LO 12.1 Identify and Describe Current Liabilities

To assist in understanding current liabilities, assume that you own a landscaping company that provides landscaping maintenance services to clients. As is common for landscaping companies in your area, you require clients to pay an initial deposit of 25% for services before you begin working on their property. Asking a customer to pay for services before you have provided them creates a current liability transaction for your business. As you’ve learned, liabilities require a future disbursement of assets or services resulting from a prior business activity or transaction. For companies to make more informed decisions, liabilities need to be classified into two specific categories: current liabilities and noncurrent (or long-term) liabilities. The differentiating factor between current and long-term is when the liability is due. The focus of this chapter is on current liabilities, while Long-Term Liabilities emphasizes long-term liabilities.

Fundamentals of Current Liabilities

A current liability is a debt or obligation due within a company’s standard operating period, typically a year, although there are exceptions that are longer or shorter than a year. A company’s typical operating period (sometimes called an operating cycle) is a year, which is used to delineate current and noncurrent liabilities, and current liabilities are considered short term and are typically due within a year or less.

Noncurrent liabilities are long-term obligations with payment typically due in a subsequent operating period. Current liabilities are reported on the classified balance sheet, listed before noncurrent liabilities. Changes in current liabilities from the beginning of an accounting period to the end are reported on the statement of cash flows as part of the cash flows from operations section. An increase in current liabilities over a period increases cash flow, while a decrease in current liabilities decreases cash flow.

| Current vs. Noncurrent Liabilities | |

|---|---|

| Current Liabilities | Noncurrent Liabilities |

| Due within one year or less for a typical one-year operating period | Due in more than one year or longer than one operating period |

|

Short-term accounts such as:

|

Long-term portion of obligations such as:

|

Examples of Current Liabilities

Common current liabilities include accounts payable, unearned revenues, the current portion of a note payable, and taxes payable. Each of these liabilities is current because it results from a past business activity, with a disbursement or payment due within a period of less than a year.

ETHICAL CONSIDERATIONS

When using financial information prepared by accountants, decision-makers rely on ethical accounting practices. For example, investors and creditors look to the current liabilities to assist in calculating a company’s annual burn rate. The burn rate is the metric defining the monthly and annual cash needs of a company. It is used to help calculate how long the company can maintain operations before becoming insolvent. The proper classification of liabilities as current assists decision-makers in determining the short-term and long-term cash needs of a company.

Another way to think about burn rate is as the amount of cash a company uses that exceeds the amount of cash created by the company’s business operations. The burn rate helps indicate how quickly a company is using its cash. Many start-ups have a high cash burn rate due to spending to start the business, resulting in low cash flow. At first, start-ups typically do not create enough cash flow to sustain operations.

Proper reporting of current liabilities helps decision-makers understand a company’s burn rate and how much cash is needed for the company to meet its short-term and long-term cash obligations. If misrepresented, the cash needs of the company may not be met, and the company can quickly go out of business. Therefore, it is important that the accountant appropriately report current liabilities because a creditor, investor, or other decision-maker’s understanding of a company’s specific cash needs helps them make good financial decisions.

Accounts Payable

Accounts payable accounts for financial obligations owed to suppliers after purchasing products or services on credit. This account may be an open credit line between the supplier and the company. An open credit line is a borrowing agreement for an amount of money, supplies, or inventory. The option to borrow from the lender can be exercised at any time within the agreed time period.

An account payable is usually a less formal arrangement than a promissory note for a current note payable. Long-term debt is covered in depth in Long-Term Liabilities. For now, know that for some debt, including short-term or current, a formal contract might be created. This contract provides additional legal protection for the lender in the event of failure by the borrower to make timely payments. Also, the contract often provides an opportunity for the lender to actually sell the rights in the contract to another party.

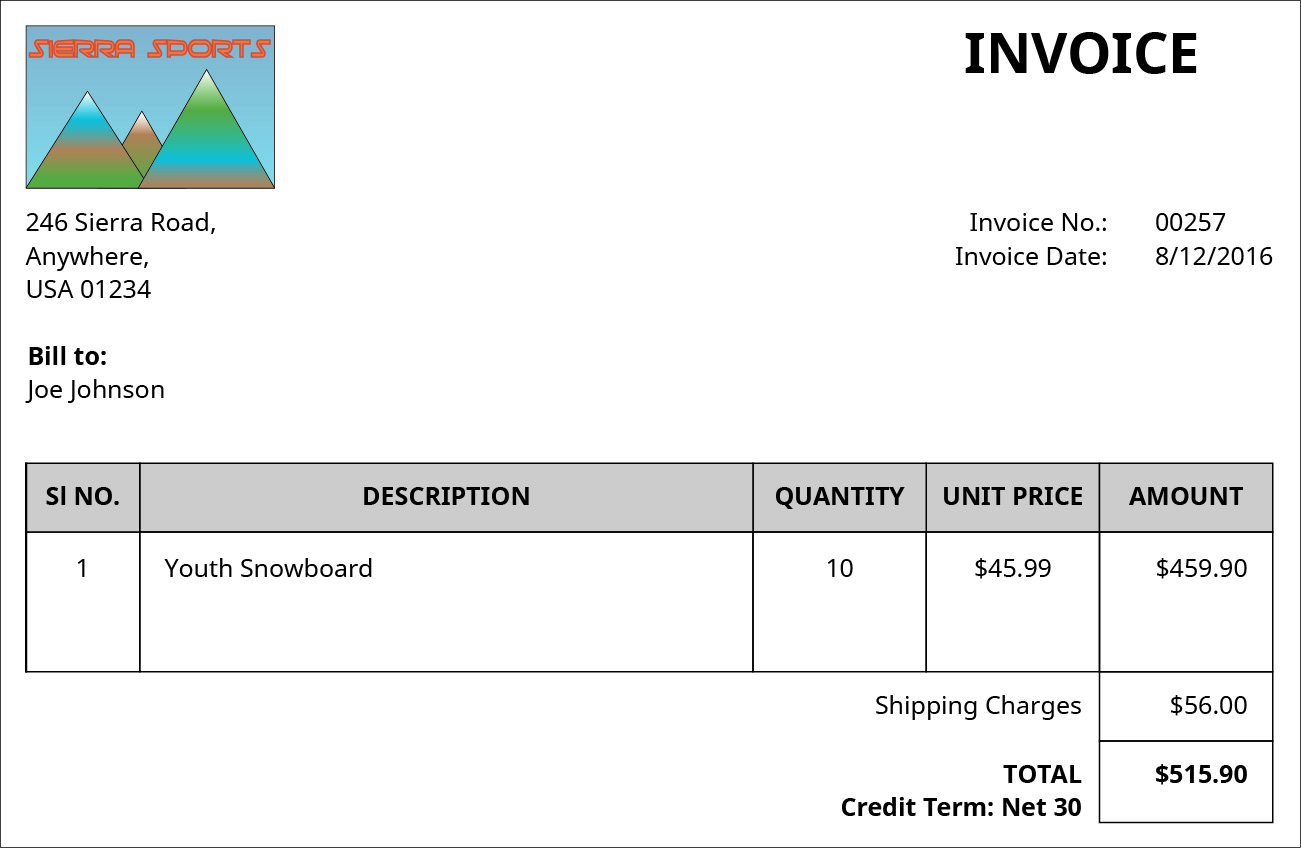

An invoice from the supplier (such as the one shown in (Figure)) detailing the purchase, credit terms, invoice date, and shipping arrangements will suffice for this contractual relationship. In many cases, accounts payable agreements do not include interest payments, unlike notes payable.

For example, assume the owner of a clothing boutique purchases hangers from a manufacturer on credit. The organizations may establish an ongoing purchase agreement, which includes purchase details (such as hanger prices and quantities), credit terms (2/10, n/60), an invoice date, and shipping charges (free on board [FOB] shipping) for each order. The basics of shipping charges and credit terms were addressed in Merchandising Transactions if you would like to refresh yourself on the mechanics. Also, to review accounts payable, you can also return to Merchandising Transactions for detailed explanations.

Unearned Revenue

Unearned revenue, also known as deferred revenue, is a customer’s advance payment for a product or service that has yet to be provided by the company. Some common unearned revenue situations include subscription services, gift cards, advance ticket sales, lawyer retainer fees, and deposits for services. As you learned when studying the accounting cycle (Analyzing and Recording Transactions, The Adjustment Process, and Completing the Accounting Cycle), we are applying the principles of accrual accounting when revenues and expenses are recognized in different months or years. Under accrual accounting, a company does not record revenue as earned until it has provided a product or service, thus adhering to the revenue recognition principle. Until the customer is provided an obligated product or service, a liability exists, and the amount paid in advance is recognized in the Unearned Revenue account. As soon as the company provides all, or a portion, of the product or service, the value is then recognized as earned revenue.

For example, assume that a landscaping company provides services to clients. The company requires advance payment before rendering service. The customer’s advance payment for landscaping is recognized in the Unearned Service Revenue account, which is a liability. Once the company has finished the client’s landscaping, it may recognize all of the advance payment as earned revenue in the Service Revenue account. If the landscaping company provides part of the landscaping services within the operating period, it may recognize the value of the work completed at that time.

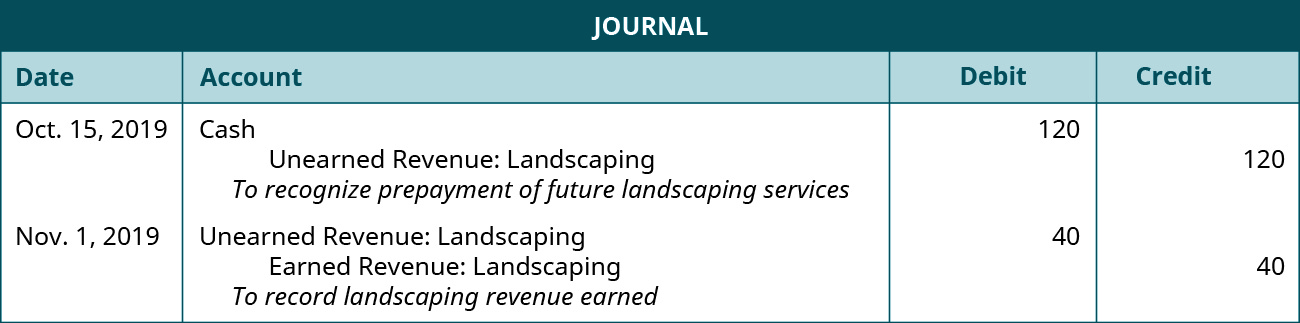

Perhaps at this point a simple example might help clarify the treatment of unearned revenue. Assume that the previous landscaping company has a three-part plan to prepare lawns of new clients for next year. The plan includes a treatment in November 2019, February 2020, and April 2020. The company has a special rate of $120 if the client prepays the entire $120 before the November treatment. In real life, the company would hope to have dozens or more customers. However, to simplify this example, we analyze the journal entries from one customer. Assume that the customer prepaid the service on October 15, 2019, and all three treatments occur on the first day of the month of service. We also assume that $40 in revenue is allocated to each of the three treatments.

Before examining the journal entries, we need some key information. Because part of the service will be provided in 2019 and the rest in 2020, we need to be careful to keep the recognition of revenue in its proper period. If all of the treatments occur, $40 in revenue will be recognized in 2019, with the remaining $80 recognized in 2020. Also, since the customer could request a refund before any of the services have been provided, we need to ensure that we do not recognize revenue until it has been earned. While it is nice to receive funding before you have performed the services, in essence, all you have received when you get the money is a liability (unearned service revenue), with the hope of it eventually becoming revenue. The following journal entries are built upon the client receiving all three treatments. First, for the prepayment of future services and for the revenue earned in 2019, the journal entries are shown.

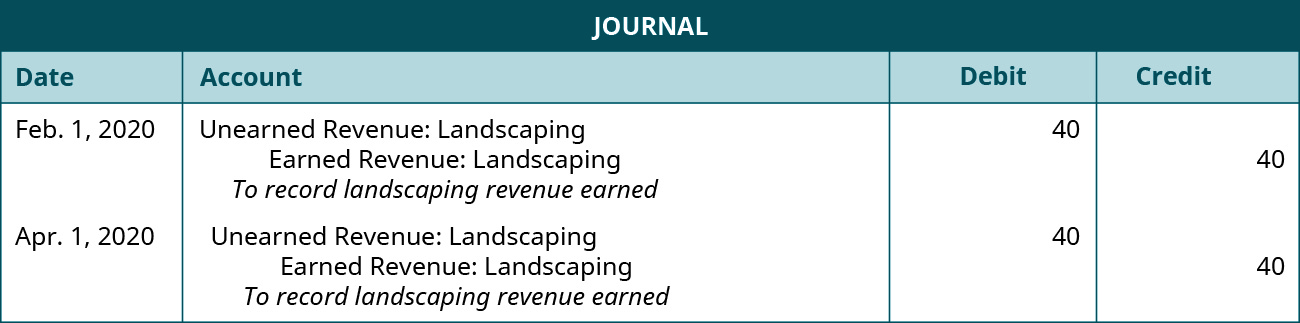

For the revenue earned in 2020, the journal entries would be.

CONCEPTS IN PRACTICE

When thinking about unearned revenue, consider the example of Amazon.com, Inc. Amazon has a large business portfolio that includes a widening presence in the online product and service space. Amazon has two services in particular that contribute to their unearned revenue account: Amazon Web Services and Prime membership.

According to Business Insider, Amazon had $4.8 billion in unearned revenue recognized in their fourth quarter report (December 2016), with most of that contribution coming from Amazon Web Services.1 This is an increase from prior quarters. The growth is due to larger and longer contracts for web services. The advance payment for web services is transferred to revenue over the term of the contract. The same is true for Prime membership. Amazon receives $99 in advance pay from customers, which is amortized over the twelve-month period of the service agreement. This means that each month, Amazon only recognizes $8.25 per Prime membership payment as earned revenue.

Current Portion of a Note Payable

A note payable is a debt to a lender with specific repayment terms, which can include principal and interest. A note payable has written contractual terms that make it available to sell to another party. The principal on a note refers to the initial borrowed amount, not including interest. In addition to repayment of principal, interest may accrue. Interest is a monetary incentive to the lender, which justifies loan risk.

Let’s review the concept of interest. Interest is an expense that you might pay for the use of someone else’s money. For example, if you have a credit card and you owe a balance at the end of the month it will typically charge you a percentage, such as 1.5% a month (which is the same as 18% annually) on the balance that you owe. Assuming that you owe $400, your interest charge for the month would be $400 × 1.5%, or $6.00. To pay your balance due on your monthly statement would require $406 (the $400 balance due plus the $6 interest expense).

We make one more observation about interest: interest rates are typically quoted in annual terms. For example, if you borrowed money to buy a car, your interest expense might be quoted as 9%. Note that this is an annual rate. If you are making monthly payments, the monthly charge for interest would be 9% divided by twelve, or 0.75% a month. For example, if you borrowed $20,000, and made sixty equal monthly payments, your monthly payment would be $415.17, and your interest expense component of the $415.17 payment would be $150.00. The formula to calculate interest on either an annual or partial-year basis is:

In our example this would be $20,000 × 9% × 1/12 = $150. (Or you can think about the Period of Time this way: $20,000 x 9% = $1,800 interest for a year. $1,800 for a year, divided by 12 months = $150 interest for one month.)

The good news is that for a loan such as our car loan or even a home loan, the loan is typically what is called fully amortizing. At this point, you just need to know that in our case the amount that you owe would go from a balance due of $20,000 down to $0 after the twentieth payment and the part of your $415.17 monthly payment allocated to interest would be less each month. For example, your last (sixtieth) payment would only incur $3.09 in interest, with the remaining payment covering the last of the principle owed. See (Figure) for an exhibit that demonstrates this concept.

CONCEPTS IN PRACTICE

Car loans, mortgages, and education loans have an amortization process to pay down debt. Amortization of a loan requires periodic scheduled payments of principal and interest until the loan is paid in full. Every period, the same payment amount is due, but interest expense is paid first, with the remainder of the payment going toward the principal balance. When a customer first takes out the loan, most of the scheduled payment is made up of interest, and a very small amount goes to reducing the principal balance. Over time, more of the payment goes toward reducing the principal balance rather than interest.

For example, let’s say you take out a car loan in the amount of $10,000. The annual interest rate is 3%, and you are required to make scheduled payments each month in the amount of $400. You first need to determine the monthly interest rate by dividing 3% by twelve months (3%/12), which is 0.25%. The monthly interest rate of 0.25% is multiplied by the outstanding principal balance of $10,000 to get an interest expense of $25. The scheduled payment is $400; therefore, $25 is applied to interest, and the remaining $375 ($400 – $25) is applied to the outstanding principal balance. This leaves an outstanding principal balance of $9,625. Next month, interest expense is computed using the new principal balance outstanding of $9,625. The new interest expense is $24.06 ($9,625 × 0.25%). This means $24.06 of the $400 payment applies to interest, and the remaining $375.94 ($400 – $24.06) is applied to the outstanding principal balance to get a new balance of $9,249.06 ($9,625 – $375.94). These computations occur until the entire principal balance is paid in full.

A note payable is usually classified as a long-term (noncurrent) liability if the note period is longer than one year or the standard operating period of the company. However, during the company’s current operating period, any portion of the long-term note due that will be paid in the current period is considered a current portion of a note payable. The outstanding balance note payable during the current period remains a noncurrent note payable. Note that this does not include the interest portion of the payments. On the balance sheet, the current portion of the noncurrent liability is separated from the remaining noncurrent liability. No journal entry is required for this distinction, but some companies choose to show the transfer from a noncurrent liability to a current liability.

For example, a bakery company may need to take out a $100,000 loan to continue business operations. The bakery’s outstanding note principal is $100,000. Terms of the loan require equal annual principal repayments of $10,000 for the next ten years. Payments will be made on July 1 of each of the ten years. Even though the overall $100,000 note payable is considered long term, the $10,000 required repayment during the company’s operating cycle is considered current (short term). This means $10,000 would be classified as the current portion of a noncurrent note payable, and the remaining $90,000 would remain a noncurrent note payable.

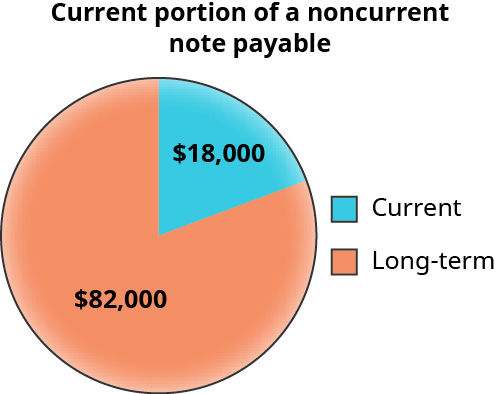

The portion of a note payable due in the current period is recognized as current, while the remaining outstanding balance is a noncurrent note payable. For example, (Figure) shows that $18,000 of a $100,000 note payable is scheduled to be paid within the current period (typically within one year). The remaining $82,000 is considered a long-term liability and will be paid over its remaining life.

In addition to the $18,000 portion of the note payable that will be paid in the current year, any accrued interest on both the current portion and the long-term portion of the note payable that is due will also be paid. Assume, for example, that for the current year $7,000 of interest will be accrued. In the current year the debtor will pay a total of $25,000—that is, $7,000 in interest and $18,000 for the current portion of the note payable. A similar type of payment will be paid each year for as long as any of the note payable remains; however, the annual interest expense would be reduced since the remaining note payable owed will be reduced by the previous payments.

Interest payable can also be a current liability if accrual of interest occurs during the operating period but has yet to be paid. An annual interest rate is established as part of the loan terms. Interest accrued is recorded in Interest Payable (a credit) and Interest Expense (a debit). To calculate interest, the company can use the following equations. This method assumes a twelve-month denominator in the calculation, which means that we are using the calculation method based on a 360-day year. This method was more commonly used prior to the ability to do the calculations using calculators or computers, because the calculation was easier to perform. However, with today’s technology, it is more common to see the interest calculation performed using a 365-day year. We will demonstrate both methods.

For example, we assume the bakery has an annual interest rate on its loan of 7%. The loan interest began accruing on July 1 and it is now December 31. The bakery has accrued six months of interest and would compute the interest liability as

The $3,500 is recognized in Interest Payable (a credit) and Interest Expense (a debit).

Taxes Payable

Taxes payable refers to a liability created when a company collects taxes on behalf of employees and customers or for tax obligations owed by the company, such as sales taxes or income taxes. A future payment to a government agency is required for the amount collected. Some examples of taxes payable include sales tax and income taxes.

Sales taxes result from sales of products or services to customers. A percentage of the sale is charged to the customer to cover the tax obligation (see (Figure)). The sales tax rate varies by state and local municipalities but can range anywhere from 1.76% to almost 10% of the gross sales price. Some states do not have sales tax because they want to encourage consumer spending. Those businesses subject to sales taxation hold the sales tax in the Sales Tax Payable account until payment is due to the governing body.

For example, assume that each time a shoe store sells a $50 pair of shoes, it will charge the customer a sales tax of 8% of the sales price. The shoe store collects a total of $54 from the customer. The $4 sales tax is a current liability until distributed within the company’s operating period to the government authority collecting sales tax.

LINK TO LEARNING

Income taxes are required to be withheld from an employee’s salary for payment to a federal, state, or local authority (hence they are known as withholding taxes). This withholding is a percentage of the employee’s gross pay. Income taxes are discussed in greater detail in Record Transactions Incurred in Preparing Payroll.

Businesses can use the Internal Revenue Service’s Sales Tax Deduction Calculator and associated tips and guidance to determine their estimated sales tax obligation owed to the state and local government authority.

KEY TAKEAWAYS

Key Concepts and Summary

- Current liabilities are debts or obligations that arise from past business activities and are due for payment within a company’s operating period (one year). Common examples of current liabilities include accounts payable, unearned revenue, the current portion of a noncurrent note payable, and taxes payable.

- Accounts payable is used to record purchases from suppliers on credit. Accounts payable typically does not include interest payments.

- Unearned revenue is recorded when customers pay in advance for products or services before receiving their benefits. The company maintains the liability until services or products are rendered.

- Notes payable is a debt to a lender with specific repayment terms, which can include principal and interest. Interest accrued can be computed with the annual interest rate, principal loan amount, and portion of the year accrued.

- Employers withhold taxes from employees and customers for payment to government agencies at a later date, but within the business operating period. Common taxes are sales tax and federal, state, and local income taxes.

Footnotes

- 1Eugene Kim. “An Overlooked Part of Amazon Will Be in the Spotlight When the Company Reports Earnings.” Business Insider. April 28, 2016. https://www.businessinsider.com/amazon-unearned-revenue-growth-shows-why-it-spent-more-on-shipping-last-quarter-2016-4

Glossary

- account payable

- account for financial obligations to suppliers after purchasing products or services on credit

- current liability

- debt or obligation due within one year or, in rare cases, a company’s standard operating cycle, whichever is greater

- current portion of a note payable

- portion of a long-term note due during the company’s current operating period

- interest

- monetary incentive to the lender, which justifies loan risk; interest is paid to the lender by the borrower

- note payable

- legal document between a borrower and a lender specifying terms of a financial arrangement; in most situations, the debt is long-term

- principal

- initial borrowed amount of a loan, not including interest; also, face value or maturity value of a bond (the amount to be paid at maturity)

- taxes payable

- liability created when a company collects taxes on behalf of employees and customers

- unearned revenue

- advance payment for a product or service that has yet to be provided by the company; the transaction is a liability until the product or service is provided

Adapted from Principles of Accounting, Volume 1: Financial Accounting (c) 2010 by Open Stax. The textbook content was produced by Open Stax and is licensed under a Creative Commons BY-NC-SA 4.0 license. Download for free at https://openstax.org/details/books/principles-financial-accounting

same as "short-term liability" -- liability typically expected to be paid within one year or less

an amount owed for the value of goods or services purchased that will be paid at a later date

business receives cash before providing services or goods; the transaction is a liability until the service or goods are provided

legal document between a borrower and a lender specifying terms of a financial arrangement; in most situations, the debt is long-term

initial borrowed amount of a loan, not including interest; also, face value or maturity value of a bond (the amount to be paid at maturity)

monetary incentive to the lender, which justifies loan risk; interest is paid to the lender by the borrower

portion of a long-term note due during the company’s current operating period

liability created when a company collects taxes on behalf of employees and customers