LO 4.5 Prepare Financial Statements Using the Adjusted Trial Balance

Once you have prepared the adjusted trial balance, you are ready to prepare the financial statements. Preparing financial statements is the seventh step in the accounting cycle. Remember that we have four financial statements to prepare: an income statement, a statement of retained earnings, a balance sheet, and the statement of cash flows. These financial statements were introduced in Introduction to Financial Statements and Statement of Cash Flows dedicates in-depth discussion to that statement.

To prepare the financial statements, a company will look at the adjusted trial balance for account information. From this information, the company will begin constructing each of the statements, beginning with the income statement. Income statements will include all revenue and expense accounts. The statement of retained earnings will include beginning retained earnings, any net income (loss) (found on the income statement), and dividends. The balance sheet is going to include assets, contra assets, liabilities, and stockholder equity accounts, including ending retained earnings and common stock.

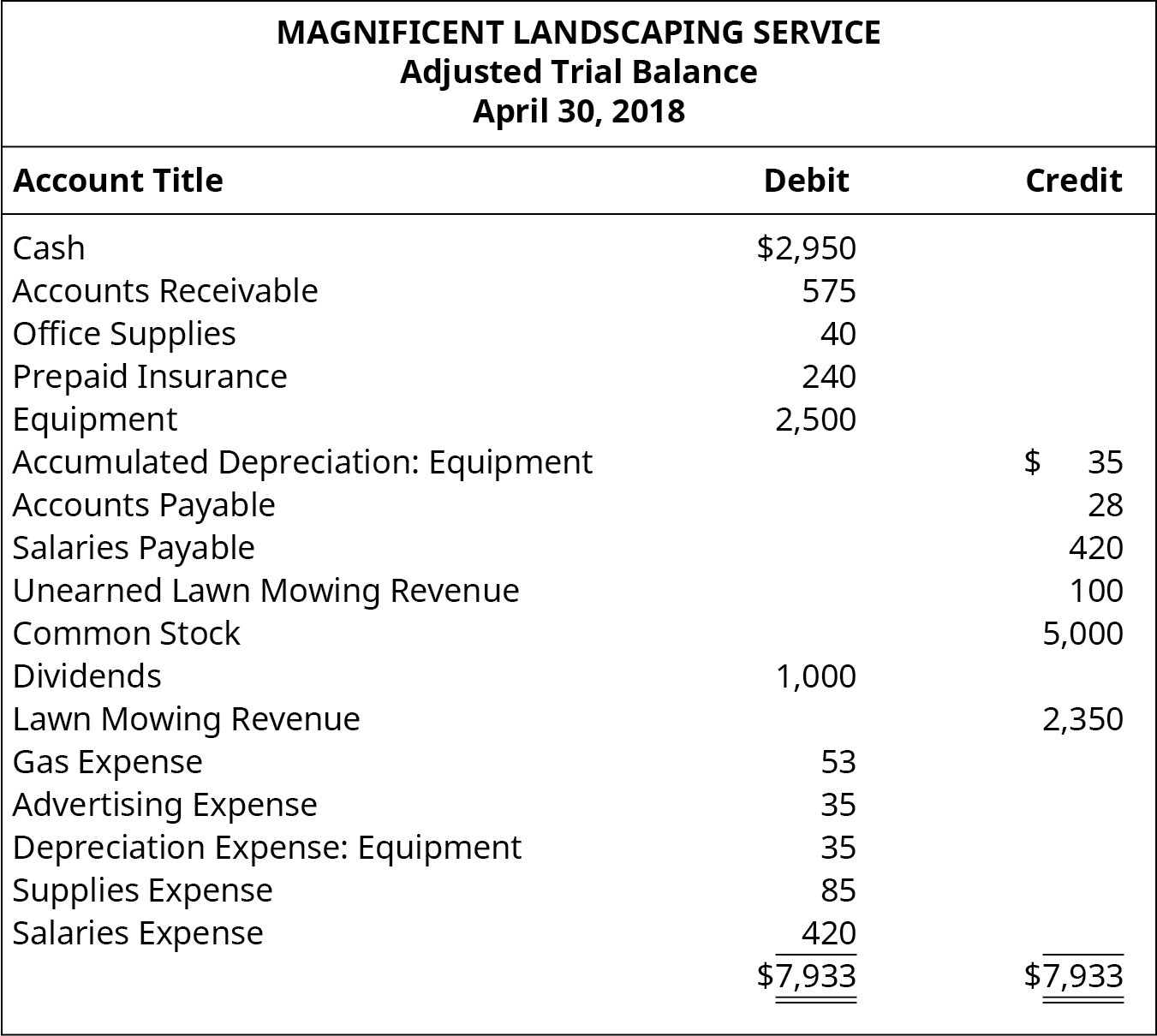

YOUR TURN

Go over the adjusted trial balance for Magnificent Landscaping Service. Identify which financial statement each account will go on: Balance Sheet, Statement of Retained Earnings, or Income Statement.

Solution

Balance Sheet: Cash, accounts receivable, office supplied, prepaid insurance, equipment, accumulated depreciation (equipment), accounts payable, salaries payable, unearned lawn mowing revenue, and common stock. Statement of Retained Earnings: Dividends. Income Statement: Lawn mowing revenue, gas expense, advertising expense, depreciation expense (equipment), supplies expense, and salaries expense.

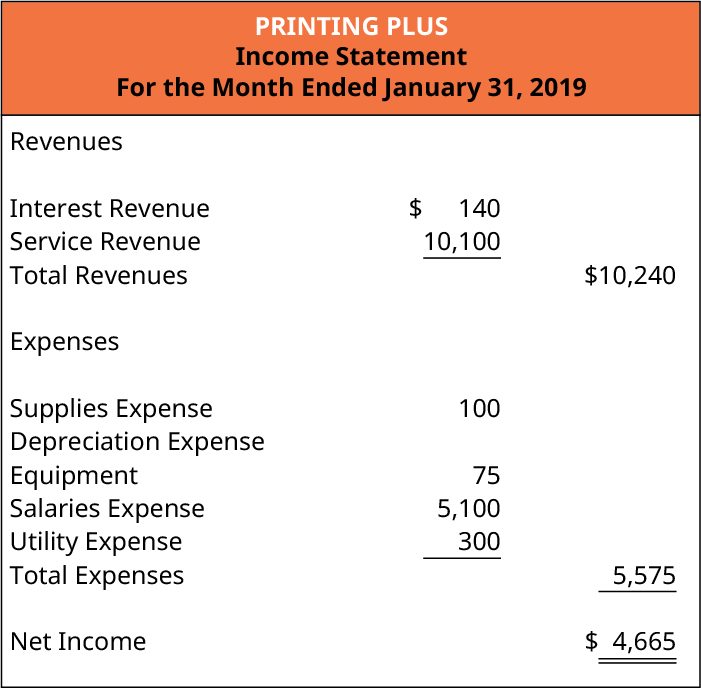

Income Statement

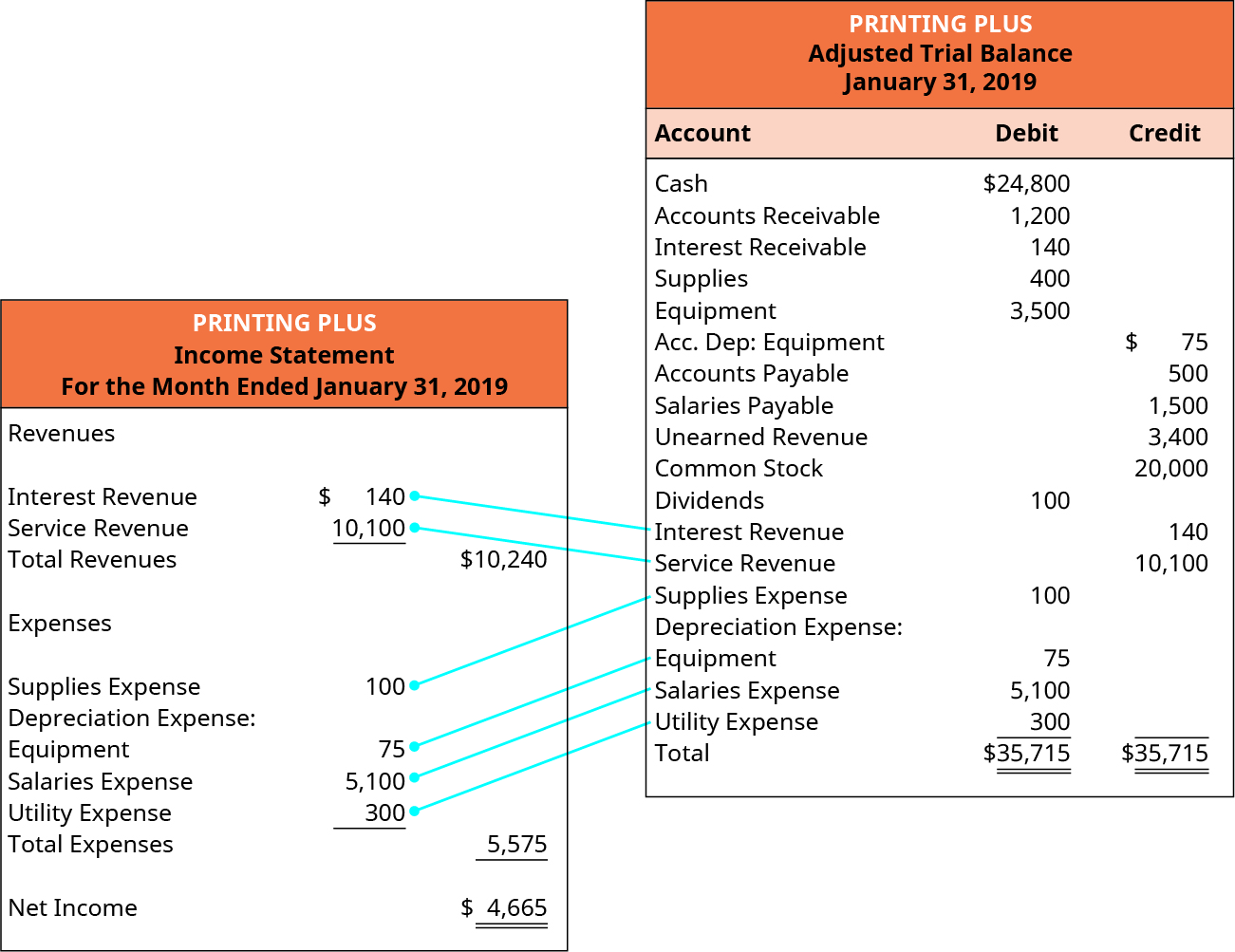

An income statement shows the organization’s financial performance for a given period of time. When preparing an income statement, revenues will always come before expenses in the presentation. For Printing Plus, the following is its January 2019 Income Statement.

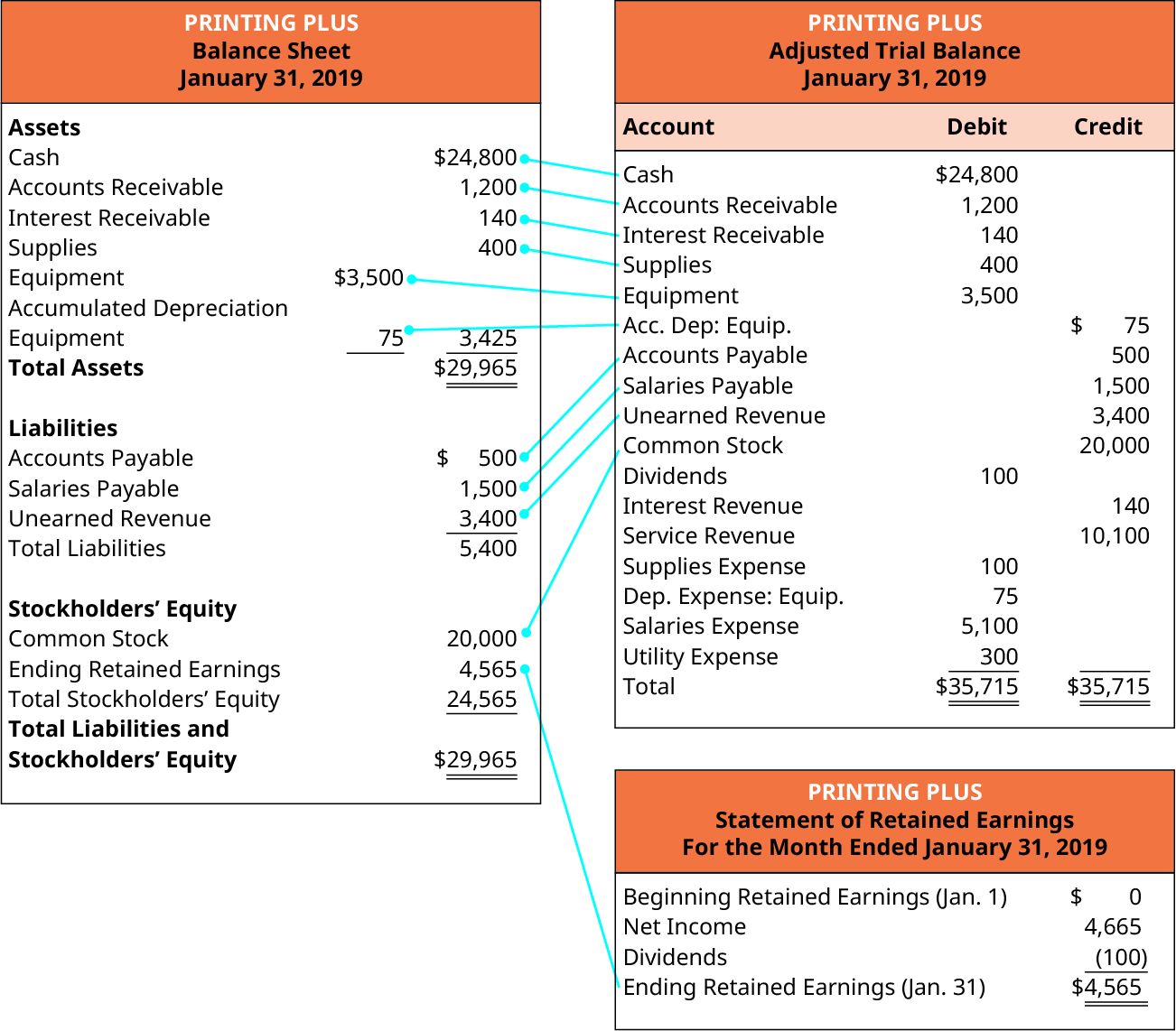

Revenue and expense information is taken from the adjusted trial balance as follows:

Total revenues are $10,240, while total expenses are $5,575. Total expenses are subtracted from total revenues to get a net income of $4,665. If total expenses were more than total revenues, Printing Plus would have a net loss rather than a net income. This net income figure is used to prepare the statement of retained earnings.

CONCEPTS IN PRACTICE

Financial statements give a glimpse into the operations of a company, and investors, lenders, owners, and others rely on the accuracy of this information when making future investing, lending, and growth decisions. When one of these statements is inaccurate, the financial implications are great.

For example, Celadon Group misreported revenues over the span of three years and elevated earnings during those years. The total overreported income was approximately $200–$250 million. This gross misreporting misled investors and led to the removal of Celadon Group from the New York Stock Exchange. Not only did this negatively impact Celadon Group’s stock price and lead to criminal investigations, but investors and lenders were left to wonder what might happen to their investment.

That is why it is so important to go through the detailed accounting process to reduce errors early on and hopefully prevent misinformation from reaching financial statements. The business must have strong internal controls and best practices to ensure the information is presented fairly.1

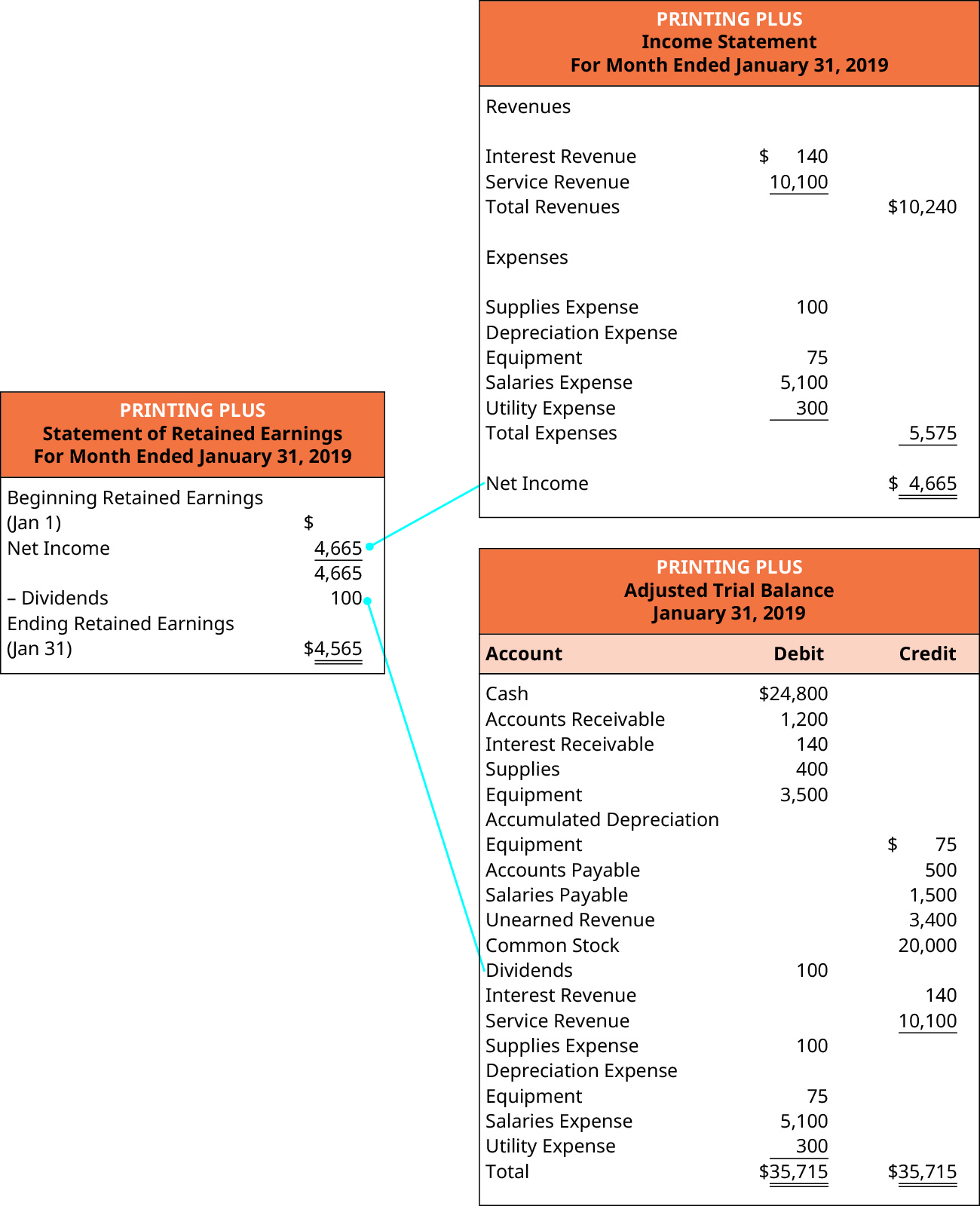

Statement of Retained Earnings

The statement of retained earnings (which is often a component of the statement of stockholders’ equity) shows how the equity (or value) of the organization has changed over a period of time. The statement of retained earnings is prepared second to determine the ending retained earnings balance for the period. The statement of retained earnings is prepared before the balance sheet because the ending retained earnings amount is a required element of the balance sheet. The following is the Statement of Retained Earnings for Printing Plus.

Net income information is taken from the income statement, and dividends information is taken from the adjusted trial balance as follows.

The statement of retained earnings always leads with beginning retained earnings. Beginning retained earnings carry over from the previous period’s ending retained earnings balance. Since this is the first month of business for Printing Plus, there is no beginning retained earnings balance. Notice the net income of $4,665 from the income statement is carried over to the statement of retained earnings. Dividends are taken away from the sum of beginning retained earnings and net income to get the ending retained earnings balance of $4,565 for January. This ending retained earnings balance is transferred to the balance sheet.

Concepts Statements give the Financial Accounting Standards Board (FASB) a guide to creating accounting principles and consider the limitations of financial statement reporting. See the FASB’s “Concepts Statements” page to learn more.

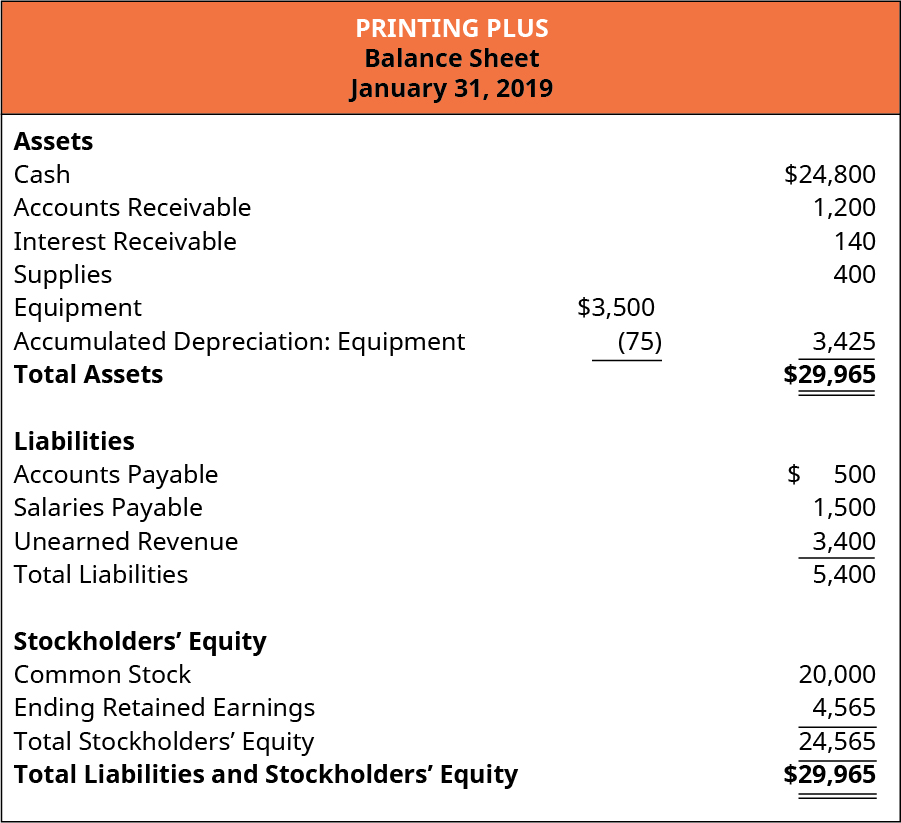

Balance Sheet

The balance sheet is the third statement prepared after the statement of retained earnings and lists what the organization owns (assets), what it owes (liabilities), and what the shareholders control (equity) on a specific date. Remember that the balance sheet represents the accounting equation, where assets equal liabilities plus stockholders’ equity. The following is the Balance Sheet for Printing Plus.

Ending retained earnings information is taken from the statement of retained earnings, and asset, liability, and common stock information is taken from the adjusted trial balance as follows.

Looking at the asset section of the balance sheet, Accumulated Depreciation–Equipment is included as a contra asset account to equipment. The accumulated depreciation ($75) is taken away from the original cost of the equipment ($3,500) to show the book value of equipment ($3,425). The accounting equation is balanced, as shown on the balance sheet, because total assets equal $29,965 as do the total liabilities and stockholders’ equity.

There is a worksheet approach ( sometimes called a 10-column worksheet) a company may use to make sure end-of-period adjustments translate to the correct financial statements. This is explained and illustrated in Use a 10-column worksheet.

IFRS CONNECTION

Both US-based companies and those headquartered in other countries produce the same primary financial statements—Income Statement, Balance Sheet, and Statement of Cash Flows. The presentation of these three primary financial statements is largely similar with respect to what should be reported under US GAAP and IFRS, but some interesting differences can arise, especially when presenting the Balance Sheet.

While both US GAAP and IFRS require the same minimum elements that must be reported on the Income Statement, such as revenues, expenses, taxes, and net income, to name a few, publicly traded companies in the United States have further requirements placed by the SEC on the reporting of financial statements. For example, IFRS-based financial statements are only required to report the current period of information and the information for the prior period. US GAAP has no requirement for reporting prior periods, but the SEC requires that companies present one prior period for the Balance Sheet and three prior periods for the Income Statement. Under both IFRS and US GAAP, companies can report more than the minimum requirements.

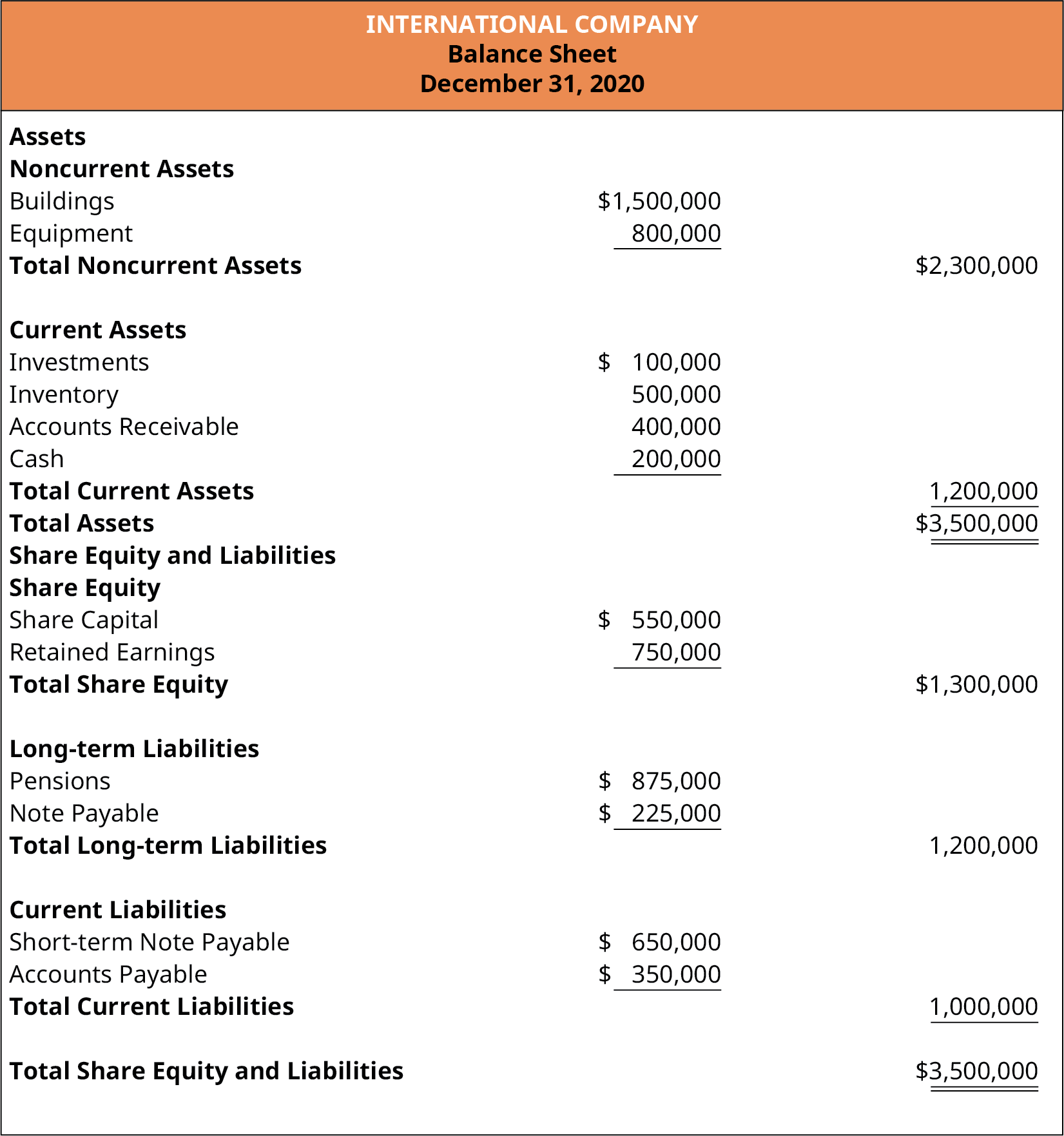

Presentation differences are most noticeable between the two forms of GAAP in the Balance Sheet. Under US GAAP there is no specific requirement on how accounts should be presented. However, the SEC requires that companies present their Balance Sheet information in liquidity order, which means current assets listed first with cash being the first account presented, as it is a company’s most liquid account. Liquidity refers to how easily an item can be converted to cash. IFRS requires that accounts be classified into current and noncurrent categories for both assets and liabilities, but no specific presentation format is required. Thus, for US companies, the first category always seen on a Balance Sheet is Current Assets, and the first account balance reported is cash. This is not always the case under IFRS. While many Balance Sheets of international companies will be presented in the same manner as those of a US company, the lack of a required format means that a company can present noncurrent assets first, followed by current assets. The accounts of a Balance Sheet using IFRS might appear as shown here.

Review the annual report of Stora Enso which is an international company that utilizes the illustrated format in presenting its Balance Sheet, also called the Statement of Financial Position. The Balance Sheet is found on page 31 of the report.

Some of the biggest differences that occur on financial statements prepared under US GAAP versus IFRS relate primarily to measurement or timing issues: in other words, how a transaction is valued and when it is recorded.

In Completing the Accounting Cycle, we continue our discussion of the accounting cycle, completing the last steps of journalizing and posting closing entries and preparing a post-closing trial balance.

KEY TAKEAWAYS

Key Concepts and Summary

- Income Statement: The income statement shows the net income or loss as a result of revenue and expense activities occurring in a period.

- Statement of Retained Earnings: The statement of retained earnings shows the effects of net income (loss) and dividends on the earnings the company maintains.

- Balance Sheet: The balance sheet visually represents the accounting equation, showing that assets balance with liabilities and equity.

Footnotes

- 1 James Jaillet. “Celadon under Criminal Investigation over Financial Statements.” Commercial Carrier Journal. July 25, 2018. https://www.ccjdigital.com/200520-2/

Glossary

- 10-column worksheet

- all-in-one spreadsheet showing the transition of account information from the trial balance through the financial statements

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

an all-in-one spreadsheet showing the transition of account information from the trial balance through the financial statements