle, whichever is longer, the liability is a current liability. If the debt is settled outside one year or one operating cycle, whichever is longer, the liability is a long-term liability.

YOUR TURN

Classify each of the following assets as current asset; property, plant, and equipment; long-term investment; or intangible asset.

- machine

- patent

- supplies

- building

- investment in bonds with intent to hold until maturity in 10 years

- copyright

- land being held for future office

- prepaid insurance

- accounts receivable

- investment in stock that will be held for six months

Solution

A. property, plant, and equipment. B. intangible asset. C. current asset. D. property, plant, and equipment. E. long-term investment. F. intangible asset. G. long-term investment. H. current asset. I. current asset. J. current asset.

The land is considered a long-term investment, because it is not land being used currently by the company to earn revenue. Buying real estate is an investment. If the company decided in the future that it was not going to build the new office, it could sell the land and would probably be able to sell the land for more than it was purchased for, because the value of real estate tends to go up over time. But like any investment, there is the risk that the land might actually go down in value.

The investment in stock that we only plan to hold for six months will be called a marketable security in the current asset section of the balance sheet.

As an example, the balance sheet in (Figure) is classified.

CONTINUING APPLICATION AT WORK

Interim reporting helps determine how well a company is performing at a given time during the year. Some companies revise their earnings estimates depending on how profitable the company has been up until a certain point in time. The grocery industry, which includes both private and publicly traded companies, performs the same exercise.

However, grocery companies use such information to inform other important business decisions. Consider the last time you walked through the grocery store and purchased your favorite brand but found another item out of stock. What if the next time you shop, the product you loved is no longer carried, but the out-of-stock item is available?

Grocery store profitably is based on small margins of revenue on a multitude of products. The bar codes scanned at checkout not only provide the price of a product but also track how much inventory has been sold. The grocery store analyzes such information to determine how quickly the product turns over, which drives profit on small margins. If a product sells well, the store might stock it all of the time, but if a product does not sell quickly enough, it could be discontinued.

Using Classified Balance Sheets to Evaluate Liquidity

Categorizing assets and liabilities on a balance sheet helps a company evaluate its business. One way a company can evaluate its business is with financial statement ratios. We consider two measures of liquidity, working capital, and the current ratio. Let’s first explore this idea of liquidity.

We first described liquidity in Prepare financial statements using the adjusted trial balance, as the ability to convert assets into cash. Liquidity is a company’s ability to convert assets into cash in order to meet short-term cash needs, so it is very important for a company to remain liquid. A critical piece of information to remember at this point is that most companies use the accrual accounting method to determine and maintain their accounting records. This fact means that even with a positive income position, as reflected by its income statement, a company can go bankrupt due to poor cash flow. It is also important to note that even if a company has a lot of cash, it may still be in bankruptcy trouble if all or much of that cash is borrowed. According to an article published in Money magazine, one in four small businesses fail because of cash flow issues.1 They are making a profit and seem financially healthy but do not have cash when needed.

Companies should analyze liquidity constantly to avoid cash shortages that may result in a need for a short-term loan. Intermittently taking out a short-term loan is often expected, but a company cannot keep coming up short on cash every year if it is going to remain liquid. A seasonal business, such as a specialized holiday retailer, may require a short-term loan to continue its operations during slower revenue-generating periods. Companies will use numbers from their classified balance sheet to test for liquidity. They want to make sure they have enough current assets to pay their current liabilities. Only cash is used to directly pay liabilities, but other current assets, such as accounts receivable or short-term investments, might be sold for cash, converted to cash, or used to bring in cash to pay liabilities.

ETHICAL CONSIDERATIONS

How does a company like Lehman Brothers Holdings, with over $639 billion in assets and $613 billion in liabilities, go bankrupt? That question still confuses many, but it comes down to the fact that having assets recorded on the books at their purchase price is not the same as the immediate value of the assets. Lehman Brothers had a liquidity crisis that led to a solvency crisis, because Lehman Brothers could not sell the assets on its books at book value to cover its short-term cash demands. Matt Johnston, in an article for the online publication Coinmonks, puts it simply: “Liquidity is all about being able to access cash when it’s needed. If you can settle your current obligations with ease, you’ve got liquidity. If you’ve got debts coming due and you don’t have the cash to settle them, then you’ve got a liquidity crisis.”2 Continuing this Coinmonks discussion, the inability to timely pay debts leads to a business entity becoming insolvent because bills cannot be paid on time and assets need to be written down. When Lehman Brothers could not timely pay their bills in 2008, it went bankrupt, sending a shock throughout the entire banking system. Accountants need to understand the differences between net worth, equity, liquidity, and solvency, and be able to inform stakeholders of their organization’s actual financial position, not just the recorded numbers on the balance sheet.

Two calculations a company might use to test for liquidity are working capital and the current ratio. Working capital, which was first described in Prepare financial statements using the adjusted trial balance, is found by taking the difference between current assets and current liabilities.

A positive outcome means the company has enough current assets available to pay its current liabilities or current debts. A negative outcome means the company does not have enough current assets to cover its current liabilities and may have to arrange short-term financing. Though a positive working capital is preferred, a company needs to make sure that there is not too much of a difference between current assets and current liabilities. A company that has a high working capital might have too much money in current assets that could be used for other company investments. Things such as industry and size of a company will dictate what type of margin is best.

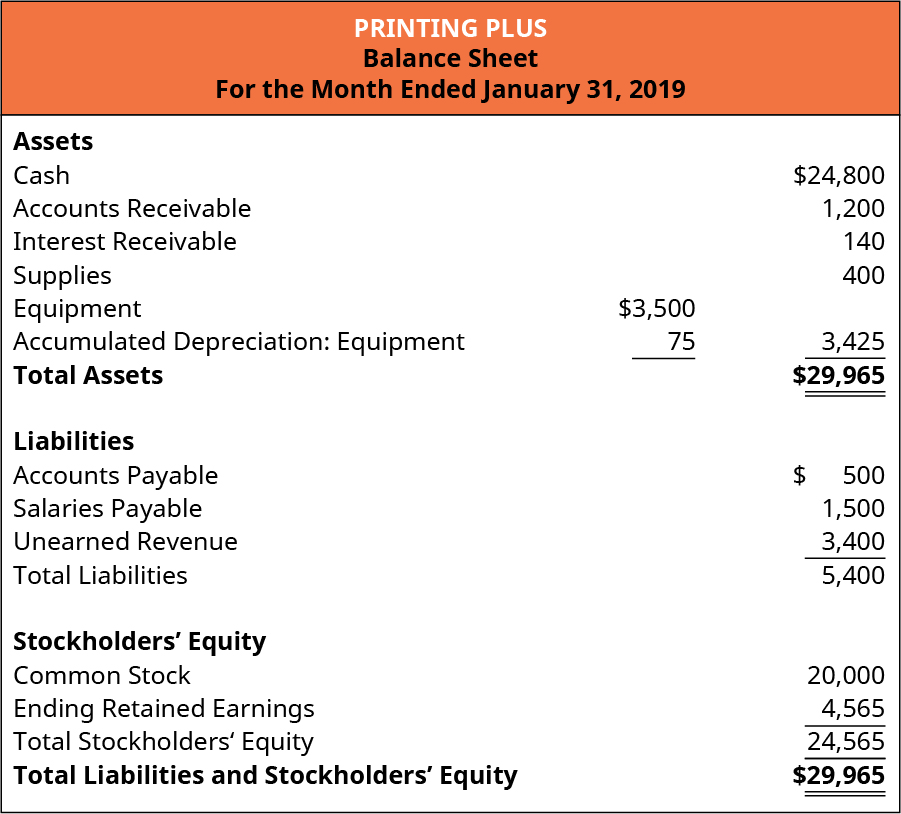

Let’s consider Printing Plus and its working capital ((Figure)).

Printing Plus’s current assets include cash, accounts receivable, interest receivable, and supplies. Their current liabilities include accounts payable, salaries payable, and unearned revenue. The following is the computation of working capital:

This means that you have more than enough working capital to pay the current liabilities your company has recorded. This figure may seem high, but remember that this is the company’s first month of operations and this much cash may need to be available for larger, long-term asset purchases. However, there is also the possibility that the company might choose to identify long-term financing options for the acquisition of expensive, long-term assets, assuming that it can qualify for the increased debt.

Notice that part of the current liability calculation is unearned revenue. If a company has a surplus of unearned revenue, it can sometimes get away with less working capital, as it will need less cash to pay its bills. However, the company must be careful, since the cash was recorded before providing the services or products associated with the unearned revenue. This relationship is why the unearned revenue was initially created, and there often will be necessary cash outflows associated with meeting the terms of the unearned revenue creation.

Companies with inventory will usually need a higher working capital than a service company, as inventory can tie up a large amount of a company’s cash with less cash available to pay its bills. Also, small companies will normally need a higher working capital than larger companies, because it is harder for smaller companies to get loans, and they usually pay a higher interest rate.

LINK TO LEARNING

The current ratio (also known as the working capital ratio), which was first described in Prepare financial statements using the adjusted trial balance, tells a company how many times over company current assets can cover current liabilities. It is found by dividing current assets by current liabilities and is calculated as follows:

For example, if a company has current assets of $20,000 and current liabilities of $10,000, its current ratio is $20,000/$10,000 = two times. This means the company has enough current assets to cover its current liabilities twice. Ideally, many companies would like to maintain a 1.5:2 times current assets over current liabilities ratio. However, depending on the company’s function or purpose, an optimal ratio could be lower or higher than the previous recommendation. For example, many utilities do not have large fluctuations in anticipated seasonal current ratios, so they might decide to maintain a current ratio of 1.25:1.5 times current assets over current liabilities ratio, while a high-tech startup might want to maintain a ratio of 2.5:3 times current assets over current liabilities ratio.

The current ratio for Printing Plus is $26,540/$5,400 = 4.91 times. That is a very high current ratio, but since the business was just started, having more cash might allow the company to make larger purchases while still paying its liabilities. However, this ratio might be a result of short-term conditions, so the company is advised to still plan on maintaining a ratio that is considered both rational and not too risky.

Using ratios for a single year does not provide a broad picture. A company will get much better information if it compares the working capital and current ratio numbers for several years so it can see increases, decreases, and where numbers remain fairly consistent. Companies can also benefit from comparing this financial data to that of other companies in the industry.

ETHICAL CONSIDERATIONS

Newly hired accountants are often sat at a computer to work off of a dashboard, which is a computer screen where entries are made into the accounting system. New accountants working with modern accounting software may not be aware that their software uses the debit and credit system you learned about, and that the system may automatically close the books without the accountant’s review of closing entries. Manually closing the books gives accountants a chance to review the balances of different accounts; if accountants do not review the entries, they will not know what is occurring in the accounting system or in their organization’s financial statements.

Many accounting systems automatically close the books if the command is made in the system. While debits and credits are being entered and may not have been reviewed, the system can be instructed to close out the revenue and expense accounts and create an Income Statement.

A knowledgeable accountant can review entries within the software’s audit function. The accountant will be able to look at every entry, its description, both sides of the entry (debit and credit), and any changes made in the entry. This review is important in determining if any incorrect entry was either a mistake or fraud. The accountant can see who made the entry and how the entry occurred in the accounting system.

To ensure the integrity of the system, each person working in the system must have a unique user identification, and no users may know others’ passwords. If there is an entry or updated entry, the accountant will be able to see the entry in the audit function of the software. If an employee has changed expense items to pay his or her personal bills, the accountant can see the change. Similarly, changes in transaction dates can be reviewed to determine whether they are fraudulent. Professional accountants know what goes on in their organization’s accounting system.

KEY TAKEAWAYS

Key Concepts and Summary

- Cash-basis versus accrual-basis system: The cash-basis system delays revenue and expense recognition until cash is collected, which can mislead investors about the daily operations of a business. The accrual-basis system recognizes revenues and expenses in the period in which they were earned or incurred, allowing for an even distribution of income and a more accurate business of daily operations.

- Classified balance sheet: The classified balance sheet breaks down assets and liabilities into subcategories focusing on current and long-term classifications. This allows investors to see company position in both the short term and long term.

- Liquidity: Liquidity means a business has enough cash available to pay bills as they come due. Being too liquid can mean that a company is not using its assets efficiently.

- Working capital: Working capital shows how efficiently a company operates. The formula is current assets minus current liabilities.

- Current ratio: The current ratio shows how many times over a company can cover its liabilities. It is found by dividing current assets by current liabilities.

Footnotes

- 1Elaine Pofeldt. “5 Ways to Tackle the Problem That Kills One of Every Four Small Businesses.” Money. May 19, 2015. http://time.com/money/3888448/cash-flow-small-business-startups/

- 2Matt Johnson. “Revisiting the Lehman Brothers Collapse, the Business of Banking and Its Inherent Crises.” Coinmonks. February 1, 2018. https://medium.com/coinmonks/revisiting-the-lehman-brothers-collapse-fb18769d6cf8

Glossary

- cash basis accounting

- method of accounting in which transactions are not recorded in the financial statements until there is an exchange of cash

- classified balance sheet

- presents information on your balance sheet in a more informative structure, where asset and liability categories are divided into smaller, more detailed sections

- current ratio

- current assets divided by current liabilities; used to determine a company’s liquidity (ability to meet short-term obligations)

- intangible asset

- asset with financial value but no physical presence; examples include copyrights, patents, goodwill, and trademarks

- liquidity

- ability to convert assets into cash in order to meet primarily short-term cash needs or emergencies

- long-term investment

- stocks, bonds, or other types of investments held for more than one operating cycle or one year, whichever is longer

- long-term liability

- debt settled outside one year or one operating cycle, whichever is longer

- operating cycle

- amount of time it takes a company to use its cash to provide a product or service and collect payment from the customer

- property, plant, and equipment

- tangible assets (those that have a physical presence) held for more than one operating cycle or one year, whichever is longer

- working capital

- current assets less current liabilities; sometimes used as a measure of liquidity

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

a balance sheet that organizes assets into current and noncurrent sections and liabilities into current and noncurrent sections

amount of time it takes a company to use its cash to provide a product or service and collect payment from the customer

tangible assets (those that have a physical presence) held for more than one operating cycle or one year, whichever is longer

stocks, bonds, or other types of investments held for more than one operating cycle or one year, whichever is longer

debt settled outside one year or one operating cycle, whichever is longer

ability to convert assets into cash in order to meet primarily short-term cash needs or emergencies

current assets less current liabilities; sometimes used as a measure of liquidity

current assets divided by current liabilities; used to determine a company’s liquidity (ability to meet short-term obligations)