LO 4.2 Discuss the Adjustment Process and Illustrate Common Types of Adjusting Entries

When a company reaches the end of a period, it must update certain accounts that have either been left unattended throughout the period or have not yet been recognized. Adjusting entries update accounting records at the end of a period for any transactions that have not yet been recorded. One important accounting principle to remember is that just as the accounting equation (Assets = Liabilities + Equity) must be in balance, it must remain in balance after you make adjusting entries. We discuss the effects of adjusting entries in greater detail throughout this chapter.

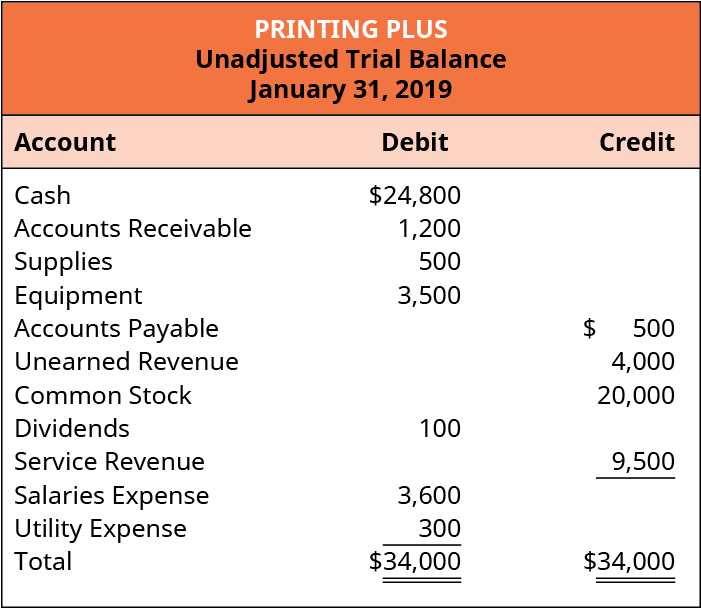

There are several steps in the accounting cycle that require the preparation of a trial balance: Step 4, preparing an unadjusted trial balance; Step 6, preparing an adjusted trial balance; and Step 9, preparing a post-closing trial balance. You might question the purpose of more than one trial balance. For example, why can we not go from the unadjusted trial balance straight into preparing financial statements for public consumption? What is the purpose of the adjusted trial balance? Does preparing more than one trial balance mean the company made a mistake earlier in the accounting cycle? To answer these questions, let’s first explore the (unadjusted) trial balance, and why some accounts have incorrect balances.

Why Some Accounts Have Incorrect Balances on the Trial Balance

The unadjusted trial balance may have incorrect balances in some accounts. Recall the trial balance from Analyzing and Recording Transactions for the example company, Printing Plus.

The trial balance for Printing Plus shows Supplies of $500, which were purchased on January 30. Since this is a new company, Printing Plus would more than likely use some of their supplies right away, before the end of the month on January 31. Supplies are only an asset when they are unused. If Printing Plus used some of its supplies immediately on January 30, then why is the full $500 still in the supply account on January 31? How do we fix this incorrect balance?

Similarly, what about Unearned Revenue? On January 9, the company received $4,000 from a customer for printing services to be performed. The company recorded this as a liability because it received payment without providing the service. To clear this liability, the company must perform the service. Assume that as of January 31 some of the printing services have been provided. Is the full $4,000 still a liability? Since a portion of the service was provided, a change to unearned revenue should occur. The company needs to correct this balance in the Unearned Revenue account.

Having incorrect balances in Supplies and in Unearned Revenue on the company’s January 31 trial balance is not due to any error on the company’s part. The company followed all of the correct steps of the accounting cycle up to this point. So why are the balances still incorrect?

Journal entries are recorded when an activity or event occurs that triggers the entry. Usually the trigger is from an original source. Recall that an original source can be a formal document substantiating a transaction, such as an invoice, purchase order, cancelled check, or employee time sheet. Not every transaction produces an original source document that will alert the bookkeeper that it is time to make an entry.

When a company purchases supplies, the original order, receipt of the supplies, and receipt of the invoice from the vendor will all trigger journal entries. This trigger does not occur when using supplies from the supply closet. Similarly, for unearned revenue, when the company receives an advance payment from the customer for services yet provided, the cash received will trigger a journal entry. When the company provides the printing services for the customer, the customer will not send the company a reminder that revenue has now been earned. Situations such as these are why businesses need to make adjusting entries.

THINK IT THROUGH

Elliot Simmons owns a small law firm. He does the accounting himself and uses an accrual basis for accounting. At the end of his first month, he reviews his records and realizes there are a few inaccuracies on this unadjusted trial balance.

One difference is the supplies account; the figure on paper does not match the value of the supplies inventory still available. Another difference was interest earned from his bank account. He did not have anything recognizing these earnings.

Why did his unadjusted trial balance have these errors? What can be attributed to the differences in supply figures? What can be attributed to the differences in interest earned?

The Need for Adjusting Entries

Adjusting entries update accounting records at the end of a period for any transactions that have not yet been recorded. These entries are necessary to ensure the income statement and balance sheet present the correct, up-to-date numbers. Adjusting entries are also necessary because the initial trial balance may not contain complete and current data due to several factors:

- The inefficiency of recording every single day-to-day event, such as the use of supplies.

- Some costs are not recorded during the period but must be recognized at the end of the period, such as depreciation, rent, and insurance.

- Some items are forthcoming for which original source documents have not yet been received, such as a utility bill.

There are a few other guidelines that support the need for adjusting entries.

Guidelines Supporting Adjusting Entries

Several guidelines support the need for adjusting entries:

- Revenue recognition principle: Adjusting entries are necessary because the revenue recognition principle requires revenue recognition when earned, thus the need for an update to unearned revenues.

- Expense recognition (matching) principle: This requires matching expenses incurred to generate the revenues earned, which affects accounts such as insurance expense and supplies expense.

- Time period assumption: This requires useful information be presented in shorter time periods such as years, quarters, or months. This means a company must recognize revenues and expenses in the proper period, requiring adjustment to certain accounts to meet these criteria.

The required adjusting entries depend on what types of transactions the company has, but there are some common types of adjusting entries. Before we look at recording and posting the most common types of adjusting entries, we briefly discuss the various types of adjusting entries.

Types of Adjusting Entries

Adjusting entries requires updates to specific account types at the end of the period. Not all accounts require updates, only those not naturally triggered by an original source document. There are two main types of adjusting entries that we explore further, deferrals and accruals.

Deferrals

Deferrals are prepaid expense and revenue accounts that have delayed recognition until they have been used or earned. This recognition may not occur until the end of a period or future periods. When deferred expenses and revenues have yet to be recognized, their information is stored on the balance sheet. As soon as the expense is incurred and the revenue is earned, the information is transferred from the balance sheet to the income statement. Two main types of deferrals are prepaid expenses and unearned revenues.

Prepaid Expenses

Recall from Analyzing and Recording Transactions that prepaid expenses (prepayments) are assets for which advanced payment has occurred, before the company can benefit from use. As soon as the asset has provided benefit to the company, the value of the asset used is transferred from the balance sheet to the income statement as an expense. Some common examples of prepaid expenses are supplies, depreciation, insurance, and rent.

When a company purchases supplies, it may not use all supplies immediately, but chances are the company has used some of the supplies by the end of the period. It is not worth it to record every time someone uses a pencil or piece of paper during the period, so at the end of the period, this account needs to be updated for the value of what has been used.

Let’s say a company paid for supplies with cash in the amount of $400. At the end of the month, the company took an inventory of supplies used and determined the value of those supplies used during the period to be $150. The following entry occurs for the initial payment.

Supplies increases (debit) for $400, and Cash decreases (credit) for $400. When the company recognizes the supplies usage, the following adjusting entry occurs.

Supplies Expense is an expense account, increasing (debit) for $150, and Supplies is an asset account, decreasing (credit) for $150. This means $150 is transferred from the balance sheet (asset) to the income statement (expense). Notice that not all of the supplies are used. There is still a balance of $250 (400 – 150) in the Supplies account. This amount will carry over to future periods until used. The balances in the Supplies and Supplies Expense accounts show as follows.

Depreciation may also require an adjustment at the end of the period.

Important note: Depreciation has different meanings in our lives as consumers and in accounting. Unlike in our consumer lives, depreciation in accounting has nothing to do with the market value of an asset. In accounting, depreciation simply spreads the cost of an asset over the years the asset is used.

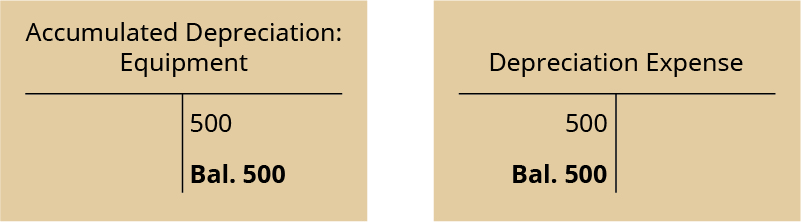

So, depreciation is the systematic method to record the allocation of cost over a given period of certain assets. This allocation of cost is recorded over the useful life of the asset, or the time period over which an asset cost is allocated. Accounting for using up the cost of an asset like a building is complicated by the fact that we need to keep track of the original cost of the building, as well as how much of the cost we’ve used up over the years. We need a third account in order to do this. The original cost sits in the asset (Building) account undisturbed. The used-up part of the asset’s cost is accumulated and stored in Accumulated Depreciation, a contra asset account. A contra account is an account paired with another account, has an opposite normal balance to the paired account, and indirectly reduces the balance in the paired account at the end of a period. The portion of the asset’s cost that has been used up in the current accounting period is recorded in Depreciation Expense.

Accumulated Depreciation is contrary to an asset account, such as Building. This means that the normal balance for Accumulated Depreciation is on the credit side. It houses all depreciation expensed in current and prior periods. Accumulated Depreciation will indirectly reduce the asset account for depreciation incurred up to that point. The difference between the asset’s cost and accumulated depreciation is called the book value of the asset. When depreciation is recorded in an adjusting entry, Accumulated Depreciation is credited and Depreciation Expense is debited.

For example, let’s say a company pays $2,000 for equipment that is supposed to last four years. The company wants to depreciate the asset over those four years equally. This means that $500 of the asset’s cost ($2,000/four years) will be used up each year. In the first year, the company would record the following adjusting entry to show depreciation (used up cost) of the equipment.

Depreciation Expense increases (debit) and Accumulated Depreciation-Equipment, increases (credit). If the company wanted to compute the book value, it would take the original cost of the equipment (which is sitting undisturbed in the Equipment account) and subtract accumulated depreciation.

This means that the current book value of the equipment is $1,500, and it will decrease by another $500 when the adjusting entry is made at the end of the next year. The following account balances after adjustment are as follows:

You will learn more about depreciation and its computation in Long-Term Assets. However, one important fact that we need to address now is that the book value of an asset is not necessarily it’s market value (the price at which the asset would sell) . For example, you might have a building for which you paid $1,000,000 that currently has been depreciated to a book value of $800,000. However, today it could sell for more than, less than, or the same as its book value. The same is true about just about any asset you can name, except, perhaps, cash itself.

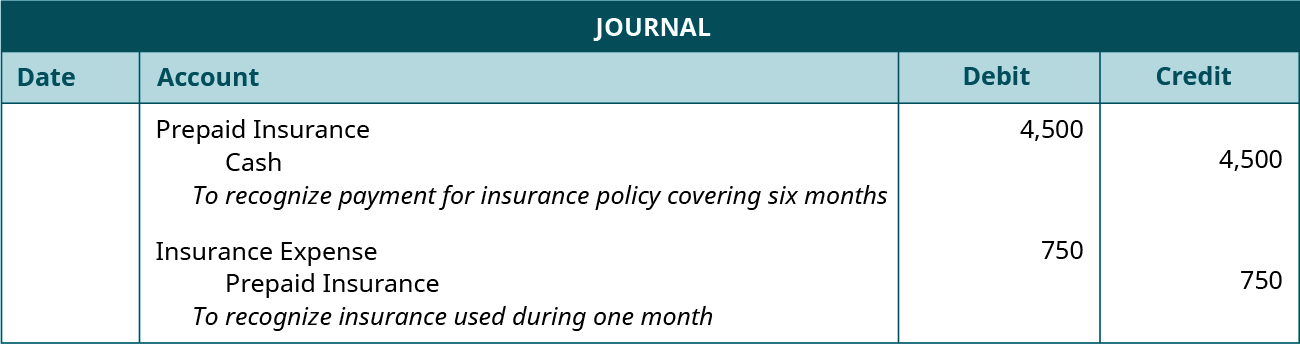

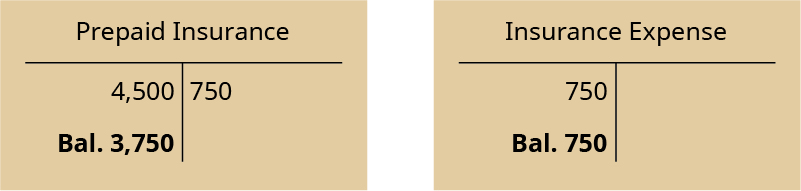

Insurance policies can require advanced payment of fees for several months at a time, six months, for example. The company does not use all six months of insurance immediately but over the course of the six months. At the end of each month, the company needs to record the amount of insurance expired during that month.

For example, a company pays $4,500 for an insurance policy covering six months. It is the end of the first month and the company needs to record an adjusting entry to recognize the insurance used during the month. The following entries show the initial payment for the policy and the subsequent adjusting entry for one month of insurance usage.

In the first entry, Cash decreases (credit) and Prepaid Insurance increases (debit) for $4,500. In the second entry, Prepaid Insurance decreases (credit) and Insurance Expense increases (debit) for one month’s insurance usage found by taking the total $4,500 and dividing by six months (4,500/6 = 750). The account balances after adjustment are as follows:

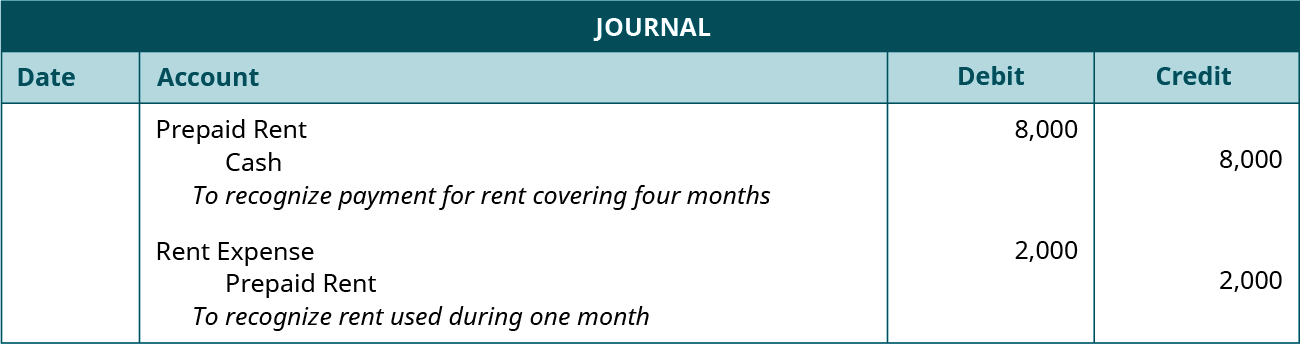

Similar to prepaid insurance, rent also requires advanced payment. Usually to rent a space, a company will need to pay rent at the beginning of the month. The company may also enter into a lease agreement that requires several months, or years, of rent in advance. Each month that passes, the company needs to record rent used for the month.

Let’s say a company pays $8,000 in advance for four months of rent. After the first month, the company records an adjusting entry for the rent used. The following entries show initial payment for four months of rent and the adjusting entry for one month’s usage.

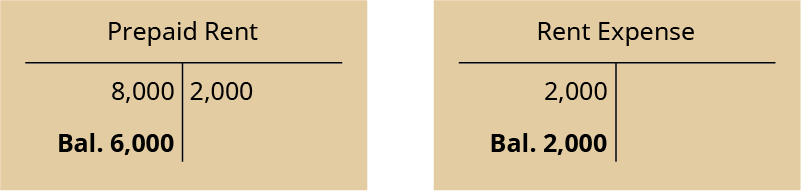

In the first entry, Cash decreases (credit) and Prepaid Rent increases (debit) for $8,000. In the second entry, Prepaid Rent decreases (credit) and Rent Expense increases (debit) for one month’s rent usage found by taking the total $8,000 and dividing by four months (8,000/4 = 2,000). The account balances after adjustment are as follows:

Another type of deferral requiring adjustment is unearned revenue.

Unearned Revenues

Recall that unearned revenue represents the company receiving cash from a customer before the company provides the product or service. Since the company has not yet provided the product or service, it cannot recognize any revenue at the time the company receives the cash, so a liability is recorded until the company provides the product or service. At the end of a period, the company will review the account to see if any of the unearned revenue has been earned. If so, this amount will be recorded as revenue in the current period.

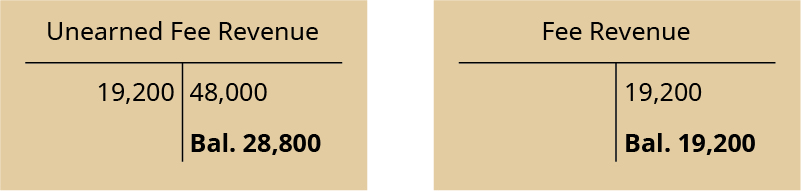

For example, let’s say the company is a law firm. During the year, it collected retainer fees totaling $48,000 from clients. Retainer fees are money lawyers collect in advance of starting work on a case. When the company collects this money from its clients, it will debit cash and credit unearned fees. Even though not all of the $48,000 was probably collected on the same day, we record it as if it was for simplicity’s sake.

In this case, Unearned Fee Revenue increases (credit) and Cash increases (debit) for $48,000.

At the end of the year after analyzing the unearned fees account, 40% of the unearned fees have been earned. This 40% can now be recorded as revenue. Total revenue recorded is $19,200 ($48,000 × 40%).

For this entry, Unearned Fee Revenue decreases (debit) and Fee Revenue increases (credit) for $19,200, which is the 40% earned during the year. The company will have the following balances in the two accounts:

Besides deferrals, other types of adjusting entries include accruals.

Accruals

Accruals are types of adjusting entries that accumulate during a period, where amounts were previously unrecorded. The two specific types of adjustments are accrued revenues and accrued expenses.

Accrued Revenues

Accrued revenues are revenues earned in a period but have yet to be recorded, and no money has been collected. Some examples include interest, and services completed but a bill has yet to be sent to the customer.

Interest can be earned from bank account holdings, notes receivable, and some accounts receivables (depending on the contract). Interest had been accumulating during the period and needs to be adjusted to reflect interest earned at the end of the period. Note that this interest has not been paid at the end of the period, only earned. This aligns with the revenue recognition principle to recognize revenue when earned, even if cash has yet to be collected.

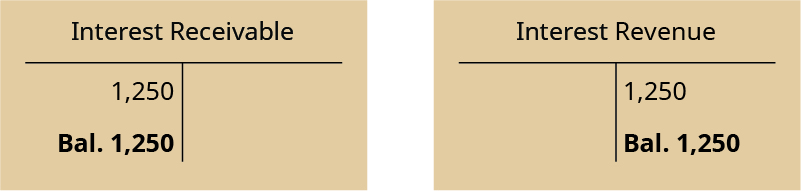

For example, assume that a company has one outstanding note receivable in the amount of $100,000. Interest on this note is 5% per year. Three months have passed, and the company needs to record interest earned on this outstanding loan. The calculation for the interest revenue earned is $100,000 × 5% × 3/12 = $1,250. The following adjusting entry occurs.

Interest Receivable increases (debit) for $1,250 because interest has not yet been paid. Interest Revenue increases (credit) for $1,250 because interest was earned in the three-month period but had been previously unrecorded.

Previously unrecorded service revenue can arise when a company provides a service but did not yet bill the client for the work. This means the customer has also not yet paid for services. Since there was no bill to trigger a transaction, an adjustment is required to recognize revenue earned at the end of the period.

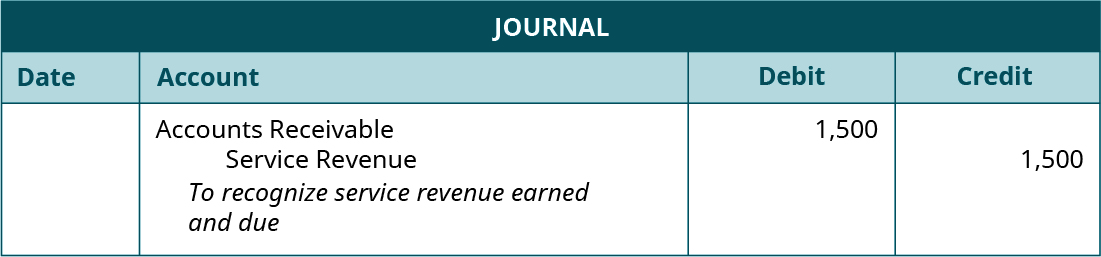

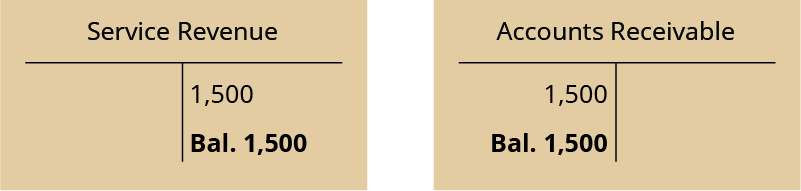

For example, a company performs landscaping services in the amount of $1,500. However, they have not yet received payment. At the period end, the company would record the following adjusting entry.

Accounts Receivable increases (debit) for $1,500 because the customer has not yet paid for services completed. Service Revenue increases (credit) for $1,500 because service revenue was earned but had been previously unrecorded.

Accrued Expenses

Accrued expenses are expenses incurred in a period but have yet to be recorded, and no money has been paid. Some examples include interest, tax, and salary expenses.

Interest expense arises from notes payable and other loan agreements. The company has accumulated interest during the period but has not recorded or paid the amount. This creates a liability that the company must pay at a future date. You cover more details about computing interest in Current Liabilities, so for now amounts are given.

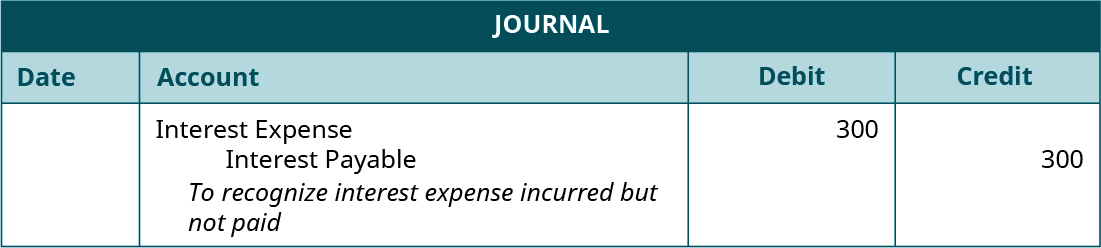

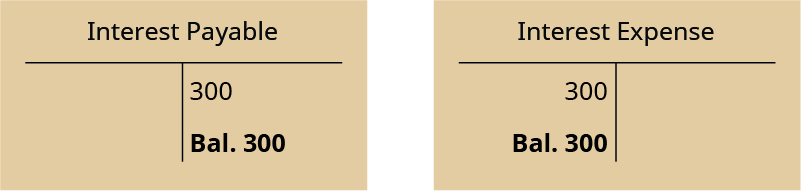

For example, a company accrued $300 of interest during the period. The following entry occurs at the end of the period.

Interest Expense increases (debit) and Interest Payable increases (credit) for $300. The following are the updated ledger balances after posting the adjusting entry.

Taxes are only paid at certain times during the year, not necessarily every month. Taxes the company owes during a period that are unpaid require adjustment at the end of a period. This creates a liability for the company. Some tax expense examples are income and sales taxes.

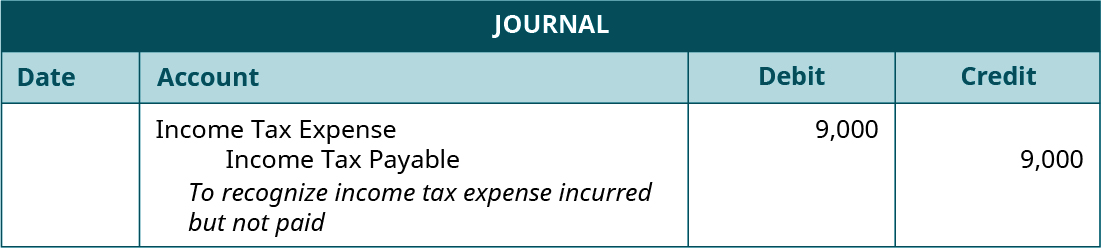

For example, a company has accrued income taxes for the month for $9,000. The company would record the following adjusting entry.

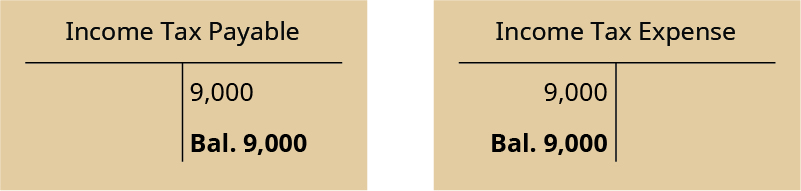

Income Tax Expense increases (debit) and Income Tax Payable increases (credit) for $9,000. The following are the updated ledger balances after posting the adjusting entry.

Many salaried employees are paid once a month. The salary the employee earned during the month might not be paid until the following month. For example, the employee is paid for the prior month’s work on the first of the next month. The financial statements must remain up to date, so an adjusting entry is needed during the month to show salaries previously unrecorded and unpaid at the end of the month.

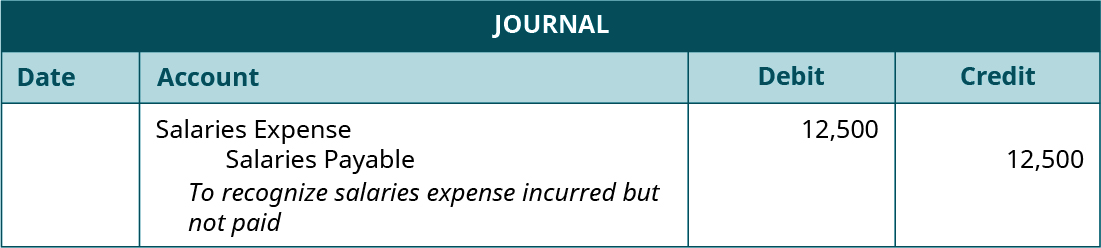

Let’s say a company has five salaried employees, each earning $2,500 per month. In our example, assume that they do not get paid for this work until the first of the next month. The following is the adjusting journal entry for salaries.

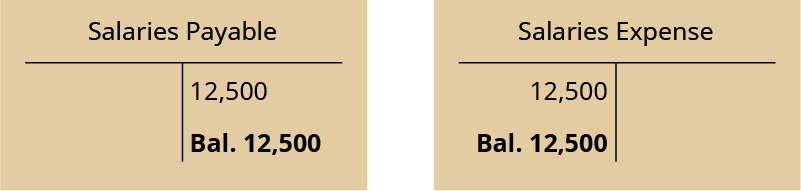

Salaries Expense increases (debit) and Salaries Payable increases (credit) for $12,500 ($2,500 per employee × five employees). The following are the updated ledger balances after posting the adjusting entry.

In Record and Post the Common Types of Adjusting Entries, we explore some of these adjustments specifically for our company Printing Plus, and show how these entries affect our general ledger (T-accounts).

YOUR TURN

| Example | Income Statement Account | Balance Sheet Account | Cash in Entry? |

|---|---|---|---|

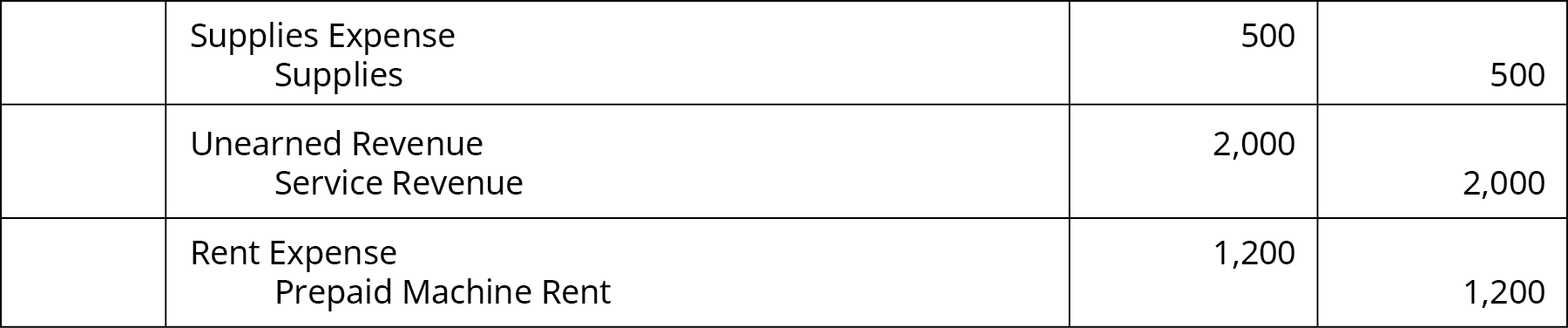

Review the three adjusting entries that follow. Using the table provided, for each entry write down the income statement account and balance sheet account used in the adjusting entry in the appropriate column. Then in the last column answer yes or no.

Solution

| Example | Income Statement Account | Balance Sheet Account | Cash in Entry? |

|---|---|---|---|

| 1 | Supplies expense | Supplies | no |

| 2 | Service Revenue | Unearned Revenue | no |

| 3 | Rent Expense | Prepaid machine rent | no |

YOUR TURN

Did we continue to follow the rules of adjusting entries in these two examples? Explain.

| Example | Income Statement Account | Balance Sheet Account | Cash in Entry? |

|---|---|---|---|

Solution

Yes, we did. Each entry has one income statement account and one balance sheet account, and cash does not appear in either of the adjusting entries.

| Example | Income Statement Account | Balance Sheet Account | Cash in Entry? |

|---|---|---|---|

| 1 | Electricity Expense | Accounts Payable | no |

| 2 | Salaries Expense | Salaries Payable | no |

KEY TAKEAWAYS

Key Concepts and Summary

- Incorrect balances: Incorrect balances on the unadjusted trial balance occur because not every transaction produces an original source document that will alert the bookkeeper it is time to make an entry. It is not that the accountant made an error, it means an adjustment is required to correct the balance.

- Need for adjustments: Some account adjustments are needed to update records that may not have original source documents or those that do not reflect change on a daily basis. The revenue recognition principle, expense recognition principle, and time period assumption all further the need for adjusting entries because they require revenue and expense reporting occur when earned and incurred in a current period.

- Prepaid expenses: Prepaid expenses are assets paid for before their use. When they are used, this asset’s value is reduced and an expense is recognized. Some examples include supplies, insurance, and depreciation.

- Unearned revenues: These are customer advanced payments for product or services yet to be provided. When the company provides the product or service, revenue is then recognized.

- Accrued revenues: Accrued revenues are revenues earned in a period but have yet to be recorded and no money has been collected. Accrued revenues are updated at the end of the period to recognize revenue and money owed to the company.

- Accrued expenses: Accrued expenses are incurred in a period but have yet to be recorded and no money has been paid. Accrued expenses are updated to reflect the expense and the company’s liability.

Glossary

- accrual

- type of adjusting entry that accumulates during a period, where an amount was previously unrecorded

- accrued expense

- expense incurred in a period but not yet recorded, and no money has been paid

- accrued revenue

- revenue earned in a period but not yet recorded, and no money has been collected

- adjusting entries

- update accounting records at the end of a period for any transactions that have not yet been recorded

- book value

- difference between the asset’s (cost) and accumulated depreciation; also, value at which assets or liabilities are recorded in a company’s financial statements

- contra account

- account paired with another account type that has an opposite normal balance to the paired account; reduces or increases the balance in the paired account at the end of a period

- deferral

- prepaid expense and revenue accounts that have delayed recognition until they have been used or earned

- depreciation

- process of allocating the costs of a tangible asset over the asset’s economic life

- useful life

- time period over which an asset cost is allocated

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

journal entries to update accounting records at the end of a period for any transactions that have not yet been recorded

prepaid expense and revenue accounts that have delayed recognition until they have been used or earned

process of allocating the costs of a tangible asset over the asset’s economic life

time period over which an asset cost is allocated

account paired with another account type that has an opposite normal balance to the paired account; indirectly reduces or increases the balance in the paired account at the end of a period

difference between the asset’s value (cost) and accumulated depreciation; also, value at which assets or liabilities are recorded in a company’s financial statements

type of adjusting entry that accumulates during a period, where an amount was previously unrecorded

revenue earned in a period but not yet recorded, and no money has been collected

expense incurred in a period but not yet recorded, and no money has been paid